|

市场调查报告书

商品编码

2019039

造粒机市场机会、成长要素、产业趋势分析及2026-2035年预测。Pelletizer Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

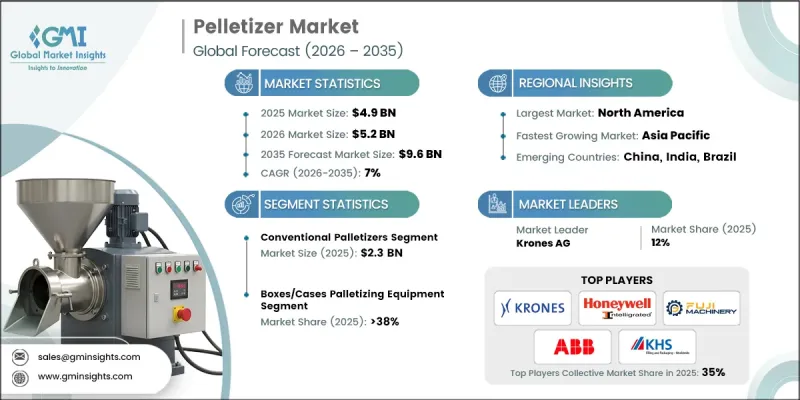

2025年全球造粒机市场价值49亿美元,预计2035年将以7%的复合年增长率成长至96亿美元。

企业正致力于提升营运效率和工作流程的稳定性,这推动了先进造粒系统的应用。曾经被视为生产设备辅助组件的系统,如今已成为管理日常营运和应对日益增长的产量的关键要素。由于供应链日益复杂,以及对营运效率的期望不断提高,企业正在投资易于整合、易于使用且能适应各种生产环境的系统。此外,对职场安全和稳定产量的日益重视也影响着系统设计,製造商正在开发只需极少监控且能与现有设备无缝整合的解决方案。对能够适应不同产品形式的灵活设备的需求不断增长,进一步塑造了市场格局,企业正在寻求兼顾效率和适应性的技术。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测期 | 2026-2035 |

| 上市时的市场规模 | 49亿美元 |

| 预测金额 | 96亿美元 |

| 复合年增长率 | 7% |

预计到2025年,传统造粒机市场规模将达到23亿美元,主要得益于其在高产量、重复性、标准化生产环境中的成本效益。这些系统非常适合稳定的生产条件,并具有可靠的加工能力和较长的运作。与现有生产布局的兼容性进一步巩固了其市场地位,尤其是在基础设施升级面临挑战的工厂中。传统系统的可靠性和耐用性持续推动其在成熟的工业环境中广泛应用。

预计到2025年,纸箱和包装盒市占率将达到38%。该细分市场之所以能保持其主导地位,是因为标准化包装形式在自动化生产和物流流程中得到了广泛应用。其统一的结构使得自动化系统能够有效率地处理并简化操作。专为该细分市场设计的设备能够与其他包装流程有效集成,从而提高整体营运效率。对结构化包装形式的持续依赖,巩固了该细分市场在更广泛的市场格局中的强势地位。

美国造粒机市场占84%的份额,预计2025年市场规模将达到13亿美元。美国之所以能维持主导地位,主要得益于其製造业和物流业自动化程度高。劳动力短缺和安全标准的持续挑战正在加速向自动化解决方案的转型。强大的工业基础设施和对先进技术的持续投资进一步推动了市场成长。成熟的自动化生态系统促进了创新,并支持造粒系统在各行业的广泛应用。

目录

第一章:调查方法

- 研究途径

- 品质改进计划

- GMI人工智慧政策和资料完整性倡议

- 资讯来源一致性协议

- GMI人工智慧政策和资料完整性倡议

- 调查轨迹和置信度评分

- 调查和路线的组成部分

- 评分组成部分

- 数据收集

- 主要来源部分列表

- 资料探勘资讯来源

- 付费资讯来源

- 区域资讯来源

- 付费资讯来源

- 基本估算和计算方法

- 每种方法中基准年的计算

- 预测模型

- 量化市场影响分析

- 生长参数对预测的数学影响

- 量化市场影响分析

- 关于调查透明度的补充信息

- 资讯来源归属框架

- 品质保证指标

- 对信任的承诺

第二章执行摘要

第三章业界考察

- 生态系分析

- 生态系测绘

- OEM

- 积分器

- 最终用户

- 零件供应商

- 相关人员之间的相互依存关係

- 价值链分析(基于初步研究)

- 价值链的各个阶段:製造、分销、安装、售后市场

- 依价值链阶段进行利润率分析

- 价值创造机制

- 生态系测绘

- 影响产业的因素

- 促进因素

- 製造业和仓储业自动化应用日益普及

- 对电子商务和高速物料输送。

- 人们对职场安全和人体工学的兴趣日益浓厚

- 产业潜在风险与挑战

- 高昂的初始投资和整合成本

- 对技术熟练的技工和维修人员的需求

- 机会

- 扩展机器人和协作式码垛解决方案

- 人工智慧、视觉系统和智慧分析的集成

- 促进因素

- 成长潜力分析

- 在具有高成长潜力的地区,商业机会不容错过。

- 高成长领域的机会

- 新兴应用领域

- 未来市场趋势

- 科技与创新趋势

- 新兴科技的发展趋势

- 按技术类型分類的创新蓝图

- 区域技术采纳曲线

- 价格分析(基于初步调查)

- 过去价格趋势分析(2022-2025)

- 以技术类型(机器人与传统自动化)分類的价格波动

- 区域价格趋势

- 监理情势

- 标准和合规要求

- 区域法规结构

- 认证标准

- 贸易资料分析(基于一手调查)(HS编码:8479)

- 进出口量及进口额趋势

- 主要贸易走廊及关税的影响

- 设备的跨境分销模式

- 人工智慧和生成式人工智慧对市场的影响

- 利用人工智慧改造现有堆垛机业务模式

- 生成式人工智慧的应用案例与实施蓝图(预测性维护、路线优化)

- 风险、限制和监管考量

- 波特五力分析

- PESTEL 分析

第四章 竞争情势

- 介绍

- 企业市占率分析

- 企业矩阵分析

- 主要市场公司的竞争分析

- 企业级基准测试(基于初步调查)

- 层级分类标准与选择标准

- 撕裂定位矩阵

- BW Packaging相对于竞争对手的品牌定位

- 竞争定位矩阵

- 主要进展

- 併购

- 伙伴关係和联盟

- 新产品发布

- 业务拓展计划

第五章 市场估算与预测:依产品类型划分,2022-2035年

- 机器人堆垛机

- 关节型机器人(4轴/5轴/6轴)

- 龙门/传送门机器人

- 协作机器人(cobots)

- 传统堆垛机(非机器人型)

- 机械分层剂

- 线上常规系统

- 半自动堆垛机

- 手动码堆垛机

第六章 市场估计与预测:依处理能力划分,2022-2035年

- 低速堆垛机(最大速度 10 箱/分钟)

- 中速堆垛机(10-25箱/分钟)

- 高速堆垛机(25-50箱/分钟)

- 超高速堆垛机

第七章 市场估算与预测:依整合类型划分,2022-2035年

- 独立式堆迭单元

- 整合线上系统

- 生产线末端托盘堆垛

- 多线码垛

- 移动/灵活单元

第八章 市场估计与预测:依应用领域划分,2022-2035年

- 袋装托盘堆迭装置

- 用于纸箱和纸盒的码垛机

- 瓶罐托盘堆迭设备

- 用于桶装和罐装食品的码垛设备

- 托盘堆迭装置

- 混合物料输送系统

- 其他的

第九章 市场估计与预测:依最终用途产业划分,2022-2035年

- 食品/饮料

- 製药

- 消费品

- 建材

- 化学品

- 其他的

第十章 市场估价与预测:依通路划分,2022-2035年

- 直销

- 间接销售

第十一章 市场估价与预测:按地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 其他拉丁美洲地区

- 中东和非洲(MEA)

- 阿拉伯聯合大公国

- 南非

- 沙乌地阿拉伯

- 其他中东和非洲地区

第十二章:公司简介

- ABB Group

- ARPAC LLC

- BEUMER Group GmbH &Co. KG

- Brenton Engineering(part of ProMach)

- Columbia Machine, Inc.

- Fanuc Corporation

- Fuji Machinery Co., Ltd.

- Gebo Cermex(part of Sidel Group)

- Honeywell Intelligrated

- Intralox, LLC(part of Laitram, LLC)

- KHS GmbH

- Krones AG

- Kuka AG

- Premier Tech Chronos

- Schneider Packaging Equipment Co., Inc.

The Global Pelletizer Market was valued at USD 4.9 billion in 2025 and is estimated to grow at a CAGR of 7% to reach USD 9.6 billion by 2035.

Businesses are focusing on streamlining operations and improving workflow consistency, which is driving the adoption of advanced pelletizing systems. What was once considered a supplementary addition to production facilities is now becoming a critical component in managing daily operations and handling increasing production volumes. Rising complexity in supply chains and higher expectations for operational efficiency are encouraging companies to invest in systems that are easy to integrate, user-friendly, and adaptable to different production environments. In addition, the growing emphasis on workplace safety and consistent output is influencing system design, with manufacturers developing solutions that require minimal supervision and fit seamlessly into existing setups. Increasing demand for flexible equipment capable of handling varied product formats is further shaping the market, as businesses seek technologies that balance efficiency with adaptability.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.9 Billion |

| Forecast Value | $9.6 Billion |

| CAGR | 7% |

The conventional pelletizers segment generated USD 2.3 billion in 2025, supported by their ability to deliver cost efficiency in high-volume production environments where operations are repetitive and standardized. These systems are well-suited for consistent production conditions, offering reliable throughput and long operational lifespans. Their compatibility with established manufacturing layouts further strengthens their position, particularly in facilities where upgrading infrastructure may present challenges. The dependability and durability of conventional systems continue to support their widespread adoption across established industrial environments.

The boxes and cases segment accounted for 38% share in 2025. This segment remains dominant due to the widespread use of standardized packaging formats in automated production and logistics processes. Their uniform structure allows for efficient handling and streamlined operations within automated systems. Equipment designed for this segment integrates effectively with other packaging processes, enhancing overall operational efficiency. The continued reliance on structured packaging formats supports the segment's strong position within the broader market landscape.

United States Pelletizer Market held an 84% share, generating USD 1.3 billion in 2025. The country maintains its leadership due to a high level of automation adoption across the manufacturing and logistics sectors. Ongoing challenges related to labor availability and safety standards are accelerating the shift toward automated solutions. Strong industrial infrastructure and continued investment in advanced technologies are further reinforcing market growth. The presence of established automation ecosystems supports innovation and widespread implementation of pelletizing systems across various industries.

Key companies operating in the Global Pelletizer Market include ABB Group, Krones AG, Fanuc Corporation, Kuka AG, BEUMER Group GmbH & Co. KG, Columbia Machine, Inc., Premier Tech Chronos, Schneider Packaging Equipment Co., Inc., Honeywell Intelligrated, ARPAC LLC, Gebo Cermex (part of Sidel Group), Brenton Engineering (part of ProMach), Fuji Machinery Co., Ltd., Intralox, LLC (part of Laitram, LLC), and KHS GmbH. Companies in the Global Pelletizer Market are strengthening their competitive position through technological innovation and strategic expansion initiatives. They are investing in advanced automation technologies to improve system efficiency, flexibility, and ease of integration. Expanding product portfolios to address diverse industry requirements is a key focus area. Businesses are also forming strategic partnerships and collaborations to enhance market reach and improve service capabilities. In addition, companies are emphasizing user-friendly designs and customizable solutions to meet evolving customer demands. Strengthening after-sales support and maintenance services is another important strategy to build long-term customer relationships.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.2 Key Trends

- 2.2.1 Region

- 2.2.2 Product type

- 2.2.3 Handling capacity

- 2.2.4 Integration type

- 2.2.5 Application

- 2.2.6 End use industry

- 2.2.7 Distribution channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Ecosystem mapping

- 3.1.1.1 OEM

- 3.1.1.2 Integrators

- 3.1.1.3 End-users

- 3.1.1.4 Component suppliers

- 3.1.2 Stakeholder interdependence

- 3.1.3 Value chain analysis (Driven by Primary Research)

- 3.1.3.1 Value chain stages: manufacturing, distribution, installation, aftermarket

- 3.1.3.2 Profit margin analysis by value chain stage

- 3.1.3.3 Value capture mechanisms

- 3.1.1 Ecosystem mapping

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising automation adoption across manufacturing and warehousing

- 3.2.1.2 Growing e-commerce and need for high-speed material handling

- 3.2.1.3 Increasing focus on workplace safety and ergonomics

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High initial investment and integration costs

- 3.2.2.2 Need for skilled technicians and maintenance personnel

- 3.2.3 Opportunities

- 3.2.3.1 Expansion of robotic and collaborative palletizing solutions

- 3.2.3.2 Integration of ai, vision systems, and smart analytics

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.3.1 High-growth regional opportunities

- 3.3.2 High-growth segment opportunities

- 3.3.3 Emerging application verticals

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Emerging technology trends

- 3.5.2 Innovation roadmap by technology type

- 3.5.3 Technology adoption curves by region

- 3.6 Pricing analysis (driven by primary research)

- 3.6.1 Historical price trend analysis (2022-2025)

- 3.6.2 Price variation by technology type (Robotic vs Conventional Automated)

- 3.6.3 Regional pricing dynamics

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Trade data analysis (driven by primary research) (HS Code: 8479)

- 3.8.1 Import/Export volume and value trends

- 3.8.2 Key trade corridors and tariff impact

- 3.8.3 Cross-border equipment flow patterns

- 3.9 Impact of AI & generative AI on the market

- 3.9.1 AI-driven disruption of existing palletizer business models

- 3.9.2 GenAI use cases and adoption roadmaps (predictive maintenance, route optimization)

- 3.9.3 Risks, limitations and regulatory considerations

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East and Africa

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Company tier benchmarking (Driven by Primary Research)

- 4.5.1 Tier classification criteria and qualifying thresholds

- 4.5.2 Tier positioning matrix

- 4.5.3 Brands positioning of BW Packaging against Competitors

- 4.6 Competitive positioning matrix

- 4.7 Key developments

- 4.7.1 Mergers & acquisitions

- 4.7.2 Partnerships & collaborations

- 4.7.3 New product launches

- 4.7.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2022 - 2035 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Robotic palletizers

- 5.2.1 Articulated arm robots (4/5/6-axis)

- 5.2.2 Gantry/portal robots

- 5.2.3 Collaborative robots (cobots)

- 5.3 Conventional palletizers (non-robotic)

- 5.3.1 Mechanical layer formers

- 5.3.2 In-line conventional systems

- 5.4 Semi-Automated palletizers

- 5.5 Manual palletizers

Chapter 6 Market Estimates & Forecast, By Handling Capacity, 2022 - 2035 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Low-speed palletizers (up to 10 cases/min)

- 6.3 Medium-speed palletizers (10-25 cases/min)

- 6.4 High-speed palletizers (25-50 cases/min)

- 6.5 Ultra-high-speed palletizers

Chapter 7 Market Estimates & Forecast, By Integration Type, 2022 - 2035 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Standalone palletizing cells

- 7.3 Integrated in-line systems

- 7.4 End-of-line palletizing

- 7.5 Multi-line palletizing

- 7.6 Mobile/flexible units

Chapter 8 Market Estimates & Forecast, By Application, 2022 - 2035 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Bags palletizing equipment

- 8.3 Boxes/cases palletizing equipment

- 8.4 Bottles/containers palletizing equipment

- 8.5 Drums/kegs palletizing equipment

- 8.6 Trays palletizing equipment

- 8.7 Mixed material handling systems

- 8.8 Others

Chapter 9 Market Estimates & Forecast, By End Use Industry, 2022 - 2035 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Food & beverage

- 9.3 Pharmaceuticals

- 9.4 Consumer goods

- 9.5 Building materials

- 9.6 Chemicals

- 9.7 Others

Chapter 10 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035 (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 Direct Sales

- 10.3 Indirect Sales

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035 (USD Billion) (Thousand Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 UK

- 11.3.2 Germany

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Rest of Europe

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 Australia

- 11.4.6 Rest of Asia Pacific

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Rest of Latin America

- 11.6 MEA

- 11.6.1 UAE

- 11.6.2 South Africa

- 11.6.3 Saudi Arabia

- 11.6.4 Rest of MEA

Chapter 12 Company Profiles

- 12.1 ABB Group

- 12.2 ARPAC LLC

- 12.3 BEUMER Group GmbH & Co. KG

- 12.4 Brenton Engineering (part of ProMach)

- 12.5 Columbia Machine, Inc.

- 12.6 Fanuc Corporation

- 12.7 Fuji Machinery Co., Ltd.

- 12.8 Gebo Cermex (part of Sidel Group)

- 12.9 Honeywell Intelligrated

- 12.10 Intralox, LLC (part of Laitram, LLC)

- 12.11 KHS GmbH

- 12.12 Krones AG

- 12.13 Kuka AG

- 12.14 Premier Tech Chronos

- 12.15 Schneider Packaging Equipment Co., Inc.

先进封装:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

先进封装:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 全球先进封装技术市场规模、份额、趋势和成长分析报告(2026-2034年)

全球先进封装技术市场规模、份额、趋势和成长分析报告(2026-2034年) 先进封装市场规模、份额、趋势及预测(按类型、最终用途及地区划分),2026-2034年

先进封装市场规模、份额、趋势及预测(按类型、最终用途及地区划分),2026-2034年 2026年全球先进封装技术市场报告

2026年全球先进封装技术市场报告 先进封装市场规模、份额和成长分析(按类型、最终用途和地区划分):产业预测(2026-2033 年)

先进封装市场规模、份额和成长分析(按类型、最终用途和地区划分):产业预测(2026-2033 年) 先进封装市场:依封装类型、应用、终端用户产业及地区划分

先进封装市场:依封装类型、应用、终端用户产业及地区划分 GMIPulse - 包装市场情报订阅

GMIPulse - 包装市场情报订阅 先进封装技术市场预测(至2032年):按封装技术、互连方法、材料类型、装置架构、最终用户和地区进行的全球分析

先进封装技术市场预测(至2032年):按封装技术、互连方法、材料类型、装置架构、最终用户和地区进行的全球分析 美国饮料包装设备市场:市场规模、份额、趋势分析(按类型、自动化程度和应用)、细分市场预测(2025-2033)下一代封装市场:按封装类型、应用和地区划分

美国饮料包装设备市场:市场规模、份额、趋势分析(按类型、自动化程度和应用)、细分市场预测(2025-2033)下一代封装市场:按封装类型、应用和地区划分