|

市场调查报告书

商品编码

1998804

可折迭瓦楞纸包装市场:商业机会、成长要素、产业趋势分析及 2026-2035 年预测。Folding Carton Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

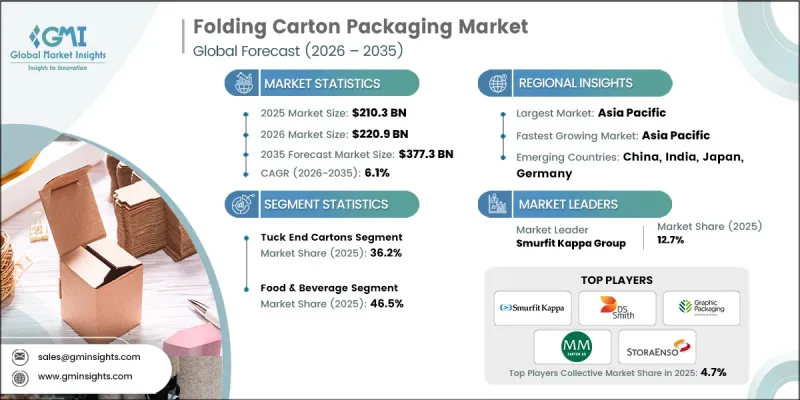

预计到 2025 年,全球可折迭瓦楞纸包装市场价值将达到 2,103 亿美元,年复合成长率为 6.1%,到 2035 年将达到 3,773 亿美元。

可折迭瓦楞纸包装市场的成长主要得益于全球对永续包装材料的转型以及可回收纤维基解决方案的日益普及。许多地区政府和监管机构正在实施更严格的包装法规,旨在减少环境影响并促进循环经济实践。这些政策正在加速从硬质塑胶包装到纸板基替代品的转变,后者兼顾了可回收性和减少环境影响。此外,电子商务和现代零售分销管道的快速发展也增加了对既能保护产品又能保持强大品牌识别度的二次包装形式的需求。製药、医疗保健、化妆品和个人护理等行业也越来越依赖高品质的可折迭纸盒来满足包装安全要求和监管标准。同时,品牌越来越重视能够提升产品吸引力并强化品牌形象的高端包装设计。这些不断变化的需求,加上纸盒製造和印刷流程的持续技术进步,将继续支撑全球可折迭纸盒包装市场的长期成长。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测期 | 2026-2035 |

| 初始市场规模 | 2103亿美元 |

| 预测金额 | 3773亿美元 |

| 复合年增长率 | 6.1% |

可折迭瓦楞纸包装市场也受到强烈的监管趋势的影响,这些趋势鼓励企业采用可回收纤维性包装解决方案。各国政府和环保组织正在实施更严格的废弃物管理政策和永续性目标,要求製造商减少包装废弃物并提高可回收性。因此,许多行业正在转向轻质纸板箱,这种包装既具有环境效益,又能提高材料利用率。这种方法使企业能够在优化包装结构的同时降低整体材料消耗。原物料成本的上涨和对碳足迹报告日益增长的关注进一步促使企业提高包装效率并减少对环境的影响。

预计2026年至2035年间,展示型纸盒市场将以8.6%的复合年增长率成长,反映出现代零售环境的强劲需求。这类包装形式因其简化了零售店内商品的搬运和展示流程而日益普及。展示型纸盒能够将产品运输和货架展示整合于单一包装结构中,从而提高零售商的营运效率并减少补货所需的工作量。零售商和消费品製造商越来越倾向于选择兼具物流效率和卓越视觉效果的包装形式。随着有组织零售业的持续扩张和消费者在零售环境中竞争的加剧,对展示型纸盒包装解决方案的需求预计将稳定成长。

预计到2025年,涂布再生纸板(CRB)的市场规模将达到699亿美元。由于其成本效益高且再生纤维含量高,这种材料持续广泛应用,使其成为寻求环保包装解决方案的企业的理想选择。 CRB在各种包装应用中都能提供可靠的结构性能,特别适用于那些对外观要求不高的场合。日益增长的监管压力促使包装产品中再生材料的比例不断提高,从而推动了CRB在各行各业的广泛应用。那些希望在控製成本的同时提升永续性绩效的企业往往会优先考虑再生纸板材料,这也巩固了CRB在可折迭瓦楞纸包装市场的主导地位。

到2025年,北美可折迭纸盒包装市占率将达到29.1%。由于严格的环境法规以及各消费品行业对可回收包装材料需求的不断增长,该地区的纸盒包装行业持续扩张。在北美营运的公司越来越多地采用纸板包装解决方案来取代传统的塑胶包装。此外,零售商也敦促供应商根据其永续发展计划,转向使用可回收包装。该地区对先进製造技术的投资也在增加,旨在提高瓦楞纸板的加工效率,并支持更高水准的产品客製化。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 成本结构

- 每个阶段增加的价值

- 影响价值链的因素

- 中断

- 影响产业的因素

- 促进因素

- 推动制定纤维基可回收包装材料的相关法规

- 电子商务对二次包装的需求不断增长。

- 从塑胶翻盖式容器过渡到纸盒

- 药品序列化和合规性要求

- 化妆品和个人护理用品包装盒的优质化

- 产业潜在风险与挑战

- 原生纸浆和纸板价格波动

- 先进模切设备的高昂资本投资成本

- 市场机会

- 使用阻隔涂层的可再生板

- 将智慧包装与QR码和NFC功能集成

- 促进因素

- 成长潜力分析

- 监理情势

- 波特五力分析

- PESTEL 分析

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 副产品

- 定价策略

- 新兴经营模式

- 合规要求

- 专利和智慧财产权分析

- 贸易数据分析(基于付费资料库)

- 进出口量及进口额趋势

- 主要贸易走廊及关税的影响

- 人工智慧和生成式人工智慧对市场的影响

- 利用人工智慧改造现有经营模式

- 针对特定领域的生成式人工智慧应用案例和实施蓝图

第四章 竞争情势

- 介绍

- 企业市占率分析

- 按地区

- 市场集中度分析

- 主要企业的竞争标竿分析

- 财务绩效比较

- 销售量

- 利润率

- 研究与发展(R&D)

- 产品系列比较

- 产品线宽度

- 科技

- 创新

- 区域扩张比较

- 全球扩张分析

- 服务网路覆盖

- 按地区分類的市场渗透率

- 竞争定位矩阵

- 领导者

- 挑战者

- 追踪者

- 小众玩家

- 战略展望矩阵

- 财务绩效比较

- 主要进展

- 併购

- 伙伴关係与合作

- 技术进步

- 业务拓展与投资策略

- 数位转型计划

- 新兴/Start-Ups竞争对手的发展趋势

第五章 市场估价与预测:依纸箱结构划分,2022-2035年

- 折迭式纸箱

- 自动锁扣/底部易碎纸箱

- 套筒纸箱

- 锁底纸箱

- 适用于展示的纸箱

- 其他折迭结构

第六章 市场估算与预测:纸板等级划分,2022-2035年

- 固态漂白硫酸浆(SBS)

- 未漂白工艺外套 (CUK)

- 涂布再生纸板(CRB)

- 无涂布纸板

第七章 市场估价与预测:依印刷技术划分,2022-2035年

- 胶印光刻

- 柔版印刷

- 数位印刷

- 凹版印刷

第八章 市场估计与预测:依应用领域划分,2022-2035年

- 食品/饮料

- 个人护理和化妆品

- 製药和医疗保健

- 家用物品/消费品

- 烟草

- 其他的

第九章 市场估计与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第十章:公司简介

- 主要企业

- DS Smith Plc

- Graphic Packaging International

- Huhtamaki Oyj

- Mayr-Melnhof Karton AG

- Oji Holdings Corporation

- Rengo Co., Ltd.

- Smurfit Kappa Group

- Stora Enso Oyj

- 按地区分類的主要企业

- 北美洲

- All Packaging Company

- American Carton Company

- Diamond Packaging

- Georgia-Pacific LLC

- Green Bay Packaging Inc.

- Meyers

- Seaboard Folding Box Company Inc.

- Wynalda Packaging

- 亚太地区

- Plastech Group Ltd.

- 欧洲

- Schur Pack Germany GmbH

- 北美洲

- 特殊玩家/干扰者

- August Faller GmbH & Co. KG

The Global Folding Carton Packaging Market was valued at USD 210.3 billion in 2025 and is estimated to grow at a CAGR of 6.1% to reach USD 377.3 billion by 2035.

Growth in the folding carton packaging market is largely driven by the global transition toward sustainable packaging materials and the increasing adoption of recyclable fiber-based solutions. Governments and regulatory authorities across many regions are introducing stricter packaging regulations aimed at reducing environmental impact and encouraging circular economy practices. These policies are accelerating the shift away from rigid plastic packaging toward paperboard-based alternatives that offer recyclability and lower environmental footprints. In addition, the rapid growth of e-commerce and modern retail distribution channels has created a stronger demand for secondary packaging formats that protect products while maintaining strong branding visibility. Industries such as pharmaceuticals, healthcare, cosmetics, and personal care are also increasing their reliance on high-quality folding cartons to meet packaging safety requirements and regulatory standards. At the same time, brands are placing greater emphasis on premium packaging designs that enhance product appeal and strengthen brand identity. These evolving requirements, combined with continuous technological improvements in carton manufacturing and printing processes, continue to support long-term expansion of the global folding carton packaging market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $210.3 Billion |

| Forecast Value | $377.3 Billion |

| CAGR | 6.1% |

The folding carton packaging market is also influenced by strong regulatory momentum encouraging companies to adopt recyclable fiber-based packaging solutions. Governments and environmental organizations are implementing stricter waste management policies and sustainability targets that require manufacturers to reduce packaging waste and improve recyclability. As a result, many industries are shifting toward lightweight paperboard cartons that offer both environmental benefits and efficient material utilization. This approach allows companies to optimize packaging structures while lowering overall material consumption. Rising costs of raw materials and increased focus on carbon footprint reporting are further motivating organizations to improve packaging efficiency and reduce environmental impact.

The display-ready cartons segment is projected to grow at a CAGR of 8.6% during 2026-2035, reflecting strong demand across modern retail environments. These packaging formats are gaining popularity because they simplify product handling and merchandising processes within retail stores. Display-ready cartons allow products to be transported and presented on retail shelves using a single packaging structure, which improves operational efficiency for retailers and reduces labor requirements during product stocking. Retailers and consumer goods companies increasingly prefer packaging formats that combine logistical efficiency with strong visual presentation. As organized retail continues to expand and consumer competition intensifies across store environments, the demand for display-ready carton packaging solutions is expected to increase steadily.

The coated recycled paperboard (CRB) segment reached USD 69.9 billion in 2025. This material remains widely used due to its cost efficiency and high recycled fiber content, making it an attractive option for companies seeking environmentally responsible packaging solutions. CRB offers reliable structural performance for various packaging applications where a premium visual appearance is not a primary requirement. Increasing regulatory pressure to incorporate higher levels of recycled materials into packaging products has strengthened the adoption of CRB across multiple industries. Companies aiming to enhance their sustainability performance while maintaining cost control often prioritize recycled paperboard materials, which continues to support the leading position of this segment within the folding carton packaging market.

North America Folding Carton Packaging Market accounted for 29.1% share in 2025. The industry in this region continues to expand due to strict environmental regulations and growing demand for recyclable packaging materials across several consumer industries. Businesses operating in North America are increasingly adopting paperboard-based packaging solutions as alternatives to conventional plastic packaging. In addition, retailers are encouraging suppliers to transition toward recyclable packaging formats that align with sustainability commitments. The region has also seen increasing investment in advanced manufacturing technologies designed to improve carton converting efficiency and support higher levels of product customization.

Key companies operating in the Global Folding Carton Packaging Market include Graphic Packaging International, DS Smith Plc, Smurfit Kappa Group, Stora Enso Oyj, Mayr-Melnhof Karton AG, Huhtamaki Oyj, Georgia-Pacific LLC, Oji Holdings Corporation, Rengo Co., Ltd., Green Bay Packaging Inc., American Carton Company, Diamond Packaging, Meyers, Schur Pack Germany GmbH, August Faller GmbH & Co. KG, Seaboard Folding Box Company Inc., Wynalda Packaging, All Packaging Company, and Plastech Group Ltd. Companies active in the Global Folding Carton Packaging Market are implementing several strategic initiatives to strengthen their competitive position and expand their market presence. Many organizations are investing in advanced converting technologies and automated production lines to improve manufacturing efficiency and reduce operational costs. Expanding sustainable packaging portfolios has become a major priority, with companies developing recyclable and lightweight paperboard materials that align with environmental regulations. Strategic partnerships with consumer goods brands and retail companies allow packaging manufacturers to create customized solutions that meet evolving product packaging requirements. Businesses are also increasing investments in digital printing and design technologies to offer flexible packaging customization and faster product launches.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Carton structure trends

- 2.2.2 Paperboard grade trends

- 2.2.3 Printing technology trends

- 2.2.4 Application trends

- 2.2.5 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Regulatory push toward fiber-based recyclable packaging

- 3.2.1.2 Growth of e-commerce secondary packaging demand

- 3.2.1.3 Shift from plastic clamshells to paperboard cartons

- 3.2.1.4 Pharmaceutical serialization and compliance requirements

- 3.2.1.5 Premiumization in cosmetics and personal care cartons

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Volatility in virgin pulp and paperboard prices

- 3.2.2.2 High capital costs for advanced die-cutting equipment

- 3.2.3 Market opportunities

- 3.2.3.1 Adoption of barrier-coated recyclable paperboard

- 3.2.3.2 Smart packaging integration with QR/NFC features

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

- 3.13 Trade Data Analysis (Based on Paid Databases)

- 3.13.1 Import/Export Volume & Value Trends

- 3.13.2 Key Trade Corridors & Tariff Impact

- 3.14 Impact of AI & Generative AI on the Market

- 3.14.1 AI-Driven Disruption of Existing Business Models

- 3.14.2 GenAI Use Cases & Adoption Roadmap by Segment

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Carton Structure, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Tuck end cartons

- 5.3 Auto-lock / crash bottom cartons

- 5.4 Sleeve cartons

- 5.5 Lock-bottom cartons

- 5.6 Display-ready cartons

- 5.7 Other folding structures

Chapter 6 Market Estimates and Forecast, By Paperboard Grade, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Solid bleached sulfate (SBS)

- 6.3 Coated unbleached kraft (CUK)

- 6.4 Coated recycled paperboard (CRB)

- 6.5 Uncoated paperboard

Chapter 7 Market Estimates and Forecast, By Printing Technology, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Offset lithography

- 7.3 Flexographic printing

- 7.4 Digital printing

- 7.5 Gravure

Chapter 8 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Food & beverage

- 8.3 Personal care & cosmetics

- 8.4 Pharmaceuticals & healthcare

- 8.5 Household & consumer goods

- 8.6 Tobacco

- 8.7 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 DS Smith Plc

- 10.1.2 Graphic Packaging International

- 10.1.3 Huhtamaki Oyj

- 10.1.4 Mayr-Melnhof Karton AG

- 10.1.5 Oji Holdings Corporation

- 10.1.6 Rengo Co., Ltd.

- 10.1.7 Smurfit Kappa Group

- 10.1.8 Stora Enso Oyj

- 10.2 Regional key players

- 10.2.1 North America

- 10.2.1.1 All Packaging Company

- 10.2.1.2 American Carton Company

- 10.2.1.3 Diamond Packaging

- 10.2.1.4 Georgia-Pacific LLC

- 10.2.1.5 Green Bay Packaging Inc.

- 10.2.1.6 Meyers

- 10.2.1.7 Seaboard Folding Box Company Inc.

- 10.2.1.8 Wynalda Packaging

- 10.2.2 Asia Pacific

- 10.2.2.1 Plastech Group Ltd.

- 10.2.3 Europe

- 10.2.3.1 Schur Pack Germany GmbH

- 10.2.1 North America

- 10.3 Niche Players/Disruptors

- 10.3.1 August Faller GmbH & Co. KG

2025-2029年全球摺迭瓦楞纸包装市场

2025-2029年全球摺迭瓦楞纸包装市场 折迭瓦楞纸包装:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

折迭瓦楞纸包装:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 折迭瓦楞纸箱市场规模、份额及成长分析(按材料类型、订单类型、最终用途产业和地区划分)-2026-2033年产业预测

折迭瓦楞纸箱市场规模、份额及成长分析(按材料类型、订单类型、最终用途产业和地区划分)-2026-2033年产业预测 折迭式纸盒市场:未来预测(2025-2030)

折迭式纸盒市场:未来预测(2025-2030) 全球折迭纸盒市场未来展望(至2030年)

全球折迭纸盒市场未来展望(至2030年) 折迭式纸盒包装市场规模、份额、趋势分析报告:按最终用途、地区和细分市场预测,2025-2030 年印尼纸包装:市场占有率分析、行业趋势和成长预测(2025-2030 年)

折迭式纸盒包装市场规模、份额、趋势分析报告:按最终用途、地区和细分市场预测,2025-2030 年印尼纸包装:市场占有率分析、行业趋势和成长预测(2025-2030 年) 折迭式纸盒市场 - 成长、未来展望、竞争分析,2025 年至 2033 年泰国折迭式纸盒包装:市场占有率分析、行业趋势和成长预测(2025-2030 年)全球折迭纸盒包装市场规模:按材料类型、按产品类型、按最终用户、按地区、范围和预测

折迭式纸盒市场 - 成长、未来展望、竞争分析,2025 年至 2033 年泰国折迭式纸盒包装:市场占有率分析、行业趋势和成长预测(2025-2030 年)全球折迭纸盒包装市场规模:按材料类型、按产品类型、按最终用户、按地区、范围和预测