|

市场调查报告书

商品编码

1440147

特种车辆:市场占有率分析、产业趋势与统计、成长预测(2024-2029)Specialty Vehicle - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

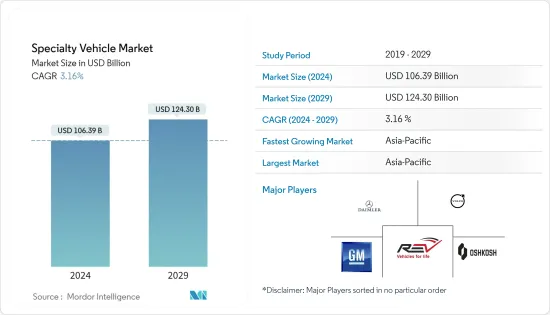

特种车辆市场规模预计到2024年为1,063.9亿美元,预计2029年将达到1,243亿美元,在预测期内(2024-2029年)复合年增长率为3.16%。

2020年专用车市场下降的主要原因是新型冠状病毒感染疾病(COVID-19)大流行导致运输活动暂停和供应链中断。然而,在封锁措施解除后,随着世界各地的治理机构开始大力投资医疗设施、紧急服务和相关设备,市场开始显着成长。

从长远来看,私营部门的积极参与预计将扩大中国和印度等国家的建筑业,从而推动特种车辆市场的发展。物流行业的扩张预计将增加对专业气动散装船和油轮拖车的需求,从而推动散装货船市场的发展。因此,玩家们也专注于开发创新产品。

主要亮点

由于成本降低、新服务模式要求、平台变化以及材料和生产价格上涨,製造商也开始关注有吸引力的服务产品。特种车辆产业的客户购买习惯正在发生巨大变化,尤其是在产品客製化方面。随着客製化需求的增加,OEM面临更多的选择和复杂性。

预计亚太地区在预测期内的复合年增长率最高,其次是欧洲和北美。在预测期内,美国中小型企业将这些车辆用于食品卡车运营、移动展示室以及广告和促销等目的的情况预计将会增加,同时对旅行、医疗和旅游的需求也会增加。具备医疗保健功能的车辆。

专用车市场趋势

执法和医疗保健设施支出增加

流行病和流行病、交通事故、家庭和工作相关事故以及政府资助的医疗保健计划的增加正在增加对医疗和保健特种车辆的需求。在美国,三分之一的人患有血癌等疾病,增加了对血液的需求,推动了血液载体市场的成长。

最近的感染疾病和大流行,例如伊波拉出血热和 COVID-19 的爆发,增加了对救护车、移动药房和移动加护病房的需求。在许多国家,救护车需求的成长速度超过了人口成长速度。一些国家使用先进的医疗车辆来应对突发卫生事件。例如,在取消 COVID-19感染疾病限制后,纽西兰的移动手术室服务已恢復。随着自动驾驶汽车技术的兴起和发展,预计在不久的将来紧急医疗车辆将配备半自动驾驶辅助技术。全球政府在执法和医疗保健设施上的支出增加正在推动对专用车辆的需求。

此外,日本使用的特种车辆数量从2012年的约164万辆增加到去年的177万辆。因此,SPV 的数量在过去十年中稳步增长。

亚太地区将在预测期内呈现最高成长率

预计亚太地区将引领特种车辆市场。技术发展的进步正在推动该地区特种车辆市场的成长。在 COVID-19感染疾病期间,多家公司向地方政府和其他国家交付了救护车。不过,疫情过后,救护车也有了新的发展,企业纷纷结成策略联盟,推出先进的救护车。

例如,2022年10月,紧急医疗回应服务供应商Medulance Healthcare与该国最大的通讯业者Reliance Jio合作推出了5G智慧连网救护车。

2022 年 5 月:印度首个电动车紧急应变装置将在 2022 年电动车博览会上亮相。 AmbulanceMe 应用程式与印度製造的电动救护车相容。

医疗保健车辆行业也是占据市场份额较大的行业。电力推进、独立病人舱、负压产生技术、紫外线消毒等创新变革等设计预计将在不久的将来推动医疗特种车辆市场的发展。

专用车产业概况

专用车市场高度分散,跨国公司如戴姆勒、通用汽车集团、沃尔沃AB等。市场上有许多针对电动和自动驾驶技术的收购、合资和投资。

例如,2022 年 2 月,Lightning e-Motors 宣布与通用汽车建立新的合作伙伴关係,使其成为第一家开发 100% 电动 3-6 级中型商用车的通用汽车特种车辆製造商 (SVM)。接驳车、货车、救护车和校车均采用通用汽车底盘。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 调查先决条件

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场动态

- 市场驱动因素

- 市场限制因素

- 波特五力分析

- 新进入者的威胁

- 买方议价能力

- 供应商的议价能力

- 替代产品的威胁

- 竞争公司之间的敌意强度

第五章市场区隔

- 按类型

- 救护车

- 消防车

- 移动式燃油运输罐车

- 其他的

- 按使用类型

- 执法和公共安全

- 医疗保健

- 露营者

- 其他的

- 按地区

- 北美洲

- 美国

- 加拿大

- 北美其他地区

- 欧洲

- 德国

- 英国

- 法国

- 其他欧洲国家

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

- 世界其他地区

- 南美洲

- 中东和非洲

- 北美洲

第六章 竞争形势

- 供应商市场占有率

- 公司简介

- LDV Inc.

- Force Motors Limited

- Matthews Specialty Vehicles Inc.

- Specialty Vehicles Inc.

- Farber Specialty Vehicles

- REV Group

- Daimler AG

- Volvo Group

- General Motors Company

- Spartan Motors Inc.(Shyft Group)

- Emergency One Group

- Oshkosh Corporation

第七章市场机会与未来趋势

The Specialty Vehicle Market size is estimated at USD 106.39 billion in 2024, and is expected to reach USD 124.30 billion by 2029, growing at a CAGR of 3.16% during the forecast period (2024-2029).

The market for specialty vehicle market experienced a decline in 2020, primarily owing to the COVID-19 pandemic, which caused a halt in transportation activities, disrupting the supply chain. However, after the lockdown measures were revoked, the market started witnessing significant growth as governing bodies across the world started investing heavily in healthcare facilities and emergency services, and associated equipment.

Over the long term, the expansion of the construction industry in countries such as China and India, with active participation from the private sector, is expected to drive the specialized vehicle market. The expansion of the logistics sector is expected to drive the demand for special pneumatically powered bulk carriers and tank truck trailers, which will drive the bulk carrier market. Therefore, players are also focusing on developing innovative products. For instance,

Key Highlights

- In October 2022, GAZ began manufacturing commercial vehicles GAZelle Next at the AvtoVAZ Argun plant in Chechenavto. The model can also be used for school buses, ambulances, housing, and community services.

Moreover, manufacturers are also focusing on lowering costs, new service model requirements, providing appealing services due to shifting platforms, and rising material and production prices. Customers' purchasing habits in the specialty vehicle industry are changing dramatically, particularly when it comes to product customization. As the demand for customization grows, OEMs face more options and complexity.

Asia-Pacific is anticipated to witness the highest CAGR over the forecast period, followed by Europe and North America. The usage of these vehicles by small businesses in the United States for purposes such as food truck businesses, mobile showrooms, and advertising and promotions, along with the demand for travel, medical, and healthcare response vehicles, is expected to rise during the forecast period.

Specialty Vehicles Market Trends

Increase in Spending on Law Enforcement and Healthcare Facilities

The rise in epidemics and pandemics, traffic accidents, household and industrial injuries, and government-sponsored healthcare programs is driving demand for medical and healthcare specialty vehicles. Diseases such as blood cancer, which affect one person every three minutes in the United States, have increased the demand for blood, propelling the market growth for bloodmobiles.

Recent epidemics and pandemics, such as the Ebola and COVID-19 outbreaks, have increased demand for ambulances, mobile pharmacies, and mobile intensive care units. In many countries, the increase in demand for ambulances has outpaced population growth. Several countries are using advanced healthcare vehicles to cater to health emergencies. For instance, after the COVID-19 lockdown restrictions were lifted, the mobile operation theatre service resumed in New Zealand. With the rise and development of autonomous vehicle technology, emergency medical vehicles are expected to be outfitted with semi-autonomous driving assistance technology in the near future. The increase in global government spending on law enforcement and healthcare facilities is driving the demand for specialty vehicles.

Moreover, the number of specialty vehicles in use in Japan reached 1.77 million last year, up from around 1.64 million in 2012. As a result, the number of SPVs increased steadily over the previous decade.

Asia-Pacific to Exhibit the Highest Growth Rate Over the Forecast Period

Asia-Pacific is anticipated to lead the specialty vehicle market. The advancements in technology developments are propelling the growth of the specialty vehicles market in the region. Various companies have delivered ambulances to local authorities and other countries during the COVID-19 pandemic. However, post-pandemic, there have also been new developments in ambulances as companies are getting into a strategic collaboration and launching advanced ambulances.

For instance, in October 2022, Medulance Healthcare, an emergency medical response service provider, launched a 5G-Smart connected ambulance in collaboration with Reliance Jio, the country's largest telecom operator.

In May 2022: At the EV Expo 2022, India's first EV emergency responder will be unveiled. The AmbulanceMe app is compatible with the Made in India Electric first responder vehicle.

The medical and healthcare response vehicles sector is another sector that holds a major share of the market. Design and other innovative changes such as electric propulsion, separate patient compartment, negative pressure creation technology, and UV disinfection are expected to propel the medical specialty vehicle market in the near future.

Specialty Vehicles Industry Overview

The specialty vehicle market is fairly fragmented, with multinational players including Daimler, GM Group, and Volvo AB. Many acquisitions, joint ventures, and investments in electric and autonomous driving technology are taking place in the market.

For instance, in February 2022, Lightning eMotors announced a new partnership with General Motors, making it the first GM Specialty Vehicle Manufacturer (SVM) to develop 100% electric Class 3 through 6 medium-duty commercial vehicles. Shuttles, delivery trucks, ambulances, and school buses are all supported by GM chassis.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.2 Market Restraints

- 4.3 Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Type

- 5.1.1 Ambulances

- 5.1.2 Fire Extinguishing Trucks

- 5.1.3 Mobile Fuel Carrying Tankers

- 5.1.4 Other Types

- 5.2 By Application Type

- 5.2.1 Law Enforcement And Public Safety

- 5.2.2 Medical And Healthcare

- 5.2.3 Recreational Vehicles

- 5.2.4 Other Services

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 Rest of the World

- 5.3.4.1 South America

- 5.3.4.2 Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles*

- 6.2.1 LDV Inc.

- 6.2.2 Force Motors Limited

- 6.2.3 Matthews Specialty Vehicles Inc.

- 6.2.4 Specialty Vehicles Inc.

- 6.2.5 Farber Specialty Vehicles

- 6.2.6 REV Group

- 6.2.7 Daimler AG

- 6.2.8 Volvo Group

- 6.2.9 General Motors Company

- 6.2.10 Spartan Motors Inc. (Shyft Group)

- 6.2.11 Emergency One Group

- 6.2.12 Oshkosh Corporation

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

工业车辆市场:按车辆类型、驱动类型、自主程度、应用分类 - 2024-2030 年全球预测

工业车辆市场:按车辆类型、驱动类型、自主程度、应用分类 - 2024-2030 年全球预测 全球工业车辆市场:按车辆类型、驱动类型、应用、能力、自主程度、类型、地区划分 - 到 2030 年的预测

全球工业车辆市场:按车辆类型、驱动类型、应用、能力、自主程度、类型、地区划分 - 到 2030 年的预测 中国商用卡车产业的成长机会

中国商用卡车产业的成长机会 工业车辆市场规模和预测、全球和地区份额、趋势和成长机会分析报告范围:按类型、驱动类型、自主程度、应用和地理位置

工业车辆市场规模和预测、全球和地区份额、趋势和成长机会分析报告范围:按类型、驱动类型、自主程度、应用和地理位置 电动轻型商用车:市场占有率分析、产业趋势与统计、成长预测(2024-2029)

电动轻型商用车:市场占有率分析、产业趋势与统计、成长预测(2024-2029) 2024 年工业车辆全球市场报告

2024 年工业车辆全球市场报告 工业车辆市场报告:2030 年趋势、预测与竞争分析

工业车辆市场报告:2030 年趋势、预测与竞争分析 全球特种商用车市场研究报告 - 2024 年至 2032 年产业分析、规模、份额、成长、趋势与预测

全球特种商用车市场研究报告 - 2024 年至 2032 年产业分析、规模、份额、成长、趋势与预测 特种商用车市场规模 - 按类型、按应用和预测,2024 年 - 2032 年

特种商用车市场规模 - 按类型、按应用和预测,2024 年 - 2032 年 2024-2028年全球商用车缓速器市场

2024-2028年全球商用车缓速器市场