|

市场调查报告书

商品编码

1940703

美国维护、修理和营运 (MRO):市场份额分析、行业趋势和统计数据、成长预测 (2026-2031)United States Maintenance, Repair, And Operations (MRO) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

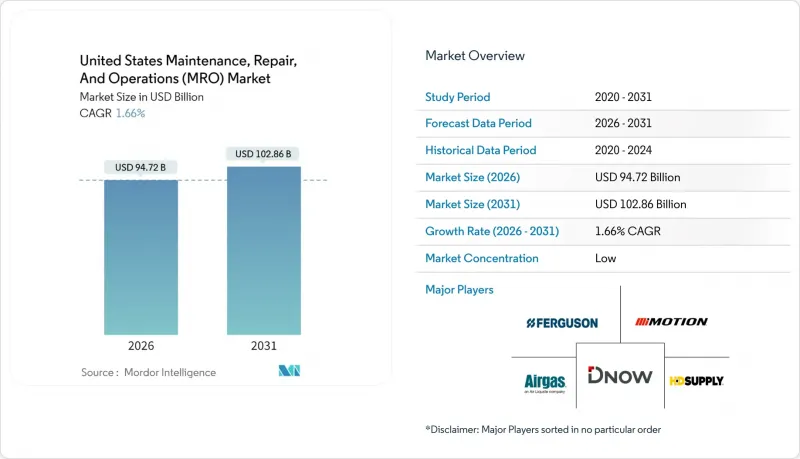

2025年美国维护、修理和营运(MRO)市场价值为931.7亿美元,预计到2031年将达到1028.6亿美元,高于2026年的947.2亿美元。

预计在预测期(2026-2031 年)内,复合年增长率将达到 1.66%。

这一前景反映了市场的成熟度,儘管受到结构性劳动力短缺的限制,但得益于联邦基础设施支出和采购业务的快速数位化。工业资产装置容量的不断增长、对节能维修需求的日益增长以及预测性维护软体的广泛应用,是推动市场温和成长的根本动力。 《基础设施投资和就业创造法案》、《晶片与科学法案》以及《通货膨胀控制法案》等政策奖励持续刺激对半导体製造厂、电池工厂和清洁能源计划的资本投资,而这些项目都依赖高价值的维护、维修和大修 (MRO) 服务。同时,随着买家转向能够提高采购效率、减少交易量并改善库存可见度的整合式线上平台,电子商务的渗透率正在加速提升。儘管存在这些机会,市场仍面临许多挑战,包括严重的技术纯熟劳工短缺、分销经销商毛利率下降以及持续的供应链波动,这些波动推高了仓储成本并延长了交货时间。租赁和分销公司之间的整合仍然是应对竞争的关键策略,近期价值超过 150 亿美元的收购案便印证了这一点,这些收购旨在实现规模经济并扩大地域覆盖范围。

美国维护、维修和营运 (MRO) 市场趋势与洞察

透过预测性维护降低成本

实施预测性维护计划的组织报告称,计划外停机时间减少了 50% 以上,缺陷减少了 70% 以上,这使得维护、维修和大修 (MRO) 从成本中心转变为价值创造者。航空业者越来越多地将状态监控纳入机队管理合同,而工业设施则将物联网感测器与分析平台集成,以确保服务水准保证。能够提供数据驱动的运转率保证的供应商可以获得更高的价格,而买家则受益于更低的生命週期成本和更高的设备运转率。政府资助的工业评估中心的兴起进一步促进了中型製造商采用预测性技术。随着预测性解决方案的规模化,软体使用费和感测器维修费将成为服务供应商的经常性收入来源,进一步推动了复合年增长率 (CAGR)。

工业资产老化导致维修週期增加

美国1950年代和1960年代运作的大量工业机械设备已超过设计寿命,导致维护频率增加,单一设备的维护成本上升。墨西哥湾沿岸地区的化学和石化设施正面临日益严格的监管审查,压力容器和管道系统必须进行强制性检修。公共交通机构报告称,车辆、轨道和设施的维修金额高达500亿至800亿美元。在航空领域,註册机械师的平均年龄已达到54岁,凸显了资产健康管理计画的紧迫性,这些计画旨在延长设备使用寿命并最大限度地降低安全风险。这些趋势共同推动了对检验服务、状态评估和维修零件的需求,从而支撑了美国MRO(维护、修理和大修)市场收入的稳定成长。

产品同质化对利润率带来压力

数位平台上的价格透明度正在挤压标准紧固件、轴承和耗材分销商的利润空间。 2024年,主要分销商报告称,由于客户转向成本最低的供应商并更多地使用自有品牌产品,其季度毛利率持续下降。市场领导格兰杰的市占率仅为7%,而且没有哪家经销商拥有足够的规模来制定产业价格。为了维持经销商正在增加附加价值服务,例如现场销售、套件组装和技术培训,但这些服务需要前期投资和较长的投资回收期,从而挤压了短期盈利。

细分市场分析

到2025年,工业MRO(维护、维修和营运)将占总收入的45.32%,这主要得益于製造业、采矿业和加工业的庞大机械设备基础。美国工业MRO市场规模的成长主要受半导体製造、汽车电气化和航太组装等领域投资回流的推动。高运转率使得密封件、轴承和液压元件的更换週期保持稳定。受电网现代化补贴和工厂电气化强制令的推动,对开关设备、驱动装置和感测器的需求增加,预计到2031年,电气MRO将以2.75%的复合年增长率成长。随着联邦奖励加速维修改造,专注于电气设备维修的服务供应商正在不断扩大市场份额。

设施维护、维修和大修 (MRO) 领域对建筑系统维护(包括暖通空调、屋顶和管道)的需求稳定,而「其他」类别则涵盖医疗设备校准和通讯设备维护等专业细分领域。操作技术( 冷暖气空调 ) 和资讯科技 (IT) 的整合正在模糊传统界限,尤其是在互联繫统需要能够同时管理机械和网路安全任务的技术人员的情况下。拥有综合性多学科团队的供应商正以可观的利润率赢得长期服务合约。

截至2025年,製造业将占美国维护、维修和营运(MRO)市场份额的37.62%,这主要得益于与机械设备维护和故障相关的570亿美元支出。五大湖区和墨西哥湾沿岸的重工业丛集对泵浦、阀门和变速箱的检修需求稳定成长。然而,医疗保健产业将主导医院升级老旧基础设施并遵守严格的设备维护标准。根据《基础设施投资和就业创造法案》,联邦政府已拨款数十亿美元用于医院的节能维修,这将进一步扩大医疗保健产业的服务市场。

能源与公共产业产业持续稳定成长,这主要得益于管线完整性维护专案和电厂延寿计划的推进。随着飞机运转率的提高,航太与国防产业的需求呈现復苏趋势,发动机维护服务也逐渐成为利润丰厚的细分市场。儘管建筑週期会带来波动,但模组化和异地製造技术的日益普及为预防性维护项目和售后零件供应创造了机会。

其他福利:

- Excel格式的市场预测(ME)表

- 分析师支持(3个月)

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 预测性维护的成本降低效益

- 工业设备老化导致维修週期增加

- MRO用品的电子商务渗透率

- 透过回流投资扩大已安装基础

- 联邦政府对节能维修的激励措施

- 用于按需製造备件的积层製造技术

- 市场限制

- 产品同质化对利润率带来压力

- 供应链波动和库存短缺

- 熟练的MRO(维修、维修和大修)劳动力短缺

- 连网装置的网路安全风险

- 产业价值链分析

- 监管环境

- 技术展望

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 对宏观经济趋势的市场评估

第五章 市场规模与成长预测

- 按MRO类型

- 工业维护、维修和运行

- 电气维护、维修和运行

- 设施维护、维修和大修

- 其他MRO类型

- 按最终用户行业划分

- 製造业

- 能源与公共产业

- 航太与国防

- 建造

- 卫生保健

- 其他终端用户产业

- 依采购模式

- 内部采购

- 外包(第三方/IFM)

- 一体化供应(VMI/一体化MRO)

- 透过维护方法

- 预防/定期

- 调整/反应

- 预知/条件

- 透过分销管道

- 线下经销商

- 线上/电子商务

- 直接从原始设备製造商采购

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Ferguson PLC

- Motion Industries Inc.(Genuine Parts Company)

- Airgas Inc.(Air Liquide SA)

- DNOW Inc.(DistributionNOW)

- HD Supply Holdings Inc.

- MRC Global Inc.

- Fastenal Company

- MSC Industrial Direct Co. Inc.

- Applied Industrial Technologies

- WESCO International Inc.

- Sonepar SA

- Rexel Holdings USA(Rexel)

- Eastern Power Technologies Inc.

- Consolidated Electrical Distributors Inc.

- Elliot Electric Supply

- Border States Industrial Inc.

- Ferguson PLC

- WW Grainger Inc.

- Fastenal Company

- MSC Industrial Direct Co. Inc.

- Distribution Solutions Group Inc.

- The Home Depot Inc.(Interline Brands Inc.)

- Builders Firstsource

- Bluelinx Holdings

第七章 市场机会与未来展望

The United States Maintenance, Repair, And Operations Market was valued at USD 93.17 billion in 2025 and estimated to grow from USD 94.72 billion in 2026 to reach USD 102.86 billion by 2031, at a CAGR of 1.66% during the forecast period (2026-2031).

This outlook reflects the market's maturity, limited by structural labor shortages yet supported by federal infrastructure spending and rapid digitalization of procurement. Moderate growth is anchored by an expanding installed base of industrial assets, rising demand for energy-efficient retrofits, and wider use of predictive maintenance software. Policy incentives from the Infrastructure Investment and Jobs Act, the CHIPS and Science Act, and the Inflation Reduction Act continue to stimulate capital investment in semiconductor fabs, battery plants, and clean-energy projects, all of which rely on high-value MRO services. At the same time, e-commerce penetration accelerates as buyers migrate to integrated online platforms that streamline sourcing, reduce transaction volume, and improve inventory visibility. Despite these opportunities, the market contends with acute skilled-labor shortages, shrinking distributor gross margins, and ongoing supply-chain volatility that inflates carrying costs and lengthens lead times. Consolidation among rental and distribution companies remains a primary competitive response, with more than USD 15 billion in recent acquisitions aimed at scale efficiencies and expanded geographic coverage.

United States Maintenance, Repair, And Operations (MRO) Market Trends and Insights

Predictive Maintenance Driven Cost Savings

Organizations adopting predictive programs report eliminating more than 50% of unplanned downtime and cutting defects by over 70%, shifting MRO from a cost center to a value generator. Aviation operators increasingly embed condition-based monitoring in fleet management contracts, and industrial facilities pair IoT sensors with analytics platforms to secure service-level guarantees. Vendors capable of delivering data-backed uptime commitments command premium rates, while buyers benefit from lower lifecycle costs and higher equipment availability. The growing roster of government-funded Industrial Assessment Centers further diffuses predictive know-how across mid-sized manufacturers. As predictive solutions scale, software fees and sensor retrofits become recurring revenue streams for service providers, reinforcing the positive CAGR contribution.

Aging Industrial Assets Increasing Repair Cycles

A large share of U.S. industrial machinery installed during the 1950s-1960s is now operating beyond its design life, driving more frequent maintenance events and higher spend per asset. Chemical and petrochemical facilities in the Gulf Coast face heightened regulatory scrutiny, prompting mandated overhauls of pressure vessels and piping systems. Public transit agencies report a USD 50-80 billion backlog for railcar, track, and facility rehabilitation . In aviation, the average certified mechanic age of 54 years underscores the urgency of asset-integrity management programs that minimize safety risks while extending service life. These dynamics collectively increase demand for inspection services, condition assessments, and refurbishment parts, supporting steady revenue growth for the United States MRO market.

Margin Pressure from Product Commoditization

Price transparency on digital platforms reduces distributor mark-ups across standard fasteners, bearings, and consumables. During 2024, leading distributors reported sequential gross-margin declines as customers migrated to lowest-cost suppliers and expanded use of private-label alternatives. With market leader Grainger holding only 7% share, no participant wields sufficient scale to set industry pricing. Distributors increasingly emphasize value-added services, such as on-site vending, kitting, and technical training, to preserve margins, yet these services entail upfront investment and longer payback periods that strain near-term profitability.

Other drivers and restraints analyzed in the detailed report include:

- E-commerce Penetration of MRO Supplies

- Reshoring Investments Expanding Installed Base

- Supply-Chain Volatility and Inventory Shortages

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Industrial MRO generated 45.32% of 2025 revenue, underpinned by the extensive machinery base in manufacturing, mining, and process industries. The United States maintenance, repair, and operations market size for industrial applications is fueled by reshoring investments in semiconductor fabrication, automotive electrification, and aerospace assembly. High-hour utilization rates create steady replacement cycles for seals, bearings, and hydraulic components. Electrical MRO, projected to grow at 2.75% CAGR to 2031, benefits from grid-modernization grants and plant electrification mandates that boost demand for switchgear, drives, and sensors. As federal incentives accelerate energy-efficiency upgrades, service providers specializing in electrical retrofits capture incremental market share.

The facility MRO segment maintains stable demand from building-system upkeep, including HVAC, roofing, and plumbing, while the "other" category comprises specialized niches such as medical-device calibration and telecom-equipment servicing. Convergence of operational technology and IT blurs traditional boundaries, particularly as interconnected systems require technicians who can manage both mechanical and cyber-security tasks. Providers that integrate multi-disciplinary teams secure longer-term service agreements at favorable margins.

Manufacturing commanded 37.62% of the United States maintenance, repair, and operations market share in 2025, supported by USD 57 billion in machinery upkeep and additional fault-related spending. Heavy-industry clusters in the Great Lakes and Gulf Coast create consistent demand for pump, valve, and gearbox overhauls. Yet healthcare leads in growth, advancing at 2.56% CAGR through 2031 as hospitals retrofit aging infrastructure and comply with stringent equipment-maintenance standards. Federal funding under the Infrastructure Investment and Jobs Act earmarks billions for hospital energy upgrades, further expanding the healthcare serviceable market.

Energy and utilities remain steady contributors, driven by pipeline-integrity programs and power-plant life-extension projects. Aerospace and defense demand rebounds alongside higher fleet-utilization rates, with engine-maintenance services surfacing as a high-margin niche. Construction cycles introduce volatility, but the rising prevalence of modular and off-site fabrication increases opportunities for pre-emptive maintenance planning and aftermarket parts supply.

The United States Maintenance, Repair, and Operations (MRO) Market Report is Segmented by MRO Type (Industrial, Electrical, and More), End-User Industry (Manufacturing, Energy and Utilities, and More), Sourcing Model (In-House, Outsourced, and More), Maintenance Approach (Preventive, Corrective, and More), and Distribution Channel (Offline, Online, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Ferguson PLC

- Motion Industries Inc. (Genuine Parts Company)

- Airgas Inc. (Air Liquide SA)

- DNOW Inc. (DistributionNOW)

- HD Supply Holdings Inc.

- MRC Global Inc.

- Fastenal Company

- MSC Industrial Direct Co. Inc.

- Applied Industrial Technologies

- WESCO International Inc.

- Sonepar SA

- Rexel Holdings USA (Rexel)

- Eastern Power Technologies Inc.

- Consolidated Electrical Distributors Inc.

- Elliot Electric Supply

- Border States Industrial Inc.

- Ferguson PLC

- W.W. Grainger Inc.

- Fastenal Company

- MSC Industrial Direct Co. Inc.

- Distribution Solutions Group Inc.

- The Home Depot Inc. (Interline Brands Inc.)

- Builders Firstsource

- Bluelinx Holdings

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Predictive maintenance driven cost savings

- 4.2.2 Aging industrial assets increasing repair cycles

- 4.2.3 E-commerce penetration of MRO supplies

- 4.2.4 Reshoring investments expanding installed base

- 4.2.5 Federal incentives for energy-efficient retrofits

- 4.2.6 Additive manufacturing for on-demand spares

- 4.3 Market Restraints

- 4.3.1 Margin pressure from product commoditization

- 4.3.2 Supply-chain volatility and inventory shortages

- 4.3.3 Skilled MRO labor shortage

- 4.3.4 Cyber-security risks in connected equipment

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Assessment of Macro-economic Trends on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By MRO Type

- 5.1.1 Industrial MRO

- 5.1.2 Electrical MRO

- 5.1.3 Facility MRO

- 5.1.4 Other MRO Types

- 5.2 By End-User Industry

- 5.2.1 Manufacturing

- 5.2.2 Energy and Utilities

- 5.2.3 Aerospace and Defense

- 5.2.4 Construction

- 5.2.5 Healthcare

- 5.2.6 Other End-user Industries

- 5.3 By Sourcing Model

- 5.3.1 In-house

- 5.3.2 Outsourced (3rd-party/IFM)

- 5.3.3 Integrated Supply (VMI/Integrated-MRO)

- 5.4 By Maintenance Approach

- 5.4.1 Preventive / Scheduled

- 5.4.2 Corrective / Reactive

- 5.4.3 Predictive / Condition-based

- 5.5 By Distribution Channel

- 5.5.1 Offline Distributors

- 5.5.2 Online / E-commerce

- 5.5.3 Direct from OEM

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Ferguson PLC

- 6.4.2 Motion Industries Inc. (Genuine Parts Company)

- 6.4.3 Airgas Inc. (Air Liquide SA)

- 6.4.4 DNOW Inc. (DistributionNOW)

- 6.4.5 HD Supply Holdings Inc.

- 6.4.6 MRC Global Inc.

- 6.4.7 Fastenal Company

- 6.4.8 MSC Industrial Direct Co. Inc.

- 6.4.9 Applied Industrial Technologies

- 6.4.10 WESCO International Inc.

- 6.4.11 Sonepar SA

- 6.4.12 Rexel Holdings USA (Rexel)

- 6.4.13 Eastern Power Technologies Inc.

- 6.4.14 Consolidated Electrical Distributors Inc.

- 6.4.15 Elliot Electric Supply

- 6.4.16 Border States Industrial Inc.

- 6.4.17 Ferguson PLC

- 6.4.18 W.W. Grainger Inc.

- 6.4.19 Fastenal Company

- 6.4.20 MSC Industrial Direct Co. Inc.

- 6.4.21 Distribution Solutions Group Inc.

- 6.4.22 The Home Depot Inc. (Interline Brands Inc.)

- 6.4.23 Builders Firstsource

- 6.4.24 Bluelinx Holdings

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

维护、维修和营运 (MRO) 市场规模、份额、趋势和预测:按供应商、MRO 类型和地区划分,2026-2034 年

维护、维修和营运 (MRO) 市场规模、份额、趋势和预测:按供应商、MRO 类型和地区划分,2026-2034 年 2026年全球工业维护服务市场报告2026年全球维护、维修和营运市场报告2026年全球维护服务市场报告

2026年全球工业维护服务市场报告2026年全球维护、维修和营运市场报告2026年全球维护服务市场报告 办公舱市场按舱体类型、建筑材料、移动性和部署方式、设计配置、分销管道和最终用户行业划分-全球预测,2026-2032年

办公舱市场按舱体类型、建筑材料、移动性和部署方式、设计配置、分销管道和最终用户行业划分-全球预测,2026-2032年 电动车维护市场机会、成长要素、产业趋势分析及2026-2035年预测飞行员舱市场依产品类型、机器类型、通路和最终用户划分,全球预测(2026-2032年)

电动车维护市场机会、成长要素、产业趋势分析及2026-2035年预测飞行员舱市场依产品类型、机器类型、通路和最终用户划分,全球预测(2026-2032年) 欧洲维护、维修和营运 (MRO) 市场:市场份额分析、行业趋势、统计数据和成长预测 (2026-2031)日本维护、修理和营运 (MRO) 市场规模、份额、趋势和预测(按供应商、MRO 类型和地区划分),2026-2034 年

欧洲维护、维修和营运 (MRO) 市场:市场份额分析、行业趋势、统计数据和成长预测 (2026-2031)日本维护、修理和营运 (MRO) 市场规模、份额、趋势和预测(按供应商、MRO 类型和地区划分),2026-2034 年 工业维护服务市场规模、份额和趋势分析报告:按服务类型、服务形式、最终用途、地区和细分市场预测(2025-2033 年)

工业维护服务市场规模、份额和趋势分析报告:按服务类型、服务形式、最终用途、地区和细分市场预测(2025-2033 年)