|

市场调查报告书

商品编码

1982314

资料中心浸没式冷却市场:成长机会、成长要素、产业趋势分析及2026-2035年预测Data Center Immersion Cooling Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

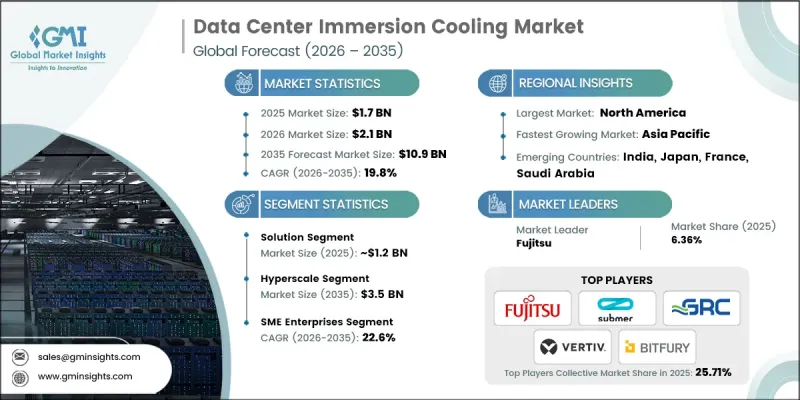

2025 年全球资料中心浸没式冷却市场价值 17 亿美元,预计到 2035 年将达到 109 亿美元,年复合成长率为 19.8%。

在数位转型加速和下一代运算需求的推动下,市场正经历快速成长。人工智慧 (AI) 和机器学习工作负载的激增、机架功率密度的不断提高以及设施整体能源效率提升的压力,都为这一增长提供了动力。随着运算负载的持续攀升,传统的冷却方式已不再适用,加速了向浸没式冷却系统的转变。不断上涨的电价和日益增强的环保意识,进一步强化了采用更有效率温度控管技术的经济合理性。託管环境和都市区资料中心有限的占地面积也促使营运商采用高密度解决方案。与传统的风冷系统相比,浸没式冷却可以显着提高每平方英尺的运算密度,使设施营运商能够在无需大规模投入的情况下,最大限度地利用现有基础设施。在单相浸没式冷却架构中,绝缘液在运作中保持液态,而泵浦和外部热交换器则有效散发累积的热负荷。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测期 | 2026-2035 |

| 上市时的市场规模 | 17亿美元 |

| 预测金额 | 109亿美元 |

| 复合年增长率 | 19.8% |

按组件划分,解决方案部分占据72%的市场份额,预计到2025年市场规模将达到12亿美元。该部分包括整合式浸没冷却系统,其中包括浸没式冷却槽、冷却液管理框架、热交换单元、监控平台和整合硬体。供应商正日益提供全面、即装即用的系统,旨在与现有资料中心环境无缝相容。现代解决方案融合了智慧温度追踪、自动冷却液调节以及与设施管理系统的集成,从而提升运行性能并优化整体能源利用。

从终端用户来看,预计到2025年,超大规模资料中心将占据29.8%的市场份额,到2035年将达到35亿美元。大型资料中心营运商正在大力投资先进的运算基础设施,以满足高效能处理的需求。这些设施在专用空间运行大规模伺服器环境,优先考虑效率、扩充性和长期基础设施弹性。超大规模业者非常重视整体拥有成本(TCO),在选择冷却技术时,会仔细权衡资本支出、营运效率和长期永续性目标。

美国资料中心浸没式冷却市场预计到2025年将达到4.542亿美元,并在2026年至2035年间以16.9%的复合年增长率成长。主要云端服务供应商和领先科技公司在美国的扩张推动了对先进冷却技术的需求成长。随着数位基础设施规模的扩大,各组织机构优先考虑经济高效且节能的温度控管系统,以维持业务竞争力。美国各地区对永续性和提高能源利用效率的坚定承诺,正在加速浸没式冷却解决方案在美国市场的普及。

目录

第一章:调查方法

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 成本结构

- 每个阶段增加的价值

- 影响价值链的因素

- 中断

- 影响产业的因素

- 促进因素

- 将机架功率密度提升到超越传统风冷极限的水平

- 人工智慧、GPU 和高密度工作负载带来的温度控管挑战日益增加。

- 我们专注于永续性、能源效率和降低PUE。

- 在超大规模和高效能运算环境中扩展部署

- 託管服务供应商和大型企业资料中心正在扩大采用范围。

- 产业潜在风险与挑战

- 前期资本投入高,系统设计复杂

- 维护、流体处理和操作标准化的挑战

- 市场机会

- 人工智慧、机器学习和超级运算工作负载的快速成长

- 在偏远地区和恶劣运行环境下扩展边缘资料中心

- 绝缘液技术的创新和两相浸没系统的广泛应用

- 促进因素

- 成长潜力分析

- 监理情势

- 北美洲

- 美国能源局(DOE) 能源效率指南

- 美国环保署(EPA)关于化学品和冷媒的法规

- ASHRAE 资料处理环境热设计指南

- 美国国家消防协会 (NFPA) 标准

- 加拿大自然资源部(NRCan)能源效率框架

- 欧洲

- 欧盟委员会的能源效率指令

- 欧盟资料中心能效行为准则

- REACH法规关于化学物质(介电液)

- 符合欧洲化学品管理局 (ECHA) 的规定

- 欧盟成员国的国家级环境与建筑法规

- 亚太地区

- 中国工业与资讯化部资料中心效率政策

- 中国的能源标籤和绿色数据中心计划

- 日本经济产业省能源效率计划

- 印度能源效率局 (BEE) 标准

- 新加坡资讯通信媒体发展局 (IMDA) 绿色资料中心指南

- 拉丁美洲

- 国家资料中心能源效率计划

- 工业流体环境合规框架

- 当地建筑和电气安全法规

- 地方基础设施管理部门推广的永续发展标准

- 中东和非洲

- 海湾合作委员会永续性与能源多元化倡议

- 沙乌地阿拉伯节能中心(SEEC)的规定

- 阿联酋绿建筑标准和资料中心永续性要求

- 非洲各地的环境监管机构

- 北美洲

- 波特的分析

- PESTEL 分析

- 科技与创新趋势

- 当前技术趋势

- 单相浸没式冷却系统

- 两相浸没式冷却技术

- 高密度GPU和AI优化的坦克设计

- 与模组化和预製资料中心集成

- 即时热监控与智慧控制软体

- 新兴技术

- 单相浸没式冷却系统

- 两相浸没式冷却技术

- 高密度GPU和AI优化的坦克设计

- 与模组化和预製资料中心集成

- 即时热监控与智慧控制软体

- 当前技术趋势

- 成本細項分析

- 浸没式水槽和围护系统

- 绝缘液成本

- 水泵、热交换器和冷却分配装置

- 监控软体

- 安装、维修和整合成本

- 永续性和环境影响

- 环境影响评估

- 社会影响和对社区的益处

- 公司管治与企业社会责任

- 永续金融与投资趋势

- 消费者行为分析

- OEM和第三方浸没式冷却系统的选择趋势

- 选择资本支出模式或营运支出模式(购买完整系统与浸没式冷却服务模式)

- 售后市场和服务趋势分析

- 浸没式冷却系统的维护合约和性能服务水准协议

- 冷却液更换週期、液体劣化监测和硬体升级

- 对浸没式水槽及组件的 OEM 和第三方服务及支援提供者进行比较评估。

- 数位化和自动化趋势分析

- 配备基于物联网的热性能监测功能的智慧浸没式冷却系统的兴起。

- 人工智慧/机器学习在预测流体管理、系统最佳化和故障检测中的作用。

- 浸没式冷却系统的引入、启动和热平衡调节的自动化。

- 与资料中心基础设施管理 (DCIM) 和遥测平台整合。

- 数位双胞胎在浸没式冷却系统性能模拟和维修规划的应用。

- 超大规模、託管、高效能运算和边缘环境的案例研究和实际应用。

- 分析可再生能源併网对资料中心浸没式冷却设计的影响

- 混合式能源配置(电网+太阳能+电池)中浸没式冷却系统的效率

- 浸没式冷却基础设施对系统级直流电和交流电源的影响。

- 与浸没式冷却系统和备用储能係统(锂离子电池、液流电池)相容

- 智慧逆变器和动态能量路由在冷冻负载管理中的作用

第四章 竞争情势

- 介绍

- 企业市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 主要进展

- 併购

- 伙伴关係和联盟

- 新产品发布

- 业务拓展计划及资金筹措

- 品牌比较分析

- 品牌知名度

- 伙伴关係生态系统

- 客户服务

- 经销网络的优势

第五章 市场估计与预测:依组件划分,2022-2035年

- 解决方案

- 冷却液

- 冷却架/模组

- 筛选

- 泵浦

- 热交换器

- 其他的

- 服务

- 安装/维护

- 培训和咨询

第六章 市场估算与预测:依冷冻技术划分,2022-2035年

- 单相冷却

- 两相冷却

第七章 市场估计与预测:依冷却液类型划分,2022-2035年

- 矿物油

- 合成冷却液

- 含氟冷媒

第八章 市场估算与预测:依组织规模划分,2022-2035年

- 小型企业

- 大公司

第九章 市场估计与预测:依应用领域划分,2022-2035年

- 超大规模

- 超级计算

- 企业级高效能运算

- 加密货币

- 边缘/5G 运算

- 其他的

第十章 市场估价与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 波兰

- 俄罗斯

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 新加坡

- 马来西亚

- 印尼

- 泰国

- 拉丁美洲

- 巴西

- 阿根廷

- 智利

- 哥伦比亚

- 中东和非洲(MEA)

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 南非

第十一章:公司简介

- 世界公司

- Asperitas

- Dell Technologies

- Fujitsu

- Green Revolution Cooling(GRC)

- Hewlett Packard Enterprise(HPE)

- Submer

- Supermicro

- Vertiv

- 当地公司

- Asetek

- Bitfury

- DCX Liquid Cooling Company

- Gigabyte Technology

- Inspur

- LiquidCool Solutions

- Midas Immersion Cooling

- 新兴企业

- ExaScaler

- Iceotope

- JetCool

- Quanta Cloud Technology(QCT)

- TAICHI Immersion Cooling

The Global Data Center Immersion Cooling Market was valued at USD 1.7 billion in 2025 and is estimated to grow at a CAGR of 19.8% to reach USD 10.9 billion by 2035.

Market growth is entering a high-growth phase, driven by accelerating digital transformation and next-generation computing requirements. Market expansion is fueled by the rapid surge in artificial intelligence and machine learning workloads, increasing rack power densities, and mounting pressure to improve energy efficiency across facilities. As computing intensity continues to escalate, traditional cooling approaches are becoming less viable, accelerating the shift toward immersion-based systems. Rising electricity costs and heightened environmental accountability are further reinforcing the economic case for more efficient thermal management technologies. Limited floor space in colocation environments and urban data facilities is also encouraging operators to adopt high-density solutions. Immersion cooling enables significantly higher compute density per square foot compared to conventional air-cooled systems, allowing facility operators to maximize existing infrastructure without major capital expansion. In single-phase immersion cooling architectures, dielectric fluid remains in a liquid state throughout operation, while pumps and external heat exchangers effectively dissipate accumulated thermal loads.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.7 Billion |

| Forecast Value | $10.9 Billion |

| CAGR | 19.8% |

By component, the solution segment held a 72% share, generating USD 1.2 billion in 2025. This segment encompasses integrated immersion cooling systems, including immersion tanks, coolant management frameworks, thermal exchange units, monitoring platforms, and supporting integration hardware. Vendors are increasingly delivering comprehensive, ready-to-deploy systems designed for seamless compatibility with established data center environments. Modern solutions incorporate intelligent temperature tracking, automated coolant regulation, and connectivity with facility management systems to enhance operational performance and overall energy optimization.

In terms of end users, the hyperscale segment held 29.8% share in 2025 and is forecast to reach USD 3.5 billion by 2035. Large-scale data center operators are heavily investing in advanced computing infrastructure to support high-performance processing demands. These facilities operate extensive server environments within purpose-built spaces, prioritizing efficiency, scalability, and long-term infrastructure resilience. Hyperscale operators place strong emphasis on total cost of ownership, carefully balancing capital expenditures, operating efficiency, and long-term sustainability objectives when selecting cooling technologies.

U.S. Data Center Immersion Cooling Market generated USD 454.2 million in 2025 and is anticipated to grow at a CAGR of 16.9% from 2026 to 2035. Increasing demand for advanced cooling technologies is driven by the expansion of large cloud service providers and major technology enterprises headquartered in the country. As digital infrastructure footprints expand, organizations are prioritizing cost-effective and energy-efficient thermal management systems to maintain operational competitiveness. Strong regional commitments to sustainability and improved power utilization effectiveness are accelerating the adoption of immersion cooling solutions across the U.S. market.

Key participants operating in the Global Data Center Immersion Cooling Market include Vertiv, Dell Technologies, Fujitsu, Submer, Green Revolution Cooling, LiquidCool Solutions, Asperitas, Bitfury, DCX Liquid Cooling Company, and Midas Immersion Cooling. Companies in the data center immersion cooling market are reinforcing their competitive positioning through continuous product innovation, strategic collaborations, and geographic expansion. Industry players are investing in research and development to enhance system reliability, thermal efficiency, and scalability to meet evolving high-density computing requirements. Many firms are introducing modular and turnkey solutions to simplify deployment and accelerate time to market. Strategic alliances with data center operators, colocation providers, and hyperscale customers are strengthening long-term supply agreements and expanding global reach. Businesses are also focusing on interoperability with existing infrastructure to reduce adoption barriers.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Cooling technique

- 2.2.4 Cooling fluid

- 2.2.5 Organization size

- 2.2.6 Application

- 2.3 TAM analysis, 2026-2035

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing rack power densities exceeding traditional air-cooling limits

- 3.2.1.2 Rising thermal management challenges from AI, GPU, and high-density workloads

- 3.2.1.3 Strong focus on sustainability, energy efficiency, and reduction in PUE

- 3.2.1.4 Growing deployment in hyperscale and high-performance computing environments

- 3.2.1.5 Increasing adoption among colocation providers and large enterprise data centers

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial capital investment and system design complexity

- 3.2.2.2 Maintenance, fluid handling, and operational standardization challenges

- 3.2.3 Market opportunities

- 3.2.3.1 Rapid expansion of AI, ML, and supercomputing workloads

- 3.2.3.2 Growth of edge data centers in remote and harsh operating environments

- 3.2.3.3 Innovation in dielectric fluids and increasing adoption of two-phase immersion systems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 U.S. Department of Energy (DOE) energy efficiency guidelines

- 3.4.1.2 Environmental Protection Agency (EPA) regulations on chemicals and refrigerants

- 3.4.1.3 ASHRAE thermal guidelines for data processing environments

- 3.4.1.4 National Fire Protection Association (NFPA) standards

- 3.4.1.5 Natural Resources Canada (NRCan) energy efficiency frameworks

- 3.4.2 Europe

- 3.4.2.1 European Commission energy efficiency directives

- 3.4.2.2 EU Code of Conduct for Data Centre Energy Efficiency

- 3.4.2.3 REACH regulation for chemical substances (dielectric fluids)

- 3.4.2.4 European Chemicals Agency (ECHA) compliance

- 3.4.2.5 National environmental and building regulations across EU member states

- 3.4.3 Asia Pacific

- 3.4.3.1 Ministry of Industry and Information Technology (China) data center efficiency policies

- 3.4.3.2 China Energy Label and green data center initiatives

- 3.4.3.3 Ministry of Economy, Trade and Industry (Japan) energy efficiency programs

- 3.4.3.4 Bureau of Energy Efficiency (India) standards

- 3.4.3.5 Singapore Infocomm Media Development Authority (IMDA) green data center guidelines

- 3.4.4 Latin America

- 3.4.4.1 National energy efficiency programs for data centers

- 3.4.4.2 Environmental compliance frameworks for industrial fluids

- 3.4.4.3 Local building and electrical safety regulations

- 3.4.4.4 Sustainability standards promoted by regional infrastructure authorities

- 3.4.5 Middle East & Africa

- 3.4.5.1 GCC sustainability and energy diversification initiatives

- 3.4.5.2 Saudi Energy Efficiency Center (SEEC) regulations

- 3.4.5.3 UAE green building codes and data center sustainability mandates

- 3.4.5.4 National environmental compliance authorities across Africa

- 3.4.1 North America

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.1.1 Single-phase immersion cooling systems

- 3.7.1.2 Two-phase immersion cooling technologies

- 3.7.1.3 High-density GPU and AI-optimized tank designs

- 3.7.1.4 Integration with modular and prefabricated data centers

- 3.7.1.5 Real-time thermal monitoring and intelligent control software

- 3.7.2 Emerging technologies

- 3.7.2.1 Single-phase immersion cooling systems

- 3.7.2.2 Two-phase immersion cooling technologies

- 3.7.2.3 High-density GPU and AI-optimized tank designs

- 3.7.2.4 Integration with modular and prefabricated data centers

- 3.7.2.5 Real-time thermal monitoring and intelligent control software

- 3.7.1 Current technological trends

- 3.8 Cost breakdown analysis

- 3.8.1 Immersion tanks and containment systems

- 3.8.2 Dielectric fluid costs

- 3.8.3 Pumps, heat exchangers, and cooling distribution units

- 3.8.4 Monitoring and control software

- 3.8.5 Installation, retrofitting, and integration costs

- 3.9 Sustainability and environmental impact

- 3.9.1 Environmental impact assessment

- 3.9.2 Social impact & community benefits

- 3.9.3 Governance & corporate responsibility

- 3.9.4 Sustainable finance & investment trends

- 3.10 Consumer behavior analysis

- 3.10.1 Preference for OEM vs third-party immersion cooling systems

- 3.10.2 Preference for CAPEX vs OPEX models (full system purchase vs immersion-as-a-service models)

- 3.11 Analysis of aftermarket and service trends

- 3.11.1 Maintenance contracts and performance SLAs for immersion cooling systems

- 3.11.2 Coolant replacement cycles, fluid degradation monitoring, and hardware upgrades

- 3.11.3 Evaluation of OEM vs third-party service and support providers for immersion tanks and components

- 3.12 Analysis of digitalization and automation trends

- 3.12.1 Rise of smart immersion systems with IoT-based thermal and performance monitoring

- 3.12.2 Role of AI/ML in predictive fluid management, system optimization, and fault detection

- 3.12.3 Automation in immersion cooling system deployment, startup, and thermal balancing

- 3.12.4 Integration with DCIM (Data Center Infrastructure Management) and telemetry platforms

- 3.12.5 Digital twin applications for simulating immersion cooling performance and planning retrofits

- 3.13 Case studies and real-world deployments across hyperscale, colocation, HPC, and edge environments

- 3.14 Analysis of impact of renewable integration on data center immersion cooling design

- 3.14.1 Immersion system efficiency in hybrid energy setups (grid + solar + battery)

- 3.14.2 System-level implications of DC-powered vs AC-powered immersion infrastructure

- 3.14.3 Compatibility of immersion cooling with backup storage systems (lithium-ion, flow batteries)

- 3.14.4 Role of smart inverters and dynamic energy routing in cooling load management

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

- 4.6 Analysis of brand comparison

- 4.6.1 Brand recognition

- 4.6.2 Partnership ecosystem

- 4.6.3 Customer service

- 4.6.4 Distribution network strength

Chapter 5 Market Estimates & Forecast, By Component, 2022 - 2035 ($Bn)

- 5.1 Key trends

- 5.2 Solution

- 5.2.1 Cooling fluids

- 5.2.2 Cooling racks/modules

- 5.2.3 Filters

- 5.2.4 Pumps

- 5.2.5 Heat exchangers

- 5.2.6 Others

- 5.3 Service

- 5.3.1 Installation & maintenance

- 5.3.2 Training & consulting

Chapter 6 Market Estimates & Forecast, By Cooling Technique, 2022 - 2035 ($Bn)

- 6.1 Key trends

- 6.2 Single phase cooling

- 6.3 Two-phase cooling

Chapter 7 Market Estimates & Forecast, By Cooling Fluid, 2022 - 2035 ($Bn)

- 7.1 Key trends

- 7.2 Mineral oil

- 7.3 Synthetic fluid

- 7.4 Fluorocarbons-based fluid

Chapter 8 Market Estimates & Forecast, By Organization Size, 2022 - 2035 ($Bn)

- 8.1 Key trends

- 8.2 SME

- 8.3 Large enterprises

Chapter 9 Market Estimates & Forecast, By Application, 2022 - 2035 ($Bn)

- 9.1 Key trends

- 9.2 Hyperscale

- 9.3 Supercomputing

- 9.4 Enterprise HPC

- 9.5 Cryptocurrency

- 9.6 Edge/5G computing

- 9.7 Others

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.2.3 Mexico

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Poland

- 10.3.7 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.4.6 Singapore

- 10.4.7 Malaysia

- 10.4.8 Indonesia

- 10.4.9 Thailand

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Argentina

- 10.5.3 Chile

- 10.5.4 Colombia

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 Saudi Arabia

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 Global players

- 11.1.1 Asperitas

- 11.1.2 Dell Technologies

- 11.1.3 Fujitsu

- 11.1.4 Green Revolution Cooling (GRC)

- 11.1.5 Hewlett Packard Enterprise (HPE)

- 11.1.6 Submer

- 11.1.7 Supermicro

- 11.1.8 Vertiv

- 11.2 Regional players

- 11.2.1 Asetek

- 11.2.2 Bitfury

- 11.2.3 DCX Liquid Cooling Company

- 11.2.4 Gigabyte Technology

- 11.2.5 Inspur

- 11.2.6 LiquidCool Solutions

- 11.2.7 Midas Immersion Cooling

- 11.3 Emerging players

- 11.3.1 ExaScaler

- 11.3.2 Iceotope

- 11.3.3 JetCool

- 11.3.4 Quanta Cloud Technology (QCT)

- 11.3.5 TAICHI Immersion Cooling

全球两相浸没式冷却液市场(按流体类型、系统类型、流动技术、应用和最终用户产业划分)预测(2026-2032年)泵送式两相冷冻系统市场(按最终用户、应用、泵类型、蒸发器设计、分销管道和冷媒类型划分),全球预测,2026-2032年资料中心氟化冷却剂市场:依流体组成、相态、冷却方式、部署配置和应用划分-全球预测,2026-2032年资料中心浸没式冷却液市场按冷却液化学成分、介电类型、流体类型、资料中心类型、应用和最终用户产业划分 - 全球预测(2026-2032 年)资料中心绿色冷却剂市场:按冷却剂类型、资料中心规模、部署模式、最终用户产业和销售管道,全球预测,2026-2032年

全球两相浸没式冷却液市场(按流体类型、系统类型、流动技术、应用和最终用户产业划分)预测(2026-2032年)泵送式两相冷冻系统市场(按最终用户、应用、泵类型、蒸发器设计、分销管道和冷媒类型划分),全球预测,2026-2032年资料中心氟化冷却剂市场:依流体组成、相态、冷却方式、部署配置和应用划分-全球预测,2026-2032年资料中心浸没式冷却液市场按冷却液化学成分、介电类型、流体类型、资料中心类型、应用和最终用户产业划分 - 全球预测(2026-2032 年)资料中心绿色冷却剂市场:按冷却剂类型、资料中心规模、部署模式、最终用户产业和销售管道,全球预测,2026-2032年 全球两相资料中心浸没式冷却市场:市场规模、占有率、成长率、产业分析、依类型、应用和地区划分的分析以及未来预测(2026-2034)

全球两相资料中心浸没式冷却市场:市场规模、占有率、成长率、产业分析、依类型、应用和地区划分的分析以及未来预测(2026-2034) 全球资料中心浸入式冷却液市场(至 2032 年)按技术(单相 vs. 双相)、资料中心类型(超大规模、AI/ML、加密货币挖矿)、类型(矿物油、氟碳基液体、合成液体)和地区划分资料中心浸入式冷却市场(按组件、技术类型、资料中心规模、部署类型和最终用户划分)- 全球预测,2025 年至 2030 年

全球资料中心浸入式冷却液市场(至 2032 年)按技术(单相 vs. 双相)、资料中心类型(超大规模、AI/ML、加密货币挖矿)、类型(矿物油、氟碳基液体、合成液体)和地区划分资料中心浸入式冷却市场(按组件、技术类型、资料中心规模、部署类型和最终用户划分)- 全球预测,2025 年至 2030 年 资料中心浸没式冷却:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030 年)

资料中心浸没式冷却:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030 年)