|

市场调查报告书

商品编码

1959623

宠物食品包装市场机会、成长要素、产业趋势分析及2026年至2035年预测Pet Food Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

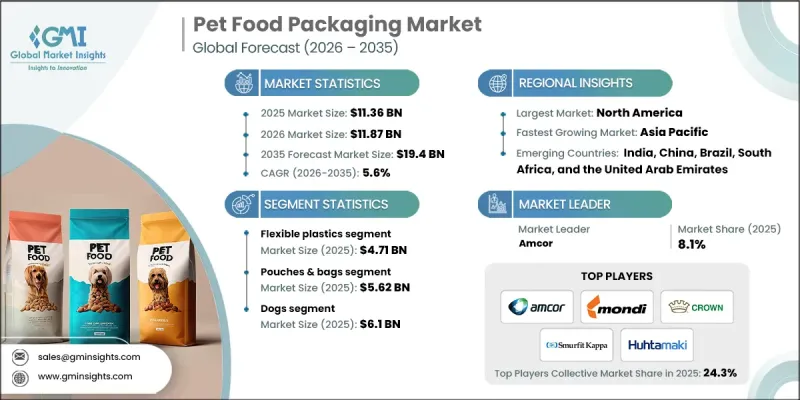

2025 年全球宠物食品包装市场价值为 113.6 亿美元,预计到 2035 年将达到 194 亿美元,年复合成长率为 5.6%。

随着宠物数量的增加,宠物食品的需求也随之成长,市场稳定扩张。消费者对高级产品、有机和已烹调宠物食品的偏好日益增长,推动了对能够确保新鲜度、安全性和便利性的先进包装的需求。电子商务和线上零售通路的快速发展,也增加了对耐用、轻巧且易于运输的包装的需求。永续性成为关键因素,越来越多的品牌正在寻求可回收、可生物降解和单一材料的包装解决方案,以实现循环经济目标。此外,儘管支持永续材料的法规结构仍在不断完善,但优质化趋势正在推动创新设计,以吸引具有环保意识的宠物饲主,这使得全球市场竞争激烈,创新主导。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 113.6亿美元 |

| 预测金额 | 194亿美元 |

| 复合年增长率 | 5.6% |

预计到2025年,软塑胶市场规模将达到47.1亿美元。随着食品接触材料监管的日益严格以及循环经济模式的兴起,市场对可再生软塑胶的需求不断增长。製造商正致力于生产符合欧盟不断完善的回收标准,同时又能吸引环保意识强的消费者的再生和单一材料柔软性塑胶。柔性包装因其耐用性、轻盈性和较长的保质期,是干、湿和半湿宠物食品的理想包装选择。透过采用永续实践,企业既可以满足监管要求,又能提升其在环保意识强的消费者群体中的品牌形象。

预计到2025年,袋装产品市场规模将达到56.2亿美元。单一材料可回收包装袋的普及,主要受可回收性监管压力和消费者对环保包装需求的推动。企业正以符合法律回收标准并能减少废弃物的单一材料替代品取代多材料薄膜。消费者对可重复密封的单份包装袋的需求不断增长,这与消费者对便利性、电商配送和份量控制的需求相契合,使得这种包装形式对寻求差异化竞争优势的宠物食品品牌越来越有吸引力。

预计到2025年,北美宠物食品包装市占率将达到41.6%。该地区正经历强劲成长,这主要得益于消费者对便利性、优质化和永续包装的需求。为了适应快节奏的生活方式和线上销售,可重复密封袋、单份包装袋和易于配送的包装正逐渐成为标准配置。醒目吸睛的设计,能够传递品质和新鲜感,正越来越多地被用于在商店中区分产品。随着永续性意识的增强,生产者延伸责任法规和回收义务正在影响包装的选择。因此,企业正在采用既能保持视觉吸引力和功能性,又能满足监管标准和消费者期望的环保解决方案。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 成本结构

- 每个阶段增加的价值

- 影响价值链的因素

- 中断

- 影响产业的因素

- 促进因素

- 宠物拥有率和饲养率上升

- 对优质有机宠物食品的需求不断增长

- 拓展电子商务与线上零售通路

- 永续环保包装的创新

- 扩大即食型和便利型宠物食品的供应

- 挑战与困难

- 先进包装材料高成本

- 严格的监管标准和合规要求

- 促进因素

- 成长潜力分析

- 监管环境

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL 分析

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 新兴经营模式

- 合规要求

- 永续性措施

- 永续材料评价

- 碳足迹分析

- 引入循环经济

- 永续性认证和标准

- 永续性投资报酬率分析

- 全球消费者态度分析

- 专利分析

第四章 竞争情势

- 介绍

- 企业市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 市场集中度分析

- 按地区

- 主要企业的竞争标竿分析

- 产品系列比较

- 产品线广度

- 科技

- 创新

- 区域扩张比较

- 全球扩张分析

- 服务网路覆盖

- 按地区分類的市场渗透率

- 竞争定位矩阵

- 领导企业

- 受让人

- 追踪者

- 小众玩家

- 战略展望矩阵

- 产品系列比较

- 2022-2025 年重大发展

- 併购

- 合作伙伴关係和合资企业

- 技术进步

- 扩张和投资策略

- 永续发展倡议

- 数位转型计划

- 新兴/Start-Ups竞争对手的发展趋势

第五章 市场估算与预测:依材料类型划分,2022-2035年

- 软质塑胶

- 硬质塑胶

- 金属

- 纸张和纸板

- 其他的

第六章 市场估价与预测:依包装类型划分,2022-2035年

- 小袋和袋子

- 能

- 纸箱/盒子

- 瓶子和罐子

- 托盘和容器

- 其他的

第七章 市场估价与预测:依宠物食品类型划分,2022-2035年

- 主要趋势

- 干粮

- 湿粮

- 点心

- 其他的

第八章 市场估算与预测:依宠物类型划分,2022-2035年

- 主要趋势

- 狗

- 猫

- 鸟类

- 鱼

- 其他的

第九章 市场估价与预测:依通路划分,2022-2035年

- 主要趋势

- 在线的

- 离线

第十章 市场估价与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿拉伯聯合大公国

第十一章:公司简介

- 主要企业

- Amcor

- Sealed Air

- Huhtamaki

- Tetra Pak

- Sonoco

- 按地区分類的主要企业

- 北美洲

- Packaging Corporation of America

- Winpak

- Crown Holdings

- Ball Corporation

- 欧洲

- Mondi

- Smurfit Kappa

- Constantia Flexibles

- Coveris

- 北美洲

- 小众/颠覆性公司

- ProAmpac

The Global Pet Food Packaging Market was valued at USD 11.36 billion in 2025 and is estimated to grow at a CAGR of 5.6% to reach USD 19.4 billion in 2035.

The market is expanding steadily as rising pet adoption and ownership drive higher demand for pet food products. Increasing consumer preference for premium, organic, and ready-to-eat pet foods is fueling demand for advanced packaging solutions that ensure freshness, safety, and convenience. The rapid growth of e-commerce and online retail channels has amplified the need for packaging that is durable, lightweight, and easy to ship. Sustainability is becoming a major factor, with brands seeking recyclable, biodegradable, and mono-material packaging solutions to meet circular economy goals. Additionally, regulatory frameworks are evolving to support sustainable materials, while premiumization trends encourage innovative designs that appeal to conscious pet owners, making the market highly competitive and innovation-driven globally.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $11.36 Billion |

| Forecast Value | $19.4 Billion |

| CAGR | 5.6% |

The flexible plastics segment reached USD 4.71 billion in 2025. Demand for recyclable flexible plastics is rising as governments implement stricter regulations for food-contact materials and circular economy compliance. Manufacturers are increasingly focusing on producing recycled and mono-material flexible plastics that meet evolving EU recyclability standards while appealing to sustainability-conscious consumers. Flexible packaging provides durability, lightweight handling, and extended shelf life, making it ideal for dry, wet, and semi-moist pet food products. By adopting sustainable practices, companies can both comply with regulations and strengthen brand perception among environmentally aware customers.

The pouches and bags segment reached USD 5.62 billion in 2025. The shift toward mono-material recyclable pouches is driven by regulatory pressure on recyclability and consumer demand for environmentally responsible packaging. Companies are replacing multi-material films with single-material alternatives that satisfy legal recycling thresholds and reduce waste. The growing preference for resealable and single-serve pouches aligns with consumer convenience, e-commerce delivery, and portion control needs, making this format increasingly attractive to pet food brands seeking competitive differentiation.

North America Pet Food Packaging Market accounted for 41.6% share in 2025. The region is witnessing strong growth due to consumer demand for convenience, premiumization, and sustainable packaging. Resealable bags, single-serve pouches, and easy-to-ship formats are becoming standard to accommodate busy lifestyles and online sales. Bold, eye-catching designs that convey quality and freshness are increasingly used to differentiate products on shelves. Awareness of sustainability is rising, with extended producer responsibility regulations and recyclability mandates shaping packaging choices. As a result, companies are adopting eco-friendly solutions while maintaining visual appeal and functionality to satisfy both regulatory standards and consumer expectations.

Key players operating in the Global Pet Food Packaging Market include Huhtamaki, Amcor, Ball Corporation, Mondi, Sealed Air, Crown Holdings, Smurfit Kappa, ProAmpac, Constantia Flexibles, Tetra Pak, Coveris, Winpak, and Packaging Corporation of America. Companies in the pet food packaging market are adopting several strategies to enhance their market presence and strengthen their foothold. They are investing heavily in research and development to create sustainable, recyclable, and biodegradable packaging that meets evolving regulatory standards. Partnerships with pet food manufacturers and converters enable tailored solutions and faster adoption of innovative formats. Companies are also expanding production capacities and distribution networks to ensure timely supply to e-commerce and retail channels. Brand differentiation is achieved through high-quality, visually appealing designs that communicate freshness and premium value.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Material type trends

- 2.2.2 Packaging format trends

- 2.2.3 Pet food type trends

- 2.2.4 Pet type trends

- 2.2.5 Distribution channel trends

- 2.2.6 Regional trends

- 2.3 TAM Analysis, 2026-2035 (USD Million)

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising pet adoption and ownership

- 3.2.1.2 Increasing demand for premium and organic pet food

- 3.2.1.3 Growing e-commerce and online retail channels

- 3.2.1.4 Innovations in sustainable and eco-friendly packaging

- 3.2.1.5 Expansion of ready-to-eat and convenient pet food products

- 3.2.2 Pitfalls and challenges

- 3.2.2.1 High cost of advanced packaging materials

- 3.2.2.2 Stringent regulatory standards and compliance requirements

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Emerging Business Models

- 3.9 Compliance Requirements

- 3.10 Sustainability Measures

- 3.10.1 Sustainable Materials Assessment

- 3.10.2 Carbon Footprint Analysis

- 3.10.3 Circular Economy Implementation

- 3.10.4 Sustainability Certifications and Standards

- 3.10.5 Sustainability ROI Analysis

- 3.11 Global Consumer Sentiment Analysis

- 3.12 Patent Analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Product portfolio comparison

- 4.3.1.1 Product range breadth

- 4.3.1.2 Technology

- 4.3.1.3 Innovation

- 4.3.2 Geographic presence comparison

- 4.3.2.1 Global footprint analysis

- 4.3.2.2 Service network coverage

- 4.3.2.3 Market penetration by region

- 4.3.3 Competitive positioning matrix

- 4.3.3.1 Leaders

- 4.3.3.2 Challengers

- 4.3.3.3 Followers

- 4.3.3.4 Niche players

- 4.3.4 Strategic outlook matrix

- 4.3.1 Product portfolio comparison

- 4.4 Key developments, 2022-2025

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Material Type, 2022 - 2035 (USD Million & Kilo Tons)

- 5.1 Key trends

- 5.2 Flexible plastics

- 5.3 Rigid plastics

- 5.4 Metal

- 5.5 Paper & paperboard

- 5.6 Others

Chapter 6 Market Estimates and Forecast, By Packaging Type, 2022 - 2035 (USD Million & Kilo Tons)

- 6.1 Key trends

- 6.2 Pouches & bags

- 6.3 Cans

- 6.4 Cartons & boxes

- 6.5 Bottles & jars

- 6.6 Trays & tubs

- 6.7 Others

Chapter 7 Market Estimates and Forecast, By Pet Food Type, 2022 - 2035 (USD Million & Kilo Tons)

- 7.1 Key Trends

- 7.2 Dry food

- 7.3 Wet food

- 7.4 Treats & snacks

- 7.5 Others

Chapter 8 Market Estimates and Forecast, By Pet Type, 2022 - 2035 (USD Million & Kilo Tons)

- 8.1 Key Trends

- 8.2 Dogs

- 8.3 Cats

- 8.4 Birds

- 8.5 Fish

- 8.6 Others

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 (USD Million & Kilo Tons)

- 9.1 Key Trends

- 9.2 Online

- 9.3 Offline

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million & Kilo Tons)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Key Players

- 11.1.1 Amcor

- 11.1.2 Sealed Air

- 11.1.3 Huhtamaki

- 11.1.4 Tetra Pak

- 11.1.5 Sonoco

- 11.2 Regional Key Players

- 11.2.1 North America

- 11.2.1.1 Packaging Corporation of America

- 11.2.1.2 Winpak

- 11.2.1.3 Crown Holdings

- 11.2.1.4 Ball Corporation

- 11.2.2 Europe

- 11.2.2.1 Mondi

- 11.2.2.2 Smurfit Kappa

- 11.2.2.3 Constantia Flexibles

- 11.2.2.4 Coveris

- 11.2.1 North America

- 11.3 Niche / Disruptors

- 11.3.1 ProAmpac

宠物食品包装市场规模、份额、成长及全球产业分析:按类型、应用和地区划分,并预测至2026-2034年全球宠物食品包装市场规模、份额、趋势和成长分析报告(2026-2034年)

宠物食品包装市场规模、份额、成长及全球产业分析:按类型、应用和地区划分,并预测至2026-2034年全球宠物食品包装市场规模、份额、趋势和成长分析报告(2026-2034年) 2026年全球宠物食品包装市场报告宠物食品包装市场-2026-2031年预测

2026年全球宠物食品包装市场报告宠物食品包装市场-2026-2031年预测 宠物食品包装机市场机会、成长动力、产业趋势分析及2025-2034年预测

宠物食品包装机市场机会、成长动力、产业趋势分析及2025-2034年预测 宠物食品包装:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)

宠物食品包装:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年) 宠物食品包装市场规模、份额及成长分析(依材料、产品、食品、动物及地区)-2025-2032 年产业预测美国宠物食品包装:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)

宠物食品包装市场规模、份额及成长分析(依材料、产品、食品、动物及地区)-2025-2032 年产业预测美国宠物食品包装:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年) 宠物食品包装市场报告:2030 年趋势、预测与竞争分析

宠物食品包装市场报告:2030 年趋势、预测与竞争分析