|

市场调查报告书

商品编码

1403921

智慧工厂:市场占有率分析、产业趋势与统计、2024年至2029年成长预测Smart Factory - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

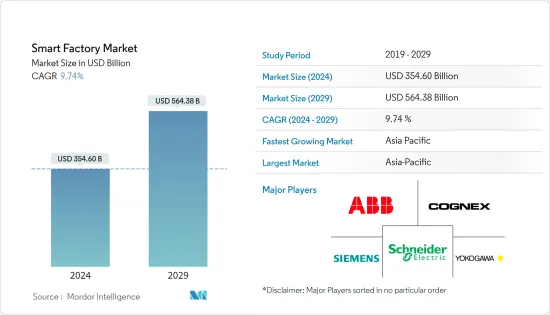

智慧工厂市场规模预计到2024年为3,546亿美元,预计到2029年将达到5,643.8亿美元,在预测期内(2024-2029年)复合年增长率为9.74%。

主要亮点

- 随着工业 4.0 和物联网 (IoT) 的核准,製造业发生了重大转变,迫使企业变得更加灵活、更具创新性和创造性,以便透过自动化补充和扩展人力的技术来推动生产,并减少因工业事故而造成的事故。处理故障必须采用方法。随着互联设备和感测器的采用率不断提高,促进了 M2M通讯,我们看到製造业中开发的资料点数量呈爆炸式增长。

- 根据 Zebra 的製造愿景研究,基于物联网和 RFID 的智慧资产追踪解决方案将在 2022 年取代基于电子表格的传统方法。根据玛丽维尔大学的计算,到 2025 年,全球每年将产生超过 180 兆千兆位元组的资料。其中大部分是由工业物联网支援的产业产生的。此外,工业IoT(IIoT) 公司 Microsoft 的一项研究发现,85% 的公司至少拥有一个 IIoT 用例计划。随着约 95% 的受访者将在 2022 年实施 IIoT 策略,这一数字有所增加。

- 技术进步加上製造设施开拓的持续增加预计将影响预测期内的市场成长率。例如,英特尔最近与义大利电信和硬体製造商 Exor International 合作开发使用人工智慧 (AI) 和 5G 网路的智慧製造设施。

- 此外,人工智慧和机器学习(ML)技术的市场渗透加速将提高资料分析的准确性和速度,从而显着推动市场发展。此外,现场设备市场、机器人和感测器的进步可能会进一步扩大研究市场的范围。根据思科预测,到 2022 年,支援物联网应用的机器对机器 (M2M) 连接可能占全球 285 亿连接装置的 50% 以上。许多政府也鼓励製造业投资物联网技术来实施智慧工厂。

- 然而,高昂的安装成本对市场成长构成了挑战。此外,需要高技能的劳动力来操作和维护自动化基础设施,这进一步增加了整体成本,并阻碍了大规模招聘,尤其是在中小型产业。

- 此外,近期经济不稳定,特别是受疫情和美国贸易争端、俄罗斯乌克兰战争等地缘政治问题影响,也导致各地区营商环境存在不确定性,也对供应链造成影响。以及各地区工业部门对製成品的需求,为研究市场的成长创造了不利的环境。

智慧工厂市场趋势

半导体产业可望推动市场成长

- 半导体製造商依靠智慧製造流程来产生更高的产量比率和利润。透过推进半导体创新并鼓励进一步实施由先进晶片驱动的创新技术,随着工厂变得更加复杂和互联,製造商将能够调整生产以满足不断增长的需求。您可以尝试迎头赶上。

- 半导体製造工厂 (fabs) 的建设和维护成本达数十亿美元。成本在于设备,维护对于持续运作至关重要。透过使用创新的製造技术来监控设备健康状况并执行预测性维护,工厂可以大幅减少非计划性维护时间。

- 全球半导体製造工厂的数量正在增加。半导体行业协会也报告称,新半导体设备的支出增加。这些因素也可能推动半导体产业智慧工厂的采用。根据半导体产业协会(SIA)预测,2022年全球半导体销售额将达5,801.3亿美元。半导体是电子设备的重要零件,产业竞争激烈。 2022年年与前一年同期比较达4.4%。此外,2022年3月欧洲半导体销售额为46.3亿美元,较上个月的45.1亿美元略有成长。

- 此外,该地区各国都致力于透过提供税收减免、资金、补贴和其他型态援助的政府政策来鼓励半导体製造。例如,据政府称,2020 年印度半导体产业价值为 150 亿美元,预计到 2026 年将成长至 630 亿美元(资料来源:电子和资讯技术部)。随着政府对半导体製造及相关产业的干预,印度有望成为全球半导体供应链的领先国家之一。

- 此外,2022 年 9 月,矿业集团 Vedanta 和台湾电子製造巨头富士康进行了有史以来最大的投资之一,投资 18.6 亿美元,在古吉拉突邦建立印度第一家半导体工厂。此类投资可能会在所研究的市场中创造更大的需求。

- 此外,半导体产业正在不断发展,以满足人工智慧主导的电子设备和自动驾驶汽车和物联网等项目对半导体材料日益增长的需求。汽车导航、安全和资讯娱乐解决方案中使用的电子元件消费的成长将再次促进半导体产业的成长。

亚太地区市场将实现显着成长

- 亚太地区是研究市场投资强劲的地区。各国政府持续采取倡议加强智慧製造和技术采用。此外,印度政府的国家製造业政策目标是到2025年将製造业占GDP的比重提高到25%。此外,印度政府的「印度製造」政策预计将增加当地製造业对机械和工具的需求和消费。

- 此外,2022年1月,Reliance向Adverb Technologies投资1.32亿美元,收购54%的股份。这些市场投资预计将加速製造业自动化的采用,并在预测期内推动智慧工厂市场的发展。

- 中国是亚洲智慧型应用转型的重要参与者。中国政府正在加强智慧製造设计,在标准体系建设方面进行多种规划和示范。中国的目标是到2025年创造40项製造业创新成果。重点领域包括自动化工具机和机器人、先进资讯技术、航太航空装备、海洋装备、现代轨道交通装备、高技术船舶、新能源汽车及装备、电力装备、农业装备、新材料、生物製药等。和先进的医疗产品。

- 此外,2022年1月,自动化专家ABB与中国最重要的汽车零件供应商华域汽车宣布成立合资公司,推动中国汽车产业下一代智慧生产。该合资企业建立在两家公司成功合作伙伴关係的基础上,代表着华域汽车中国业务在生产弹性且永续的汽车零件方面的重要发展。

- 此外,日本正快速迈向“社会5.0”,这个全新的超级智慧社会将迎来人类发展四大阶段的第五章。一切都透过物联网技术连接起来,所有技术都整合在一起,生活品质正在显着提高。此外,日本政府还宣布推出连网型工业以响应德国政府的工业 4.0 计划,新的製造业革命的势头正在增强。

- 此外,韩国商业和公共部门已同意增加该地区智慧工厂的数量,并计划在 2022 年将超过 30,000 家采用最新数位和分析技术的工厂投入运作。韩国产业通商资源部 (MOTIE) 重申政府愿意协助中小企业采用和扩展智慧製造技术。中小企业(SME)占韩国所有企业的99%以上,政府资料显示中小企业出口正在成长。

智慧工厂产业概况

智慧工厂市场较为分散,主要企业包括ABB有限公司、康耐视公司、西门子公司、Schneider Electric公司及横河电机。市场参与者正在采取创新、合作、併购和收购等策略来改善其产品供应并获得永续的竞争优势。

2023年3月,工业自动化和能源管理数位解决方案供应商Schneider Electric在匈牙利新建的智慧工厂破土动工。投资额为4,000万欧元(4,300万美元),用地面积25,000平方公尺,员工人数约500人。

2023年3月,领先的消费电子製造商三星电子宣布计画扩大投资,在诺伊达的行动电话製造厂安装智慧製造能力。该公司还宣布计划扩大国内研发设施,以实现具有竞争力的本地生产。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买方议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争强度

- 产业价值链分析

- 评估宏观经济趋势对市场的影响

第五章市场动态

- 市场驱动因素

- 在整个价值链中扩大物联网 (IoT) 技术的采用

- 对能源效率的需求不断增长

- 市场抑制因素

- 庞大资金投入转型

- 容易受到网路攻击

第六章市场区隔

- 依产品类型

- 机器视觉系统

- 相机

- 处理器

- 软体

- 外壳

- 影像撷取卡

- 整合服务

- 照明

- 工业机器人

- 关节式机器人

- 笛卡儿机器人

- 圆柱形机器人

- SCARA机器人

- 并联机器人

- 协作工作机器人

- 控制设备

- 继电器和交换器

- 伺服马达及驱动器

- 感应器

- 通讯科技

- 有线

- 无线的

- 其他产品类型

- 机器视觉系统

- 依技术

- 产品生命週期管理 (PLM)

- 人机介面 (HMI)

- 企业资源规划(ERP)

- 製造执行系统(MES)

- 集散控制系统(DCS)

- 监控和资料采集 (SCADA)

- 可程式逻辑控制器(PLC)

- 其他技术

- 按最终用户产业

- 车

- 半导体

- 油和气

- 化工/石化

- 製药

- 航太/国防

- 食品与饮品

- 矿业

- 其他最终用户产业

- 按地区

- 北美洲

- 美国

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 欧洲其他地区

- 亚太地区

- 中国

- 印度

- 日本

- 其他亚太地区

- 拉丁美洲

- 巴西

- 阿根廷

- 墨西哥

- 其他拉丁美洲

- 中东/非洲

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 南非

- 其他中东/非洲

- 北美洲

第七章竞争形势

- 公司简介

- ABB Ltd

- Cognex Corporation

- Siemens AG

- Schneider Electric SE

- Yokogawa Electric Corporation

- KUKA AG

- Rockwell Automation Inc.

- Honeywell International Inc.

- Robert Bosch GmbH

- Mitsubishi Electric Corporation

- Fanuc Corporation

- Emerson Electric Co.

- FLIR Systems Inc.(Teledyne Technologies Incorporated)

第八章投资分析

第9章市场的未来

The Smart Factory Market size is estimated at USD 354.60 billion in 2024, and is expected to reach USD 564.38 billion by 2029, growing at a CAGR of 9.74% during the forecast period (2024-2029).

Key Highlights

- Tremendous shifts in manufacturing due to Industry 4.0 and the approval of IoT require enterprises to adopt agile, more innovative, and creative ways to advance production with technologies that complement and augment human labor with automation and reduce industrial accidents caused by process failure. With the increased rate of adoption of connected devices and sensors and the fostering of M2M communication, a surge in the data points that are developed in the manufacturing industry is being observed.

- According to Zebra's Manufacturing Vision Study, smart asset-tracking solutions based on IoT and RFID overtook traditional, spreadsheet-based methods in 2022. Maryville University calculates that by 2025, more than 180 trillion gigabytes of data are anticipated to be created worldwide yearly. IIoT-enabled industries will generate a large portion of this. In addition, an Industrial IoT (IIoT) company Microsoft Corporation survey found that 85 percent of companies have at least one IIoT use case project. This number increased, as approx 95 percent of respondents implemented IIoT strategies in 2022.

- Incremental advancement in technology, coupled with a sustained increase in the development of manufacturing facilities, is expected to impact the market growth rate during the forecast period. For instance, Intel has recently partnered with Telecom Italia and hardware manufacturer Exor International to develop a smart manufacturing facility that uses artificial intelligence (AI) and 5G networking.

- Furthermore, the glowing market penetration of AI and machine learning (ML) technologies may enhance the accuracy and speed of data analysis, thereby significantly driving the market forward. Moreover, the advancement in the field devices market, robots, and sensors may further expand the scope of the studied market. According to Cisco projections, by 2022, machine-to-machine (M2M) connections that support IoT applications may have accounted for more than 50 percent of the world's 28.5 billion connected devices. Many governments also motivate manufacturing companies to invest in IoT technologies for smart factory adoption, which creates a favorable outlook for the growth of the studied market.

- However, a high installation cost is the primary factor challenging the market's growth. Additionally, the requirement of a highly skilled workforce to operate and maintain the automation infrastructure further adds to the overall cost, restraining mass adoption, especially in small and medium-scale industries.

- Additionally, the recent economic instability, especially as an outcome of the pandemic and geo-political issues such as the US-China trade dispute and the Russia-Ukraine war, is also challenging the studied market's growth as it has not only led to an uncertain business environment across various regions but are also impacting the supply chain of industrial sectors and demand for manufactured products across various region, leading to an unfavorable environment for the studied market's growth.

Smart Factory Market Trends

Semiconductor Sector is Expected to Drive the Market Growth

- Semiconductor manufacturers rely on smart manufacturing processes to produce higher yields and margins. By advancing semiconductor innovation and encouraging the further implementation of innovative technologies powered by advanced chips, manufacturers can ensure that production keeps pace with rising demand as factories become more complex and connected.

- Semiconductor fabrication plants, or fabs, cost billions of dollars to build and maintain. The cost goes on equipment, the maintenance of which is vital to ongoing operation. By using innovative manufacturing technologies to observe equipment health and execute predictive maintenance, fabs can decrease unplanned maintenance time significantly.

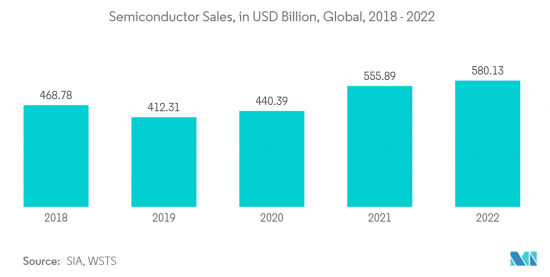

- The semiconductor fabrication plants globally are on the rise. Also, the Semiconductor Industry Association reported increased spending on new semiconductor equipment. These factors will also drive the adoption of smart factories in the semiconductor industry. According to the Semiconductor Industry Association (SIA), in 2022, semiconductor sales reached USD 580.13 billion worldwide. Semiconductors are crucial components of electronic devices, and the industry is highly competitive. The year-on-year growth rate in 2022 reached 4.4 percent. Additionally, semiconductor sales in Europe in March 2022 were USD 4.63 billion, up slightly from last month's figures, which recorded USD 4.51 billion.

- Moreover, various countries in this region are focused on encouraging semiconductor manufacturing through government policies offering tax breaks, money, subsidies, and other forms of assistance. For instance, according to the government, the Indian semiconductor sector was valued at USD 15 billion in 2020 and is anticipated to grow to USD 63 billion by 2026 (Source: Ministry of Electronics & IT). Through governmental intervention in the manufacturing of semiconductors and the peripheral sector, India is expected to become one of the leading countries in global semiconductor supply chains.

- In addition, in September 2022, mining conglomerate Vedanta and Taiwanese electronics manufacturing giant Foxconn made one of the largest ever investments of USD 1,860 million to set up India's first semiconductor plant in Gujarat. Such investment may further create significant demand in the studied Market.

- Besides, the semiconductor industry is growing to accommodate the rising demand for semiconductor materials in AI-driven electronics and programs such as autonomous vehicles and IoT. The growth in the consumption of electronic components utilized in the navigation of automobiles, safety, and infotainment solutions intention again contribute to the semiconductor industry's growth.

Asia-Pacific to Experience Significant Market Growth

- Asia-Pacific significantly invests in the studied Market. Governments continuously take the initiative to enhance smart manufacturing and technology adoptions in various countries. In addition, the National Manufacturing Policy of the Government of India aims to improve the share of manufacturing in GDP to 25 percent by 2025. Also, the "Make in India" policy of the Government of India is anticipated to increase the demand and consumption of machinery and tools by the local manufacturing industry.

- Moreover, in January 2022, Reliance invested USD 132 million in Addverb Technologies to acquire a 54 percent stake. Such investments in the Market are expected to fuel the adoption of automation in the manufacturing industry, thereby fueling the smart factory market during the forecast period.

- China is an integral part of Asia's rising shift to intelligent applications. The Chinese government has strengthened the design of smart manufacturing by implementing various schemes and demonstrations in developing standard systems. China aims to create 40 manufacturing innovations by 2025. The focus areas include automated machine tools and robotics, new advanced information technology, aerospace and aeronautical equipment, marine equipment, modern rail transport equipment, high-tech shipping, new-energy vehicles and equipment, power equipment, agricultural equipment, new materials, biopharma, and advanced medical products.

- Further, in January 2022, ABB, an automation expert, and HASCO, China's most significant automotive components supplier, announced the construction of a joint venture to push China's automotive industry's next generation of smart production. The joint venture will build on the two businesses' successful partnership, resulting in the vital development of highly flexible and sustainable car parts production within HASCO's China operations.

- Furthermore, Japan is rapidly moving toward "Society 5.0", thus introducing the fifth chapter to the four major stages of human development in this new ultra-smart society. All things are connected through IoT technology, and all technologies are getting integrated, dramatically improving the quality of life. Further, the Japanese government announced connected industries in response to the German government's "Industry 4.0" program, and the momentum for a new manufacturing revolution is rising.

- Further, Korea's commercial and public sectors have agreed to boost the number of local smart factories, intending to have more than 30,000 of them working with the newest digital and analytical technology by 2022. Korea's Ministry of Trade, Industry, and Energy (MOTIE) has reaffirmed the government's ambitions to assist small and medium-sized businesses in adopting and expanding smart manufacturing technology. Small and medium-sized firms (SMEs) account for more than 99 percent of all companies in Korea, and government data suggests that SMEs' exports are growing.

Smart Factory Industry Overview

The smart factory market is fragmented, with significant players like ABB Ltd, Cognex Corporation, Siemens AG, Schneider Electric SE, and Yokogawa Electric Corporation. Players in the market are adopting strategies such as innovations, partnerships, mergers, and acquisitions to improve their product offerings and achieve sustainable competitive advantage.

In March 2023, Schneider Electric, a solution provider for the digital transformation of industrial automation and energy management, broke ground on its new smart factory in Hungary. With an expected investment of EUR 40 million (USD 43 million), the new site will span 25,000 m2 with a headcount of about 500 employees.

In March 2023, Samsung Electronics, a leading consumer electronic device manufacturer, announced its plans to increase investment in setting up smart manufacturing capabilities at its mobile phone manufacturing plant in Noida. The company also announced its plans to expand its research and development facility in the country to make production more competitive and localized.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competition

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of Impact of Macroeconomic Trends on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Adoption of Internet of Things (IoT) Technologies Across the Value Chain

- 5.1.2 Rising Demand for Energy Efficiency

- 5.2 Market Restraints

- 5.2.1 Huge Capital Investments for Transformations

- 5.2.2 Vulnerable to Cyberattacks

6 MARKET SEGMENTATION

- 6.1 By Product Type

- 6.1.1 Machine Vision Systems

- 6.1.1.1 Cameras

- 6.1.1.2 Processors

- 6.1.1.3 Software

- 6.1.1.4 Enclosures

- 6.1.1.5 Frame Grabbers

- 6.1.1.6 Integration Services

- 6.1.1.7 Lighting

- 6.1.2 Industrial Robotics

- 6.1.2.1 Articulated Robots

- 6.1.2.2 Cartesian Robots

- 6.1.2.3 Cylindrical Robots

- 6.1.2.4 SCARA Robots

- 6.1.2.5 Parallel Robots

- 6.1.2.6 Collaborative Industry Robots

- 6.1.3 Control Devices

- 6.1.3.1 Relays and Switches

- 6.1.3.2 Servo Motors and Drives

- 6.1.4 Sensors

- 6.1.5 Communication Technologies

- 6.1.5.1 Wired

- 6.1.5.2 Wireless

- 6.1.6 Other Product Types

- 6.1.1 Machine Vision Systems

- 6.2 By Technology

- 6.2.1 Product Lifecycle Management (PLM)

- 6.2.2 Human Machine Interface (HMI)

- 6.2.3 Enterprise Resource and Planning (ERP)

- 6.2.4 Manufacturing Execution System (MES)

- 6.2.5 Distributed Control System (DCS)

- 6.2.6 Supervisory Controller and Data Acquisition (SCADA)

- 6.2.7 Programmable Logic Controller (PLC)

- 6.2.8 Other Technologies

- 6.3 By End-user Industry

- 6.3.1 Automotive

- 6.3.2 Semiconductors

- 6.3.3 Oil and Gas

- 6.3.4 Chemical and Petrochemical

- 6.3.5 Pharmaceutical

- 6.3.6 Aerospace and Defense

- 6.3.7 Food and Beverage

- 6.3.8 Mining

- 6.3.9 Other End-user Industries

- 6.4 By Geography

- 6.4.1 North America

- 6.4.1.1 United States

- 6.4.1.2 Canada

- 6.4.2 Europe

- 6.4.2.1 United Kingdom

- 6.4.2.2 Germany

- 6.4.2.3 France

- 6.4.2.4 Rest of Europe

- 6.4.3 Asia-Pacific

- 6.4.3.1 China

- 6.4.3.2 India

- 6.4.3.3 Japan

- 6.4.3.4 Rest of the Asia-Pacific

- 6.4.4 Latin America

- 6.4.4.1 Brazil

- 6.4.4.2 Argentina

- 6.4.4.3 Mexico

- 6.4.4.4 Rest of Latin America

- 6.4.5 Middle-East and Africa

- 6.4.5.1 United Arab Emirates

- 6.4.5.2 Saudi Arabia

- 6.4.5.3 South Africa

- 6.4.5.4 Rest of Middle-East and Africa

- 6.4.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 ABB Ltd

- 7.1.2 Cognex Corporation

- 7.1.3 Siemens AG

- 7.1.4 Schneider Electric SE

- 7.1.5 Yokogawa Electric Corporation

- 7.1.6 KUKA AG

- 7.1.7 Rockwell Automation Inc.

- 7.1.8 Honeywell International Inc.

- 7.1.9 Robert Bosch GmbH

- 7.1.10 Mitsubishi Electric Corporation

- 7.1.11 Fanuc Corporation

- 7.1.12 Emerson Electric Co.

- 7.1.13 FLIR Systems Inc. (Teledyne Technologies Incorporated)

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

2025-2033 年日本智慧工厂市场报告(按现场设备、技术、最终用途产业和地区)

2025-2033 年日本智慧工厂市场报告(按现场设备、技术、最终用途产业和地区) 智慧工厂介绍:2024

智慧工厂介绍:2024 智慧工厂市场:按技术、组件和行业划分 - 2025-2030 年全球预测

智慧工厂市场:按技术、组件和行业划分 - 2025-2030 年全球预测 智慧工厂市场 - 全球产业规模、份额、趋势、机会和预测,按产品、技术、最终用户产业、地区和竞争细分,2019-2029F

智慧工厂市场 - 全球产业规模、份额、趋势、机会和预测,按产品、技术、最终用户产业、地区和竞争细分,2019-2029F 2024-2032 年按现场设备、技术、最终用途产业和地区分類的智慧工厂市场报告

2024-2032 年按现场设备、技术、最终用途产业和地区分類的智慧工厂市场报告 智慧工厂市场报告:2030 年趋势、预测与竞争分析

智慧工厂市场报告:2030 年趋势、预测与竞争分析 智慧工厂全球市场2024-2028

智慧工厂全球市场2024-2028 2030 年智慧工厂市场预测:按组件、连接性、技术、最终用户和地区进行的全球分析

2030 年智慧工厂市场预测:按组件、连接性、技术、最终用户和地区进行的全球分析 全球智慧工厂市场:按组件、按解决方案、按行业、按地区 - 预测至 2029 年

全球智慧工厂市场:按组件、按解决方案、按行业、按地区 - 预测至 2029 年 2024 年智慧工厂全球市场报告

2024 年智慧工厂全球市场报告