|

市场调查报告书

商品编码

1982343

MEMS压力感测器市场机会、成长要素、产业趋势分析及2026-2035年预测。MEMS Pressure Sensors Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

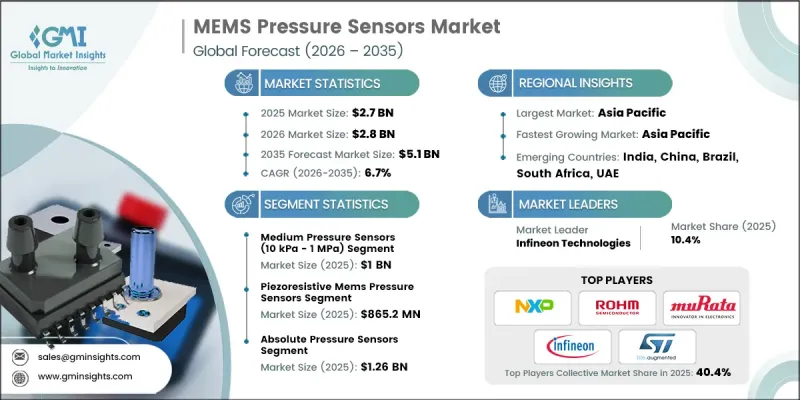

全球 MEMS 压力感测器市场预计到 2025 年价值 27 亿美元,预计到 2035 年将以 6.7% 的复合年增长率增长至 51 亿美元。

在连网型设备、汽车系统、医疗保健技术、工业自动化和高阶家用电子电器领域的日益普及推动下,MEMS压力感测器产业正稳步发展。物联网生态系统的快速扩张催生了对能够提供精确即时资料的紧凑型、低功耗感测解决方案的强劲需求。汽车製造商正在采用MEMS压力感知器来提升安全性、燃油效率和系统最佳化。在医疗领域,随着穿戴式监测设备和携带式诊断设备的日益普及,MEMS压力感测器的应用也不断成长。工业设施正在部署先进的压力感测解决方案,以增强製程控制、提高生产效率并确保符合法规要求。此外,消费性电子产品製造商正在整合智慧感测功能,以提升设备性能和使用者介面。随着各产业加速数位转型和自动化进程,MEMS压力感测器正成为全球下一代智慧系统不可或缺的一部分。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测期 | 2026-2035 |

| 初始市场规模 | 27亿美元 |

| 预计金额 | 51亿美元 |

| 复合年增长率 | 6.7% |

MEMS压力感测器凭藉其紧凑、节能的环境监测功能,在建构物联网基础设施中发挥着至关重要的作用。其小巧的尺寸和低功耗使其成为整合到智慧基础设施网路、连接型家电和先进行动装置中的理想选择。数位化专案的扩展和智慧城市的建设正在推动感测器在公共产业、交通和能源管理系统中的应用。日益增强的环保意识、先进的感测技术和自适应系统控制技术,进一步加速了感测器在下一代智慧产品中的整合。

中压感测器(量程范围为10 kPa至1 MPa)预计到2025年市场规模将达到10亿美元,占据最大的市场份额。这项需求主要源自于其在汽车系统中的广泛应用,在这些系统中,精确的压力监控对于安全性和运作效率至关重要。此外,包括製程自动化和空调系统在内的工业应用也越来越多地采用中压感测器,以便在保持性能标准的同时,精确控制流体和气压。

到2025年,压阻式MEMS压力感测器市场规模将达到8.652亿美元。其在汽车、工业和医疗领域的高普及率得益于其高测量精度和可靠的性能。压阻式感测器能够有效率地将压力波动转换为电讯号,从而在关键应用中实现精确监测。其成本效益和成熟的製造流程支持其在各个工业领域的大规模部署。製造商正致力于提高感测器的灵敏度,并扩大其在汽车和工业平台中的整合度,同时利用成熟的生产能力实现可扩展的成长。

到2025年,北美MEMS压力感测器市场占有率将达到28.6%。汽车、航太和医疗保健行业的强劲需求推动了该地区的扩张,而先进的工业基础设施和严格的安全标准则为其提供了支撑。联网汽车技术、工业自动化系统和新一代製造流程的普及应用正在加速市场成长,美国仍是主要的收入来源。强大的创新生态系统、半导体专业知识和持续的研发投入将继续巩固北美在精密感测技术领域的领先地位。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 成本结构

- 每个阶段增加的价值

- 影响价值链的因素

- 中断

- 影响产业的因素

- 促进因素

- 物联网和连网型设备的广泛应用

- 汽车产业对安全性和效率的需求日益增长

- 在医疗领域和穿戴式装置方面的应用不断扩展

- 在工业自动化和製程控制领域应用日益广泛

- 具备智慧感测功能的家用电子电器的需求日益增长

- 挑战与挑战

- 製造成本高且结构复杂

- 对影响精度的环境条件的敏感性

- 促进因素

- 成长潜力分析

- 监理情势

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL 分析

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 新兴经营模式

- 合规要求

- 供应链韧性

- 地缘政治分析

第四章 竞争情势

- 介绍

- 企业市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 市场集中度分析

- 按地区

- 主要企业的竞争标竿分析

- 产品系列比较

- 产品线宽度

- 科技

- 创新

- 区域部署对比

- 全球扩张分析

- 服务网路覆盖

- 按地区分類的市场渗透率

- 竞争定位矩阵

- 领导者

- 挑战者

- 追踪者

- 小众玩家

- 战略展望矩阵

- 产品系列比较

- 2022-2025 年重大发展

- 併购

- 伙伴关係和联盟

- 技术进步

- 业务拓展与投资策略

- 永续发展倡议

- 数位转型计划

- 新兴/Start-Ups竞争对手的发展趋势

第五章 市场估计与预测:依类型划分,2022-2035年

- 压阻式MEMS压力感测器

- 谐振式MEMS压力感测器

- 电容式MEMS压力感测器

- 光学MEMS压力感测器

- 热式MEMS压力感测器

第六章 市场估计与预测:依压力范围划分,2022-2035年

- 低电压感测器(小于10 kPa)

- 中压感测器(10 kPa 至 1 MPa)

- 高压感测器(超过 1 MPa)

第七章 市场估计与预测:依检测技术划分,2022-2035年

- 主要趋势

- 绝对压力感测器

- 压力感测器

- 差压感知器

第八章 市场估价与预测:依包装类型划分,2022-2035年

- 表面黏着型元件(SMD)

- 通孔技术(THT)

- 板载晶片(COB)

第九章 市场估价与预测:依销售管道划分,2022-2035年

- 直销

- 线上销售

第十章 市场估价与预测:依最终用户产业划分,2022-2035年

- 车

- 卫生保健

- 家用电子电器

- 工业製造

- 航太/国防

- 石油和天然气

- 环境监测

- 其他的

第十一章 市场估价与预测:按地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿拉伯聯合大公国

第十二章:公司简介

- 主要企业

- Analog Devices

- Honeywell

- STMicroelectronics

- NXP Semiconductors

- Infineon Technologies

- Bosch Sensortec

- Sensata Technologies

- Murata Manufacturing Co., Ltd.

- 按地区分類的主要企业

- 北美洲

- Amphenol Advanced Sensors

- Silicon Microstructures Inc.

- Merit Medical Systems

- 欧洲

- Endress+Hauser

- Melexis

- 亚太地区

- MinebeaMitsumi Inc.

- Omron Corporation

- ROHM Semiconductor

- TDK Corporation

- NOVOSENSE Microelectronics

- 北美洲

- 小众/颠覆者

- Winsen

The Global MEMS Pressure Sensors Market was valued at USD 2.7 billion in 2025 and is estimated to grow at a CAGR 6.7% to reach USD 5.1 billion by 2035.

The MEMS pressure sensors industry is gaining steady momentum due to increasing deployment across connected devices, automotive systems, healthcare technologies, industrial automation, and advanced consumer electronics. Rapid expansion of IoT-enabled ecosystems is creating strong demand for compact, low-power sensing solutions capable of delivering accurate real-time data. Automotive manufacturers are integrating MEMS pressure sensors to improve safety, fuel efficiency, and system optimization. In healthcare, the growing use of wearable monitoring devices and portable diagnostic equipment is strengthening adoption. Industrial facilities are implementing advanced pressure sensing solutions to enhance process control, productivity, and regulatory compliance. Additionally, consumer electronics manufacturers are incorporating smart sensing features to improve device performance and user interaction. As industries accelerate digital transformation and automation initiatives, MEMS pressure sensors are becoming critical components in next-generation intelligent systems worldwide.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.7 Billion |

| Forecast Value | $5.1 Billion |

| CAGR | 6.7% |

MEMS pressure sensors play a vital role in enabling IoT infrastructure by delivering compact and energy-efficient environmental monitoring capabilities. Their small form factor and low power consumption make them ideal for integration into smart infrastructure networks, connected appliances, and advanced mobile devices. Expanding digitalization programs and smart city developments are encouraging broader sensor deployment across utilities, transportation, and energy management systems. Enhanced environmental awareness, altitude detection, and adaptive system control are driving further integration into next-generation smart products.

The medium pressure sensors segment, covering the 10 kPa to 1 MPa range, generated USD 1 billion in 2025, representing the largest market share. Demand is supported by widespread integration into automotive systems that require precise pressure monitoring for safety and operational efficiency. Industrial applications, including process automation and climate control systems, are increasingly adopting medium pressure sensors to ensure accurate fluid and air pressure regulation while maintaining performance standards.

The piezoresistive MEMS pressure sensors segment accounted for USD 865.2 million in 2025. Strong adoption across automotive, industrial, and medical sectors is driven by their high measurement accuracy and dependable performance. Piezoresistive sensors efficiently convert pressure variations into electrical signals, enabling precise monitoring in critical applications. Their cost-effectiveness and established manufacturing processes support large-scale deployment across diverse industries. Manufacturers are focusing on improving sensitivity levels and expanding integration into automotive and industrial platforms while leveraging mature production capabilities for scalable growth.

North America MEMS Pressure Sensors Market captured 28.6% share in 2025. Regional expansion is fueled by robust demand from automotive, aerospace, and healthcare industries, supported by advanced industrial infrastructure and strict safety standards. Adoption of connected vehicle technologies, industrial automation systems, and next-generation manufacturing processes is accelerating growth, with the United States serving as the primary revenue contributor. A strong innovation ecosystem, semiconductor expertise, and sustained research and development investments continue to reinforce North America's leadership in precision sensing technologies.

Key companies operating in the Global MEMS Pressure Sensors Market include Honeywell, Bosch Sensortec, Analog Devices, STMicroelectronics, NXP Semiconductors, Infineon Technologies, Sensata Technologies, Amphenol Advanced Sensors, Murata Manufacturing Co., Ltd., TDK Corporation, Omron Corporation, ROHM Semiconductor, MinebeaMitsumi Inc., Melexis, Silicon Microstructures Inc., Endress+Hauser, Merit Medical Systems, NOVOSENSE Microelectronics, and Winsen. Companies in the MEMS Pressure Sensors Market are strengthening their competitive position through continuous innovation and strategic expansion initiatives. Leading manufacturers are investing in advanced fabrication technologies to enhance sensor accuracy, miniaturization, and energy efficiency. Integration of MEMS sensors into multifunctional modules is enabling broader applications across automotive, healthcare, and industrial sectors. Strategic collaborations with OEMs and system integrators are accelerating product adoption and design integration. Firms are also expanding production capacity to meet rising global demand while optimizing supply chain resilience.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Type trends

- 2.2.2 Pressure range trends

- 2.2.3 Sensing technology trends

- 2.2.4 Packaging type trends

- 2.2.5 Sales channel trends

- 2.2.6 End-user industry trends

- 2.2.7 Regional trends

- 2.3 TAM Analysis, 2026 - 2035 (USD Million)

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising adoption of IoT and connected devices

- 3.2.1.2 Growing automotive industry demand for safety and efficiency

- 3.2.1.3 Expansion of healthcare applications and wearable devices

- 3.2.1.4 Increasing use in industrial automation and process control

- 3.2.1.5 Rising demand for consumer electronics with smart sensing capabilities

- 3.2.2 Pitfalls and challenges

- 3.2.2.1 High manufacturing costs and complexity

- 3.2.2.2 Sensitivity to environmental conditions affecting accuracy

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Emerging Business Models

- 3.9 Compliance Requirements

- 3.10 Supply Chain Resilience

- 3.11 Geopolitical Analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Product portfolio comparison

- 4.3.1.1 Product range breadth

- 4.3.1.2 Technology

- 4.3.1.3 Innovation

- 4.3.2 Geographic presence comparison

- 4.3.2.1 Global footprint analysis

- 4.3.2.2 Service network coverage

- 4.3.2.3 Market penetration by region

- 4.3.3 Competitive positioning matrix

- 4.3.3.1 Leaders

- 4.3.3.2 Challengers

- 4.3.3.3 Followers

- 4.3.3.4 Niche players

- 4.3.4 Strategic outlook matrix

- 4.3.1 Product portfolio comparison

- 4.4 Key developments, 2022-2025

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Piezoresistive MEMS Pressure Sensors

- 5.3 Resonant MEMS Pressure Sensors

- 5.4 Capacitive MEMS Pressure Sensors

- 5.5 Optical MEMS Pressure Sensors

- 5.6 Thermal MEMS Pressure Sensors

Chapter 6 Market Estimates and Forecast, By Pressure Range, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Low Pressure Sensors (<10 kPa)

- 6.3 Medium Pressure Sensors (10 kPa - 1 MPa)

- 6.4 High Pressure Sensors (>1 MPa)

Chapter 7 Market Estimates and Forecast, By Sensing Technology, 2022 - 2035 (USD Million)

- 7.1 Key Trends

- 7.2 Absolute Pressure Sensors

- 7.3 Gauge Pressure Sensors

- 7.4 Differential Pressure Sensors

Chapter 8 Market Estimates and Forecast, By Packaging Type, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Surface-Mount Devices (SMD)

- 8.3 Through-Hole Technology (THT)

- 8.4 Chip-On-Board (COB)

Chapter 9 Market Estimates and Forecast, By Sales Channel, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 Direct Sales

- 9.3 Online Sales

Chapter 10 Market Estimates and Forecast, By End-User Industry, 2022 - 2035 (USD Million)

- 10.1 Key trends

- 10.2 Automotive

- 10.3 Healthcare

- 10.4 Consumer Electronics

- 10.5 Industrial Manufacturing

- 10.6 Aerospace & Defense

- 10.7 Oil & Gas

- 10.8 Environmental Monitoring

- 10.9 Others

Chapter 11 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Netherlands

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 Saudi Arabia

- 11.6.2 South Africa

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Global Key Players

- 12.1.1 Analog Devices

- 12.1.2 Honeywell

- 12.1.3 STMicroelectronics

- 12.1.4 NXP Semiconductors

- 12.1.5 Infineon Technologies

- 12.1.6 Bosch Sensortec

- 12.1.7 Sensata Technologies

- 12.1.8 Murata Manufacturing Co., Ltd.

- 12.2 Regional Key Players

- 12.2.1 North America

- 12.2.1.1 Amphenol Advanced Sensors

- 12.2.1.2 Silicon Microstructures Inc.

- 12.2.1.3 Merit Medical Systems

- 12.2.2 Europe

- 12.2.2.1 Endress+Hauser

- 12.2.2.2 Melexis

- 12.2.3 Asia Pacific

- 12.2.3.1 MinebeaMitsumi Inc.

- 12.2.3.2 Omron Corporation

- 12.2.3.3 ROHM Semiconductor

- 12.2.3.4 TDK Corporation

- 12.2.3.5 NOVOSENSE Microelectronics

- 12.2.1 North America

- 12.3 Niche / Disruptors

- 12.3.1 Winsen

家用电子电器用MEMS声学感测器市场:按感测器类型、介面、频率范围和应用划分-全球预测,2026-2032年

家用电子电器用MEMS声学感测器市场:按感测器类型、介面、频率范围和应用划分-全球预测,2026-2032年 先进MEMS感测器市场分析及预测(至2035年):依类型、产品类型、技术、应用、最终用户、组件类型、材料类型、装置、製程及功能划分

先进MEMS感测器市场分析及预测(至2035年):依类型、产品类型、技术、应用、最终用户、组件类型、材料类型、装置、製程及功能划分 MEMS感测器市场-全球产业规模、份额、趋势、机会、预测:按类型、材料、终端用户产业、地区和竞争格局划分,2021-2031年MEMS气体感测器市场按感测器类型、应用和分销管道划分,全球预测(2026-2032年)MEMS硅压力感测器晶片市场按类型、技术、压力范围、动作温度、晶圆尺寸、终端用户产业和销售管道划分-2026-2032年全球预测基于MEMS的自动对焦致动器市场:按致动器类型、镜头类型、应用程式和最终用户划分,全球预测,2026-2032年

MEMS感测器市场-全球产业规模、份额、趋势、机会、预测:按类型、材料、终端用户产业、地区和竞争格局划分,2021-2031年MEMS气体感测器市场按感测器类型、应用和分销管道划分,全球预测(2026-2032年)MEMS硅压力感测器晶片市场按类型、技术、压力范围、动作温度、晶圆尺寸、终端用户产业和销售管道划分-2026-2032年全球预测基于MEMS的自动对焦致动器市场:按致动器类型、镜头类型、应用程式和最终用户划分,全球预测,2026-2032年 MEMS压力感测器市场(2025-2029)

MEMS压力感测器市场(2025-2029) MEMS 感测器市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

MEMS 感测器市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测 MEMS 压力感测器:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)MEMS 感测器 -市场占有率分析、行业趋势与统计、成长预测(2025-2030 年)

MEMS 压力感测器:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)MEMS 感测器 -市场占有率分析、行业趋势与统计、成长预测(2025-2030 年)