|

市场调查报告书

商品编码

1936590

大型燃气涡轮机市场机会、成长要素、产业趋势分析及2026年至2035年预测Heavy Duty Gas Turbine Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

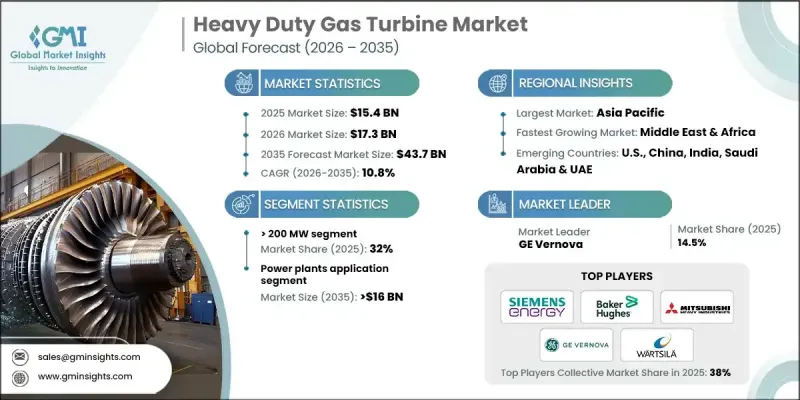

全球大型燃气涡轮机市场预计到 2025 年将达到 154 亿美元,到 2035 年将达到 437 亿美元,年复合成长率为 10.8%。

全球电力消耗量不断增长,加之逐步向低排放量发电转型,持续推动先进燃气涡轮机解决方案的需求。各国政府和电力公司在取代老旧基础设施、提升电网性能的同时,也日益依赖燃气发电作为过渡能源来源。大型燃气涡轮机是高度工程化的电力系统,旨在提供稳定、高运转率和长寿命的电力输出。这些燃气涡轮机透过先进的系统整合、精密的燃烧控制和精确的空气动力学设计,最大限度地提升了热性能。它们能够在严苛的工况下可靠运行,同时具备满足电网负载波动所需的运行柔软性。其适应多种燃料路径的能力在不断发展的能源策略中变得日益重要。随着电力系统向高效高性能转型,大型燃气涡轮机仍然是现代发电投资的核心,为能源安全和长期永续性目标提供支援。

| 市场覆盖范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 154亿美元 |

| 预测金额 | 437亿美元 |

| 复合年增长率 | 10.8% |

预计到2025年,200兆瓦以上机组的市占率将达到32%,并在2035年之前以10.5%的复合年增长率成长。该细分市场的成长得益于不断增长的电力需求、日益严格的能源效率要求以及长期脱碳目标。电力公司越来越倾向于选择容量更大的燃气涡轮机,因为这些燃气涡轮机能够提供更高的运作柔软性、更佳的输出效率和更优化的系统性能,同时也能满足不断变化的环境要求。

预计到2025年,石油和天然气产业的大型燃气涡轮机市场规模将达到23亿美元。这些燃气涡轮机在能源生产、运输和加工过程中发挥至关重要的作用,满足持续的机械驱动和发电需求。由于偏远地区和恶劣运作环境下对可靠性能的需求,市场对燃气涡轮机的需求仍然强劲。营运商优先考虑的是燃气涡轮机的耐用性、更长的维护週期、连续运转下的稳定效率以及符合日益严格的排放法规。

预计2025年,美国大型燃气涡轮机市场规模将达26亿美元,占74%的市场。不断增长的电力需求、基础设施更新以及长期排放目标正在推动市场成长。电力公司持续投资于高性能发电设备,这些设备具有运作柔软性、电网稳定性和成本效益,从而巩固了美国在区域市场的主导地位。

目录

第一章调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 原物料供应及采购分析

- 製造能力评估

- 供应链韧性与风险因素

- 配电网路分析

- 监管环境

- 产业影响因素

- 司机

- 产业潜在风险与挑战

- 成长潜力分析

- 波特五力分析

- PESTEL 分析

- 大型燃气涡轮机的成本结构分析

- 价格趋势分析(美元/兆瓦)

- 按地区

- 按产能

- 新机会与科技趋势

- 投资环境及未来前景

- 数位转型与产业4.0融合

- 永续性措施与脱碳策略

第四章 竞争情势

- 介绍

- 按地区分類的公司市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 中东和非洲

- 拉丁美洲

- 战略仪錶板

- 策略倡议

- 重要伙伴关係与合作

- 重大併购活动

- 产品创新与新产品发布

- 市场扩大策略

- 竞争标竿分析

- 创新与永续性格局

第五章 依产能分類的市场规模及预测(2022-2035年)

- 50千瓦或以下

- 50千瓦至500千瓦

- 500千瓦至1兆瓦以上

- 1兆瓦以上~30兆瓦

- 30兆瓦~70兆瓦

- 70兆瓦~200兆瓦

- 超过200兆瓦

第六章 依技术分類的市场规模及预测(2022-2035年)

- 开环

- 复合循环

第七章 依应用领域分類的市场规模及预测(2022-2035年)

- 发电厂

- 石油和天然气

- 加工厂

- 航空领域

- 船

- 其他的

第八章 2022-2035年各地区市场规模及预测

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 英国

- 法国

- 德国

- 俄罗斯

- 义大利

- 荷兰

- 芬兰

- 希腊

- 丹麦

- 罗马尼亚

- 波兰

- 瑞典

- 亚太地区

- 中国

- 澳洲

- 日本

- 印度

- 韩国

- 印尼

- 泰国

- 马来西亚

- 孟加拉

- 中东和非洲

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 卡达

- 科威特

- 阿曼

- 埃及

- 土耳其

- 巴林

- 伊拉克

- 约旦

- 黎巴嫩

- 南非

- 奈及利亚

- 阿尔及利亚

- 肯亚

- 迦纳

- 拉丁美洲

- 巴西

- 阿根廷

- 秘鲁

第九章:公司简介

- Ansaldo Energia

- Baker Hughes

- Boldrocchi

- Bharat Heavy Electricals

- Capstone Green Energy

- Centrax Gas Turbines

- Destinus Energy

- Doosan Enerbility

- Ethos Energy Group

- Flex Energy Solutions

- GE Vernova

- Harbin Electric

- Kawasaki Heavy Industries

- MAN Energy Solutions

- Mitsubishi Heavy Industries

- Nanjing Steam Turbine Motor

- Rolls Royce

- Siemens Energy

- Shanghai Electric Gas Turbine

- Solar Turbines

- Vericor

- Wartsila

The Global Heavy Duty Gas Turbine Market was valued at USD 15.4 billion in 2025 and is estimated to grow at a CAGR of 10.8% to reach USD 43.7 billion by 2035.

Rising global electricity consumption, combined with the gradual shift toward lower-emission power generation, continues to support demand for advanced gas turbine solutions. Governments and power producers increasingly rely on gas-based generation as a transitional energy source while upgrading aging infrastructure and improving grid performance. Heavy duty gas turbines represent highly engineered power systems developed to deliver consistent output, high availability, and long operational life. These turbines are designed to maximize thermal performance through advanced system integration, refined combustion control, and precision-driven aerodynamic design. They operate reliably under demanding conditions while providing the operational flexibility required to respond to fluctuating grid loads. Their ability to accommodate multiple fuel pathways further strengthens their relevance within evolving energy strategies. As power systems become more efficiency-driven and performance-focused, heavy duty gas turbines remain central to modern power generation investments, supporting both energy security and long-term sustainability goals.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $15.4 Billion |

| Forecast Value | $43.7 Billion |

| CAGR | 10.8% |

The segment rated above 200 MW accounted for 32% share in 2025 and is expected to grow at a CAGR of 10.5% through 2035. Growth in this segment is supported by rising power demand, stricter efficiency expectations, and long-term decarbonization objectives. Utilities increasingly favor large-capacity turbines that offer operational flexibility, improved output efficiency, and enhanced system optimization while maintaining compliance with evolving environmental requirements.

The oil & gas heavy duty gas turbine segment generated USD 2.3 billion in 2025. These turbines play a critical role across energy production, transportation, and processing operations by supporting continuous mechanical drive and power generation needs. Demand remains strong due to the requirement for dependable performance in remote locations and challenging operating environments. Operators emphasize durability, extended service intervals, consistent efficiency under continuous operation, and adherence to increasingly stringent emissions regulations.

US Heavy Duty Gas Turbine Market accounted for 74% share and generated USD 2.6 billion in 2025. Market growth is supported by increasing electricity requirements, infrastructure upgrades, and long-term emissions reduction targets. Utilities continue to invest in high-efficiency power generation assets that offer operational flexibility, grid stability, and cost-effective performance, reinforcing the country's leadership position within the regional market.

Major companies operating in the Global Heavy Duty Gas Turbine Market include Siemens Energy, Mitsubishi Heavy Industries, GE Vernova, Ansaldo Energia, Baker Hughes, Rolls Royce, Wartsila, MAN Energy Solutions, Doosan Enerbility, Kawasaki Heavy Industries, Shanghai Electric Gas Turbine, Harbin Electric, Bharat Heavy Electricals, Solar Turbines, Vericor, Ethos Energy Group, Flex Energy Solutions, Centrax Gas Turbines, Boldrocchi, Nanjing Steam Turbine Motor, Capstone Green Energy, and Destinus Energy. Companies operating in the heavy duty gas turbine market focus on strengthening their market position through continuous performance improvement, lifecycle optimization, and technology differentiation. Many invest heavily in efficiency enhancement, emissions reduction capabilities, and long-term reliability to meet evolving utility and industrial requirements. Strategic partnerships with utilities and energy developers support early-stage project integration and recurring service contracts. Firms also prioritize digitalization to improve asset monitoring, maintenance planning, and operational transparency.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Market estimates & forecasts parameters

- 1.8 Forecast model

- 1.8.1 Quantified market impact analysis

- 1.8.1.1 Mathematical impact of growth parameters on forecast

- 1.8.1 Quantified market impact analysis

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

- 1.10 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.1.1 Business trends

- 2.1.2 Capacity trends

- 2.1.3 Technology trends

- 2.1.4 Application trends

- 2.1.5 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Manufacturing capacity assessment

- 3.1.3 Supply chain resilience & risk factors

- 3.1.4 Distribution network analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Cost structure analysis of heavy duty gas turbines

- 3.8 Price trend analysis (USD/MW)

- 3.8.1 By region

- 3.8.2 By capacity

- 3.9 Emerging opportunities & technological trends

- 3.10 Investment landscape & future prospects

- 3.11 Digital transformation & industry 4.0 integration

- 3.12 Sustainability initiatives & decarbonization strategies

Chapter 4 Competitive Landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Strategic dashboard

- 4.4 Strategic initiatives

- 4.4.1 Key partnerships & collaborations

- 4.4.2 Major M&A activities

- 4.4.3 Product innovations & launches

- 4.4.4 Market expansion strategies

- 4.5 Competitive benchmarking

- 4.6 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Capacity, 2022 - 2035 (USD Million & MW)

- 5.1 Key trends

- 5.2 ≤ 50 kW

- 5.3 > 50 kW to 500 kW

- 5.4 > 500 kW to 1 MW

- 5.5 > 1 MW to 30 MW

- 5.6 > 30 MW to 70 MW

- 5.7 > 70 MW to 200 MW

- 5.8 > 200 MW

Chapter 6 Market Size and Forecast, By Technology, 2022 - 2035 (USD Million & MW)

- 6.1 Key trends

- 6.2 Open cycle

- 6.3 Combined cycle

Chapter 7 Market Size and Forecast, By Application, 2022 - 2035 (USD Million & MW)

- 7.1 Key trends

- 7.2 Power plants

- 7.3 Oil & gas

- 7.4 Process plants

- 7.5 Aviation

- 7.6 Marine

- 7.7 Others

Chapter 8 Market Size and Forecast, By Region, 2022 - 2035 (USD Million & MW)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.2.3 Mexico

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 France

- 8.3.3 Germany

- 8.3.4 Russia

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.3.7 Finland

- 8.3.8 Greece

- 8.3.9 Denmark

- 8.3.10 Romania

- 8.3.11 Poland

- 8.3.12 Sweden

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Australia

- 8.4.3 Japan

- 8.4.4 India

- 8.4.5 South Korea

- 8.4.6 Indonesia

- 8.4.7 Thailand

- 8.4.8 Malaysia

- 8.4.9 Bangladesh

- 8.5 Middle East & Africa

- 8.5.1 Saudi Arabia

- 8.5.2 UAE

- 8.5.3 Qatar

- 8.5.4 Kuwait

- 8.5.5 Oman

- 8.5.6 Egypt

- 8.5.7 Turkey

- 8.5.8 Bahrain

- 8.5.9 Iraq

- 8.5.10 Jordan

- 8.5.11 Lebanon

- 8.5.12 South Africa

- 8.5.13 Nigeria

- 8.5.14 Algeria

- 8.5.15 Kenya

- 8.5.16 Ghana

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Argentina

- 8.6.3 Peru

Chapter 9 Company Profiles

- 9.1 Ansaldo Energia

- 9.2 Baker Hughes

- 9.3 Boldrocchi

- 9.4 Bharat Heavy Electricals

- 9.5 Capstone Green Energy

- 9.6 Centrax Gas Turbines

- 9.7 Destinus Energy

- 9.8 Doosan Enerbility

- 9.9 Ethos Energy Group

- 9.10 Flex Energy Solutions

- 9.11 GE Vernova

- 9.12 Harbin Electric

- 9.13 Kawasaki Heavy Industries

- 9.14 MAN Energy Solutions

- 9.15 Mitsubishi Heavy Industries

- 9.16 Nanjing Steam Turbine Motor

- 9.17 Rolls Royce

- 9.18 Siemens Energy

- 9.19 Shanghai Electric Gas Turbine

- 9.20 Solar Turbines

- 9.21 Vericor

- 9.22 Wartsila

全球大型燃气涡轮机市场规模、份额、趋势和成长分析报告:2026-2034年

全球大型燃气涡轮机市场规模、份额、趋势和成长分析报告:2026-2034年 重型燃气涡轮机机服务市场规模、份额和成长分析(按服务类型、应用、涡轮机、最终用户产业、零件和地区划分)-2026-2033年产业预测

重型燃气涡轮机机服务市场规模、份额和成长分析(按服务类型、应用、涡轮机、最终用户产业、零件和地区划分)-2026-2033年产业预测 大型燃气涡轮机市场规模、份额和成长分析(按燃料类型、功率输出、应用、涡轮机类型和地区划分)-2026-2033年产业预测

大型燃气涡轮机市场规模、份额和成长分析(按燃料类型、功率输出、应用、涡轮机类型和地区划分)-2026-2033年产业预测 全球重型燃气涡轮机服务市场全球重型燃气涡轮机市场

全球重型燃气涡轮机服务市场全球重型燃气涡轮机市场 发电厂重型燃气涡轮机市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

发电厂重型燃气涡轮机市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测 到 2030 年大型燃气涡轮机服务市场预测:按服务类型、涡轮机容量、涡轮机类型、最终用户和地区进行的全球分析

到 2030 年大型燃气涡轮机服务市场预测:按服务类型、涡轮机容量、涡轮机类型、最终用户和地区进行的全球分析