|

市场调查报告书

商品编码

1431024

水泥:市场占有率分析、产业趋势与统计、成长预测(2024-2029)Cement - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

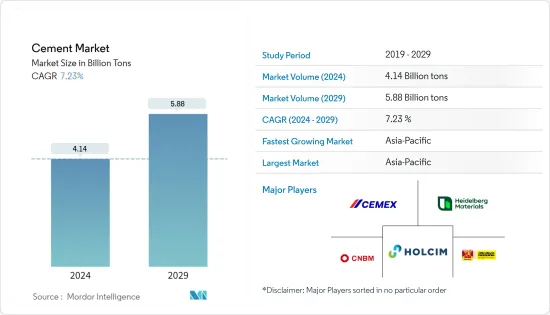

预计2024年水泥市场规模为41.4亿吨,预计到2029年将达到58.8亿吨,预测期内(2024-2029年)复合年增长率为7.23%,预计还会增长。

主要亮点

- 由于 COVID-19 大流行,水泥市场受到负面影响,整个建设产业的需求减少,并导致各种製造设施关闭。然而,市场正在逐渐復苏,并可能很快达到新冠疫情前的水平。

- 短期来看,亚太地区住宅的增加以及中东和非洲地区基础设施活动的活性化是推动市场需求的因素之一。此外,飞灰等原料的充足供应预计也将推动市场向前发展。

- 然而,政府有关水泥製造厂二氧化碳排放的法规正在阻碍市场成长。

- 儘管如此,绿色建筑方向的转变以及 HBC(海贝莱特水泥)在中国的良好表现可能会为所研究的市场提供机会。

- 亚太地区在市场上占据主导地位,并且在预测期内可能保持最高的复合年增长率。

水泥市场趋势

住宅成长

- 住宅部门是水泥最重要的需求部门之一。随着中产阶级可支配收入的增加,新住宅建设将会增加,并可能推动这个市场。

- 由于规范节能建筑的建筑规范和法律不断增加,水泥在住宅领域变得越来越受欢迎。加拿大政府的各种计划,例如经济适用房计划(AHI)、加拿大新建筑计划(NBCP)和加拿大製造,预计将极大地促进该行业的扩张,从而促进环保水泥在工业领域的使用。住宅部门。我是。

- 另外,根据越南建设部近日发布的消息,广宁省下龙市人民委员会将于11月初在下龙市鸿海区和草滩区开始建设约1000套公寓的社会住宅计划2022 年。做到了。

- 除了新住宅开发外,美国还在住宅维修方面投入大量资金。随着流动人口的增加,恢復的需求也越来越大。此外,人们对永续性和高效建设重要性的认识不断提高,也推动了修復趋势。许多政府贷款的提供也支持了该国的住宅维修。

- 根据美国人口普查局的统计,2023年1月竣工私人住宅数量经季节已调整的后的年率为140.6万套,比2022年12月修正后的139.2万套增加1.0%,增幅为12.8%增加超过1,247,000例。

- 此外,根据德国联邦统计局的报告,2023 年 1 月至 3 月期间,该国总合发放了 68,700 个住宅建筑许可证。光是 2023 年 3 月,就批准了 24,500 套住宅。

- 此外,已确认将拨款115亿英镑(约148亿美元)用于英国政府的经济适用住宅计划,2021年至2026年五年内将建造约18万套新房,目标是提供住宅。该计划还将额外拨款 380 亿英镑(约 490 亿美元)用于公共和私人投资经济适用住宅。

- 由于所有这些因素,水泥市场在预测期内可能会成长。

亚太地区主导市场

- 亚太地区的水泥市场正在显着成长,中国和印度等国家占据了水泥消费的大部分。

- 中国的建筑业正在经历显着成长。根据中国国家统计局数据,2022年第四季中国建筑业产值约2,760亿元人民币(约400亿美元),较上季(约276亿美元)成长约50%。

- 此外,根据中国国家统计局公告,预计2022年中国建设产业增加价值额将超过8.33兆元人民币(约合1.2兆美元),与前一年同期比较增长约4% .马苏。

- 印度工商联合会 (FICCI) 的数据显示,2022 年印度大都会圈根据 PMAY 计画建造和批准的住宅数量分别约为 550 万套和 1,140 万套。

- 根据印度知名房地产服务商Anarock预计,2022年印度销售住宅套数将超过30万套,超过先前2014年印度七大城市创下的住宅销售纪录。与 2021 年第四季相比,2022 年第四季该国住宅销售量成长约 16%。

- 此外,印尼政府还推出了百万住宅 (OMH) 计划,每年建造超过 100 万套住宅。据公共工程和公共住宅部 (PUPR) 称,到年终,根据「百万套住房」计划,已建成约 1,117,491 套住宅。

- 日本国土交通省也在报告中表示,2022年日本住宅量约859,500套,仅比前一年(856,480套)增加0.4%。

- 所有上述因素预计将在预测期内推动日本石膏板市场。

水泥业概况

水泥市场已部分整合。市场主要企业包括(排名不分先后)中国建材集团公司、CEMEX、SAB de CV、HOLCIM、Heidelberg Materials 和 UltraTech Cement Ltd。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第一章简介

- 调查先决条件

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场动态

- 促进因素

- 亚太地区住宅增加

- 中东和非洲地区基础建设力道加大

- 飞灰等原料供应充足

- 抑制因素

- 关于水泥製造厂碳排放的政府法规

- 其他限制因素

- 产业价值链分析

- 波特五力分析

- 供应商的议价能力

- 买方议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章市场区隔(市场规模:基于数量)

- 类型

- 波特兰

- 混合物

- 其他类型

- 目的

- 住宅

- 商业的

- 基础设施

- 产业/设施

- 地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 东南亚国协

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 义大利

- 法国

- 其他欧洲国家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东/非洲

- 沙乌地阿拉伯

- 南非

- 其他中东/非洲

- 亚太地区

第六章 竞争形势

- 併购、合资、联盟、协议

- 市场占有率(%)/排名分析

- 主要企业策略

- 公司简介

- Buzzi SpA

- China National Building Material Group Corporatio

- CEMEX, SAB de CV

- CRH

- Heidelberg Materials

- HOLCIM

- InterCement

- Mitsubishi Cement Corporation

- SCG

- TAIHEIYO CEMENT CORPORATION

- Taiwan Cement Ltd

- TITAN CEMENT

- UltraTech Cement Ltd.

- Votorantim Cimentos

第七章 市场机会及未来趋势

- 绿建筑偏好的转变

- HBC(海贝莱特水泥)在中国的表现可期

简介目录

Product Code: 91436

The Cement Market size is estimated at 4.14 Billion tons in 2024, and is expected to reach 5.88 Billion tons by 2029, growing at a CAGR of 7.23% during the forecast period (2024-2029).

Key Highlights

- The cement market was negatively impacted due to the COVID-19 pandemic, which resulted in decreasing demand across the construction industry and the closing of various manufacturing facilities. However, the market is recovering gradually and is likely to reach pre-COVID levels soon.

- Over the short term, the growing residential constructions across the Asia Pacific region and the growing infrastructural activities in the Middle East and Africa region are some of the driving factors which are fueling the market demand. Moreover, the abundance availability of raw materials, such as fly ash, is also expected to drive the market forward.

- However, government regulations on carbon emissions from cement manufacturing plants are hindering the market's growth.

- Nevertheless, the shifting preference towards green construction and encouraging performance of HBC (High Belite Cement) in China are likely to provide opportunities to the market studied.

- The Asia-Pacific region is expected to dominate the market and is also likely to witness the highest CAGR during the forecast period.

Cement Market Trends

Growing Residential Construction

- The residential sector is one of the most significant demanding sectors for cement. The market studied is likely to be driven by increased construction of new residential buildings as middle-class disposable income rises.

- Cement is becoming more popular in the residential sector as a result of an increase in the number of building standards and legislation regulating energy-efficient structures. Various government programs in Canada, such as the Affordable Housing Initiative (AHI), New Building Canada Plan (NBCP), and Made in Canada, are expected to significantly promote the industry's expansion, consequently driving the usage of green cement in the residential sector.

- The Ministry of Construction of Vietnam, in its recent publication, also stated that the People's Committee of Ha Long City in Quang Ninh Province commenced construction of a social housing project for nearly 1,000 apartments in Ha Long City's Hong Hai Ward and Cao Thang Ward in the early November of 2022.

- Aside from new home development, the United States is investing heavily in home improvements. The necessity for rehabilitation has become increasingly critical as the country's migrant population has grown. In addition, the increased awareness of the importance of sustainability and high-efficiency constructions has fueled the restoration trend. The availability of many government loans also encourages home upgrading in the country.

- The statistics by the US Census Bureau also stated that the privately owned housing completions were at a seasonally adjusted annual rate of 1,406,000 in January 2023, which is 1.0 percent more than the revised December 2022 estimate of 1,392,000 and 12.8 percent higher than the January 2022 rate of 1,247,000.

- Moreover, according to the report by Federal Statistical Office in Germany, from January to March 2023, a total of 68,700 building permits for dwellings were issued in the country. In March 2023 alone, the construction of 24,500 dwellings was permitted in Germany.

- Further, a GBP 11.5 billion (~USD 14.8 billion) budget was confirmed for allocation in the United Kingdom's Affordable Homes Program by the Government, which targets to deliver around 180,000 new homes over five years of timespan between 2021 and 2026. The program is also due to unlock an added budget of GBP 38 billion (~USD 49 billion) for public and private investment in affordable housing.

- Owing to all these factors, the market for cement is likely to grow during the forecast period.

Asia-Pacific Region to Dominate the Market

- The Asia-Pacific region has seen significant growth in the cement market, with countries such as China and India accounting for significant consumption of cement.

- China is experiencing massive growth in its construction sector. According to the National Bureau of Statistics of China, in the fourth quarter of 2022, the construction output in China was valued at approximately CNY 276 billion (~USD 40 billion), a growth of approximately 50% when compared with the previous quarter (~USD 27.6 billion).

- Moreover, the value added in the Chinese construction industry in the year 2022 was estimated to be more than CNY 8,330 billion (~USD 1.2 trillion), approximately 4% more than the previous year's value, as stated by the National Bureau of Statistics of China.

- According to the Federation of Indian Chambers of Commerce and Industry (FICCI), the number of residences constructed and sanctioned under the PMAY plan in India's metropolitan regions in 2022 was roughly around 5.5 million and 11.4 million, respectively.

- According to Anarock, a well-known real estate service provider in India, more than 300,000 housing units were sold in India in 2022, exceeding the previous record of all-time high sales of houses in India's top seven cities set in 2014. House sales in the country increased by around 16% in the fourth quarter of 2022 as compared to the fourth quarter of 2021.

- Moreover, the Indonesian government introduced the 'One Million Houses' (OMH) program to construct at least 1 million units per year. According to the Ministry of Public Works and Public Housing (PUPR), under the One Million Houses program, about 1,117,491 housing units were recorded until the end of 2022.

- The Ministry of Land, Infrastructure, Transport and Tourism (MLIT) of Japan also stated in its report that approximately 859.5 thousand housing starts were initiated in Japan in 2022, just 0.4% more than the previous year's value (856.48 thousand).

- All the aforementioned factors, in turn, are expected to drive the market for gypsum boards in the country during the forecast period.

Cement Industry Overview

The cement market is partially consolidated in nature. Some of the major players in the market include China National Building Material Group Corporation, CEMEX, S.A.B. de C.V., HOLCIM, Heidelberg Materials, and UltraTech Cement Ltd., among others (not in any particular order).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increase in Residential Constructions Across Asia Pacific

- 4.1.2 Growing Infrastructural Activities In The Middle East And Africa Region

- 4.1.3 Abundance Availability of Raw Materials Such as Fly Ash

- 4.2 Restraints

- 4.2.1 Government Regulations On Carbon Emissions From Cement Manufacturing Plants

- 4.2.2 Other Restraints

- 4.3 Industry Value-Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Type

- 5.1.1 Portland

- 5.1.2 Blended

- 5.1.3 Other Types

- 5.2 Application

- 5.2.1 Residential

- 5.2.2 Commercial

- 5.2.3 Infrastructure

- 5.2.4 Industrial and Institutional

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest Of South America

- 5.3.5 Middle-East And Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest Of Middle-East And Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Buzzi S.p.A.

- 6.4.2 China National Building Material Group Corporatio

- 6.4.3 CEMEX, S.A.B. de C.V.

- 6.4.4 CRH

- 6.4.5 Heidelberg Materials

- 6.4.6 HOLCIM

- 6.4.7 InterCement

- 6.4.8 Mitsubishi Cement Corporation

- 6.4.9 SCG

- 6.4.10 TAIHEIYO CEMENT CORPORATION

- 6.4.11 Taiwan Cement Ltd

- 6.4.12 TITAN CEMENT

- 6.4.13 UltraTech Cement Ltd.

- 6.4.14 Votorantim Cimentos

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Shifting Preference Towards Green Construction

- 7.2 Encouraging Performance of HBC (High Belite Cement) in China

02-2729-4219

+886-2-2729-4219

全球水泥市场:产量、消费量、类型、应用与区域分析、规模、趋势、新冠疫情影响及 2030 年预测

全球水泥市场:产量、消费量、类型、应用与区域分析、规模、趋势、新冠疫情影响及 2030 年预测 2025年水泥胶黏剂全球市场报告混合水泥市场 - 全球产业规模、份额、趋势、机会和预测,细分,按应用、按最终用户、按类型、按地区、按竞争,2020-2030F

2025年水泥胶黏剂全球市场报告混合水泥市场 - 全球产业规模、份额、趋势、机会和预测,细分,按应用、按最终用户、按类型、按地区、按竞争,2020-2030F 亚太水泥 -市场占有率分析、产业趋势和成长预测(2025-2030 年)印尼水泥:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)印度水泥:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)

亚太水泥 -市场占有率分析、产业趋势和成长预测(2025-2030 年)印尼水泥:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)印度水泥:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年) 水泥包装市场规模、份额及成长分析(依材料、包装类型、产量、最终用途及地区)-2025-2032 年产业预测

水泥包装市场规模、份额及成长分析(依材料、包装类型、产量、最终用途及地区)-2025-2032 年产业预测 混凝土和水泥,全球市场 2025-20292025年全球水泥和混凝土产品市场报告再生混凝土骨材市场规模、份额、成长分析、按来源、按产品类型、按加工方法、按应用、按地区 - 产业预测,2025 年至 2032 年

混凝土和水泥,全球市场 2025-20292025年全球水泥和混凝土产品市场报告再生混凝土骨材市场规模、份额、成长分析、按来源、按产品类型、按加工方法、按应用、按地区 - 产业预测,2025 年至 2032 年

▼