|

市场调查报告书

商品编码

1959596

露营家具市场机会、成长要素、产业趋势分析及2026年至2035年预测Camping Furniture Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

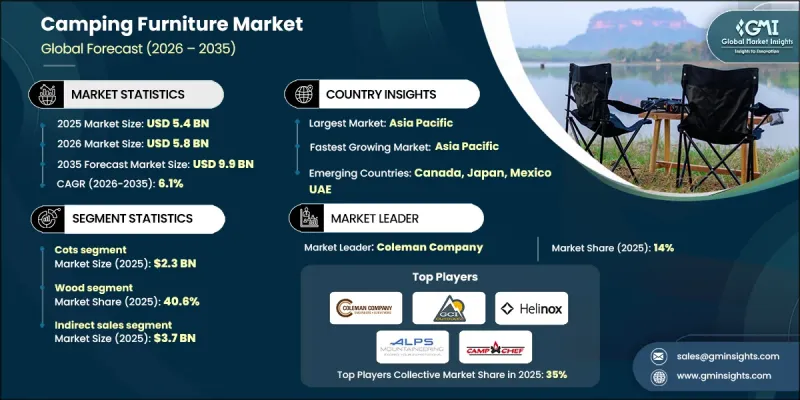

2025 年全球露营家具市场价值 54 亿美元,预计到 2035 年将达到 99 亿美元,年复合成长率为 6.1%。

市场成长的驱动力在于人们对户外休閒和亲近大自然的休閒活动日益浓厚的兴趣。都市区的压力、长时间的萤幕使用以及远距办公的普及,促使越来越多的人寻求与家人朋友一起短暂亲近大自然,例如週末露营、公路旅行和野餐。露营已从一项以冒险为中心的爱好发展成为一项主流休閒活动,受到都市区家庭、露营新手和户外爱好者的青睐,从而为露营装备创造了更广泛的客户群。这种转变推动了对便携、适合临时使用且功能齐全的户外家具的需求,这些家具能够提升舒适性和易用性。露营家具在支持人们参与户外活动方面发挥着至关重要的作用,它使消费者能够轻鬆地从入门级的基本装备过渡到更高级的户外生活环境,从而鼓励重复购买和长期参与。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 54亿美元 |

| 预测金额 | 99亿美元 |

| 复合年增长率 | 6.1% |

预计到2025年,便携式床市场规模将达到23亿美元,成为最受欢迎的露营家具之一。便携式床能让露营者远离地面,隔绝寒冷的地面,改善通风,提升舒适度。这些特点使其尤其受到家庭、自驾露营者和老年人的青睐,他们更倾向于选择支撑性更强、使用更便捷的睡眠解决方案,而非简约型床。便携式床的便利性、耐用性和舒适性使其成为追求高品质露营体验且不愿牺牲易用性的露营者的必备之选。

预计到2025年,木製家具市占率将达到40.6%。木材兼具美观性和功能性,是桌子、储物柜、长凳和豪华露营床等对刚性和稳定性要求极高的家具的理想材料。与金属和塑胶相比,木材给人温暖自然的感受,吸引追求更精緻露营环境的消费者。凭藉其耐用性、设计多样性和视觉吸引力,木材预计将在露营家具市场(从入门级到高端系列)保持热销地位。

预计到2025年,美国露营家具市占率将达到89%。美国市场高度发达,深受包括自驾露营和户外活动在内的浓厚休閒文化的影响。消费者在选择露营家具时,越来越重视舒适性、便携性、功能性和美观性。从折迭式椅到豪华露营床和组合桌,对各种露营家具的需求反映了消费者多样化的偏好以及家庭露营和户外休閒的持续增长。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 每个阶段增加的价值

- 影响价值链的因素

- 影响产业的因素

- 促进因素

- 过渡到户外活动

- 对户外环境舒适度的需求

- 国内旅行增加

- 产业潜在风险与挑战

- 市场区隔程度高,价格竞争激烈

- 强烈的季节性和需求波动

- 机会

- 多功能混合家具

- 模组化和节省空间的设计

- 促进因素

- 成长潜力分析

- 未来市场趋势

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 副产品

- 监管环境

- 标准和合规要求

- 区域法规结构

- 认证标准

- 波特五力分析

- PESTEL 分析

第四章 竞争情势

- 介绍

- 企业市占率分析

- 按地区

- 公司矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 主要进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章 市场估价与预测:依产品划分,2022-2035年

- 椅子和凳子

- 桌子

- 婴儿床

- 吊床

- 其他的

第六章 市场估计与预测:依材料划分,2022-2035年

- 金属

- 木头

- 塑胶

- 纤维

- 其他的

第七章 市场估计与预测:依价格区间划分,2022-2035年

- 低价位

- 中价位

- 高价位范围

第八章 市场估算与预测:依通路划分,2022-2035年

- 线下超级市场/专卖店/其他(百货公司等)/线上/电子商务/企业网站

- 超级市场

- 专卖店

- 其他(百货公司等)

- 在线的

- 电子商务

- 公司网站

第九章 市场估计与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第十章:公司简介

- ALPS Mountaineering

- Big Agnes

- Camp Chef

- Coleman Company

- GCI Outdoor

- Helinox

- Kampa

- Kelty

- Kijaro

- Lippert

- NEMO Equipment

- Outwell

- QuikShade

- Snow Peak

- Vango

The Global Camping Furniture Market was valued at USD 5.4 billion in 2025 and is estimated to grow at a CAGR of 6.1% to reach USD 9.9 billion by 2035.

The market growth is driven by a rising interest in outdoor recreation and nature-focused leisure activities. Urban stress, prolonged screen exposure, and the expansion of remote work arrangements are motivating individuals to seek short-term escapes into nature with family and friends, including weekend camping, road trips, and picnicking. Camping has evolved from an adventure-focused pastime into a mainstream leisure activity embraced by urban families, first-time campers, and casual outdoor enthusiasts, creating a broader audience for camping products. This shift is generating increasing demand for portable, temporary, and functional outdoor furniture that enhances comfort and usability. Camping furniture plays a vital role in supporting participation, offering consumers a seamless transition from basic entry-level setups to more sophisticated outdoor living arrangements, encouraging repeat purchases and long-term engagement.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $5.4 Billion |

| Forecast Value | $9.9 Billion |

| CAGR | 6.1% |

In 2025, the cots segment generated USD 2.3 billion, becoming one of the most sought-after camping furniture items. Cots elevate campers above the ground, offering insulation from cold surfaces, better airflow, and enhanced comfort. These features make them particularly attractive for family campers, car campers, and older adults who prefer supportive and easy-to-use sleeping solutions rather than minimalistic options. The convenience, durability, and comfort of cots have made them a staple for those seeking a premium camping experience without compromising on usability.

The wooden furniture segment held 40.6% share in 2025. Wood provides a blend of aesthetic appeal and functional strength, making it an ideal material for tables, storage units, benches, and high-end cots where rigidity and stability are essential. Compared to metal or plastic, wood offers a warmer and more natural look, which attracts consumers desiring a more elegant camping setup. Its combination of durability, design versatility, and visual appeal ensures its continued popularity in both entry-level and premium camping furniture lines.

U.S. Camping Furniture Market accounted for 89% share in 2025. The market in the U.S. is highly developed and influenced by a strong culture of recreational activities, including car-based camping and outdoor events. Consumers place increasing importance on comfort, portability, functionality, and aesthetics when selecting camping furniture. The demand spans a wide spectrum of products, from folding chairs to premium cots and modular tables, reflecting diverse consumer preferences and the continued expansion of family-oriented camping and outdoor leisure.

Leading companies in the Global Camping Furniture Market include Camp Chef, Big Agnes, QuikShade, NEMO Equipment, Coleman Company, Helinox, Vango, Lippert, Outwell, Kampa, ALPS Mountaineering, Kijaro, Kelty, GCI Outdoor, and Snow Peak. Key strategies adopted by companies in the camping furniture market focus on innovation, product differentiation, and expanding consumer reach. Firms are developing lightweight, portable, and multi-functional furniture to appeal to casual and family campers. They invest in premium designs using materials such as wood, aluminum, and high-grade fabrics to target upscale segments. Companies leverage online and offline retail channels to enhance accessibility while offering customization options to increase brand loyalty. Marketing efforts emphasize comfort, convenience, and lifestyle appeal, and partnerships with outdoor events, resorts, and recreational service providers strengthen market visibility.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Material

- 2.2.4 Price range

- 2.2.5 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Shift toward outdoor activities

- 3.2.1.2 Demand for comfort in outdoor settings

- 3.2.1.3 Rise in domestic travel

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High market fragmentation & price competition

- 3.2.2.2 Strong seasonality & demand volatility

- 3.2.3 Opportunities

- 3.2.3.1 Multi-use & hybrid furniture

- 3.2.3.2 Modular & space-efficient designs

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By product

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022 - 2035 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Chairs and stools

- 5.3 Tables

- 5.4 Cots

- 5.5 Hammocks

- 5.6 Others

Chapter 6 Market Estimates and Forecast, By Material, 2022 - 2035 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Metal

- 6.3 Wood

- 6.4 Plastic

- 6.5 Textile

- 6.6 Others

Chapter 7 Market Estimates and Forecast, By Price Range, 2022 - 2035 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Low

- 7.3 Medium

- 7.4 High

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.1.1 Offline

- 8.1.1.1 Supermarkets

- 8.1.1.2 Specialty stores

- 8.1.1.3 Others (Departmental stores. Etc.)

- 8.1.2 Online

- 8.1.2.1 E-commerce

- 8.1.2.2 Company websites

- 8.1.1 Offline

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 ALPS Mountaineering

- 10.2 Big Agnes

- 10.3 Camp Chef

- 10.4 Coleman Company

- 10.5 GCI Outdoor

- 10.6 Helinox

- 10.7 Kampa

- 10.8 Kelty

- 10.9 Kijaro

- 10.10 Lippert

- 10.11 NEMO Equipment

- 10.12 Outwell

- 10.13 QuikShade

- 10.14 Snow Peak

- 10.15 Vango

房车市场:2026-2032年全球市场预测(按房车类型、销售管道和应用划分)露营厨房市场:2026-2032年全球市场预测(按产品类型、燃料类型、价格范围、活动类型、材料类型、分销管道和最终用户划分)露营椅市场:2026-2032年全球市场预测(依产品类型、材料、价格范围、承重能力、销售管道及最终用户划分)露营冷藏箱市场:全球市场按产品类型、容量、材料、应用和销售管道分類的预测 - 2026-2032 年露营和房车市场:2026-2032年全球市场预测(按露营方式、产品类型、活动、最终用户和分销管道划分)

房车市场:2026-2032年全球市场预测(按房车类型、销售管道和应用划分)露营厨房市场:2026-2032年全球市场预测(按产品类型、燃料类型、价格范围、活动类型、材料类型、分销管道和最终用户划分)露营椅市场:2026-2032年全球市场预测(依产品类型、材料、价格范围、承重能力、销售管道及最终用户划分)露营冷藏箱市场:全球市场按产品类型、容量、材料、应用和销售管道分類的预测 - 2026-2032 年露营和房车市场:2026-2032年全球市场预测(按露营方式、产品类型、活动、最终用户和分销管道划分) 露营装备市场规模、份额、趋势和预测:按产品类型、分销管道和地区划分,2026-2034年

露营装备市场规模、份额、趋势和预测:按产品类型、分销管道和地区划分,2026-2034年 露营装备市场机会、成长要素、产业趋势分析及2026年至2035年预测

露营装备市场机会、成长要素、产业趋势分析及2026年至2035年预测 露营冷藏箱市场 - 全球产业规模、份额、趋势、机会、预测:按类型、材料、产能、应用、地区和竞争格局划分,2021-2031年露营房车市场 - 全球产业规模、份额、趋势、机会、预测:按类型、房车类型、年龄层、地区和竞争格局划分,2021-2031年露营装备市场-全球产业规模、份额、趋势、机会及预测(依产品类型、应用、通路、地区及竞争格局划分,2021-2031年)

露营冷藏箱市场 - 全球产业规模、份额、趋势、机会、预测:按类型、材料、产能、应用、地区和竞争格局划分,2021-2031年露营房车市场 - 全球产业规模、份额、趋势、机会、预测:按类型、房车类型、年龄层、地区和竞争格局划分,2021-2031年露营装备市场-全球产业规模、份额、趋势、机会及预测(依产品类型、应用、通路、地区及竞争格局划分,2021-2031年)