|

市场调查报告书

商品编码

1982293

汽车道路救援系统市场机会、成长要素、产业趋势分析及2026-2035年预测Vehicle Roadside Assistance Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

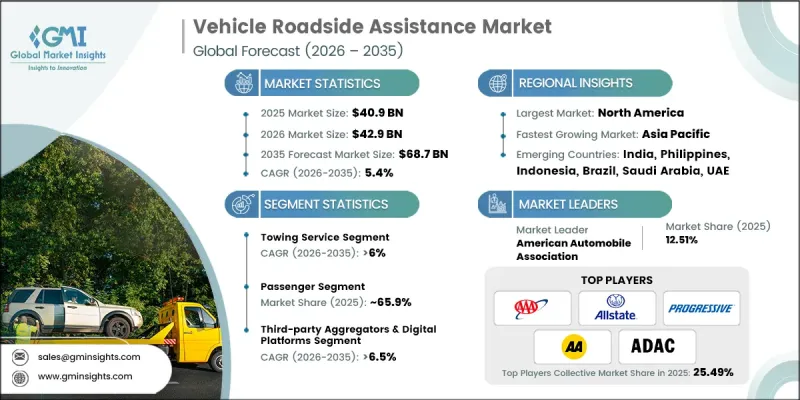

全球汽车道路救援系统市场预计到 2025 年将达到 409 亿美元,预计到 2035 年将以 5.4% 的复合年增长率增长至 687 亿美元。

随着全球车辆数量的增长、交通拥堵的加剧以及现代汽车技术的进步,车辆道路救援系统(VRA)行业正在经历重大变革。道路救援系统不再只是在车辆发生故障时救援车服务;它已成为一个全面的出行支援网络,旨在保障驾驶员安全、最大限度地减少车辆停运时间并维持服务的连续性。在人们对可靠性和便利性日益增长的需求驱动下,道路救援系统正成为保险套餐、原厂保固计画、车队管理解决方案和订阅式旅游服务的重要组成部分。随着与联网汽车技术和数位平台的整合不断深入,援助的提供方式也在改变。随着车辆系统变得越来越复杂,专业的道路救援支援服务对于个人驾驶员和商业车队营运商都至关重要,这有助于在已开发市场和新兴市场实现长期的市场扩张。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测期 | 2026-2035 |

| 上市时的市场规模 | 409亿美元 |

| 预测金额 | 687亿美元 |

| 复合年增长率 | 5.4% |

现代车辆道路救援系统平台以技术主导,功能多元。救援车、电池支援、更换轮胎、燃油输送、开锁服务和小型机械维修等服务,如今都由支援GPS定位的叫车工具、远端资讯处理连接、预测性诊断和行动应用程式提供支援。服务供应商正努力透过缩短回应时间、简化数位化计费和实施即时车辆追踪功能来提高营运效率和客户满意度。保险公司、汽车製造商、远端资讯处理公司、独立服务供应商和数位出行平台之间的合作正在不断加强。基于订阅的承保模式、保险辅助服务、基于使用量的服务以及应用程式驱动的按需解决方案,正在重新定义车辆道路救援系统市场的收入模式和服务可及性。

预计到2025年,救援车服务市占率将达到33%,并在2035年之前以6%的复合年增长率成长。救援车服务仍然是车主和车队管理人员最常需要的道路救援服务。其需求涵盖个人车和商用车,满足车辆救援、事故应变以及都市区和高速公路网路上的长途运输需求。救援车服务的必要性巩固了其在行业中的主导地位。

预计到2025年,乘用车市占率将达到65.9%,并在2026年至2035年间以4.2%的复合年增长率成长。私家车保有量高、城市人口不断增长以及对快速可靠的紧急救援服务日益增长的需求,是推动该细分市场成长的主要因素。乘用车对各种道路救援服务的需求也显着增加。数位平台和联网汽车系统的引进,能够加快回应速度,实现更顺畅的沟通,并提升驾驶者的使用者体验。

预计到2025年,北美汽车道路救援系统市场将占据33.5%的市场份额,并在2035年之前以5.7%的复合年增长率成长。高汽车保有率、高保险渗透率以及联网汽车汽车和电动车的快速普及是该地区成长的主要驱动力。完善的汽车俱乐部、汽车製造商支援的项目以及数位化按需救援平台确保了广泛的服务网络。此外,物流业者和商用车队越来越依赖整合式道路救援系统解决方案来减少停机时间并保持营运效率,这进一步增强了该地区的市场表现。

目录

第一章:调查方法

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率分析

- 成本结构

- 每个阶段增加的价值

- 影响价值链的因素

- 中断

- 影响产业的因素

- 促进因素

- 全球汽车拥有量增加

- 保险单中包含的道路救援系统增加

- 联网汽车和OEM项目的激增

- 都市化进程和人们日益增强的交通安全意识

- 产业潜在风险与挑战

- 新兴市场渗透率低

- 由于覆盖范围重迭,增量收入减少

- 市场机会

- 电动车服务增加

- 商用车辆和共享出行方式的增加

- 数位平台和聚合平台的扩张

- 新兴市场汽车拥有量增加

- 促进因素

- 成长潜力分析

- 监理情势

- 北美洲

- 美国联邦机动车辆安全管理局 (FMCSA)道路救援系统与紧急服务指南

- 美国国家公路交通安全管理局 (NHTSA) 车辆安全召回和援助计划

- 欧洲

- 欧盟道路救援系统指令(2006/126/EC)

- 德国:遵守《道路车辆登记条例》(StVZO) 下的紧急援助规定

- 英国:道路救援与车辆援助条例

- 法国:道路交通法 - 车辆故障时的道路救援

- 亚太地区

- 中国:道路交通安全法-道路救援系统指南

- 日本:道路运输车辆法-有关路边服务的规定

- 韩国:《汽车管理法》-关于紧急援助的规定

- 新加坡:《道路交通法》-车辆故障与路边援助

- 拉丁美洲

- 巴西:ANTT道路救援系统。

- 墨西哥:道路安全与车辆援助联邦标准

- 智利:道路运输安全与支援指南

- 中东和非洲

- 阿联酋:联邦交通管理局关于道路救援系统和紧急服务的政策

- 沙乌地阿拉伯:2030愿景-车辆路边支援框架

- 南非:《国家道路交通法》—道路救援系统条例

- 北美洲

- 波特的分析

- PESTEL 分析

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 专利分析

- 价格分析与成本结构

- 按服务类型分類的平均价格

- 订阅模式与计量收费模式的比较

- 成本结构细分:人事费用、燃料成本、保险费

- 各地区价格波动

- 成本上升的趋势和影响

- 永续性和环境影响分析

- 永续倡议

- 减少废弃物策略

- 生产中的能源效率

- 具有环保意识的倡议

- 碳足迹考量

- 未来展望与机会

- 永续性和环境影响分析

- 永续倡议

- 减少废弃物策略

- 生产中的能源效率

- 具有环保意识的倡议

- 碳足迹考量

- 未来展望与机会

- 服务等级协定 (SLA) 和绩效指标

- 业界标准 SLA 基准

- 按服务类型分類的平均回应时间

- 首次解析率

- 顾客满意度评分 (CSAT) 指标

- 净推荐值 (NPS) 基准

- 单位经济效益和盈利基准

- 每次服务的平均收入

- 每次服务事件的成本

- 按服务类型分類的贡献利润

- 客户获取成本 (CAC)

- 客户生命週期价值(LTV)

第四章 竞争情势

- 介绍

- 企业市占率分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 主要进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 业务拓展计划及资金筹措

第五章 市场估计与预测:依服务业划分,2022-2035年

- 救援车服务

- 轮胎更换服务

- 电池支援服务

- 燃料配送服务

- 钥匙遗失及更换服务

- 赢得和挽救服务

- 其他的

第六章 市场估价与预测:依车辆类型划分,2022-2035年

- 搭乘用车

- 轿车

- SUV 与跨界车

- 掀背车

- 商用车辆

- 轻型商用车(LCV)

- 中型商用车(MCV)

- 重型商用车(HCV)

第七章 市场估计与预测:依服务管道划分,2022-2035年

- OEM网路

- 保险公司网络

- 独立服务供应商

- 第三方聚合器和数位平台

第八章 市场估算与预测:依最终用途划分,2022-2035年

- 个人/零售客户

- 商用车辆营运商

- 汽车经销店

- 租赁公司

- 其他的

第九章 市场估计与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 比利时

- 荷兰

- 瑞典

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 菲律宾

- 印尼

- 新加坡

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲(MEA)

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第十章:公司简介

- 世界公司

- Automobile Association(AA)

- Agero

- Allianz Global Assistance

- Allstate Insurance

- American Automobile Association(AAA)

- AXA Assistance USA

- Europ Assistance

- GEICO

- Liberty Mutual Insurance

- Nationwide

- Progressive Insurance

- RAC Limited

- Travelers Insurance

- 本地球员

- ADAC

- Better World Club

- Japan Automobile Federation(JAF)

- RACE

- 新兴企业

- ARC

- Five Star Roadside

- HONK Technologies

The Global Vehicle Roadside Assistance Market was valued at USD 40.9 billion in 2025 and is estimated to grow at a CAGR of 5.4% to reach USD 68.7 billion by 2035.

The vehicle roadside assistance (VRA) industry is undergoing significant evolution as global vehicle ownership rises, traffic congestion intensifies, and modern vehicles become more technologically advanced. Roadside assistance is no longer limited to basic breakdown towing; it now operates as a comprehensive mobility support network designed to ensure driver safety, minimize vehicle downtime, and maintain service continuity. Growing expectations for reliability and convenience are positioning roadside assistance as an essential component of insurance packages, OEM warranty programs, fleet management solutions, and subscription-based mobility services. Increasing integration of connected vehicle technologies and digital platforms is reshaping how assistance is delivered. As vehicle systems become more complex, professional roadside support services are becoming indispensable to both individual drivers and commercial fleet operators, supporting long-term market expansion across developed and emerging economies.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $40.9 Billion |

| Forecast Value | $68.7 Billion |

| CAGR | 5.4% |

Modern vehicle roadside assistance platforms are technology-driven and multi-functional. Services such as towing, battery support, tire replacement, fuel delivery, lockout assistance, and minor mechanical repairs are now supported by GPS-enabled dispatch tools, telematics connectivity, predictive diagnostics, and mobile applications. Providers are improving response times, streamlining digital claims processing, and enabling real-time vehicle tracking to enhance operational efficiency and customer satisfaction. Collaboration among insurers, automotive manufacturers, telematics firms, independent service providers, and digital mobility platforms is intensifying. Subscription-based coverage models, insurance add-ons, usage-based services, and app-enabled on-demand solutions are redefining revenue models and service accessibility within the vehicle roadside assistance market.

The towing services segment accounted for 33% share in 2025 and is projected to grow at a CAGR of 6% through 2035. Towing remains the most frequently requested roadside service among vehicle owners and fleet managers. Demand spans across personal and commercial vehicles, addressing breakdown recovery, accident response, and long-distance transport needs across urban and highway networks. The essential nature of towing services continues to anchor its dominant position within the industry.

The passenger vehicle segment held 65.9% share in 2025 and is anticipated to grow at a CAGR of 4.2% between 2026 and 2035. High levels of private vehicle ownership, expanding urban populations, and increased dependence on fast and reliable emergency assistance services are driving this segment's growth. Passenger vehicles generate substantial demand for a wide range of roadside support services. The adoption of digital platforms and connected vehicle systems enables quicker dispatch, improved communication, and enhanced user experience for individual motorists.

North America Vehicle Roadside Assistance Market accounted for 33.5% share in 2025 and is expected to grow at a CAGR of 5.7% through 2035. Strong vehicle ownership rates, widespread insurance penetration, and rapid adoption of connected and electric vehicles are key contributors to regional growth. The presence of established automotive clubs, OEM-supported programs, and digital on-demand assistance platforms ensures extensive service coverage. Additionally, logistics providers and commercial fleets increasingly rely on integrated roadside assistance solutions to reduce downtime and maintain operational efficiency, further strengthening regional market performance.

Major companies operating in the Global Vehicle Roadside Assistance Market include American Automobile Association, Allianz, Allstate, GEICO, Progressive, ADAC, Automobile Association, Japan Automobile Federation (JAF), Better World Club, and RACE. Companies in the Vehicle Roadside Assistance Market are reinforcing their competitive position through digital transformation and strategic partnerships. Leading providers are investing in telematics integration, AI-powered dispatch systems, and mobile application platforms to enhance response speed and service transparency. Collaboration with insurance companies, automotive OEMs, and fleet operators is expanding bundled service offerings and subscription-based coverage models. Firms are also focusing on data analytics to predict service demand and optimize resource allocation. Expansion into electric vehicle support services and specialized fleet solutions is creating new revenue streams.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Vehicle

- 2.2.3 Service

- 2.2.4 Service Channel

- 2.2.5 End Use

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rise in global vehicle ownership

- 3.2.1.2 Increase in insurance-bundled roadside assistance

- 3.2.1.3 Surge in connected cars and OEM programs

- 3.2.1.4 Growth in urbanization and road safety awareness

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Low penetration in emerging markets

- 3.2.2.2 Overlap in coverage reducing incremental revenue

- 3.2.3 Market opportunities

- 3.2.3.1 Rise in electric vehicle (EV) specific services

- 3.2.3.2 Growth in commercial fleets and shared mobility

- 3.2.3.3 Expansion of digital and aggregator platforms

- 3.2.3.4 Increase in vehicle ownership in emerging markets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 Federal Motor Carrier Safety Administration (FMCSA) Roadside Assistance & Emergency Service Guidelines

- 3.4.1.2 National Highway Traffic Safety Administration (NHTSA) Vehicle Safety Recall & Assistance Programs.

- 3.4.2 Europe

- 3.4.2.1 EU Roadside Assistance Directive (2006/126/EC)

- 3.4.2.2 Germany: Straßenverkehrs-Zulassungs-Ordnung (StVZO) Emergency Assistance Compliance

- 3.4.2.3 UK: Roadside Recovery & Vehicle Assistance Regulations

- 3.4.2.4 France: Code de la Route - Vehicle Breakdown Assistance

- 3.4.3 Asia Pacific

- 3.4.3.1 China: Road Traffic Safety Law - Roadside Assistance Guidelines

- 3.4.3.2 Japan: Road Transport Vehicle Act - Roadside Service Regulations

- 3.4.3.3 South Korea: Motor Vehicle Management Act - Emergency Assistance Provisions

- 3.4.3.4 Singapore: Road Traffic Act - Vehicle Breakdown & Roadside Support

- 3.4.4 Latin America

- 3.4.4.1 Brazil: ANTT Roadside Assistance Regulations

- 3.4.4.2 Mexico: Federal Road Safety & Vehicle Assistance Norms

- 3.4.4.3 Chile: Road Transport Safety & Assistance Guidelines

- 3.4.5 MEA

- 3.4.5.1 UAE: Federal Transport Authority Roadside Assistance & Emergency Services Policy

- 3.4.5.2 Saudi Arabia: Vision 2030 - Vehicle Roadside Support Framework

- 3.4.5.3 South Africa: National Road Traffic Act - Roadside Assistance Regulations

- 3.4.1 North America

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Patent analysis

- 3.9 Pricing analysis & cost structure

- 3.9.1 Average service pricing by type

- 3.9.2 Subscription vs. pay-per-use models

- 3.9.3 Cost structure breakdown: labor, fuel, insurance

- 3.9.4 Regional price variations

- 3.9.5 Cost inflation trends & impact

- 3.10 Sustainability and environmental impact analysis

- 3.10.1 Sustainable practices

- 3.10.2 Waste reduction strategies

- 3.10.3 Energy efficiency in production

- 3.10.4 Eco-friendly initiatives

- 3.10.5 Carbon footprint considerations

- 3.11 Future outlook & opportunities

- 3.12 Sustainability and environmental impact analysis

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

- 3.13 Future outlook & opportunities

- 3.14 Service level agreement (SLA) & performance metrics

- 3.14.1 Industry-standard SLA benchmarks

- 3.14.2 Average response time by service type

- 3.14.3 First-call resolution rates

- 3.14.4 Customer Satisfaction Score (CSAT) metrics

- 3.14.5 Net Promoter Score (NPS) benchmarking

- 3.15 Unit Economics & Profitability Benchmarking

- 3.15.1 Average revenue per service call

- 3.15.2 Cost per service event

- 3.15.3 Contribution margin by service type

- 3.15.4 Customer acquisition cost (CAC)

- 3.15.5 Customer lifetime value (LTV)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Service, 2022 - 2035 ($Bn)

- 5.1 Key trends

- 5.2 Towing Services

- 5.3 Tire Replacement Services

- 5.4 Battery Assistance Services

- 5.5 Fuel Delivery Services

- 5.6 Lockout & Replacement Key Services

- 5.7 Winching & Extraction Services

- 5.8 Others

Chapter 6 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Bn)

- 6.1 Key trends

- 6.2 Passenger Cars

- 6.2.1 Sedans

- 6.2.2 SUVs & Crossovers

- 6.2.3 Hatchbacks

- 6.3 Commercial Vehicles

- 6.3.1 Light Commercial Vehicles (LCVs)

- 6.3.2 Medium Commercial Vehicles (MCVs)

- 6.3.3 Heavy Commercial Vehicles (HCVs)

Chapter 7 Market Estimates & Forecast, By Service Channel, 2022 - 2035 ($Bn)

- 7.1 Key trends

- 7.2 OEM Networks

- 7.3 Insurance Company Networks

- 7.4 Independent Service Providers

- 7.5 Third-Party Aggregators & Digital Platforms

Chapter 8 Market Estimates & Forecast, By End Use, 2022 - 2035 ($Bn)

- 8.1 Key trends

- 8.2 Individual/Retail Customers

- 8.3 Commercial Fleet Operators

- 8.4 Automotive Dealerships

- 8.5 Rental & Leasing Companies

- 8.6 Others

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Belgium

- 9.3.8 Netherlands

- 9.3.9 Sweden

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Philippines

- 9.4.7 Indonesia

- 9.4.8 Singapore

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Players

- 10.1.1 Automobile Association (AA)

- 10.1.2 Agero

- 10.1.3 Allianz Global Assistance

- 10.1.4 Allstate Insurance

- 10.1.5 American Automobile Association (AAA)

- 10.1.6 AXA Assistance USA

- 10.1.7 Europ Assistance

- 10.1.8 GEICO

- 10.1.9 Liberty Mutual Insurance

- 10.1.10 Nationwide

- 10.1.11 Progressive Insurance

- 10.1.12 RAC Limited

- 10.1.13 Travelers Insurance

- 10.2 Regional Players

- 10.2.1 ADAC

- 10.2.2 Better World Club

- 10.2.3 Japan Automobile Federation (JAF)

- 10.2.4 RACE

- 10.3 Emerging Players

- 10.3.1 ARC

- 10.3.2 Five Star Roadside

- 10.3.3 HONK Technologies

2026年全球车辆道路救援系统市场报告

2026年全球车辆道路救援系统市场报告 2026-2034年全球车辆道路救援系统市场规模、份额、趋势和成长分析报告

2026-2034年全球车辆道路救援系统市场规模、份额、趋势和成长分析报告 全球紧急道路救援系统服务市场(按服务类型、车辆类型、合约类型、最终用户、分销管道和获取管道划分)预测(2026-2032年)车辆道路救援系统服务市场:依拖车、电瓶搭电、轮胎修理、燃油输送、开锁服务及绞盘救援划分,全球预测,2026-2032年

全球紧急道路救援系统服务市场(按服务类型、车辆类型、合约类型、最终用户、分销管道和获取管道划分)预测(2026-2032年)车辆道路救援系统服务市场:依拖车、电瓶搭电、轮胎修理、燃油输送、开锁服务及绞盘救援划分,全球预测,2026-2032年 全球车辆道路援助市场全球连网路边援助解决方案市场

全球车辆道路援助市场全球连网路边援助解决方案市场 车辆道路援助市场规模、份额、趋势分析报告:按服务类型、提供者、车辆类型、地区和细分市场预测,2025 年至 2030 年

车辆道路援助市场规模、份额、趋势分析报告:按服务类型、提供者、车辆类型、地区和细分市场预测,2025 年至 2030 年 汽车道路救援系统的全球市场:各服务形式,各车辆类型,供应商,各地区,机会,预测,2018年~2032年

汽车道路救援系统的全球市场:各服务形式,各车辆类型,供应商,各地区,机会,预测,2018年~2032年 车辆道路救援系统:市场占有率分析、产业趋势/统计、成长预测(2025-2030)

车辆道路救援系统:市场占有率分析、产业趋势/统计、成长预测(2025-2030) 到 2030 年汽车道路援助市场预测:按服务类型、车型、平台、分销管道、订阅模式、最终用户和地区进行的全球分析

到 2030 年汽车道路援助市场预测:按服务类型、车型、平台、分销管道、订阅模式、最终用户和地区进行的全球分析