|

市场调查报告书

商品编码

1959584

食品机器人市场:机会、成长要素、产业趋势分析及2026年至2035年预测Food Robotics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

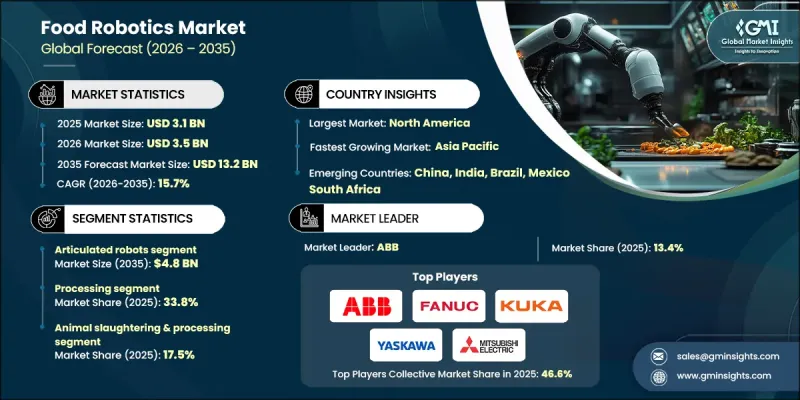

2025 年全球食品机器人市场价值 31 亿美元,预计到 2035 年将达到 132 亿美元,年复合成长率为 15.7%。

劳动力短缺、对生鲜食品精准处理的需求不断增长以及加工食品和即食食品消费量上升是推动该行业成长的主要因素。快速的都市化和消费者生活方式的改变,促使人们对便利食品的需求日益增长,进而促使企业投资高速自动化加工、分类和包装设备。食品机器人技术正从固定式、单任务机器发展为配备人工智慧和机器视觉的智慧系统。这使得系统能够即时适应原材料的波动,而无需进行大量的重新编程。目前,能够管理从生产到包装整个流程的端到端机器人解决方案正在广泛应用,在降低营运成本的同时,提高了效率、食品安全和卫生水平。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 31亿美元 |

| 预测金额 | 132亿美元 |

| 复合年增长率 | 15.7% |

2025年,Delta/并联机器人市场规模预计为7.558亿美元,并预计到2035年将以17.2%的复合年增长率增长。由于其精准性、快速反应以及能够最大限度地减少对易碎食品的损伤,这些机器人越来越多地应用于高速取放作业。在生鲜食品、糖果甜点和烘焙食品等易碎产品处理方面的应用,正在推动其在自动化食品环境中的普及。

预计到2025年,加工产业将占据33.8%的市场。人工智慧机器人正越来越多地应用于重复性、高风险和劳动密集任务,例如食品的切割、分装、混合和组装。它们的应用提高了生产的一致性、卫生标准和整体营运效率,同时减少了人与危险作业的接触。这一趋势正在加速大型食品製造和包装设施对机器人的应用。

预计到2025年,北美食品机器人市占率将达到36%。该地区拥有先进的製造业基础设施、高昂的人事费用以及严格的食品安全法规,因此自动化已成为战略性必然选择。北美在肉类、乳製品、烘焙和包装食品行业中引领机器人技术的应用,利用机器人技术优化生产、减少对劳动力的依赖,并确保符合严格的卫生和品质标准。早期采用机器人技术使该地区成为人工智慧整合食品自动化技术的领导者。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率分析

- 成本结构

- 每个阶段增加的价值

- 影响价值链的因素

- 中断

- 影响产业的因素

- 促进因素

- 食品加工和包装产业自动化应用的扩展

- 监管压力加大了对可追溯性和品质合规性的要求

- 加工食品和速食消费量增加

- 智慧工厂的扩展和工业4.0的引入

- 劳动力严重短缺,以及对生鲜食品。

- 产业潜在风险与挑战

- 高昂的初始资本投入与实施成本

- 技术复杂性与整合挑战

- 市场机会

- 即食食品和加工食品领域的扩张

- 人工智慧和机器视觉在机器人领域的应用日益广泛

- 促进因素

- 监理情势

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL 分析

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 新兴经营模式

- 合规要求

- 专利和智慧财产权分析

- 地缘政治和贸易趋势

第四章 竞争情势

- 介绍

- 企业市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 按地区

- 主要企业的竞争标竿分析

- 财务绩效比较

- 收入

- 利润率

- 研究与开发

- 产品系列比较

- 产品线的广度

- 科技

- 创新

- 区域扩张比较

- 全球扩张分析

- 服务网路覆盖

- 按地区分類的市场渗透率

- 竞争定位矩阵

- 领导企业

- 受让人

- 追踪者

- 小众玩家

- 战略展望矩阵

- 财务绩效比较

- 2021-2024 年重大发展

- 併购

- 合作伙伴关係和合资企业

- 技术进步

- 扩张和投资策略

- 数位转型计划

- 新兴/Start-Ups竞争对手的发展趋势

第五章 市场估价与预测:依机器人类型划分,2022-2035年

- 联合机器人

- SCARA机器人

- Delta/并联机器人

- 笛卡儿机器人/龙门机器人

- 协作机器人(cobots)

- 其他的

第六章 市场估计与预测:依功能划分,2022-2035年

- 加工

- 包装

- 码垛和卸垛

- 检验和品管

- 物料输送与物流

- 其他的

第七章 市场估计与预测:依最终用途划分,2022-2035年

- 动物饲料生产

- 谷物和油籽加工

- 糖和糖果甜点

- 水果和蔬菜的保藏和加工

- 乳製品生产

- 肉类加工

- 水产品加工

- 麵包房和玉米饼生产

- 其他的

第八章 市场估计与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第九章:公司简介

- 主要企业

- ABB

- FANUC

- KUKA

- Yaskawa Electric

- 按地区分類的主要企业

- 北美洲

- Rockwell Automation

- Key Technology(Duravant)

- Miso Robotics

- 欧洲

- Universal Robots

- Staubli

- Buhler Group

- 亚太地区

- Mitsubishi Electric

- OMRON

- Nachi-Fujikoshi

- 北美洲

- 特殊玩家/干扰者

- Mayekawa

- Marel

The Global Food Robotics Market was valued at USD 3.1 billion in 2025 and is estimated to grow at a CAGR of 15.7% to reach USD 13.2 billion by 2035.

The industry's growth is driven by labor shortages, increasing demand for precise handling of perishable products, and the rising consumption of processed and ready-to-eat foods. Rapid urbanization and changing consumer lifestyles are increasing demand for convenience foods, prompting companies to invest in high-speed automation for processing, sorting, and packaging. Food robotics is evolving from fixed, single-task machines to intelligent systems equipped with AI and machine vision, capable of adapting in real time to variations in ingredients without extensive reprogramming. End-to-end robotic solutions are now being deployed to manage the entire production and packaging workflow, improving efficiency, food safety, and hygiene while reducing operational costs.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $3.1 Billion |

| Forecast Value | $13.2 Billion |

| CAGR | 15.7% |

The delta/parallel robots segment was valued at USD 755.8 million in 2025 and is forecasted to grow at a CAGR of 17.2% through 2035. These robots are increasingly utilized for high-speed pick-and-place operations due to their precision, rapid response, and ability to handle delicate food items with minimal damage. Their application in sensitive product handling such as fresh produce, confectionery, and bakery items is driving adoption in automated food environments.

The processing segment accounted for 33.8% share in 2025. AI-enabled robots are increasingly being used in repetitive, high-risk, and labor-intensive operations such as cutting, portioning, mixing, and assembling food products. Their deployment enhances production consistency, hygiene standards, and overall operational efficiency, while also reducing human exposure to potentially hazardous tasks. This trend is accelerating adoption across large-scale food manufacturing and packaging facilities.

North America Food Robotics Market held a 36% share in 2025. The region benefits from advanced manufacturing infrastructure, high labor costs, and strict food safety regulations, making automation a strategic necessity. North America leads adoption in meat, dairy, bakery, and packaged food sectors, leveraging robotics to optimize production, reduce labor dependency, and maintain compliance with stringent hygiene and quality standards. Early adoption of robotics has positioned the region as a trendsetter in AI-integrated food automation technologies.

Key players in the Global Food Robotics Market include ABB, FANUC, KUKA, Yaskawa Electric, Mitsubishi Electric, Universal Robots, OMRON, and Staubli. Companies in the Food Robotics Market are implementing strategies to strengthen their market position by investing in AI-driven automation, machine vision, and adaptive robotics capable of handling diverse food items in real time. They are forming strategic alliances with food manufacturers and integrators to enable faster deployment and ensure compatibility with existing production lines. Product diversification, including robotic solutions for packaging, processing, and material handling, allows companies to address multiple food segments. Expansion into emerging markets with rising automation demand is a key growth tactic. Additionally, continuous R&D to improve speed, precision, and hygiene compliance ensures that firms maintain a competitive edge and meet evolving regulatory standards while supporting scalable production.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Robot type trends

- 2.2.2 Function trends

- 2.2.3 End-use application trends

- 2.2.4 Regional trends

- 2.3 TAM analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising automation adoption in food processing and packaging

- 3.2.1.2 Regulatory pressure for traceability and quality compliance

- 3.2.1.3 Increasing consumption of processed and ready-to-eat foods

- 3.2.1.4 Expansion of smart factories and Industry 4.0 adoption

- 3.2.1.5 Acute labor shortages and the need for gentle, high-precision handling of perishable produce

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial capital investment and implementation costs

- 3.2.2.2 Technical complexity and integration challenges

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion in ready-to-eat and processed food segments

- 3.2.3.2 Growing adoption of AI and machine vision in robotics

- 3.2.1 Growth drivers

- 3.3 Regulatory landscape

- 3.3.1 North America

- 3.3.2 Europe

- 3.3.3 Asia Pacific

- 3.3.4 Latin America

- 3.3.5 Middle East & Africa

- 3.4 Porter’s analysis

- 3.5 PESTEL analysis

- 3.6 Technology and innovation landscape

- 3.6.1 Current technological trends

- 3.6.2 Emerging technologies

- 3.7 Emerging business models

- 3.8 Compliance requirements

- 3.9 Patent and IP analysis

- 3.10 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Robot Type, 2022 - 2035 ($ Mn & Units)

- 5.1 Key trends

- 5.2 Articulated robots

- 5.3 Scara robots

- 5.4 Delta/parallel robots

- 5.5 Cartesian/gantry robots

- 5.6 Collaborative robots (cobots)

- 5.7 Others

Chapter 6 Market Estimates and Forecast, By Function, 2022 - 2035 ($ Mn & Units)

- 6.1 Key trends

- 6.2 Processing

- 6.3 Packaging

- 6.4 Palletizing & depalletizing

- 6.5 Inspection & quality control

- 6.6 Material handling & logistics

- 6.7 Others

Chapter 7 Market Estimates and Forecast, By End-use Application, 2022 - 2035 ($ Mn & Units)

- 7.1 Key trends

- 7.2 Animal food manufacturing

- 7.3 Grain & oilseed milling

- 7.4 Sugar & confectionery

- 7.5 Fruit & vegetable preserving

- 7.6 Dairy product manufacturing

- 7.7 Animal slaughtering & processing

- 7.8 Seafood product preparation

- 7.9 Bakeries & tortilla manufacturing

- 7.10 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn & Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Global Key Players

- 9.1.1 ABB

- 9.1.2 FANUC

- 9.1.3 KUKA

- 9.1.4 Yaskawa Electric

- 9.2 Regional Key Players

- 9.2.1 North America

- 9.2.1.1 Rockwell Automation

- 9.2.1.2 Key Technology (Duravant)

- 9.2.1.3 Miso Robotics

- 9.2.2 Europe

- 9.2.2.1 Universal Robots

- 9.2.2.2 Staubli

- 9.2.2.3 Buhler Group

- 9.2.3 APAC

- 9.2.3.1 Mitsubishi Electric

- 9.2.3.2 OMRON

- 9.2.3.3 Nachi-Fujikoshi

- 9.2.1 North America

- 9.3 Niche Players / Disruptors

- 9.3.1 Mayekawa

- 9.3.2 Marel

食品机器人市场:机器人类型、酬载能力、运作模式、应用及最终用途-2026-2032年全球市场预测

食品机器人市场:机器人类型、酬载能力、运作模式、应用及最终用途-2026-2032年全球市场预测 食品服务机器人市场预测至 2034 年:按机器人类型、自主程度、移动方式、组件、功能、部署模式、最终用户和地区进行全球分析。全自动豆腐凝固机市场:依机器类型、产能、自动化程度、价格范围、最终用户、通路划分,全球预测(2026-2032年)工业柑橘加工设备市场:按设备类型、最终产品、产能、技术和运作模式划分,全球预测(2026-2032年)

食品服务机器人市场预测至 2034 年:按机器人类型、自主程度、移动方式、组件、功能、部署模式、最终用户和地区进行全球分析。全自动豆腐凝固机市场:依机器类型、产能、自动化程度、价格范围、最终用户、通路划分,全球预测(2026-2032年)工业柑橘加工设备市场:按设备类型、最终产品、产能、技术和运作模式划分,全球预测(2026-2032年) 食品机器人市场规模、份额、趋势及预测(按类型、有效载荷、应用和地区划分)(2026-2034 年)

食品机器人市场规模、份额、趋势及预测(按类型、有效载荷、应用和地区划分)(2026-2034 年) 餐厅机器人市场按类型、应用和地区划分

餐厅机器人市场按类型、应用和地区划分 2026年全球食品机器人市场报告

2026年全球食品机器人市场报告 全球机器人服务员市场2032 年食品机器人市场预测:按类型、有效载荷容量、应用、最终用户和地区进行的全球分析2032 年食品机器人市场预测:按机器人类型、有效载荷、组件、应用、最终用户和地区进行的全球分析

全球机器人服务员市场2032 年食品机器人市场预测:按类型、有效载荷容量、应用、最终用户和地区进行的全球分析2032 年食品机器人市场预测:按机器人类型、有效载荷、组件、应用、最终用户和地区进行的全球分析