|

市场调查报告书

商品编码

1959588

现场可程式闸阵列(FPGA) 市场机会、成长要素、产业趋势分析及 2026 年至 2035 年预测Field Programmable Gate Array (FPGA) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

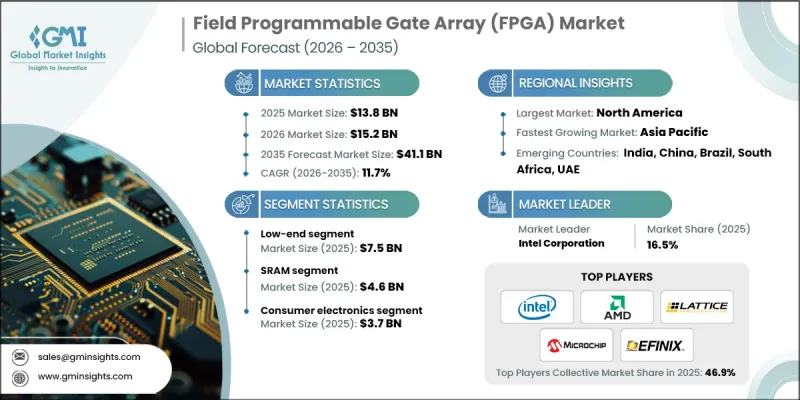

2025 年全球现场可程式闸阵列(FPGA) 市场价值为 138 亿美元,预计到 2035 年将达到 411 亿美元,复合年增长率为 11.7%。

市场成长的驱动力来自人工智慧 (AI) 和机器学习的广泛应用、5G 和下一代通讯基础设施的快速部署、先进汽车电子和高级驾驶辅助系统 (ADAS) 的日益普及,以及工业自动化、智慧製造、边缘运算和物联网 (IoT) 设备的激增。世界各国政府的政策日益重视促进人工智慧领域的创新,增强战略竞争力,并支持人才培育。公共部门对人工智慧研究的投资正在强化技术生态系统,使私营和公共机构都能利用灵活的高效能运算平台来处理动态工作负载。下一代行动网路的持续扩展推动了对具有先进讯号处理和自适应能力的可程式逻辑装置的需求,进一步扩大了 FPGA 技术的市场机会。这些趋势的融合为多个终端应用领域的长期成长奠定了坚实的基础。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 138亿美元 |

| 预测金额 | 411亿美元 |

| 复合年增长率 | 11.7% |

预计2025年,低端FPGA市场规模将达到75亿美元,成为推动市场成长的主要动力。这主要得益于家用电子电器、基础工业控制和物联网终端对高性价比可程式解决方案的需求不断增长。这些装置无需自订ASIC晶片,即可提供设计柔软性,从而避免了相关的成本和复杂性,使其成为需要可扩展和可重构硬体的应用的首选。政府为促进数位基础设施和电子製造业发展而推出的各项倡议,正在加速入门级FPGA装置的普及,进一步推动该细分市场的成长。

预计到2025年,基于SRAM的FPGA市场规模将达到46亿美元。凭藉高逻辑密度、卓越性能和可程式设计等优势,SRAM FPGA在人工智慧加速、资料中心运维、通讯基础设施以及需要频繁硬体更新的应用领域至关重要。汽车、工业和通讯系统对快速原型製作和部署后配置变更的需求日益增长,进一步推动了基于SRAM的FPGA的普及。製造商正在扩展其SRAM FPGA产品线,整合高频宽记忆体、增强安全性并配备先进的开发工具链,以满足高效能灵活运算应用的需求。

预计到2025年,北美现场可程式闸阵列(FPGA)市场份额将达到36.3%,凭藉主导地位。该地区受益于公共和私人对5G、人工智慧和国防相关FPGA应用领域的投资,以及产业界和学术研究中心之间的合作。先进的製造能力和高技能的劳动力使得FPGA能够无缝整合到云端基础设施、嵌入式系统和通讯网路中,从而将北美打造成为可程式逻辑技术的全球创新中心。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 成本结构

- 每个阶段增加的价值

- 影响价值链的因素

- 中断

- 影响产业的因素

- 促进因素

- 人工智慧和机器学习简介

- 5G和下一代通讯基础设施

- 汽车电子和ADAS的发展

- 工业自动化和智慧製造

- 边缘运算和物联网的扩展

- 挑战与困难

- 程式设计复杂度

- 先进FPGA高成本

- 促进因素

- 成长潜力分析

- 监管环境

- 波特五力分析

- PESTEL 分析

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 新兴经营模式

- 合规要求

- 永续发展倡议

- 供应链韧性

- 地缘政治分析

- 数位转型

第四章 竞争情势

- 介绍

- 企业市占率分析

- 按地区

- 市场集中度分析

- 主要企业的竞争标竿分析

- 产品系列比较

- 产品线的广度

- 科技

- 创新

- 地理位置比较

- 全球扩张分析

- 服务网路覆盖

- 按地区分類的市场渗透率

- 竞争定位矩阵

- 领导企业

- 受让人

- 追踪者

- 小众玩家

- 战略展望矩阵

- 产品系列比较

- 2022-2025 年重大发展

- 併购

- 伙伴关係与合作

- 技术进步

- 扩张和投资策略

- 永续发展倡议

- 数位转型计划

- 新兴/Start-Ups竞争对手的发展趋势

第五章 市场估计与预测:依类型划分,2022-2035年

- 低阶

- 中檔

- 高阶

第六章 市场估计与预测:依技术划分,2022-2035年

- SRAM

- EEPROM

- 耐熔熔丝

- 快闪记忆体

- 其他的

第七章 市场估计与预测:依应用领域划分,2022-2035年

- 主要趋势

- 家用电子电器

- 车

- 工业的

- 资料处理

- 军事/航太

- 沟通

- 其他的

第八章 市场估计与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿拉伯聯合大公国

第九章:公司简介

- 主要企业

- Advanced Micro Devices, Inc.

- Intel Corporation

- Lattice Semiconductor Corporation

- Microchip Technology Inc.

- 按地区分類的主要企业

- 北美洲

- Achronix Semiconductor Corporation

- Efinix, Inc.

- Flex Logix Technologies, Inc.

- Quicklogic Corporation

- 欧洲

- Cologne Chip AG

- Enclustra GmbH

- Menta SAS

- NanoXplore

- 亚太地区

- Gowin Semiconductor Corp.

- Renesas Electronics Corporation

- Cyient DLM

- 北美洲

- 小众/颠覆性公司

- Trenz Electronic GmbH

The Global Field Programmable Gate Array (FPGA) Market was valued at USD 13.8 billion in 2025 and is estimated to grow at a CAGR of 11.7% to reach USD 41.1 billion by 2035.

The market's growth is fueled by widespread adoption of artificial intelligence (AI) and machine learning, rapid deployment of 5G and next-generation telecommunication infrastructure, the rising use of advanced automotive electronics and ADAS systems, industrial automation, smart manufacturing, and the proliferation of edge computing and IoT devices. Governmental policies worldwide are increasingly focused on fostering innovation in AI, promoting strategic competitiveness, and supporting workforce training. Public investment in AI research strengthens the technological ecosystem, enabling both private and public organizations to leverage flexible, high-performance computing platforms capable of handling dynamic workloads. The ongoing expansion of next-generation mobile networks drives demand for programmable logic devices capable of sophisticated signal processing and adaptive performance, further enhancing market opportunities for FPGA technologies. The convergence of these trends is creating a strong foundation for long-term growth across multiple end-use sectors.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $13.8 Billion |

| Forecast Value | $41.1 Billion |

| CAGR | 11.7% |

The low-end FPGA segment generated USD 7.5 billion in 2025, leading the market due to rising demand for cost-effective programmable solutions in consumer electronics, basic industrial controls, and IoT endpoints. These devices provide design flexibility without the cost and complexity associated with custom ASICs, making them a preferred choice for applications requiring scalable, reconfigurable hardware. Government initiatives promoting digital infrastructure and electronics manufacturing are accelerating the adoption of entry-level FPGA devices, further boosting segment growth.

The SRAM-based FPGAs segment reached USD 4.6 billion in 2025. Their dominance is driven by high logic density, superior performance, and reprogrammability, making them essential for AI acceleration, data center operations, telecom infrastructure, and applications requiring frequent hardware updates. Increasing demand for rapid prototyping and post-deployment configuration across automotive, industrial, and communication systems continues to reinforce SRAM-based FPGA adoption. Manufacturers are enhancing SRAM FPGA offerings with integrated high-bandwidth memory, improved security, and advanced development toolchains to meet the needs of performance-critical and flexible computing applications.

North America Field Programmable Gate Array (FPGA) Market accounted for 36.3% share in 2025, maintaining a leadership position due to a robust semiconductor ecosystem, early adoption of AI and automotive electronics, and a strong presence of hyperscale data centers. The region benefits from significant public and private investment in 5G, AI, and defense-related FPGA applications, supported by collaborations between industry and academic research centers. Advanced manufacturing capabilities and a highly skilled workforce enable seamless FPGA integration across cloud infrastructure, embedded systems, and communication networks, establishing North America as a global innovation hub for programmable logic technologies.

Key players shaping the Global Field Programmable Gate Array (FPGA) Market include Lattice Semiconductor Corporation, Intel Corporation, Achronix Semiconductor Corporation, Efinix, Inc., Microchip Technology Inc., Quicklogic Corporation, Renesas Electronics Corporation, Advanced Micro Devices, Inc., Flex Logix Technologies, Inc., Gowin Semiconductor Corp., Menta S.A.S., Enclustra GmbH, Trenz Electronic GmbH, Cyient DLM, and Cologne Chip AG. Companies in the Field Programmable Gate Array (FPGA) Market are adopting strategies to strengthen their market presence through continuous innovation and portfolio expansion. Firms are investing heavily in research and development to introduce high-performance, reconfigurable hardware optimized for AI, telecom, automotive, and industrial applications. Strategic collaborations and licensing agreements expand geographic reach and enable access to emerging markets. Emphasis on advanced toolchains, security features, and high-bandwidth memory integration ensures differentiation in performance-critical applications. Many companies are enhancing production capabilities and establishing localized support networks to improve customer service and reduce time-to-market.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Type trends

- 2.2.2 Technology trends

- 2.2.3 Application trends

- 2.2.4 Regional trends

- 2.3 TAM Analysis, 2026-2035 (USD Million)

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 AI and machine learning adoption

- 3.2.1.2 5G and next-generation telecom infrastructure

- 3.2.1.3 Automotive electronics and ADAS growth

- 3.2.1.4 Industrial automation and smart manufacturing

- 3.2.1.5 Edge computing and IoT expansion

- 3.2.2 Pitfalls and challenges

- 3.2.2.1 Programming complexity

- 3.2.2.2 High cost of advanced FPGAs

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Emerging Business Models

- 3.9 Compliance Requirements

- 3.10 Sustainability Initiatives

- 3.11 Supply Chain Resilience

- 3.12 Geopolitical Analysis

- 3.13 Digital Transformation

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Product portfolio comparison

- 4.3.1.1 Product range breadth

- 4.3.1.2 Technology

- 4.3.1.3 Innovation

- 4.3.2 Geographic presence comparison

- 4.3.2.1 Global footprint analysis

- 4.3.2.2 Service network coverage

- 4.3.2.3 Market penetration by region

- 4.3.3 Competitive positioning matrix

- 4.3.3.1 Leaders

- 4.3.3.2 Challengers

- 4.3.3.3 Followers

- 4.3.3.4 Niche players

- 4.3.4 Strategic outlook matrix

- 4.3.1 Product portfolio comparison

- 4.4 Key developments, 2022-2025

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Low-end

- 5.3 Mid-range

- 5.4 High-end

Chapter 6 Market Estimates and Forecast, By Technology, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 SRAM

- 6.3 EEPROM

- 6.4 Antifuse

- 6.5 Flash

- 6.6 Others

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million)

- 7.1 Key Trends

- 7.2 Consumer Electronics

- 7.3 Automotive

- 7.4 Industrial

- 7.5 Data Processing

- 7.6 Military & Aerospace

- 7.7 Telecom

- 7.8 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Global Key Players

- 9.1.1 Advanced Micro Devices, Inc.

- 9.1.2 Intel Corporation

- 9.1.3 Lattice Semiconductor Corporation

- 9.1.4 Microchip Technology Inc.

- 9.2 Regional Key Players

- 9.2.1 North America

- 9.2.1.1 Achronix Semiconductor Corporation

- 9.2.1.2 Efinix, Inc.

- 9.2.1.3 Flex Logix Technologies, Inc.

- 9.2.1.4 Quicklogic Corporation

- 9.2.2 Europe

- 9.2.2.1 Cologne Chip AG

- 9.2.2.2 Enclustra GmbH

- 9.2.2.3 Menta S.A.S.

- 9.2.2.4 NanoXplore

- 9.2.3 Asia Pacific

- 9.2.3.1 Gowin Semiconductor Corp.

- 9.2.3.2 Renesas Electronics Corporation

- 9.2.3.3 Cyient DLM

- 9.2.1 North America

- 9.3 Niche / Disruptors

- 9.3.1 Trenz Electronic GmbH

现场可程式闸阵列 (FPGA) 市场:2026-2032 年全球市场预测(按配置类型、节点尺寸、技术、架构、处理器类型和应用划分)FPGA 安全市场:按技术类型、整合、威胁类型和应用划分 - 2026-2032 年全球市场预测

现场可程式闸阵列 (FPGA) 市场:2026-2032 年全球市场预测(按配置类型、节点尺寸、技术、架构、处理器类型和应用划分)FPGA 安全市场:按技术类型、整合、威胁类型和应用划分 - 2026-2032 年全球市场预测 2026年全球现场可程式闸阵列市场报告

2026年全球现场可程式闸阵列市场报告 全球FPGA(现场可程式闸阵列)市场:按节点尺寸、应用、逻辑密度、装置类型、国家和地区划分-产业分析、市场规模、份额和预测(2025-2032年)

全球FPGA(现场可程式闸阵列)市场:按节点尺寸、应用、逻辑密度、装置类型、国家和地区划分-产业分析、市场规模、份额和预测(2025-2032年) FPGA市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、形状、材料类型、最终用户及部署方式划分2026年嵌入式现场可程式闸阵列(FPGA)全球市场报告

FPGA市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、形状、材料类型、最终用户及部署方式划分2026年嵌入式现场可程式闸阵列(FPGA)全球市场报告 现场可程式闸阵列市场 - 全球产业规模、份额、趋势、机会及预测(按技术、应用、配置、垂直产业、地区和竞争格局划分,2021-2031年)

现场可程式闸阵列市场 - 全球产业规模、份额、趋势、机会及预测(按技术、应用、配置、垂直产业、地区和竞争格局划分,2021-2031年) FPGA 安全市场 - 2026-2031 年预测

FPGA 安全市场 - 2026-2031 年预测 现场可程式闸阵列(FPGA)-市场占有率分析、产业趋势与统计、成长预测(2026-2031)

现场可程式闸阵列(FPGA)-市场占有率分析、产业趋势与统计、成长预测(2026-2031) FPGA加速市场预测至2032年:全球分析,依架构、结构类型、介面类型、应用、最终用户及地区划分

FPGA加速市场预测至2032年:全球分析,依架构、结构类型、介面类型、应用、最终用户及地区划分