|

市场调查报告书

商品编码

1982345

工业热泵市场机会、成长要素、产业趋势分析及2026-2035年预测Industrial Heat Pump Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

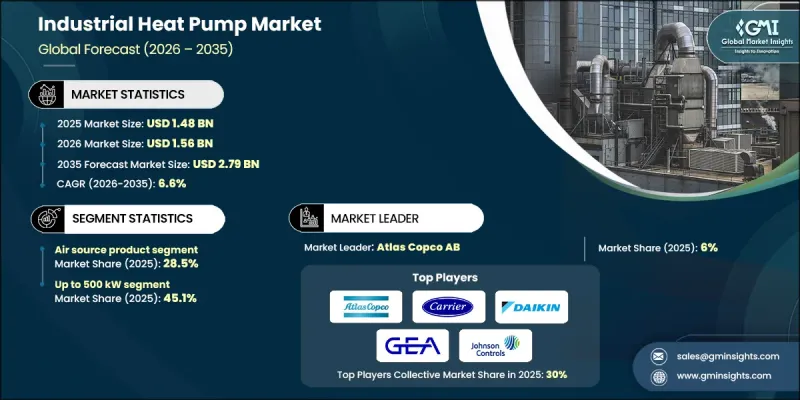

预计到 2025 年,全球工业热泵市场规模将达到 14.8 亿美元,年复合成长率为 6.6%,到 2035 年将达到 27.9 亿美元。

人们日益关注环境问题,并加强减少工业活动中的碳排放,这推动了对节能技术的需求。工业热泵已成为回收和再利用低温废热的关键解决方案,能够提高效率和永续性。随着越来越多的产业优先考虑减少对石化燃料的依赖,这些系统的应用正在加速。支持性的监管政策,加上不断上涨的能源成本和永续性目标压力,正在改变工业热能的管理方式。工业工厂对高效供暖和製冷的需求,以及对逐步淘汰系统的日益关注,持续推动市场的发展势头。产业相关人员认识到热泵在提高能源效率和降低营运成本方面的潜力。加之对干净科技和智慧基础设施(尤其是在新兴经济体)投资的增加,预计未来几年该市场将迎来强劲成长。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测期 | 2026-2035 |

| 初始市场规模 | 14.8亿美元 |

| 预测金额 | 27.9亿美元 |

| 复合年增长率 | 6.6% |

预计到2025年,空气源热泵市占率将达到28.5%。工业应用领域对高效供暖、冷气和热水解决方案的需求不断增长,以及人们对减少碳排放日益关注,预计将进一步巩固该行业的发展前景。组件技术的持续进步,例如改进的热泵压缩机和冷媒的改进,提高了整体效率,正在加速空气源热泵的普及应用。此外,空气源热泵易于安装、操作灵活、经济高效,并且广泛适用于各种工业流程,这些优势也进一步推动了空气源热泵市场的成长。

预计到2025年,500kW以下功率段的市占率将达到45.1%,并在2035年之前维持超过6.5%的复合年增长率。在工业领域,节能型暖气和冷气系统的应用日益普及,以降低营运成本和碳排放,从而推动了製造业、化工、食品饮料以及纸浆造纸等行业的需求成长。针对特定工业需求量身定制的先进热泵技术的应用正在重塑市场格局,而各行业的快速普及进一步巩固了其成长势头。

预计到2025年,美国工业热泵市场将占据75.6%的市场份额,市场规模达3.396亿美元。北美市场预计将保持强劲成长,2026年至2035年的复合年增长率(CAGR)将达到7.2%。 《通货膨胀控制法案》(IRA)等政策以及美国能源局(DOE)的定向津贴显着降低了工业电气化投资的门槛。能源密集型产业,尤其是食品饮料和纸浆造纸产业,正越来越多地采用热泵来取代老旧的燃气锅炉,并满足企业环境、社会和治理(ESG)目标。 2026年的技术进步将催生出能够在加拿大和美国北部等恶劣环境下运作的高效机组,从而扩大目标市场。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 每个阶段增加的价值

- 影响价值链的因素

- 影响产业的因素

- 促进因素

- 遏止工业排放的前景光明

- 大型工业应用领域的新投资流入

- 各主管机关支持的法规结构

- 产业潜在风险与挑战

- 前期实施成本高

- 特种合金供应链的可变性

- 机会

- 工业製程脱碳

- 政府奖励和支持政策

- 促进因素

- 成长潜力分析

- 未来市场趋势

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 依产品类型

- 监理情势

- 标准和合规要求

- 区域法规结构

- 认证标准

- 波特五力分析

- PESTEL 分析

第四章 竞争情势

- 介绍

- 企业市占率分析

- 按地区

- 企业矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 主要进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 业务拓展计划

第五章 市场估价与预测:依产品划分,2022-2035年

- 空气源

- 地热

- 水源

- 闭式循环机械热泵

- 开式循环机械蒸气压缩热泵

- 开式循环机械热压缩热泵

- 封闭回路型吸收式热泵

第六章 市场估计与预测:依产能划分,2022-2035年

- 500千瓦或以下

- 500千瓦至2兆瓦

- 2 MW~5 MW

- 超过5兆瓦

第七章 市场估计与预测:依温度划分,2022-2035年

- 80~100°C

- 100~150°C

- 150~200°C

- 高于 200 度C

第八章 市场估计与预测:依应用领域划分,2022-2035年

- 工业的

- 造纸

- 食品/饮料

- 化学

- 钢

- 机器

- 非金属矿物

- 其他行业

- 区域供热

第九章 市场估计与预测:依国家划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第十章:公司简介

- Armstrong International Inc.

- Atlas Copco AB

- Baker Hughes Company

- Carrier

- 大金应用欧洲有限公司

- Dalrada Climate Technology

- Ecop

- Emerson Electric Co.

- Enerin AS

- GEA Group Aktiengesellschaft

- Hien New Energy Equipment Co., Ltd.

- Johnson Controls

- MAN Energy Solutions

- OCHSNER

- Oilon Group Oy

- Piller Blowers &Compressors GmbH

- Qvantum Energi AB

- Swegon Ltd

- Trane Technologies International Limited

- Turboden SpA

The Global Industrial Heat Pump Market was valued at USD 1.48 billion in 2025 and is estimated to grow at a CAGR of 6.6% to reach USD 2.79 billion by 2035.

Rising environmental concerns and increased efforts to cut carbon emissions in industrial operations are pushing the demand for energy-efficient technologies. Industrial heat pumps have emerged as a key solution for capturing and repurposing low-temperature waste heat, enhancing both efficiency and sustainability. As more industries prioritize reducing reliance on fossil fuels, the adoption of these systems is accelerating. Supportive regulatory policies, combined with increasing energy costs and growing pressure to align with sustainability targets, are reshaping how industries manage thermal energy. The need for efficient heating and cooling across industrial plants, along with growing interest in phasing out outdated systems, continues to boost market momentum. Industrial players are recognizing the potential of heat pumps to improve energy performance while cutting operational expenditures. Coupled with rising investments in clean technologies and smart infrastructure, especially across emerging economies, the market is set to witness robust expansion in the years ahead.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.48 Billion |

| Forecast Value | $2.79 Billion |

| CAGR | 6.6% |

The air source heat pump segment held 28.5% share in 2025. Rising demand for efficient solutions in space heating, cooling, and hot water across industrial applications, coupled with the increasing focus on reducing carbon emissions, is expected to strengthen the industry outlook. Continuous advancements in component technologies, including improvements in heat pump compressors and refrigerants to enhance overall efficiency, are accelerating adoption. Additionally, the ease of installation, operational versatility, cost-effectiveness, and wide applicability across various industrial processes are further supporting the growth of the air source heat pump market.

The up to 500 kW segment accounted for 45.1% share in 2025 and is projected to grow at over 6.5% CAGR through 2035. Industrial sectors are increasingly deploying energy-efficient heating and cooling systems to lower operational costs and reduce carbon footprints, driving demand in manufacturing, chemical processing, food & beverage, and pulp & paper industries. The adoption of advanced heat pump technologies tailored to specific industrial requirements is reshaping the market, with rapid implementation across diverse sectors further enhancing the growth trajectory.

U.S. Industrial Heat Pump Market held 75.6% share in 2025, generating USD 339.6 million. North America is expected to grow at a strong CAGR of 7.2% from 2026 to 2035. Policies such as the Inflation Reduction Act (IRA) and targeted Department of Energy (DOE) grants are significantly reducing capital expenditure barriers for industrial electrification. Energy-intensive industries, particularly food & beverage and pulp & paper, are increasingly adopting heat pumps to replace aging gas-fired boilers and meet corporate ESG targets. Technological advances in 2026 have introduced high-efficiency units capable of operating under extreme conditions in Canada and northern U.S., broadening the addressable market.

Key players shaping the competitive landscape of the Global Industrial Heat Pump Market include Turboden S.p.A., Ecop, MAN Energy Solutions, Carrier, Qvantum Energi AB, Oilon Group Oy, Dalrada Climate Technology, Armstrong International Inc., Johnson Controls, Atlas Copco AB, GEA Group Aktiengesellschaft, Hien New Energy Equipment Co., Ltd., Daikin Applied Europe S.p.A., Trane Technologies International Limited, Swegon Ltd, Enerin AS, OCHSNER, Emerson Electric Co., Baker Hughes Company, and Piller Blowers & Compressors GmbH. To strengthen their positioning, companies in the industrial heat pump space are prioritizing strategic investments in product innovation and R&D to offer higher efficiency systems compatible with modern industrial demands. Several players are expanding global manufacturing capabilities and establishing local partnerships to cater to region-specific requirements. Firms are also aligning their portfolios with low-carbon and renewable energy trends, introducing systems capable of integrating with waste heat recovery and hybrid setups.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Countrywise

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product Type

- 2.2.3 By Power Range

- 2.2.4 Material/Construction

- 2.2.5 End-User

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Positive outlook to curb industrial emission levels

- 3.2.1.2 Influx of new investments across heavy-duty industrial applications

- 3.2.1.3 Encouraging regulatory framework by respective authorities

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Significant initial deployment cost

- 3.2.2.2 Supply Chain Volatility for Specialized Alloys

- 3.2.3 Opportunities

- 3.2.3.1 Decarbonization of industrial processes

- 3.2.3.2 Government incentives and supportive policies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By Product Type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022 - 2035 (USD Million) (Thousand Units)

- 5.1 Key trends

- 5.2 Air source

- 5.3 Ground source

- 5.4 Water source

- 5.5 Closed cycle mechanical heat pump

- 5.6 Open cycle mechanical vapor compression heat pump

- 5.7 Open cycle mechanical thermocompression heat pump

- 5.8 Closed cycle absorption heat pump

Chapter 6 Market Estimates and Forecast, By Capacity, 2022 - 2035 (USD Million) (Thousand Units)

- 6.1 Key trends

- 6.2 Up to 500 kW

- 6.3 > 500 kW to 2 MW

- 6.4 2 MW - 5 MW

- 6.5 > 5 MW

Chapter 7 Market Estimates and Forecast, By Temperature, 2022 - 2035 (USD Million) (Thousand Units)

- 7.1 Key trends

- 7.2 80 - 100 °C

- 7.3 100 - 150 °C

- 7.4 150 - 200 °C

- 7.5 > 200 °C

Chapter 8 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million) (Thousand Units)

- 8.1 Key trends

- 8.2 Industrial

- 8.2.1 Paper

- 8.2.2 Food & beverages

- 8.2.3 Chemical

- 8.2.4 Iron & Steel

- 8.2.5 Machinery

- 8.2.6 Non-Metallic minerals

- 8.2.7 Other industries

- 8.3 District heating

Chapter 9 Market Estimates and Forecast, By Country, 2022 - 2035 (USD Million) (Thousand Units)

- 9.1 Key trends

- 9.2 Key trends

- 9.3 North America

- 9.3.1 U.S.

- 9.3.2 Canada

- 9.4 Europe

- 9.4.1 Germany

- 9.4.2 UK

- 9.4.3 France

- 9.4.4 Italy

- 9.4.5 Spain

- 9.5 Asia Pacific

- 9.5.1 China

- 9.5.2 Japan

- 9.5.3 India

- 9.5.4 Australia

- 9.5.5 South Korea

- 9.6 Latin America

- 9.6.1 Brazil

- 9.6.2 Mexico

- 9.6.3 Argentina

- 9.7 Middle East and Africa

- 9.7.1 South Africa

- 9.7.2 Saudi Arabia

- 9.7.3 UAE

Chapter 10 Company Profiles

- 10.1 Armstrong International Inc.

- 10.2 Atlas Copco AB

- 10.3 Baker Hughes Company

- 10.4 Carrier

- 10.5 Daikin Applied Europe S.p.A.

- 10.6 Dalrada Climate Technology

- 10.7 Ecop

- 10.8 Emerson Electric Co.

- 10.9 Enerin AS

- 10.10 GEA Group Aktiengesellschaft

- 10.11 Hien New Energy Equipment Co., Ltd.

- 10.12 Johnson Controls

- 10.13 MAN Energy Solutions

- 10.14 OCHSNER

- 10.15 Oilon Group Oy

- 10.16 Piller Blowers & Compressors GmbH

- 10.17 Qvantum Energi AB

- 10.18 Swegon Ltd

- 10.19 Trane Technologies International Limited

- 10.20 Turboden S.p.A.

2026年全球二氧化碳卸载帮浦系统市场报告

2026年全球二氧化碳卸载帮浦系统市场报告 2026-2030年全球工业热泵市场

2026-2030年全球工业热泵市场 烟叶空气源热泵干燥机市场:依烟草类型、技术类型、容量范围、电源、运作模式、通路划分,全球预测(2026-2032年)

烟叶空气源热泵干燥机市场:依烟草类型、技术类型、容量范围、电源、运作模式、通路划分,全球预测(2026-2032年) 全球热泵市场规模、份额、趋势和成长分析报告(2026-2034年)

全球热泵市场规模、份额、趋势和成长分析报告(2026-2034年) 全球工业热泵市场:预测(至2034年)-按热源、容量、温度范围、技术、最终用户和地区进行分析2026年全球热泵市场报告

全球工业热泵市场:预测(至2034年)-按热源、容量、温度范围、技术、最终用户和地区进行分析2026年全球热泵市场报告 热驱动热泵市场-全球产业规模、份额、趋势、机会、预测:依产品类型、应用、技术、地区和竞争格局划分,2021-2031年空气源热泵市场按类型、容量、应用和分销管道划分-2026-2032年全球预测

热驱动热泵市场-全球产业规模、份额、趋势、机会、预测:依产品类型、应用、技术、地区和竞争格局划分,2021-2031年空气源热泵市场按类型、容量、应用和分销管道划分-2026-2032年全球预测 全球热泵市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031年)

全球热泵市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031年) 日本热泵市场报告(按额定容量、产品类型、最终用途产业和地区划分,2026-2034 年)

日本热泵市场报告(按额定容量、产品类型、最终用途产业和地区划分,2026-2034 年)