|

市场调查报告书

商品编码

1408554

资料中心伺服器:市场占有率分析、产业趋势与统计、2024年至2030年成长预测Data Center Server - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2030 |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

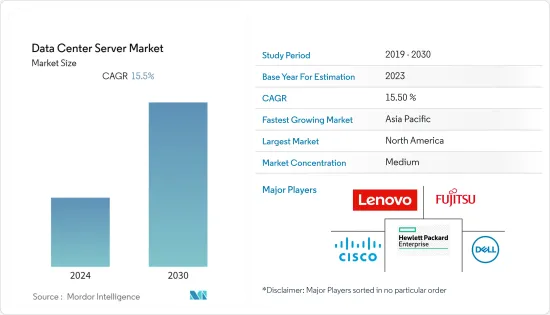

上年度全球资料中心伺服器市场规模达到889亿美元,预计在预测期间内复合年增长率为15.5%。

中小企业对云端运算需求的增加、政府对资料安全的监管以及国内企业投资的增加是推动全球资料中心需求的主要因素。

主要亮点

- 预计到2029年,全球资料中心伺服器市场未来IT负载容量将达到7.1亿度。

- 到 2029 年,该地区的占地面积预计将增加至 2.739 亿平方英尺。

- 到2029年,安装的机架总数预计将达到1420万个。预计到 2029 年,北美安装的机架数量将最多。

- 有近500个海底电缆系统连接世界各地,其中许多正在建设中。 CAP-1 就是一个这样的例子,它计划于 2025 年开始服务,是一条横跨 12,000 多公里的海底电缆,登陆点位于美国格罗弗海滩。

资料中心伺服器市场趋势

IT和通讯占很大比例。

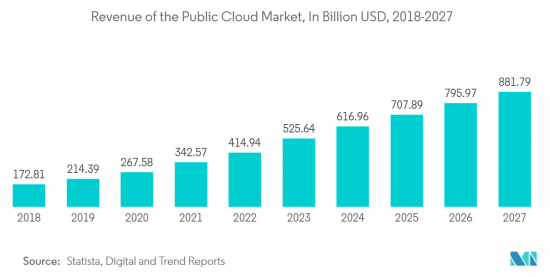

- 云端和通讯预计将推动需求成长。北美、欧洲和亚洲国家对云端服务的需求前景广阔。目前,澳洲 10-15% 的资料是在集中式资料中心和云端之外创建和处理的,但预计到 2025 年,这一数字将升至 60-70% 以上,反映了全球趋势。丹麦对云端解决方案的需求持续成长,并且对云端基础的资料保护和备份解决方案的需求预计将保持强劲。

- 拉丁美洲(美国、加拿大、墨西哥、巴西)、中东和非洲(奈及利亚、南非、埃及、土耳其、阿拉伯联合大公国、沙乌地阿拉伯)以及东南亚(马来西亚、越南)对云端基础的服务的需求正在增长、泰国、印尼、菲律宾)、新加坡)、亚太地区(印度、日本、中国)及欧洲部分地区。

- 在北美,云端还提供计量收费选项,让企业可以根据消费者存取云端服务的频率支付云端服务费用,从而节省资金。大型组织正在迅速采用云,因为云端服务可以按需提供。 2022 年,美国航空将把麵向客户的应用程式迁移到 IBM Cloud 上的 VMware HCX,以提供数位自助服务功能。随着许多中小型企业采用云端基础的系统,北美资料中心市场预计将会成长。

- 此外,随着4G的普及和5G浪潮的到来,通讯业者正在鼓励对资料中心业务的投资。 2022年10月,南非通讯Telkom在中国华为科技公司的支援下建造了5G高速网路网路。华为持续支持南非5G网路发展。非洲大陆着名的 5G 网路部署了 2,800 多个基地台。

- 新兴市场的开拓,例如云端服务的日益采用、5G网路的扩展以及线上付款需求的增加,预计将推动IT和通讯领域对资料中心市场的需求,从而导致成长预测期内的伺服器需求。我是。

快速成长的亚太地区

- 亚太地区是全球资料中心成长最快的地区之一。该地区庞大的人口基数占全球估计人口的近 50%,是主机代管资料中心服务和设施的主要推动力。

- 中国和澳洲拥有最多的资料中心设施。中国的运算能力正在不断增强,已成为超级电脑数量的领先国家。截至2022年6月,全球最强大的500台超级电脑中有173台位于中国,比其最接近的竞争对手美国多三分之一。

- 在澳大利亚,澳洲政府资讯管理办公室 (AGIMO) 等政府倡议在优化资料中心资源方面处于领先地位,推出了《2010-2025 年澳洲政府资料中心策略》。这项策略意味着从使用政府营运的资料中心转向第三方多租户资料中心。

- 在澳大利亚,2019 年对公共云端服务的需求持续成长,42% 的澳洲企业报告使用云端运算(2015-16 年为 31%)。市场供应商正在开发为 IT 行业最终用户量身定制的丰富产品,这也推动了该领域的成长。

- 在印度和印尼等新兴市场,都市化的加速和普及的提高预计将带来下一波成长。截至 2022 年 7 月,印度拥有 6.92 亿活跃网路用户,截至 2022 年 2 月,印度全国活跃社群媒体用户为 4.67 亿。普及互联网的日益普及增加了Over-The-Top和社交媒体的使用,增强了连接的力量。孟买和清奈等印度沿海城市因其密集的湿电缆生态系统而在竞争中处于领先地位。该地区拥有可靠的电力供应和有线网路登陆站,可以实现足够的延迟。

- 技术的不断发展、云端服务的不断采用、电子商务销售以及网路人口的成长正在推动资料中心的需求,资料中心伺服器的需求预计将增加,并在未来几年出现显着增长。

资料中心伺服器产业概况

该地区即将进行的资料中心建设计划将增加未来几年对资料中心伺服器的需求。全球资料中心伺服器市场由戴尔、惠普企业、富士通和联想集团有限公司等几家主要企业适度整合。凭藉压倒性的市场占有率,这些领先公司正专注于扩大每个地区的基本客群。

2023 年 8 月,戴尔将把下一代 Dell PowerEdge 伺服器从 OSA 迁移到 ESA,其中 PowerEdge R760 配备第四代英特尔至强处理器。

2023 年 1 月,思科宣布推出搭载第四代英特尔至强可扩充处理器的第七代 UCS C 系列和 X 系列伺服器。凭藉对最新英特尔处理器的支持,思科发布了 X 系列的两款新刀片:Cisco UCS X210c M7 计算节点和 Cisco UCS X410c M7 计算节点。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场动态

- 市场概况

- 市场驱动因素

- 采用云端运算服务

- 5G网路大规模商用

- 市场抑制因素

- 加大资料中心建置资金投入

- 网路安全威胁与勒索软体攻击

- 价值链/供应链分析

- 产业吸引力-波特五力分析

- 新进入者的威胁

- 买家/消费者的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争公司之间敌对关係的强度

- COVID-19 影响评估

第五章市场区隔

- 按外形尺寸

- 刀锋伺服器

- 机架式伺服器

- 直立式伺服器

- 按最终用户

- 资讯科技/通讯

- BFSI

- 政府机关

- 媒体与娱乐

- 其他最终用户

- 按地区

- 北美洲

- 南美洲

- 欧洲

- 中东

- 非洲

- 亚太地区

第六章 竞争形势

- 公司简介

- Dell Inc.

- Hewlett Packard Enterprise

- Lenovo Group Limited

- Fujitsu Limited

- Cisco Systems Inc.

- Kingston Technology Company Inc.

- Huawei Technologies Co. Ltd.

- Inspur Group

- International Business Machines(IBM)Corporation

- Atos SE

第七章 投资分析

第八章 市场机会及未来趋势

The Global data center server market reached the value of USD 88.9 billion in the previous year, and it is further projected to register a CAGR of 15.5% during the forecast period. The increasing demand for cloud computing among small and medium-sized enterprises (SMEs), government regulations for local data security, and growing investment by domestic players are some of the major factors driving the demand for data centers globally.

Key Highlights

- The upcoming IT load capacity of the Global data center server market is expected to reach 71K MW by 2029.

- The region's construction of raised floor area is expected to increase 273.9 million sq. ft by 2029.

- The region's total number of racks to be installed is expected to reach 14.2 million units by 2029. North America is expected to house the maximum number of racks by 2029.

- There are close to 500 submarine cable systems connecting the regions globally, and many are under construction. One such submarine cable that is estimated to start service in 2025 is CAP-1, which stretches over 12,000 Kilometers with a landing point in Grover Beach, United States.

Data Center Server Market Trends

IT & Telecommunication Holds the Major Share.

- Cloud and telecom are expected to drive the major demand growth. The demand for cloud services is promising in North American, European, and Asian countries. Currently, 10-15% of data in Australia is created and processed outside a centralized data center or cloud, but the number is expected to cross 60-70% by 2025, a global trend that is also reflected in Australia. The need for cloud solutions continues to grow in Denmark, and the demand for cloud-based data protection and backup solutions is expected to get robust.

- The demand for cloud-based services is highly concentrated in regions like Central America and South America (the United States, Canada, Mexico, and Brazil), Middle East & Africa (Nigeria, South Africa, Egypt, Turkey, the United Arab Emirates, and Saudi Arabia), Southeast Asia (Malaysia, Vietnam, Thailand, Indonesia, the Philippines, and Singapore), Asia-Pacific (India, Japan, and China), and parts of Europe.

- In North America, the cloud also offers pay-as-you-go options, which enable businesses to pay for cloud services in accordance with how frequently consumers access them, resulting in lower expenses. Since cloud services are available on demand, large-scale organizations are embracing them quickly. In 2022, American Airlines moved customer-facing applications to VMware HCX on IBM Cloud to offer digital self-service features. The North American market for data centers is expected to grow due to many small and medium-sized businesses adopting cloud-based systems.

- Further, Telecom suppliers are encouraged to invest in the data center business due to the rising adoption of 4G and the impending 5G wave. In October 2022, the 5G high-speed internet network was established by South African telecoms provider "Telkom," supported by Huawei Technologies from China. Huawei continues to assist South Africa in developing its 5G networks. The prominent 5G network on the African continent has more than 2,800 base stations deployed.

- Developments such as increasing adoption of cloud services, expansion of 5G networks, and the ongoing demand for online payments are, in turn, expected to boost the demand for the data center market from the IT and telecom segment, leading to major demand for the servers during the forecast period.

Asia-Pacific Region is the Fastest Growing

- APAC is one of the fastest-developing data center regions in the world. The region's huge population base, which accounts for nearly 50% of the estimated global count, is ultimately the key driver for colocation data center services and facilities.

- China and Australia have the most data center facilities. China is boosting its computing power, and it has become a prominent nation in terms of supercomputer volume. As of June 2022, 173 of the world's 500 most powerful supercomputers were located in China, which is a third more than that of its nearest competitor, the United States.

- In Australia, government initiatives such as the Australia Government Information Management Office (AGIMO) are leading the way in optimizing data center resources with the introduction of the Australia Government Data Centre Strategy 2010-2025. The strategy represents a transition from using government-run data centers to third-party, multi-tenant data centers.

- The appetite for public cloud services in Australia continued to grow in 2019, with 42% of businesses in the country reporting the use of cloud computing compared to 31% in 2015-16. Market vendors are rolling out enhanced product offerings curated for IT industry end users, which is also driving growth in this segment.

- Growing urbanization and greater penetration in emerging markets such as India and Indonesia are expected to drive the next wave of growth. In India, as of July 2022, there were 692 million active internet users, and as of February 2022, there were 467 million active social media users across the country. The growing penetration of mobile internet boosted the power of connectivity through increased over-the-top (OTT) and social media usage. Due to their dense wet cable ecosystem, coastal cities in India, such as Mumbai and Chennai, are leading the race. The proper latencies can be found here, having reliable power sources and landing stations for cable networks.

- The increasing technology developments, the growing adoption of cloud services, e-commerce sales, and the increasing internet population drive the demand for data centers, which is expected to grow significantly, resulting in an increasing need for data center servers in the coming years.

Data Center Server Industry Overview

The upcoming DC construction projects in the region will increase the demand for data center servers in the coming years. The global data center server market is moderately consolidated with a few major players, such as Dell Inc., Hewlett Packard Enterprise, Fujitsu, and Lenovo Group Limited. These major players, with a prominent market share, focus on expanding their regional customer base.

In August 2023, Dell Inc. is transitioning its servers with Next-generation Dell PowerEdge servers from OSA to ESA with PowerEdge R760 powered by 4th-generation Intel Xeon Processors.

In January 2023, Cisco announced the launch of the 7th generation of UCS C-Series and X-Series servers, powered by 4th generation Intel Xeon Scalable processors. With support for the latest Intel processors, Cisco has launched two new blades for the X-Series: the Cisco UCS X210c M7 Compute Node and the Cisco UCS X410c M7 Compute Node.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Dynamics

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Adoption of cloud computing services

- 4.2.2 Large-scale commercialization of 5G networks

- 4.3 Market Restraints

- 4.3.1 Rising CapEx for data center construction

- 4.3.2 Cybersecurity Threats and Ransomware attacks

- 4.4 Value Chain / Supply Chain Analysis

- 4.5 Industry Attractiveness - Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Assessment of COVID-19 Impact

5 MARKET SEGMENTATION

- 5.1 Form Factor

- 5.1.1 Blade Server

- 5.1.2 Rack Server

- 5.1.3 Tower Server

- 5.2 End-User

- 5.2.1 IT & Telecommunication

- 5.2.2 BFSI

- 5.2.3 Government

- 5.2.4 Media & Entertainment

- 5.2.5 Other End-User

- 5.3 Geography

- 5.3.1 North America

- 5.3.2 South America

- 5.3.3 Europe

- 5.3.4 Middle East

- 5.3.5 Africa

- 5.3.6 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Dell Inc.

- 6.1.2 Hewlett Packard Enterprise

- 6.1.3 Lenovo Group Limited

- 6.1.4 Fujitsu Limited

- 6.1.5 Cisco Systems Inc.

- 6.1.6 Kingston Technology Company Inc.

- 6.1.7 Huawei Technologies Co. Ltd.

- 6.1.8 Inspur Group

- 6.1.9 International Business Machines (IBM) Corporation

- 6.1.10 Atos SE

7 INVESTMENT ANALYSIS

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

资料中心伺服器市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)

资料中心伺服器市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年) 资料中心智慧推理伺服器:全球市场份额和排名、总收入和需求预测(2025-2031 年)

资料中心智慧推理伺服器:全球市场份额和排名、总收入和需求预测(2025-2031 年) CPX和Rubin的整合:全球伺服器的GDDR7

CPX和Rubin的整合:全球伺服器的GDDR7 2025年全球资料中心和伺服器市场报告

2025年全球资料中心和伺服器市场报告 2025-2029年全球资料中心与伺服器市场全球资料中心伺服器市场:2034 年的机会与策略

2025-2029年全球资料中心与伺服器市场全球资料中心伺服器市场:2034 年的机会与策略 资料中心伺服器市场规模、份额、成长分析(按组件、按类型、按设计、按公司规模、按层级、按地区)—产业预测 2025-2032

资料中心伺服器市场规模、份额、成长分析(按组件、按类型、按设计、按公司规模、按层级、按地区)—产业预测 2025-2032 日本资料中心伺服器市场:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)

日本资料中心伺服器市场:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年) 2025 年至 2033 年资料中心伺服器市场报告(按产品(机架式伺服器、刀锋式伺服器、微型伺服器、塔式伺服器)、应用程式(工业伺服器、商用伺服器)和地区划分)

2025 年至 2033 年资料中心伺服器市场报告(按产品(机架式伺服器、刀锋式伺服器、微型伺服器、塔式伺服器)、应用程式(工业伺服器、商用伺服器)和地区划分) 全球资料中心伺服器市场、市场规模和占有率分析:依类型和应用分类 - 收入估算和需求预测(截至 2030 年)

全球资料中心伺服器市场、市场规模和占有率分析:依类型和应用分类 - 收入估算和需求预测(截至 2030 年)