|

市场调查报告书

商品编码

1687832

MEMS 感测器 -市场占有率分析、行业趋势与统计、成长预测(2025-2030 年)MEMS Sensor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

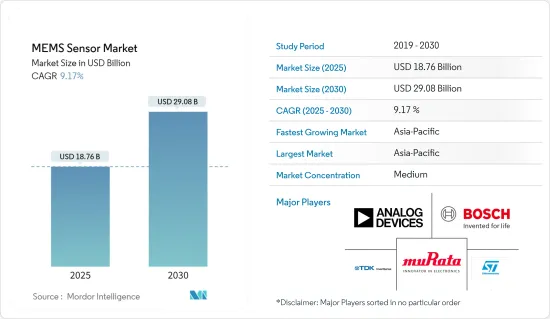

预计2025年MEMS感测器市场规模为187.6亿美元,到2030年预计将达到290.8亿美元,预测期内(2025-2030年)的复合年增长率为9.17%。

半导体领域物联网的日益普及、对智慧家电和穿戴式装置的需求不断增长以及工业和住宅自动化应用的日益普及是影响研究市场成长的关键因素。

主要亮点

- MEMS 感测器具有多种优势,包括准确性、可靠性和电子小型化。因此,MEMS 感测器近年来广受欢迎。微型消费性设备,包括物联网连网型设备和穿戴式设备,是 MEMS 感测器的新兴应用。

- 根据IFR预测,未来几年,全球工厂运作的工业机器人数量预计将达到51.8万台,这意味着全球机器人使用量将大幅增加。工业机器人市场的积极成长轨迹预计将在同一时期推动对 MEMS 感测器的需求。

- 此外,可支配收入的增加、5G的出现以及通讯基础设施的发展等因素正在推动智慧型手机需求的激增。例如,根据爱立信预测,未来几年全球智慧型手机用户数量将达到76.9亿。

- 此外,由于压力感测器在生物医学、汽车电子、小家电、穿戴式和健身电子等众多应用领域的应用,预计将实现最快的成长率。其他 MEMS 感测器,如麦克风、超音波MEMS 感测器、环境感测器和微测辐射热计,预计也将占据市场研究的很大份额。

- 波士顿半导体设备公司 (BSE) 是一家美国半导体测试处理公司,最近订单汽车客户的重复订单,要求购买多台 Zeus Gravity 测试处理机,用于 MEMS 高功率和压力 IC 测试应用。 Zeus 处理器具有灵活的 MEMS 压力感测测试单元范围,并在生产处理器中提供高电压水平,用于测试 IGBT、MOSFET、闸极驱动器、GaN 和 SiC 功率半导体。

- 此外,市场成长面临的挑战还包括由于介面设计考量而导致的 MEMS 感测器实施成本上升,以及 MEMS 製造流程缺乏标准化。毫无疑问,MEMS的标准化程度不如传统半导体製程和模型环境那么先进。然而,标准化程序应该在未来几年内到位,使得这些挑战的影响在未来几年内越来越不明显。

- COVID-19 疫情导致某些类型的 MEMS 感测器的需求激增。例如,由于需要非接触式监测人体温度,对温度枪和热成像仪中使用的热电堆和微测辐射热计的需求增加。此外,用于检测 COVID-19 的即时聚合酵素链锁反应(PCR) 诊断测试和用于 DNA序列测定的微流体在市场上也具有重要意义。

- 此外,医院加护病房(ICU)的人工呼吸器压力和流量计的需求也在增加。因此,这场疫情凸显了拥有强大医疗保健基础设施的重要性,预计随后该行业的开放将在预测期内推动市场需求。

MEMS感测器市场趋势

汽车产业预计将推动市场成长

- MEMS感测器应用于汽车工业和智慧汽车。预计MEMS感测器的开发将集中在汽车产业。广泛应用于引擎防锁死煞车系统(ABS)、电子稳定程式(ESP)、电子控制悬吊(ECS)、电子手煞车(EPB)、坡道启动辅助(HAS)、轮胎压力监测(EPMS)、汽车引擎稳定、角度测量、心率侦测、自我调整导航系统等。

- 对车辆安全和保障的需求不断增加是市场成长的主要因素之一。根据世界卫生组织统计,每年有超过135万人死于道路交通事故。 MEMS感测器在改善汽车安全性能方面发挥着至关重要的作用,从而成为市场成长的催化剂。

- OMRON发布了用于机械臂的全新系列FH-SMD视觉感测器。透过为机器人配备这些功能,它可以识别三种尺寸的随机(批量)汽车零件,这对于传统机器人来说很难做到,并提高生产率,从而实现节省空间、检查和拾取放置。

- 例如,塔塔汽车于 2022 年 4 月宣布了计划,将在未来五年为其乘用车业务融资 24,000 亿印度卢比(30.8 亿美元)。此外,2022年3月,中国上汽集团旗下名爵汽车宣布,计画将在印度的保密投资扩大3.5亿美元至5亿美元,以满足包括电动车扩张在内的未来融资需求。此类车辆的发展可能会进一步促进所研究市场的成长。

- 此外,随着新能源汽车、无人驾驶汽车等新型智慧汽车市场的发展,MEMS感测器未来很可能在汽车感测器市场占据更大的份额。最近,InvenSense 在 CES 上展示了其丰富的创新 MEMS 感测器技术。例如用于 ADAS 和自动驾驶系统的 IMU IAM-20685 高性能汽车 6 轴运动追踪感测器平台,以及用于家庭、工业、汽车、医疗保健和其他应用中的直接和精确的 CO2 检测的微型、超低功耗 MEMS 平台 TCE-11101。

亚太地区预计将占据主要市场占有率

- 由于印度、日本和中国经济的成长,以及家用电子电器和汽车产业的成长,亚太地区预计将成为 MEMS 感测器的最大市场。据思科称,预计今年亚太地区穿戴式装置销量约 3.11 亿台,北美地区约 4.39 亿台。这进一步推动了该地区对 MEMS 感测器的需求。

- 近年来,受汽车和消费市场成长以及智慧型手机、平板电脑、无人机和其他微型系统和半导体产品出口的推动,中国 MEMS 感测器的使用量大幅增加。多种MEMS感测器,包括加速计、陀螺仪、压力感测器和射频(RF)滤波器,都进口到中国进行产品组装。

- 此外,中国政府将汽车产业(包括汽车零件产业)视为其重点产业之一。中央政府预计未来几年中国汽车产量将达3,500万辆。因此,汽车产业有望成为中国MEMS感测器的突出应用领域之一。

- 根据印度品牌股权基金会(IBEF)的数据,印度家用电器和家用电子电器(ACE)市场今年的复合年增长率为 9%,达到 3.15 兆印度卢比(约 483.7 亿美元)。政府已采取多项倡议推广该产品,包括《2019 年国家电子产品政策》,该政策旨在促进国内电子产品製造业和出口完整价值链,以在未来几年实现约 4,000 亿美元的营业额。预计此类地方政府倡议将增强所研究的市场。

- 印度汽车产业在经济和人口方面都具有良好的成长条件,能够刺激国内兴趣和出口潜力。作为「印度製造」计画的一部分,印度政府旨在将汽车製造业作为该计画的关键驱动力。正如《2016-26 年汽车使命计画》(AMP)所强调的,该计画预计在未来几年内将乘用车市场扩大到 940 万辆。预计这一因素将推动该地区汽车产业对 MEMS 感测器的采用。

- 此外,日本MinbearMitsumi株式会社近日宣布,其子公司三美电机株式会社已与Omron Corporation达成协议,三美电机将收购OMRON位于野洲工厂的半导体和MEMS製造设施,作为其MEMS产品开发职能。透过收购MEMS感测器业务,三美将加强其感测器业务,这是其最重要的业务之一。

MEMS感测器产业概况

MEMS 感测器市场竞争相对激烈,拥有多家大型企业。就市场占有率而言,目前一些关键参与者占据了相当大的市场份额,包括意法半导体 (STMicroelectronics NV)、Invensense Inc.(TDK Corporation)、Bosch Sensortec GmbH(Robert Bosch GmbH)、Analog Devices Inc. 和村田製作所 (Murata Manufacturing Co.)。此外,这些公司正在不断创新其产品,以提高市场占有率和盈利。

- 2022 年 4 月:Bosch Sensatec 推出首款电容式气压感知器 BMP581。这款节能气压感测器是一款高精度高度追踪 IC,可为室内定位、地板侦测和导航应用提供准确的位置资讯。此感测器支援多种通讯接口,包括I2C、I3C和SPI数位串行接口。它体积小、功耗低,非常适合智慧穿戴装置、可听设备和物联网应用。

- 2022 年 1 月:TDK 推出其最新的具有 SoundWire 功能 MEMS 麦克风。全新 T5828 MEMS(微电子机械系统)麦克风符合 MIPI SoundWire通讯协定。它具有 68dBA SNR(信噪比)的声学活动侦测元件和始终开启的超低功耗模式。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概览

- 产业价值链分析

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争强度

- COVID-19 市场影响评估

第五章市场动态

- 市场驱动因素

- 汽车产业越来越重视安全

- 自动化和工业4.0的出现

- 市场挑战

- 多种介面设计复杂性推高了 MEMS 感测器的整体成本

- MEMS 缺乏标准化製造工艺

第六章市场区隔

- 按类型

- 压力感测器

- 惯性感测器

- 其他类型

- 按最终用户产业

- 车

- 卫生保健

- 家电

- 工业的

- 航太与国防

- 按地区

- 北美洲

- 美国

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 其他欧洲国家

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 其他亚太地区

- 世界其他地区

- 北美洲

第七章竞争格局

- 公司简介

- STMicroelectronics NV

- InvenSense Inc.(TDK Corp.)

- Bosch Sensortec GmbH(Robert Bosch GmbH)

- Analog Devices Inc.

- Murata Manufacturing Co. Ltd

- Kionix Inc.(ROHM Co Ltd)

- Infineon Technologies AG

- Freescale Semiconductors Ltd(NXP Semiconductors NV)

- Panasonic Corporation

- Omron Corporation

- First Sensor AG(TE Connectivity)

第八章投资分析

第九章:市场的未来

The MEMS Sensor Market size is estimated at USD 18.76 billion in 2025, and is expected to reach USD 29.08 billion by 2030, at a CAGR of 9.17% during the forecast period (2025-2030).

The rising popularity of IoT in semiconductors, the growing need for smart consumer electronics and wearable devices, and the enhanced adoption of automation in industries and residences are some significant factors influencing the growth of the studied market.

Key Highlights

- MEMS sensors deliver multiple advantages, such as accuracy, reliability, and the prospect of making smaller electronic devices. As a result, they have gained considerable traction in the past few years. Miniaturized consumer devices, such as IoT-connected devices and wearables, are emerging applications of MEMS sensors in the market.

- According to the IFR forecasts, global adoption is expected to increase significantly to 518,000 industrial robots operational across factories all around the globe in the next few years. The positive growth trajectory of the industrial robots market is expected to drive the demand for MEMS sensors during the same period.

- Moreover, the demand for smartphones has been witnessing an upsurge owing to several factors increasing disposable income, the advent of 5G, and the development of telecom infrastructure. For instance, according to Ericsson, worldwide smartphone subscriptions are expected to reach 7,690 million in the next few years.

- Furthermore, pressure sensors are anticipated to witness the fastest growth rate as they are used in numerous application areas, such as biomedicine, automotive electronics, small home appliances, and wearable and fitness electronics. Other MEMS sensors, such as microphones and ultrasonic MEMS sensors, environmental sensors, and microbolometers, are expected to hold a significant share of the market studied.

- The US-based Boston Semi Equipment (BSE), a semiconductor test handler company, recently received repeat orders from automotive customers for multiple Zeus gravity test handlers configured for MEMS high-power and pressure IC testing applications. Zeus handlers have a flexible range for MEMS pressure sensing test cells and offer high voltage levels in a production handler for testing IGBT, MOSFET, gate drivers, GaN, and SiC power semiconductors.

- In addition, the factors challenging the market's growth include the increase in the cost of MEMS sensors implementation due to interface design considerations and the lack of a standardized fabrication process of MEMS. The standardization in MEMS is undoubtedly less advanced than it is for conventional semiconductor processes and model environments. However, the standard procedure is bound to happen in the next few years, making the impact of the challenge gradually low in the next few years.

- Due to the COVID-19 pandemic, certain types of MEMS sensors significantly spiked in demand. For instance, the demand for thermopiles and microbolometers used in temperature guns and thermal cameras increased because of the need for contactless monitoring of people's temperatures. Moreover, real-time polymerase chain reaction (PCR) diagnostic tests for detecting COVID-19 and microfluidics for DNA sequencing gained substantial market relevance.

- Furthermore, pressure and flowmeters in ventilators grew because of hospital intensive care units (ICUs). Therefore, the pandemic highlighted the criticality of having a robust healthcare infrastructure, and the industry's subsequent developments are expected to propel market demand over the forecast period.

MEMS Sensor Market Trends

Automotive Sector Expected to Drive the Market Growth

- MEMS sensors are used in the automobile industry and intelligent automobiles. MEMS sensor development is expected to focus on the automotive industry. It is widely used in engine e(ABS), electronic stability program (ESP), electronic control suspension (ECS), electric hand brake (EPB), slope starter auxiliary (HAS), tire pressure monitoring (EPMS), car engine stabilization, angle measure, and heartbeat detection, as well as adaptive navigation systems.

- The increasing demand for safety and security in automobiles is one of the main factors that play a vital role in the market's growth. According to the WHO, more than 1.35 million people yearly are killed in road accidents. MEMS sensors play a critical role in improving the safety features of vehicles and act as a catalyst for the market's growth.

- OMRON has newly released the FH-SMD Vision Sensor series for robot arms, which can be used for fast detection for humans and flexibility for auto-selection of the compartment. These can be mounted on a robot to recognize random (bulk) automotive parts in three sizes that are hard to use with conventional robots and improve productivity, thereby saving space, inspection, and pick and place.

- For instance, in April 2022, Tata Motors announced projects to finance INR 24,000 crores (USD 3.08 billion) in its passenger motorcar business over the next five years. Furthermore, in March 2022, MG Motors, owned by China's SAIC Motor Corp., declared plans to expand USD 350-500 million in confidential equity in India to fund its future requirements, including EV expansion. Such developments in automobiles will further drive the studied market growth.

- Furthermore, with the development of new intelligent vehicles, such as new energy vehicles and driverless vehicles, MEMS sensors may occupy a more significant share of the automotive sensor market in the future. Recently, InvenSense presented its vast portfolio of innovative MEMS sensor technologies at CES. For instance, it released the IMU IAM-20685 high-performance automotive 6-Axis MotionTracking sensor platform for ADAS and autonomous systems and TCE-11101, a miniaturized ultra-low-power MEMS platform for direct and accurate detection of CO2 in home, industrial, automotive, healthcare, and other applications.

Asia-Pacific Expected to Hold Significant Market Share

- Asia-Pacific is anticipated to be the most extensive market for MEMS sensors due to economies, such as India, Japan, and China, along with the increasing growth of the consumer electronics and automobile segments. According to Cisco, this year, around 311 million and 439 million wearable device units are expected to be sold in Asia-Pacific and North America, respectively. This is further driving the demand for MEMS sensors in the region.

- China has witnessed a significant increase in the usage of MEMS sensors in the past couple of years due to the rise in its automotive and consumer markets and the export of smartphones, tablets, drones, and other microsystem and semiconductor-enabled products. Multiple MEMS sensors, such as accelerometers, gyroscopes, pressure sensors, and radio frequency (RF) filters, have been imported into China for product assembly.

- Moreover, the Chinese administration also views its automotive industry, including the auto parts sector, as one of the major industries. The Central Government expects China's automobile output to reach 35 million units in the next few years. This is posed to make the automotive sector one of the prominent uses of MEMS sensors in China.

- According to the India Brand Equity Foundation (IBEF), the Indian appliances and consumer electronics (ACE) market has registered a CAGR of 9% to achieve INR 3.15 trillion (USD 48.37 billion) this year. The government has taken several initiatives to propel this product, including the National Policy on Electronics 2019, which aims to promote domestic electronic manufacturing and export a complete value chain to achieve a turnover of approximately USD 400 billion in the next few years. Such regional government initiatives are estimated to bolster the studied market.

- The Indian automotive industry is well-positioned for growth economically and demographically, serving domestic interest and export possibilities, which will rise shortly. As a part of the Make in India scheme, the Government of India aims to make automobile fabricating the main driver for the initiative. The system is poised to make the passenger vehicles market rise to 9.4 million units in the next few years, as underlined in the 2016-26 Auto Mission Plan (AMP). This factor is expected to raise the adoption of MEMS sensors in the region's automotive sector.

- Furthermore, Minbea Mitsumi Inc., based in Japan, recently announced that Mitsumi Electric Co. Ltd, a company subsidiary, has reached an agreement with Omron Corporation to acquire the semiconductor and MEMS Manufacturing plant as the MEMS product development function at OMRON's Yasu facility through MITSUMI. Acquiring the MEMS sensor business will strengthen Mitsumi's sensor business, which is one of its most important.

MEMS Sensor Industry Overview

The MEMS sensors market is relatively competitive and consists of numerous significant players. In terms of market share, a few crucial players, such as STMicroelectronics NV, Invensense Inc. (TDK Corp), Bosch Sensortec GmbH (Robert Bosch GmbH), Analog Devices Inc., and Murata Manufacturing Co. Ltd, currently hold a significant market share. Additionally, these companies continuously innovate their products to increase their market share and profitability.

- April 2022: Bosch Sensortec released its first capacitive barometric pressure sensor, the BMP581. The energy-efficient barometric is a highly accurate altitude-tracking IC that can provide precise location information for indoor localization, floor detection, and navigation applications. The sensor supports multiple communication interfaces, including I2C, I3C, and SPI digital serial interfaces. Its small size and low power consumption create it ideal for smart wearables, hearables, and IoT applications.

- January 2022: TDK introduced the most recent MEMS microphone with SoundWire functionality. The new T5828 MEMS (micro-electromechanical system) microphone complies with the MIPI SoundWire protocol. It includes 68dBA SNR (signal-to-noise ratio) and acoustic activity detect elements with always-on ultra-low power mode.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Assessment of Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Safety Concerns in the Automotive Industry

- 5.1.2 Emergence of Automation and Industry 4.0

- 5.2 Market Challenges

- 5.2.1 Increase in Overall Cost of MEMS Sensors due to Multiple Interface Design Complexity

- 5.2.2 Lack of Standardized Fabrication Process for MEMS

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Pressure Sensors

- 6.1.2 Inertial Sensors

- 6.1.3 Other Types

- 6.2 By End-user Industry

- 6.2.1 Automotive

- 6.2.2 Healthcare

- 6.2.3 Consumer Electronics

- 6.2.4 Industrial

- 6.2.5 Aerospace and Defense

- 6.3 By Geography

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.2 Europe

- 6.3.2.1 Germany

- 6.3.2.2 United Kingdom

- 6.3.2.3 France

- 6.3.2.4 Italy

- 6.3.2.5 Rest of Europe

- 6.3.3 Asia-Pacific

- 6.3.3.1 China

- 6.3.3.2 Japan

- 6.3.3.3 India

- 6.3.3.4 South Korea

- 6.3.3.5 Rest of the Asia-Pacific

- 6.3.4 Rest of the World

- 6.3.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 STMicroelectronics NV

- 7.1.2 InvenSense Inc. (TDK Corp.)

- 7.1.3 Bosch Sensortec GmbH (Robert Bosch GmbH)

- 7.1.4 Analog Devices Inc.

- 7.1.5 Murata Manufacturing Co. Ltd

- 7.1.6 Kionix Inc. (ROHM Co Ltd)

- 7.1.7 Infineon Technologies AG

- 7.1.8 Freescale Semiconductors Ltd (NXP Semiconductors NV)

- 7.1.9 Panasonic Corporation

- 7.1.10 Omron Corporation

- 7.1.11 First Sensor AG (TE Connectivity)

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

家用电子电器用MEMS声学感测器市场:按感测器类型、介面、频率范围和应用划分-全球预测,2026-2032年

家用电子电器用MEMS声学感测器市场:按感测器类型、介面、频率范围和应用划分-全球预测,2026-2032年 MEMS压力感测器市场机会、成长要素、产业趋势分析及2026-2035年预测。

MEMS压力感测器市场机会、成长要素、产业趋势分析及2026-2035年预测。 先进MEMS感测器市场分析及预测(至2035年):依类型、产品类型、技术、应用、最终用户、组件类型、材料类型、装置、製程及功能划分

先进MEMS感测器市场分析及预测(至2035年):依类型、产品类型、技术、应用、最终用户、组件类型、材料类型、装置、製程及功能划分 MEMS感测器市场-全球产业规模、份额、趋势、机会、预测:按类型、材料、终端用户产业、地区和竞争格局划分,2021-2031年MEMS气体感测器市场按感测器类型、应用和分销管道划分,全球预测(2026-2032年)MEMS硅压力感测器晶片市场按类型、技术、压力范围、动作温度、晶圆尺寸、终端用户产业和销售管道划分-2026-2032年全球预测基于MEMS的自动对焦致动器市场:按致动器类型、镜头类型、应用程式和最终用户划分,全球预测,2026-2032年

MEMS感测器市场-全球产业规模、份额、趋势、机会、预测:按类型、材料、终端用户产业、地区和竞争格局划分,2021-2031年MEMS气体感测器市场按感测器类型、应用和分销管道划分,全球预测(2026-2032年)MEMS硅压力感测器晶片市场按类型、技术、压力范围、动作温度、晶圆尺寸、终端用户产业和销售管道划分-2026-2032年全球预测基于MEMS的自动对焦致动器市场:按致动器类型、镜头类型、应用程式和最终用户划分,全球预测,2026-2032年 MEMS压力感测器市场(2025-2029)MEMS 感测器市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

MEMS压力感测器市场(2025-2029)MEMS 感测器市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测 MEMS 压力感测器:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)

MEMS 压力感测器:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)