|

市场调查报告书

商品编码

1982281

电动车维护市场机会、成长要素、产业趋势分析及2026-2035年预测EV Maintenance Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

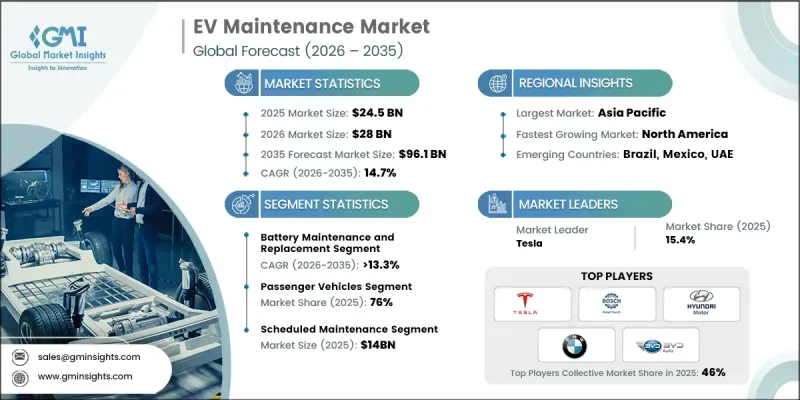

全球电动车维护市场预计到 2025 年将达到 245 亿美元,预计到 2035 年将以 14.7% 的复合年增长率增长至 961 亿美元。

电动车市场扩张的驱动力来自全球电动车的日益普及、车队电气化的推进以及对电池健康维护、提高车辆运转率和合规性日益增长的需求。北美、欧洲和亚太地区政府推行的清洁交通途径、永续性发展和电气化政策及奖励,正促使原始设备製造商 (OEM)、车队营运商和服务供应商为搭乘用和商用电动车实施先进的维护策略和预测性维护解决方案。最大限度地延长电池寿命、提高能源效率和最大限度地减少运作的压力不断增加,推动了对先进电动车维护服务的需求。这些服务包括电池诊断和更换、电机维修、暖通空调和辅助系统检查、空中下载 (OTA) 软体更新以及充电基础设施维护。随着搭乘用电动车、轻型商用车 (LCV) 和中重型商用电动车的日益普及,对专业化、高效且数据驱动的维护系统的需求也日益增长。电池管理系统 (BMS)、利用远端资讯处理技术的预测性维护、即时监控和整合诊断平台等技术创新正在改变电动车服务的提供方式。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测期 | 2026-2035 |

| 上市时的市场规模 | 245亿美元 |

| 预测金额 | 961亿美元 |

| 复合年增长率 | 14.7% |

预计到2025年,电池维护和更换市场将占电动车市场36%的份额,并在2026年至2035年间以13.3%的复合年增长率成长。这个市场之所以主导,是因为电池对电动车的性能、续航里程、能源效率和安全性有着至关重要的影响。由于更换成本高且技术复杂,预计乘用车、轻型商用车以及中重型商用电动车对定期维护和预测性维护的需求将持续成长。

预计到2025年,乘用车市占率将达到76%,并在2035年之前以14.2%的复合年增长率成长。这一细分市场的主导地位主要得益于电动乘用车的日益普及,以及消费者对电池健康、马达可靠性、软体更新和车辆运作的日益重视。汽车製造商和授权服务中心正在加速维修服务的标准化,提供符合保固要求的、数据驱动型服务。中国、欧洲和北美等主要地区对定期维护的需求进一步巩固了乘用车市场的主导地位。

中国电动车维护市场目前占据全球51%的份额,预计2025年市场规模将达到45亿美元。该地区的成长主要得益于电动车的快速普及、强劲的产能以及众多整车製造商、一级供应商和服务供应商的强大实力。政府的奖励、大规模的製造基础设施、高性价比的服务网络以及不断扩展的数位化维护平台,都在推动乘用车和商用车电动车领域的需求成长。凭藉其庞大的电动车产量、先进的电池和电机服务以及整车製造商、车队营运商和数位化服务供应商之间的紧密合作,中国仍然是亚太地区最大的电动车市场。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 成本结构

- 每个阶段增加的价值

- 影响价值链的因素

- 中断

- 影响产业的因素

- 促进因素

- 电动车的快速普及和车队规模的扩张

- 关注电池健康和寿命

- 预测性维护的技术进步

- 监管和政府奖励

- 产业潜在风险与挑战

- 先进维护系统的初始成本较高

- 售后市场分散与技能缺口

- 市场机会

- 拓展商用车和车队服务

- 开发预测性和数据驱动型服务

- 扩大电动车车队规模并引进商用车领域

- 智慧充电与基础设施维护的整合

- 促进因素

- 成长潜力分析

- 监理情势

- 北美洲

- 美国:EPA、CARB、NHTSA 标准

- 加拿大:加拿大运输部,CMVSS 305

- 欧洲

- 德国:BMDV,欧6/7法规

- 法国:运输部,6/7欧元

- 英国:运输部,Euro 6/7

- 义大利:基础设施和运输部加强对排放气体法规的执行力度

- 亚太地区

- 中国:工信部、中国 6/7 标准

- 日本:国土交通省,JIS排放气体法规

- 韩国:国土交通部(MOLIT)、韩国(KS)排放气体标准

- 印度:MoRTH,BS6标准

- 拉丁美洲

- 巴西:DENATRAN、CONAMA 标准

- 墨西哥:通讯与运输部NOM排放气体法规

- 中东和非洲

- 阿联酋:RTA 和 ESMA排放气体法规

- 沙乌地阿拉伯:运输部,SASO排放气体标准

- 北美洲

- 波特五力分析

- PESTEL 分析

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 副产品

- 成本細項分析

- 专利分析

- 永续性和环境方面

- 永续倡议

- 减少废弃物策略

- 生产中的能源效率

- 环保意识的倡议

- 关于碳足迹的考量

- 使用案例场景

- 软体、OTA 和网路安全对电动车维护的影响

- 车队电气化对维修需求模式的影响

第四章 竞争情势

- 介绍

- 企业市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 战略展望矩阵

- 主要进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 业务拓展计划及资金筹措

第五章 市场估计与预测:依维护类别划分,2022-2035年

- 电池维护和更换

- 软体更新和诊断

- 充电基础设施的维护

- 马达的维护和检查

- 暖通空调及辅助系统的维护

第六章 市场估价与预测:依车辆类型划分,2022-2035年

- 搭乘用车

- 掀背车

- 轿车

- SUV

- 商用车辆

- 轻型商用车(LCV)

- 中型商用车(MCV)

- 重型商用车(HCV)

第七章 市场估计与预测:依服务业划分,2022-2035年

- 定期维护

- 预测性保护

- 紧急维修

第八章 市场估算与预测:依最终用途划分,2022-2035年

- 个人电动车车主

- 车主

- 政府和地方政府车辆

- 商业充电网路营运商

第九章 市场估计与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 比利时

- 荷兰

- 瑞典

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 新加坡

- 韩国

- 越南

- 印尼

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲(MEA)

- 阿拉伯聯合大公国

- 南非

- 沙乌地阿拉伯

第十章:公司简介

- Global Player

- BMW

- BYD Auto

- Continental

- DENSO

- Hyundai Motor

- LKQ

- Magna International

- Robert Bosch

- Tesla

- Volkswagen

- Regional Player

- BorgWarner

- CATL Service Solutions

- Cummins

- Eberspacher

- Faurecia

- HJS Emission Technology

- Johnson Matthey

- MANN+HUMMEL

- Tenneco

- Valeo

The Global EV Maintenance Market was valued at USD 24.5 billion in 2025 and is estimated to grow at a CAGR of 14.7% to reach USD 96.1 billion by 2035.

Market expansion is driven by the rising global adoption of EVs, the growth of fleet electrification, and the increasing need to maintain battery health, vehicle uptime, and regulatory compliance. Government policies and incentives promoting clean transportation, sustainability mandates, and electrification across North America, Europe, and Asia-Pacific are encouraging OEMs, fleet operators, and service providers to implement advanced maintenance strategies and predictive servicing solutions for both passenger and commercial electric vehicles. The growing pressure to maximize battery longevity, enhance energy efficiency, and minimize operational downtime is fueling demand for advanced EV maintenance services. These include battery diagnostics and replacement, electric motor servicing, HVAC and auxiliary system inspections, over-the-air (OTA) software updates, and maintenance of charging infrastructure. Increasing adoption of passenger EVs, light commercial vehicles (LCVs), and medium to heavy commercial EVs is driving the need for specialized, high-efficiency, data-driven maintenance systems. Technological innovations such as battery management systems (BMS), telematics-enabled predictive maintenance, real-time monitoring, and integrated diagnostics platforms are transforming traditional EV service approaches.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $24.5 Billion |

| Forecast Value | $96.1 Billion |

| CAGR | 14.7% |

The battery maintenance and replacement segment held 36% share in 2025 and is expected to grow at a CAGR of 13.3% from 2026 to 2035. This segment dominates due to the battery's critical impact on EV performance, range, energy efficiency, and safety. High replacement costs and technical complexity ensure ongoing demand for both scheduled and predictive maintenance across passenger, LCV, and medium/heavy commercial EVs.

The passenger vehicles segment held 76% share in 2025 and is expected to grow at a CAGR of 14.2% through 2035. The dominance of this segment is driven by the widespread adoption of electric passenger cars and the emphasis on battery health, motor reliability, software updates, and vehicle uptime. OEMs and authorized service centers are increasingly standardizing maintenance services, delivering data-driven, warranty-compliant servicing. Recurring maintenance demand across major regions such as China, Europe, and North America reinforces the leadership of the passenger vehicle segment.

China EV Maintenance Market accounted for 51% share, generating USD 4.5 billion in 2025. The region's growth is supported by rapid EV adoption, robust production volumes, and the strong presence of OEMs, Tier-1 suppliers, and service providers. Favorable government incentives, large-scale manufacturing infrastructure, cost-efficient service networks, and expanding digital maintenance platforms are boosting demand across passenger and commercial EVs. China remains the largest market in Asia-Pacific due to its high EV production, advanced battery and motor service adoption, and strong collaboration between OEMs, fleet operators, and digital service providers.

Leading companies operating in the Global EV Maintenance Market include BMW, Hyundai Motor, LKQ, Continental, Tesla, BYD Auto, Robert Bosch, DENSO, Volkswagen, and Magna International. Companies in the EV Maintenance Market are deploying multiple strategies to strengthen their foothold. They are investing in predictive maintenance platforms, AI-driven diagnostics, and telematics to enhance service efficiency. Strategic partnerships with OEMs, fleet operators, and charging infrastructure providers improve market reach and service integration. Firms are expanding their service networks to offer localized support and quicker turnaround for EV maintenance. Product and service diversification, including battery health monitoring, motor servicing, and software updates, enhances value propositions.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Maintenance

- 2.2.3 Vehicle

- 2.2.4 Services

- 2.2.5 End Use

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rapid EV Adoption and Fleet Expansion

- 3.2.1.2 Battery Health and Longevity Focus

- 3.2.1.3 Technological Advancements in Predictive Maintenance

- 3.2.1.4 Regulatory and Government Incentives

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High Initial Costs for Advanced Maintenance Systems

- 3.2.2.2 Fragmented Aftermarket and Skill Gaps

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion in Commercial and Fleet Services

- 3.2.3.2 Development of Predictive and Data-Driven Services

- 3.2.3.3 Growing EV Fleet and Commercial Vehicle Adoption

- 3.2.3.4 Integration of Smart Charging and Infrastructure Maintenance

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 U.S.: EPA, CARB, NHTSA Standards

- 3.4.1.2 Canada: Transport Canada, CMVSS 305

- 3.4.2 Europe

- 3.4.2.1 Germany: BMDV, Euro 6/7 Regulations

- 3.4.2.2 France: Ministry of Transport, Euro 6/7

- 3.4.2.3 UK: Department for Transport, Euro 6/7

- 3.4.2.4 Italy: Ministry of Infrastructure & Transport, Emission Compliance

- 3.4.3 Asia Pacific

- 3.4.3.1 China: MIIT, China 6/7 Standards

- 3.4.3.2 Japan: MLIT, JIS Emission Regulations

- 3.4.3.3 South Korea: MOLIT, KS Emission Standards

- 3.4.3.4 India: MoRTH, BS6 Norms

- 3.4.4 Latin America

- 3.4.4.1 Brazil: DENATRAN, CONAMA Standards

- 3.4.4.2 Mexico: Ministry of Communications & Transport, NOM Emission Regulations

- 3.4.5 Middle East and Africa

- 3.4.5.1 UAE: RTA, ESMA Emission Regulations

- 3.4.5.2 Saudi Arabia: Ministry of Transport, SASO Emission Standards

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation Landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Cost breakdown analysis

- 3.10 Patent analysis

- 3.11 Sustainability and Environmental Aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly initiatives

- 3.11.5 Carbon footprint considerations

- 3.12 Use case scenarios

- 3.13 Software, OTA & Cybersecurity Implications on EV Maintenance

- 3.14 Fleet Electrification Impact on Maintenance Demand Patterns

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Maintenance, 2022 - 2035 ($Bn)

- 5.1 Key trends

- 5.2 Battery Maintenance and Replacement

- 5.3 Software Updates and Diagnostics

- 5.4 Charging Infrastructure Maintenance

- 5.5 Electric Motor Servicing

- 5.6 HVAC and Auxiliary Systems Maintenance

Chapter 6 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Bn)

- 6.1 Key trends

- 6.2 Passenger vehicles

- 6.2.1 Hatchbacks

- 6.2.2 Sedans

- 6.2.3 SUV

- 6.3 Commercial vehicles

- 6.3.1 Light commercial vehicles (LCV)

- 6.3.2 Medium commercial vehicles (MCV)

- 6.3.3 Heavy commercial vehicles (HCV)

Chapter 7 Market Estimates & Forecast, By Services, 2022 - 2035 ($Bn)

- 7.1 Key trends

- 7.2 Scheduled Maintenance

- 7.3 Predictive Maintenance

- 7.4 Emergency Maintenance

Chapter 8 Market Estimates & Forecast, By End Use, 2022 - 2035 ($Bn)

- 8.1 Key trends

- 8.2 Individual EV Owners

- 8.3 Fleet Operators

- 8.4 Government & Municipal Fleets

- 8.5 Commercial Charging Network Operators

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Belgium

- 9.3.7 Netherlands

- 9.3.8 Sweden

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 Singapore

- 9.4.6 South Korea

- 9.4.7 Vietnam

- 9.4.8 Indonesia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Global Player

- 10.1.1 BMW

- 10.1.2 BYD Auto

- 10.1.3 Continental

- 10.1.4 DENSO

- 10.1.5 Hyundai Motor

- 10.1.6 LKQ

- 10.1.7 Magna International

- 10.1.8 Robert Bosch

- 10.1.9 Tesla

- 10.1.10 Volkswagen

- 10.2 Regional Player

- 10.2.1 BorgWarner

- 10.2.2 CATL Service Solutions

- 10.2.3 Cummins

- 10.2.4 Eberspacher

- 10.2.5 Faurecia

- 10.2.6 HJS Emission Technology

- 10.2.7 Johnson Matthey

- 10.2.8 MANN+HUMMEL

- 10.2.9 Tenneco

- 10.2.10 Valeo

维护、维修和营运 (MRO) 市场规模、份额、趋势和预测:按供应商、MRO 类型和地区划分,2026-2034 年

维护、维修和营运 (MRO) 市场规模、份额、趋势和预测:按供应商、MRO 类型和地区划分,2026-2034 年 2026年全球工业维护服务市场报告2026年全球维护、维修和营运市场报告2026年全球维护服务市场报告

2026年全球工业维护服务市场报告2026年全球维护、维修和营运市场报告2026年全球维护服务市场报告 办公舱市场按舱体类型、建筑材料、移动性和部署方式、设计配置、分销管道和最终用户行业划分-全球预测,2026-2032年

办公舱市场按舱体类型、建筑材料、移动性和部署方式、设计配置、分销管道和最终用户行业划分-全球预测,2026-2032年 美国维护、修理和营运 (MRO):市场份额分析、行业趋势和统计数据、成长预测 (2026-2031)飞行员舱市场依产品类型、机器类型、通路和最终用户划分,全球预测(2026-2032年)欧洲维护、维修和营运 (MRO) 市场:市场份额分析、行业趋势、统计数据和成长预测 (2026-2031)日本维护、修理和营运 (MRO) 市场规模、份额、趋势和预测(按供应商、MRO 类型和地区划分),2026-2034 年

美国维护、修理和营运 (MRO):市场份额分析、行业趋势和统计数据、成长预测 (2026-2031)飞行员舱市场依产品类型、机器类型、通路和最终用户划分,全球预测(2026-2032年)欧洲维护、维修和营运 (MRO) 市场:市场份额分析、行业趋势、统计数据和成长预测 (2026-2031)日本维护、修理和营运 (MRO) 市场规模、份额、趋势和预测(按供应商、MRO 类型和地区划分),2026-2034 年 工业维护服务市场规模、份额和趋势分析报告:按服务类型、服务形式、最终用途、地区和细分市场预测(2025-2033 年)

工业维护服务市场规模、份额和趋势分析报告:按服务类型、服务形式、最终用途、地区和细分市场预测(2025-2033 年)