|

市场调查报告书

商品编码

1771254

自动驾驶车辆的4D影像雷达市场 - 产业,市场,竞争分析(2025年版)4D Imaging Radar in Autonomous Vehicles - Industry, Market, and Competition Analysis, Edition 2025 |

||||||

用于 ADAS 和自动驾驶汽车内外感知的 4D 成像雷达,60GHz、76-81GHz、140GHz 频段,SAE 2+ 级及以上应用,新兴 4D 成像公司竞争力评估

重点

- 预计从 2025 年到 2035 年,ADAS 和 AV 雷达模组市场将成长 2.7 倍,复合年增长率为 11.7%,从 2025 年的 90 亿美元增至 2035 年的 250 亿美元。

- 预计到 2035 年,4D 成像雷达模组的渗透率将达到 56% 以上,较目前的市场渗透率激增 45%。

- 到 2035 年,随着自动驾驶汽车的兴起和成本降低,4D 雷达可能在短距离和中距离领域占据主导地位,并在许多 ADAS 和 AV 系统中取代传统的 3D 雷达。

- 由于欧洲新车安全评估协会 (EURO NCAP) 等监管要求,用于乘员监控和儿童遗留检测的车载应用正在成为利基市场增长。

- 台积电、格芯和 imec 开发的 140GHz 雷达技术专注于室内和室外应用的高解析度感测。

- 大陆集团、博世、Vayyar、Arbe、Uhnder、恩智浦和特斯拉等主要参与者正在推动创新,最近在 CES 2025 和 IAA Mobility 2025 上展示了其在分辨率、效率和监管准备方面的进步。

- RFISee、RadSee、Smart Radar System、Zadar Labs、InnoSenT、英飞凌和 Ainstein 是 4D 成像雷达行业值得关注的新创公司。同时,德州仪器 (TI)、恩智浦半导体 (NXP Semiconductors)、意法半导体 (STMicroelectronics)、赛灵思 (Xilinx) 和亚德诺半导体 (ADI) 是领先的片上系统 (SoC) 供应商,正在积极开发 4D 半导体 (ADI) 是领先的片上系统 (SoC) 供应商,正在积极开发 4D 辅助系统解决方案,以支援 ADAS(高阶车辆)和更高的车辆控制系统。

- 一些新创公司,例如 Zendar Inc.,专注于利用 AI 实现动态分辨率的软体定义雷达;Sensrad AB,从 Qamcom 集团分拆出来;Waveye,专注于快速进入市场;Altos Radar,旨在在机器人出租车和城市自动驾驶汽车中率先采用;Altos Radar 正在与中国原始设备製造商(利基、吉利等)进行防电

样品view

全面覆盖

M14 Intelligence 凭藉其在自动驾驶、网联、电动和共享出行领域关键趋势识别方面的核心竞争力,发布了关于 4D 成像雷达技术的研究成果。

- ADAS、自动驾驶汽车、机器人汽车 - 市场展望

- ADAS 和 AV 产业中雷达感测器的现状

- 从自动化等级(ADAS、L2/L2+、L3、L4/L5)、工作范围(短程、中长程)、工作频段(60GHz、76-81GHz、140GHz)等多个角度了解雷达需求和市场规模的潜在变化

- 调变技术 - FMCW 与数位编码调变 (DCM)

- 片上雷达与 MIMO 天线设计

- 基于 AI 的处理

- 用于车载和外部感测的 4D 成像片上雷达感测器的全球市场渗透趋势

- 各地区频率监管与分配的影响

- 4D 成像雷达和感测器套件动态硬体晶片软体解决方案面临的挑战

- 颠覆性趋势正在重塑人工智慧整合、片上雷达和感测器融合等市场挑战

- 高成本和整合复杂性等挑战,以及半导体和软体定义雷达的进步如何应对这些挑战

- 对新兴领导者和新创企业的竞争评估,以及晶片供应商和汽车雷达市场第一线解决方案供应商的策略和市场发展。

市场概览

自动驾驶汽车的 4D成像雷达市场处于汽车技术创新的前沿,推动着高级驾驶辅助系统 (ADAS) 和自动驾驶汽车 (AV) 的发展。预计该市场规模将在 2024 年达到约 20 亿美元,到 2030 年将达到 100 亿美元,复合年增长率为 38%。这得益于对更高安全性、法规要求以及更高级别自动驾驶(SAE 4/5 级)的不断增长的需求。

本报告摘要探讨了雷达感测器在ADAS和AV中的应用、4D雷达取代3D雷达的普及情况、当前和未来的雷达技术及频段、主要参与者和新兴参与者、竞争策略、近期趋势、4D雷达在AV中的关键作用以及机器人出租车和穿梭巴士的市场发展潜力,重点关注亚太地区等前景广阔的地区。

雷达感测器在ADAS和自动驾驶汽车中的应用

雷达感知器在ADAS和AV中至关重要,可实现自适应巡航控制 (ACC)、自动紧急煞车 (AEB)、盲点侦测 (BSD)、车道变换辅助 (LCA) 和儿童存在侦测 (CPD) 等关键功能。与摄影机和雷射雷达不同,雷达在恶劣天气条件(雾、雨、雪等)和低光源条件下表现更佳,可提供可靠的物体侦测和测距。预计到2024年,全球雷达感测器出货量将超过1.69亿个,平均每辆车配备0.8个远端雷达,到2030年将接近1个。自动驾驶计程车,例如Cruise(每辆车配备21个雷达)和Waymo(配备6个高性能4D雷达),已证明其在4/5级自动驾驶中高度依赖雷达,以确保强大的环境感知能力。在消费者对安全性的需求和监管要求(例如,2024年7月欧盟 "车辆通用安全法规" )的推动下,ADAS的普及正在加速雷达在乘用车、商用卡车和自动驾驶班车中的部署。

4D雷达技术取代3D雷达

4D成像雷达在3D雷达的距离、方向和多普勒数据的基础上增加了速度和高度数据,凭藉其卓越的分辨率和精度,正在迅速取代传统雷达。到2025年,4D雷达预计将占据汽车雷达市场的11.4%,并在2-3年内从小众技术发展成为主流技术。与难以实现高程解析度和复杂物体分离(例如区分行人和车辆)的3D雷达不同,4D雷达利用大规模多输入多输出 (MIMO)、数位码调变 (DCM) 和人工智慧驱动的处理技术,产生高解析度点云,在某些应用领域可与雷射雷达相媲美。例如,搭载Drive Pilot系统的宾士EQS和搭载大陆集团ARS540 4D雷达的现代IONIQ 5在低能见度下均表现出色。这种转变源自于3-5级自动驾驶对精准感知的需求,以及对路口行人AEB等高阶安全功能的监管要求。

竞争策略与区域市场机会

现有企业充分利用专注于高解析度雷达和光达/摄影机感测器融合的研发、全球布局以及与原始设备製造商 (OEM) 的合作伙伴关係(例如,博世与大众的合作)。同时,新兴企业则在成本效益设计(RadSee 的 COTS、Uhnder 的 RoC)、AI 整合(Waveye、Zendar)和利基应用(Sensrad 的工业重点)方面脱颖而出。与一级供应商和原始设备製造商 (OEM)(例如,Arbe-BAIC)的合作方式正在加速新进入者的市场准入。

亚太地区是成长最快的地区,其复合年增长率最高,这得益于中国电动车的蓬勃发展和政府对智慧城市的支持。上汽集团和蔚来汽车等公司正在整合 4D 雷达(例如,采埃孚 (ZF) 和上汽集团的合作(2022 年 12 月))。北美市场以美国为主导,占据了最大的销售占有率,福特、通用和特斯拉等汽车製造商在其 BlueCruise、Super Cruise 和 Autopilot 系统中都采用了 4D 雷达。由于严格的安全法规(例如,欧盟 2024 年强制规定),欧洲市场成长强劲。例如,梅赛德斯-奔驰和宝马在 2+/3 级系统方面处于领先地位,而高阶汽车和合规驱动型市场也蕴藏着巨大的机会。

市场机会

包括自动驾驶计程车和接驳车在内的 SAE 4/5 级自动驾驶汽车市场是 4D 雷达的主要成长动力。 Cruise和Waymo 已广泛部署 4D 雷达,预计到 2024 年,其车队规模将超过 1,000 辆,这标誌着商业化自动驾驶计程车服务的兴起。预计到 2035 年,仅 Level 4/5 自动驾驶汽车的全球 4D 雷达市场规模将达到 9.11 亿美元,其中,自动驾驶计程车和接驳车在城市和高速公路上的自动驾驶过程中将消耗大量雷达单元。

机会包括:

- 城市出行:在密集环境中导航对雷达的需求很高(例如,Waveye 的城市专用雷达)。

- 最后一哩配送:自动驾驶接驳车和配送车辆将采用 4D 雷达来确保安全。

- 监管支援:强制性 AEB 和 CPD 将推动雷达整合到 4/5 级自动驾驶系统中。

主要的问题

- SAE 1-5 级自动驾驶汽车中 4D 成像雷达的采用率和趋势如何?

- 到 2035 年,汽车 4D 成像雷达市场的当前市场规模和成长潜力如何?

- 哪些 ADAS 功能(例如 AEB、ACC、BSM)最依赖 4D 雷达?它们如何提升安全性和性能?

- 4D 雷达的成本如何演变(例如 77GHz、60GHz、140GHz)?

- 将 4D 雷达与其他感测器(例如 LiDAR、摄影机)整合以实现稳健的感测器融合面临哪些挑战?

- 全球的频率法规(例如 77GHz、60GHz、140GHz)有何差异?它们将如何影响 4D 雷达的部署?

- 4D 雷达在座舱监控(例如乘员监控和儿童遗留检测)中的作用如何创造市场机会?

- 哪些新兴公司(例如 Arbe、Uhnder、Zendar)正在颠覆 4D 雷达市场?它们有哪些独特的战略?

- 在 4D 雷达市场中,现有企业(大陆集团、博世、恩智浦等)与新兴企业相比,有哪些竞争优势?

- 合作、併购如何塑造 4D 雷达市场?它们将为利害关係人带来哪些机会?

- 哪些投资和融资趋势正在支撑 4D 雷达市场的成长?利害关係人如何利用这些趋势?

取得 4D 成像雷达产业最有趣问题的答案!

企业清单

|

|

目录

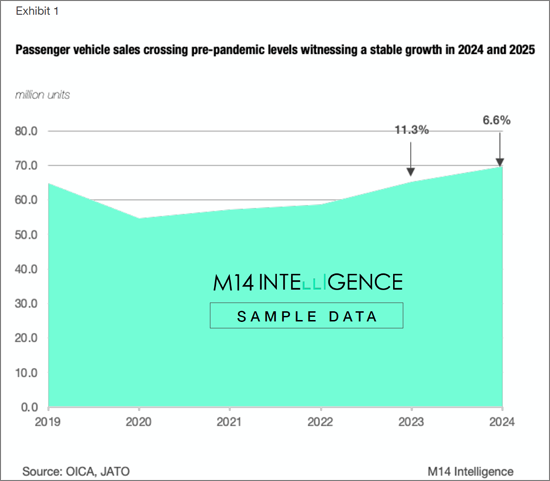

乘用车销售量 - 市场展望

- 全球乘用车销量 (2019-2024)

- 以自动化等级 (L1-L5) 划分的乘用车销量

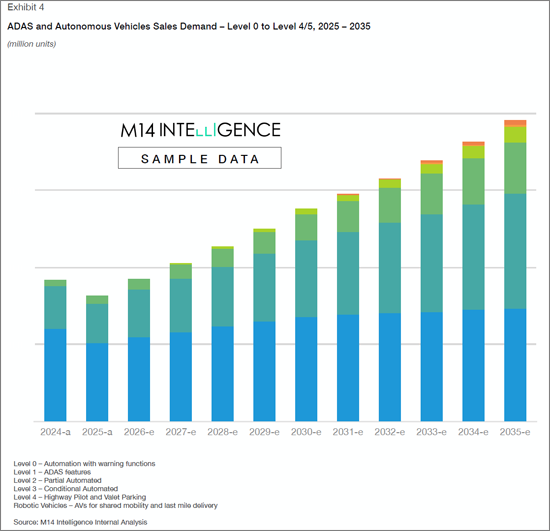

- 2025-2035 年 ADAS 与自动驾驶汽车市场销售及预测

- 中国占据市场主导地位,欧洲具有高成长潜力

- 城市交通、最后一哩配送和监管支援将成为新的收入来源

汽车雷达产业现况 - 2025-2035 年市场展望、产量与价值

- 每辆车的雷达感测器需求

- 雷达平均售价及预期降幅

- 依自动化等级划分的雷达需求

- 依操作范围 (LRR、 MRR/SRR,车内)

- 按频率划分的雷达需求

- 按频率划分的雷达市场渗透率

- 4D 成像雷达快速扩张趋势

汽车 4D 雷达产业 - 市场展望、数量与价值,2025-2035

- 4D 雷达市场 - 按自动化水平划分

- 4D 雷达市场 - 按 ADAS 和 AV 应用划分

- 用于外部感测应用的 4D 成像雷达

- 用于车载应用的 4D 成像雷达

汽车 4D 雷达产业 - 竞争评估

- 汽车 4D 雷达应用领域的新兴公司概况

- 产品比较与基准分析

- 合作伙伴图谱与供应商分析

- 汽车产业的 OEM、一级供应商和感测器供应商4D雷达业务

- 重点公司研发投入

- 4D雷达业务新创企业的融资及投资分析

In-cabin and Exterior Sensing Applications of 4D imaging radar in ADAS and Autonomous Vehicles; 60 GHz, 76-81 GHz, and 140 GHz Band, SAE Level 2+ and above applications, Emerging 4D imaging players competition assessment.

Key Highlights

- ADAS and AV radar module market size anticipated to grow 2.7x times between 2025 to 2035, accounting $25 billion in 2035 from $9 billion by 2025 at a CAGR of 11.7 percent

- 4D imaging radar modules expected to penetrate over 56 percent by 2035, a jump of 45% from the current market penetration

- By 2035, with the rise of autonomous vehicles and cost reductions, 4D radar could dominate short- and medium-range applications, potentially replacing conventional 3D radar in many ADAS and AV systems

- The in-cabin applications of occupant monitoring and left-child detection is a growing niche due to regulatory mandates like those from EURO NCAP

- Development of 140 GHz radar technology by TSMC, GlobalFoundries, and imec focuses on high-resolution sensing for both interior and exterior applications, though not yet commercialized, the technology is expected to strongly compete with 77GHz system by 2035

- Leading companies like Continental, Bosch, Vayyar, Arbe, Uhnder, NXP, and Tesla are driving innovation, with recent showcases at CES 2025 and IAA Mobility 2025 highlighting advancements in resolution, efficiency, and regulatory compliance.

- RFISee, RadSee, Smart Radar System, Zadar Labs, InnoSenT, Infineon, and Ainstein are prominent emerging players in the 4D imaging radar industry. Meanwhile, Texas Instruments, NXP Semiconductors, STMicroelectronics, Xilinx, and Analog Devices are leading System-on-Chip (SoC) providers actively developing 4D imaging radar solutions to support Advanced Driver Assistance Systems (ADAS) and higher levels of vehicle automation.

- Emerging start-ups such as Zendar Inc. focusing on software-defined radar with AI for dynamic resolution, Sensrad AB is a spin-out from Qamcom Group, focusing on rapid market entry, Waveye is targeting early adoption in robotaxis and urban AVs, Altos Radar partnering with Chinese OEMs (e.g., SAIC, Geely) for regional expansion, Xavveo is targeting niche markets like autonomous shuttles and industrial applications

SAMPLE VIEW

Countries Covered: Global (China, India, Japan, South Korea, US, Canada, South America, Germany, France, Italy, UK, Israel, others).

Exhaustive Coverage

M14 Intelligence with its core capabilities in understanding the key trends of autonomous, connected, electric, and shared mobility published the research on 4D imaging radar technology which talks about following important factors of the market.

- ADAS, Autonomous and Robotic Vehicles - Market Outlook

- Status of radar sensors in the ADAS and AV industry

- Understanding the potential change in the radar demand and its market size from different perspectives including - automation levels (ADAS, Level 2/2+, Level 3 and Level 4/5), range of operations (short, medium-long), and frequency band of operation (60 GHz, 76-81 GHz , and 140GHz)

- Modulation Techniques- FMCW and Digital Code Modulation (DCM)

- Radar-on-Chip and MIMO antenna design

- AI-based processing

- Market penetration trend of 4D imaging radar-on-chip sensors for in-cabin and world-facing exterior sensing applications

- Impact of frequency regulations and allocations across different geographies

- 4D imaging radar hardware chip and software solutions and how it is expected to challenge the sensor suite dynamics

- Disruptive trends like AI integration, radar-on-chip, and sensor fusion that will reshape the market

- Challenges like high costs and integration complexities, and how advancements in semiconductors and software-defined radar are addressing these hurdles

- Competition assessment of emerging leaders and start-ups, along with the strategies and developments of chip providers and tier-1s offering solutions in automotive radar market.

Market Overview

The 4D imaging radar market for autonomous vehicles is at the forefront of automotive innovation, driving the evolution of Advanced Driver Assistance Systems (ADAS) and autonomous vehicles (AVs) . Valued at approximately USD 2 billion in 2024, the market is projected to reach USD 10 billion by 2030, with a CAGR of 38%, fueled by the increasing demand for enhanced safety, regulatory mandates, and the push for higher autonomy levels (SAE Level 4/5).

This report summary explores the adoption of radar sensors in ADAS and AVs, the penetration of 4D radar replacing 3D radar, current and future radar technologies and frequency bands, leading and emerging players, competitive strategies, recent developments, the critical role of 4D radar in AVs, and market potential for robotaxis and shuttles, with a focus on high-potential regions like Asia-Pacific.

Adoption of Radar Sensors in ADAS and Autonomous Vehicles

Radar sensors are integral to ADAS and AVs, enabling critical features like Adaptive Cruise Control (ACC), Automatic Emergency Braking (AEB), Blind Spot Detection (BSD), Lane Change Assist (LCA), and Child Presence Detection (CPD) . Unlike cameras and LiDAR, radar excels in adverse weather conditions (e.g., fog, rain, snow) and low-light scenarios, providing reliable object detection and ranging. In 2024, over 169 million radar sensors were shipped globally, with an average of 0.8 long-range radars per vehicle in 2024, expected to approach 1 per vehicle by 2030. Robotaxis, such as Cruise (21 radars per vehicle) and Waymo (six high-performance 4D radars), demonstrate heavy reliance on radar for Level 4/5 autonomy, ensuring robust environmental perception. The rising adoption of ADAS, driven by consumer demand for safety and regulatory mandates (e.g., EU's Vehicle General Safety Regulations, July 2024), is accelerating radar deployment across passenger vehicles, commercial trucks, and autonomous shuttles.

Penetration of 4D Radar Technology Replacing 3D Radars

4D imaging radar, which adds velocity and elevation to the range, azimuth, and Doppler data of 3D radar, is rapidly replacing its predecessor due to superior resolution and accuracy. By 2025, 4D radar is expected to penetrate 11.4% of the automotive radar market, transitioning from a niche to a mainstream technology within 2-3 years. Unlike 3D radar, which struggles with elevation resolution and complex object separation (e.g., distinguishing a pedestrian from a vehicle), 4D radar leverages Massive MIMO, Digital Code Modulation (DCM) , and AI-driven processing to create high-resolution point clouds, rivaling LiDAR in some applications. For instance, Mercedes-Benz EQS with Drive Pilot and Hyundai IONIQ 5 with Continental's ARS540 4D radar showcase enhanced performance in poor visibility. The shift is driven by the need for precise perception in Level 3-5 autonomy and regulatory requirements for advanced safety features like Junction Pedestrian AEB.

Competitive Strategies and regional market opportunities

Established players leverage R&D, global presence, and OEM partnerships (e.g., Bosch's collaboration with Volkswagen) focusing on high-resolution radar and sensor fusion with LiDAR/cameras. On the other hand, start-ups differentiate through cost-effective designs (RadSee's COTS, Uhnder's RoC), AI integration (Waveye, Zendar), and niche applications (Sensrad's industrial focus). A collaborative approach is wherein partnership with Tier 1s and OEMs (e.g., Arbe-BAIC) is accelerating market entry for new players.

Asia-Pacific is the fastest-growing region with the highest CAGR, driven by China's EV boom and government support for smart cities. Companies like SAIC and NIO integrate 4D radar (e.g., ZF's partnership with SAIC, Dec 2022). Opportunities lie in mass-market EVs and robotaxi fleets in urban centers like Shanghai. North America holds largest revenue share, led by the US with OEMs like Ford, GM, and Tesla adopting 4D radar for BlueCruise, Super Cruise, and Autopilot. Europe shows strong growth due to stringent safety regulations (e.g., EU's 2024 mandates). For instance, Mercedes-Benz and BMW lead with Level 2+/3 systems and opportunities are evidently reflected in premium vehicles and compliance-driven markets.

Market Potential

The market for SAE Level 4/5 AVs, including robotaxis and shuttles, is a key growth driver for 4D radar. By 2035, the AV segment is expected to exhibit the highest CAGR (127%) from 2025 to 2035 within the 4D radar market, driven by the need for multiple high-performance radars (6-21 per vehicle). Cruise and Waymo deploy 4D radar extensively, with fleets exceeding 1,000 vehicles in 2024, signaling commercial robotaxi services' rise. The global 4D radar market is projected to reach USD 911 million by 2035 for Level 4/5 AVs alone, with robotaxis and shuttles consuming significant radar units for urban and highway autonomy.

Opportunities include:

- Urban Mobility: High radar demand for navigating dense environments (e.g., Waveye's urban-focused radar).

- Last-Mile Delivery: Autonomous shuttles and delivery vehicles adopting 4D radar for safety.

- Regulatory Support: Mandates for AEB and CPD boost radar integration in Level 4/5 systems.

Key Questions Answered:

- How rapidly is 4D imaging radar penetrating autonomous vehicles across SAE Levels 1-5, and what are the adoption trends?

- What is the current market size and growth potential of the 4D imaging radar market for automotive applications through 2035?

- Which ADAS features (e.g., AEB, ACC, BSM) are most reliant on 4D radar, and how do they enhance safety and performance?

- How are 4D radar costs (e.g., 77 GHz, 60 GHz, 140 GHz) evolving, and what factors drive cost erosion for mass production?

- What are the challenges of integrating 4D radar with other sensors (e.g., LiDAR, cameras) for robust sensor fusion?

- How do frequency regulations (e.g., 77 GHz, 60 GHz, 140 GHz) vary globally, and what impact do they have on 4D radar deployment?

- How 4D radar's role in in-cabin monitoring applications of occupant monitoring and left-child detection is creating market opportunity?

- Which emerging startups (e.g., Arbe, Uhnder, Zendar) are disrupting the 4D radar market, and what are their unique strategies?

- What are the competitive advantages of established players (e.g., Continental, Bosch, NXP) versus emerging startups in the 4D radar market?

- How are partnerships, mergers, and acquisitions shaping the 4D radar market, and what opportunities do they create for stakeholders?

- What investment and funding trends are supporting the growth of the 4D radar market, and how can stakeholders capitalize on them?

Get answers to the most intriguing questions in the 4D imaging radar industry!

List of Companies

|

|

Table of Contents

Passenger Vehicle Sales - Market Outlook

- Global Passenger Vehicle Sales, 2019-2024

- Passenger Vehicle Sales Breakdown, by Level of Automation, L1 to L5

- ADAS and Autonomous Vehicle Market sales and forecast, 2025-2035

- China dominating the market while Europe holds strong growth potential

- Urban mobility, last-mile delivery and regulatory support will be the new revenue pockets

Status of Automotive Radar Industry - Market Outlook Volume & Value, 2025-2035

- Radar Sensor requirement per vehicle

- ASP of Radar and Expected Price Erosion

- Radar Demand by Levels of Automation

- Radar Demand by Range of Operation (LRR, MRR/SRR, In-cabin)

- Radar Demand by Frequency

- Radar Market Penetration by Frequency

- Trend towards 4D Imaging Radar is Growing Rapidly

Automotive 4D Radar Industry - Market Outlook Volume & Value, 2025-2035

- 4D Radar Market - Split by Levels of Automation

- 4D Radar Market - Split by ADAS and AV Applications

- 4D Imaging Radar for Exterior Sensing Application

- 4D Imaging Radar for In-cabin Application

Automotive 4D Radar Industry - Competition Assessment

- Profiles of Emerging Companies in Automotive 4D Radar Application

- Product Comparison and Benchmarking

- Partnership Mapping and Supplier Analysis

- OEMs, Tier-1s, and Sensor Suppliers in 4D Radar Business

- Investment in R&D by leading players

- Funding and Investment Analysis of Start-ups in 4D Radar Business

汽车4D雷达产业(2025)

汽车4D雷达产业(2025) 汽车影像处理市场规模、份额、成长分析(按产品类型、车辆类型、自动化程度、应用、成像技术和地区划分)-2025-2032年产业预测

汽车影像处理市场规模、份额、成长分析(按产品类型、车辆类型、自动化程度、应用、成像技术和地区划分)-2025-2032年产业预测 自规则系统成像雷达的专利形势的分析(2025年)

自规则系统成像雷达的专利形势的分析(2025年) 汽车影像感测器市场 - 预测 2025-2030

汽车影像感测器市场 - 预测 2025-2030 全球4D成像雷达市场

全球4D成像雷达市场 4D 成像雷达市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

4D 成像雷达市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测 全球 4D 成像雷达市场(至 2030 年)按范围(短程、中程、远距)、应用(ADAS、安全与监控、病患诊断与监控)和最终用户(汽车、航太与国防、医疗保健、工业)划分

全球 4D 成像雷达市场(至 2030 年)按范围(短程、中程、远距)、应用(ADAS、安全与监控、病患诊断与监控)和最终用户(汽车、航太与国防、医疗保健、工业)划分 4D成像雷达市场,规模,占有率,趋势,产业分析报告:各类型,各用途,各地区 - 2025~2034年的市场预测

4D成像雷达市场,规模,占有率,趋势,产业分析报告:各类型,各用途,各地区 - 2025~2034年的市场预测 2025年全球汽车4D成像雷达市场报告2025年四维(4D)成像雷达全球市场报告

2025年全球汽车4D成像雷达市场报告2025年四维(4D)成像雷达全球市场报告