|

市场调查报告书

商品编码

1432934

小型液化天然气:市场占有率分析、产业趋势与统计、成长预测(2024-2029)Small-scale LNG - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

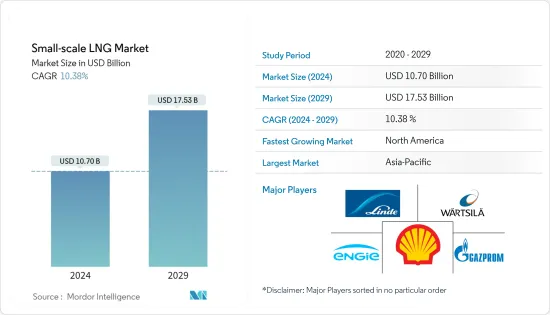

预计小型液化天然气市场规模到2024年将达到107亿美元,预计2029年将达到175.3亿美元,在预测期内(2024-2029年)复合年增长率为10.38%。

主要亮点

- 从长远来看,燃料库、道路运输和离网电力等方面对液化天然气的需求不断增加等因素预计将在未来几年推动小型液化天然气市场的发展。

- 另一方面,在中东、非洲等地区,小型LNG营业成本高、配套基础设施欠发达、投资回收期长(12年以上)、所需的资本投资额很高,预计有一些因素会阻碍所研究市场的成长。

- 然而,由于小型液化天然气基础设施所需的资本支出较高,开发具有成本效益的小型液化天然气基础设施预计将为小型液化天然气技术供应商和运输商提供重大机会。

- 亚太地区在市场上占据主导地位,并且在预测期内也可能实现最高的复合年增长率。这一增长归因于对液化天然气的需求增加、净零碳排放目标、政府开发液化天然气相关基础设施的倡议,以及日本、中国和韩国等国家私人公司投资的增加。

小型液化天然气市场趋势

交通运输领域预计将主导市场

- 液化天然气主要用作卡车和船舶的燃料,主要是因为它在经济和环境上都优于柴油和燃油。液化天然气无腐蚀性且无毒,这意味着它可以将车辆的使用寿命延长三倍。此外,液化天然气的沸点极低,因此在高压下将其转化为气态所需的热和机械能可以忽略不计。这使得液化天然气成为一种高效率的运输燃料。

- 处理液化天然气是一项艰鉅的任务,因为即使是最轻微的温差也会导致燃料沸腾或蒸发,导致燃料浪费。因此,小客车的实用性远不如商用卡车等大型车辆。因此,LNG在运输领域的使用受到限制。

- 使用液化天然气作为运输燃料正在世界各地蓬勃发展。中国、美国和欧洲已经开始部署液化天然气动力卡车,主要用于远距货物运输。这主要得益于政府政策以及脱碳和排放气体监管政策,例如国六和欧洲绿色交易。

- 欧盟委员会于 2019 年制定的《欧洲绿色新政》是一系列政策倡议,旨在到 2050 年使欧洲实现碳中和。该政策简洁地强调了液化天然气在实现这些目标中的重要性,并强调其作为卡车和船舶燃料的用途。

- 据SEA-LNG称,截至2022年2月,已有137艘液化天然气运输船在运营,350艘液化天然气运输船正在订购。液化天然气动力船舶的订单成长速度比以往任何时候都快,越来越多的船东和营运商正在认识到液化天然气的环境和气候效益。

- 2020 年 1 月,国际海事组织 (IMO) 开始实施新法规,规定船用燃料的硫含量上限为 0.5%。因此,与现有的石油基船用燃料油相比,液化天然气的氮氧化物排放减少了近90%,并且几乎不排放硫氧化物或颗粒物,使其成为更现实的船用燃料选择。因此,液化天然气将在这项清洁空气倡议中发挥重要作用。预计这也将对小型液化天然气市场产生重大正面影响。

- 新兴经济体也计划为未来液化天然气运输奠定基础。例如,商船三井计划到 2022 年 4 月至 2035 年,有 110 艘净零排放远洋船舶投入营运。此外,作为推动清洁能源普及的一部分,我们计划在2030年投入使用90艘液化天然气运输船。

- 因此,由于上述因素,交通运输领域对小型液化天然气基础设施的需求可能会在预测期内增长,并显着主导市场。

亚太地区主导市场

- 亚太地区最近成为全球实施小型液化天然气计划的先驱。近年来,随着中国、印度、新加坡和日本等国家对天然气的需求增加,人们对使用小型液化天然气(SSLNG)的兴趣增加。

- 截至2021年,中国是全球引领液化天然气需求成长的主要国家之一。 2022年液化天然气进口量约6,440万吨。需求的激增使中国成为世界上最大的液化天然气进口国之一。需求的增加是由于中国液化天然气买家签署了每年超过2000万吨的长期合约。

- 中国的天然气市场包括国内生产以及透过管道和液化天然气接收站进口。在中国,工业、住宅和发电业对小型液化天然气的需求正在成长,其中潜力最大的是交通运输业。由于柴油价格高于天然气,液化天然气卡车数量的增加预计将成为中国小型液化天然气设施增加的主要原因。

- 在印度,小型液化天然气还处于非常早期的阶段,但有多个液化天然气站,并且透过液化天然气卡车进行液化天然气运输。印度的目标是到2030年将天然气在其能源结构中的比例提高到15%,该国很可能会建设小型液化天然气设施,向没有管道基础设施的偏远地区供应天然气。例如,2022年6月,天然气勘探和生产公司GAIL Limited计划在未连接液化天然气管道的地区建立小型液化设施。此外,GAIL可能会试建两座小型液化厂。

- 新加坡的小型液化天然气业务主要由新加坡港的液化天然气燃料库设施推动。新加坡是世界领先的贸易港口之一,也是国际航运的世界领导者。 2021年5月,FueLNG与新加坡海事及港务局(MPA)完成了新加坡首艘LNG燃料油轮Pacific Emerald的燃料库。

- 因此,鑑于上述几点,亚太地区预计将在预测期内主导小型市场的成长。

小型液化天然气产业概况

小规模液化天然气市场较分散。市场上的主要企业(排名不分先后)包括 Linde plc、Wartsila Oyj ABP、Shell PLC、Engie SA 和 PJSC Gazprom。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第一章简介

- 调查范围

- 市场定义

- 研究场所

第 2 章执行摘要

第三章调查方法

第四章市场概况

- 介绍

- 2028年之前的市场规模与需求预测(单位:美元)

- 最新趋势和发展

- 政府法规政策

- 市场动态

- 促进因素

- 增加液化天然气基础设施投资

- 燃料库、道路运输和离网电力对液化天然气的需求增加

- 抑制因素

- 中东、非洲等地区基础建设匮乏

- 促进因素

- 供应链分析

- 波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间的敌对关係

第五章市场区隔

- 类型

- 液化终端

- 再气化终端

- 供货型态

- 卡车

- 转运和燃料库

- 管道和铁路

- 目的

- 运输

- 工业原料

- 发电

- 其他用途

- 区域市场分析:2028 年之前的市场规模和需求预测(仅限区域)

- 北美洲

- 美国

- 加拿大

- 北美其他地区

- 欧洲

- 德国

- 法国

- 英国

- 其他欧洲国家

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东/非洲

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 南非

- 其他中东和非洲

- 北美洲

第六章 竞争形势

- 併购、合资、联盟、协议

- 主要企业策略

- 公司简介

- Small-scale LNG Technology Providers

- Linde plc

- Wartsila Oyj ABP

- Baker Hughes Company

- Honeywell UoP

- Chart Industries Inc.

- Black & Veatch Holding Company

- Small-scale LNG Marine Transporter

- Anthony Veder Group NV

- Engie SA

- Evergas AS

- Small-scale LNG Operators

- Shell PLC

- Eni SpA

- PJSC Gazprom

- TotalEnergies SE

- Gasum Oy

- Small-scale LNG Technology Providers

第七章 市场机会及未来趋势

- 开发具有成本效益的小型液化天然气基础设施

简介目录

Product Code: 55955

The Small-scale LNG Market size is estimated at USD 10.70 billion in 2024, and is expected to reach USD 17.53 billion by 2029, growing at a CAGR of 10.38% during the forecast period (2024-2029).

Key Highlights

- Over the long term, the factors such as increasing demand for LNG in bunkering, road transportation, and off-grid power, are expected to drive the small-scale LNG market in the coming years.

- On the other hand, factors such as the high operation cost of small-scale LNG and lack of supporting infrastructure in the regions such as the Middle East and Africa, and high CAPEX requirements, along with a long payback period of more than 12 years, are expected to hinder the growth of the market studied.

- Nevertheless, owing to the high capital expenditure required for a small-scale LNG infrastructure, the development of cost-efficient small-scale LNG infrastructure is expected to provide significant opportunities to the small-scale LNG technology providers and transporters in the future.

- The Asia-Pacific region dominates the market and is also likely to witness the highest CAGR during the forecast period. This growth is attributed to the increased demand for LNG, the net-zero carbon emission targets, the government's initiative to develop the LNG-related infrastructure and rise in investment from private companies coming from countries such as Japan, China, and South Korea.

Small Scale LNG Market Trends

Transportation Segment Expected to Dominate the Market

- LNG is primarily used to fuel trucks and ships, mainly due to its economic and environmental benefits, as compared to diesel and fuel oil. Since LNG is non-corrosive and non-toxic in nature, it can extend the life of a vehicle by up to three times. Moreover, since LNG has an extremely low boiling point, very little heat is required to convert it into a gaseous form at high pressure, with negligible mechanical energy. This makes LNG an efficient fuel for transportation.

- Handling LNG is an immense task since even a slight difference in the temperature can lead to the boiling and vaporization of fuel, which, in turn, leads to fuel wastage. Therefore, it makes passenger cars far less viable than heavy vehicles, such as commercial trucks. This has limited the application of LNG in the transportation segment.

- The use of LNG as a transportation fuel is gaining momentum across the world. China, the United States, and Europe have already started deploying LNG-powered trucks, mainly for long-distance freight carriage. This is mainly due to the government policies and regulations on decarbonizing and emission control, such as China VI and European Green Deal.

- Formed in 2019 by the European Commission, the European Green Deal is a set of policy initiatives with an aim to make Europe carbon-neutral by 2050. The policies briefly underline the importance of LNG in reaching the aim, and they emphasize the usage of LNG as fuel for trucks and marine vessels.

- According to SEA-LNG, as of February 2022, there were 137 LNG-fueled ships in operation, and 350 LNG-fueled ships were on order. The rapidly growing order book for LNG-fuelled vessels has witnessed rapid growth compared to previous years and increasing numbers of ship owners and operators apprehend LNG's environmental and climate benefits.

- In January 2020, the International Maritime Organization began implementing a new regulation by placing a 0.5% global sulfur cap on marine fuels. Thus, LNG has become a more viable option as a marine fuel since it emits almost 90% lower NOx and virtually no SOx and particulate matter in comparison to the existing petroleum-based marine fuel oils. Therefore, in this clean air initiative, LNG will play a key role. This will also have a significantly positive impact on the small-scale LNG market.

- New emerging economies are also planning to lay foundation for the future of LNG for transportation. For instance, in April 2022, Mitsui O.S.K. Lines (MOL) plans to launch 110 net zero emission oceangoing vessels by 2035. In addition to promoting the wide adoption of clean energy, the Japanese carrier plans to launch 90 LNG-powered vessels by 2030 as part of its goal to promote widespread adoption of clean energy.

- Hence, owing to the above-mentioned factors, the demand for small-scale LNG infrastructure for the transportation segment is likely to grow and significantly dominate the market during the forecast period.

Asia-Pacific to Dominate the Market

- Asia-Pacific, in recent years, has been a pioneer in the implementation of small-scale LNG projects across the globe. Interest in the use of small-scale LNG (SSLNG) has increased in recent years, as the demand for natural gas continues to increase in countries like China, India, Singapore, Japan, and others.

- As of 2021, China is one of the major countries in the world that led to the growth in LNG demand. The LNG import was around 64.4 million tons in 2022. Due to this surge in demand, China became the one of the world's largest LNG importer. The increased demand is due to Chinese LNG buyers signing long-term contracts for more than 20 million tons a year.

- China's natural gas market includes domestic production and import via pipelines and LNG terminals. In China, the rising demand for small-scale LNG is from industrial, residential, and power generation sectors, with the highest potential being in the transportation sector. Growth in the number of LNG trucks due to the higher price of diesel, as compared to natural gas, is expected to be the prime reason for which small LNG facilities are growing in China.

- While in India, Small-scale LNG is in a very nascent stage, however, there are a few LNG stations, for which LNG transportation through LNG trucks is taking place. With the intention of increasing the share of natural gas to 15% in its energy mix by 2030, India is likely to construct small-scale LNG facilities for natural gas supply to remote places, with no pipeline infrastructure. For instance, in June 2022, GAIL Limited, a government-owned natural gas explorer and producer company, aimed to set up small liquefaction facilities for areas not connected to LNG pipelines. Furthermore, GAIL is likely to set up two small-scale liquefaction plants on a pilot basis.

- Small-scale LNG business in Singapore is majorly driven by the LNG bunkering facilities in the ports of Singapore. Singapore has one of the leading trade ports and is one of the global leaders in international marine shipping. In May 2021, FueLNG and the Maritime and Port Authority of Singapore (MPA) completed Singapore's first bunkering of an LNG-fueled oil tanker, Pacific Emerald.

- Therefore, owing to the above points, Asia-Pacific is expected to dominate the growth of the small-scale market during the forecast period.

Small Scale LNG Industry Overview

The small-scale LNG market is semi-fragmented. Some of the major players in the market (in no particular order) include Linde plc, Wartsila Oyj ABP, Shell PLC, Engie SA, and PJSC Gazprom among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2028

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing Investment in LNG Infrastructure

- 4.5.1.2 Rising Demand for LNG in Bunkering, Road Transportation, and Off-grid Power

- 4.5.2 Restraints

- 4.5.2.1 Lack of Supporting Infrastructure in the Regions such as the Middle East and Africa

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Liquefaction Terminal

- 5.1.2 Regasification Terminal

- 5.2 Mode of Supply

- 5.2.1 Truck

- 5.2.2 Transshipment and Bunkering

- 5.2.3 Pipeline and Rail

- 5.3 Application

- 5.3.1 Transportation

- 5.3.2 Industrial Feedstock

- 5.3.3 Power Generation

- 5.3.4 Other Applications

- 5.4 Geography (Regional Market Analysis {Market Size and Demand Forecast till 2028 (for regions only)})

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 France

- 5.4.2.3 United Kingdom

- 5.4.2.4 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 South Africa

- 5.4.5.4 Rest of Middle-East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Small-scale LNG Technology Providers

- 6.3.1.1 Linde plc

- 6.3.1.2 Wartsila Oyj ABP

- 6.3.1.3 Baker Hughes Company

- 6.3.1.4 Honeywell UoP

- 6.3.1.5 Chart Industries Inc.

- 6.3.1.6 Black & Veatch Holding Company

- 6.3.2 Small-scale LNG Marine Transporter

- 6.3.2.1 Anthony Veder Group NV

- 6.3.2.2 Engie SA

- 6.3.2.3 Evergas AS

- 6.3.3 Small-scale LNG Operators

- 6.3.3.1 Shell PLC

- 6.3.3.2 Eni SpA

- 6.3.3.3 PJSC Gazprom

- 6.3.3.4 TotalEnergies SE

- 6.3.3.5 Gasum Oy

- 6.3.1 Small-scale LNG Technology Providers

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 The Development of Cost-efficient Small-scale LNG Infrastructure

02-2729-4219

+886-2-2729-4219

2025 年小型液化天然气全球市场报告

2025 年小型液化天然气全球市场报告 2025 年至 2033 年小型液化天然气市场报告,按终端类型、供应方式、储槽类型(加压槽、常压槽、浮动储槽)、应用和地区划分

2025 年至 2033 年小型液化天然气市场报告,按终端类型、供应方式、储槽类型(加压槽、常压槽、浮动储槽)、应用和地区划分 小型液化天然气市场规模、份额、成长分析,按类型、供应模式、储存槽容量、应用、最终用途、地区 - 产业预测,2025-2032

小型液化天然气市场规模、份额、成长分析,按类型、供应模式、储存槽容量、应用、最终用途、地区 - 产业预测,2025-2032 亚太地区小型液化天然气 -市场占有率分析、产业趋势与统计、成长预测(2025-2030)

亚太地区小型液化天然气 -市场占有率分析、产业趋势与统计、成长预测(2025-2030) 小型液化天然气市场:按特征、类型、应用和供应模式划分 - 2025-2030 年全球预测

小型液化天然气市场:按特征、类型、应用和供应模式划分 - 2025-2030 年全球预测 全球小型液化天然气市场 - 2024-2031

全球小型液化天然气市场 - 2024-2031 小型液化天然气市场规模/份额/趋势分析报告:按类型、供应形式、应用、地区、细分市场预测,2024-2030

小型液化天然气市场规模/份额/趋势分析报告:按类型、供应形式、应用、地区、细分市场预测,2024-2030 小型液化天然气市场 - 全球产业规模、份额、趋势、机会和预测,2018-2028F 按类型、供应方式、储槽容量(常压、加压和浮动储存)、应用、按地区、竞争细分

小型液化天然气市场 - 全球产业规模、份额、趋势、机会和预测,2018-2028F 按类型、供应方式、储槽容量(常压、加压和浮动储存)、应用、按地区、竞争细分 全球小型液化天然气市场:按类型、应用、供应方式和地区划分 - 预测(至 2028 年)

全球小型液化天然气市场:按类型、应用、供应方式和地区划分 - 预测(至 2028 年) 2022-2029年全球小规模LNG市场规模研究和预测,按类型(液化、再气化)、应用(重型车辆、工业和电力、海洋运输)和区域分析。

2022-2029年全球小规模LNG市场规模研究和预测,按类型(液化、再气化)、应用(重型车辆、工业和电力、海洋运输)和区域分析。