|

市场调查报告书

商品编码

1440420

全球纸张和纸板包装 - 市场份额分析、行业趋势与统计、成长预测(2024 - 2029)Global Paper and Paperboard Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

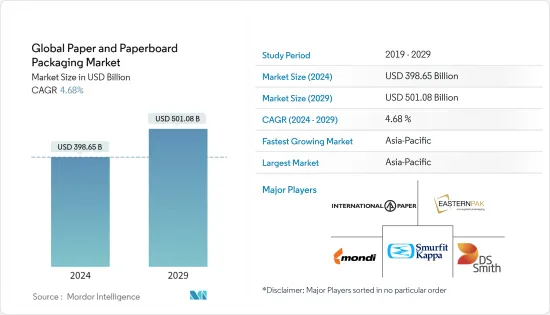

2024年,全球纸张和纸板包装市场规模预计为3986.5亿美元,预计到2029年将达到5,010.8亿美元,在预测期内(2024-2029年)CAGR为4.68%。

纸板和折迭纸盒一样,是製造容器最常用的材料。纸板必须经过製浆、可选的漂白、精炼、纸张成形、干燥、压光和捲绕等过程才能製造纸张。与金属和塑胶等其他材料相比,纸包装材料可以轻鬆重复使用和回收。

主要亮点

- 纸板包装是包装食品市场的首选。它存在于各种食物中,包括汤、调味品和乳製品。纸板通常覆盖有聚合物或塑料,以保持其清洁和不被损坏。与玻璃和金属相比,它有助于减轻最终产品的总重量,同时保持食品的新鲜度。由于其气味和味道中性,纸板是完美的包装材料。

- 电子商务销售的扩大和折迭纸盒包装需求的上升是推动市场的两大因素。然而,高性能替代品的出现可能会限制市场的成长。纸板包装是最受欢迎的环保包装选择之一。与其他体积较大的包装解决方案相比,这种包装格式可以以较小的占地面积创建各种尺寸,使其适用于几乎所有最终用户领域。

- 世界各地的消费者越来越意识到包装对环境的危害,并正在将他们的购买习惯转向更环保的选择。消费者、政府和媒体向製造商施加压力,要求其产品、包装和工艺更加环保。人们愿意为环保包装付出更多的钱。因此,纸板包装行业预计将由于这些趋势而增长。

- 然而,儘管对纸包装的需求增加,但不负责任的森林砍伐很快就会造成原料损失,严重影响纸板包装产业。据忧思科学家联盟称,纸张等「木製品」约占森林砍伐总量的 10%。其他主要来源包括牛、大豆和棕榈油。

- COVID-19 大流行对包装行业造成了严重破坏,全国范围内的封锁造成了影响,企业将采购从中国转移出去,包装中使用的材料也被重新考虑。儘管纸包装的供应面受到了实质影响,但特定应用领域最终用户需求的大幅成长显着扩大了纸包装的范围。

纸和纸板包装市场趋势

食品和饮料行业的需求增加

- 食品和饮料製造商正在做出更大的努力,提供可持续的材料和包装、功能性和方便的展示以及更健康的食品选择,以满足消费者的需求。纸袋在餐厅、饭店、咖啡馆和其他食品场所越来越受欢迎。同样,外带和线上送餐服务的日益普及也增加了食品服务中对纸袋的需求。

- 推动饮料趋势的相同基本要素也会影响饮料包装的趋势,也就是消费者的偏好。由于永续发展、客製化和电子商务,消费者的期望发生了变化,这激发了包装创新。

- 为了满足消费者的需求,领先的国际食品和饮料企业制定了使所有包装可回收或可生物降解的目标。例如,百加得表示打算透过发明新型纸质饮料瓶,在 2030 年消除塑料,加入全球反对一次性塑料的行动。这种对循环经济概念的奉献可以为造纸业带来更大的进步。

- 此外,永续发展在食品和饮料行业中得到了重视,快速消费品解决了产品包装产生的大量碳足迹。根据联合国统计,塑胶垃圾已从 1950 年的 200 万吨增加到 2017 年的 3.48 亿吨,预计到 2040 年将增加一倍。

预计亚太地区将占据重要份额

- 亚太地区是最大的折迭纸盒包装市场之一,由于其巨大的潜在扩张,需求可能会扩大。这主要是由中国推动的,中国是折迭纸盒的主要买家,就像许多其他行业一样。随着经济从製造业转向服务业,中国的经济成长率预计将放缓。

- 一些亚洲新兴国家的市场需求预计将强劲,而东北亚等老市场的成长预计将缓慢。亚太地区主导全球折迭纸盒包装产业。由于中国、印度和东南亚国家对即食食品的需求不断增长,市场需求增加。

- 随着人们关注的重点转向环保和永续实践,亚太地区多个行业的折迭纸盒需求不断增长,包括食品和饮料、医疗保健、个人护理、家庭护理、零售等。消费者对永续包装偏好、原材料可用性、纸张的轻质、可生物降解和可回收特性以及森林砍伐的认识都促进了该地区对折迭纸盒包装的需求。

- 由于印度和东南亚消费量的增长,对折迭纸盒包装的需求可能会增加。少数重要参与者定义了市场。回收级包装因其用于非接触类别(例如早餐麦片和茶)而最受欢迎。

- 印度、中国、日本和韩国是亚太地区正在经历工业化浪潮的主要国家,为瓦楞包装产品製造商提供了大量机会。瓦楞纸箱广泛应用于食品饮料、电子和电子商务等众多行业。随着人们越来越意识到生态和经济高效的包装选择,这些盒子在该地区的需求不断增加。

- 此外,受益于日益活跃的消费者基础,中国的个人护理市场一直是过去几年成长最快的行业之一,这也促进了所研究市场的成长。

纸和纸板包装产业概述

全球纸板包装市场相当分散。主要公司包括日本製纸工业公司、Mondi、METS BOARD、WestRock Company 和 ITC Limited。两家公司不断创新并建立策略伙伴关係,以维持其市场份额。

2022 年 12 月,Mondi 与 FRESH!PACKING 合作,打造了一款尖端的冷藏袋,供消费者运输冷冻或冷藏食品。 Fresh!Bag 的外层完全由 Mondi 的坚固牛皮纸製成,将冷却保护提高了 2.5 倍,取代了先前使用的多材料、不可回收的包装。袋子的冷却部分由纸浆製成。它采用 Mondi 牛皮纸封装,该牛皮纸经过认证,可在欧洲当前的纸张废物流中完全回收。由于纸张具有高拉伸性,将多层缝合在一起形成坚固的袋子结构变得简单。

2022 年 9 月,Smurfit Kappa 透露,已同意收购位于里约热内卢以东 70 公里的 Saquarema 的包装工厂 PaperBox。由于 Smurfit Kappa 已在米纳斯吉拉斯、南里奥格兰德州和塞阿拉开展业务,此次收购大大拓宽了 Smurfit Kappa 在巴西的营运基础。

额外的好处:

- Excel 格式的市场估算 (ME) 表

- 3 个月的分析师支持

目录

第 1 章:简介

- 研究假设和市场定义

- 研究范围

第 2 章:研究方法

第 3 章:执行摘要

第 4 章:市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代产品的威胁

- 竞争激烈程度

- 产业生态系统分析

- COVID-19 对市场的影响

第 5 章:市场动态

- 市场驱动因素

- 食品和饮料行业的需求不断增加

- 塑胶包装产品的法规促进了更高的需求

- 电子商务的不断增长创造了对各种纸和纸板包装类型的需求

- 市场挑战

- 原料成本增加和外包

- 森林砍伐对纸和纸板包装的影响

第 6 章:市场细分

- 北美洲

- 依产品类型

- 折迭纸盒

- 瓦楞纸箱

- 其他产品类型

- 按最终用户垂直领域

- 食物

- 饮料

- 卫生保健

- 个人护理

- 电力

- 其他最终用户垂直领域

- 按国家/地区

- 美国

- 加拿大

- 依产品类型

- 欧洲

- 依产品类型

- 折迭纸盒

- 瓦楞纸箱

- 其他产品类型

- 按最终用户垂直领域

- 食物

- 饮料

- 卫生保健

- 个人护理

- 电力

- 其他最终用户垂直领域

- 按国家/地区

- 英国

- 德国

- 法国

- 义大利

- 波兰

- 欧洲其他地区

- 依产品类型

- 亚太

- 依产品类型

- 折迭纸盒

- 瓦楞纸箱

- 其他产品类型

- 按最终用户垂直领域

- 食物

- 饮料

- 卫生保健

- 个人护理

- 电力

- 其他最终用户垂直领域

- 按国家/地区

- 中国

- 印度

- 韩国

- 日本

- 印尼

- 泰国

- 澳洲

- 亚太其他地区

- 依产品类型

- 中东和非洲

- 依产品类型

- 折迭纸盒

- 瓦楞纸箱

- 其他产品类型

- 按最终用户垂直领域

- 食物

- 饮料

- 卫生保健

- 个人护理

- 电力

- 其他最终用户垂直领域

- 按国家/地区

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 埃及

- 以色列

- 卡达

- 中东和非洲其他地区

- 依产品类型

- 拉丁美洲

- 依产品类型

- 折迭纸盒

- 瓦楞纸箱

- 其他产品类型

- 按最终用户垂直领域

- 食物

- 饮料

- 卫生保健

- 个人护理

- 电力

- 其他最终用户垂直领域

- 按国家/地区

- 巴西

- 墨西哥

- 阿根廷

- 哥伦比亚

- 拉丁美洲其他地区

- 依产品类型

第 7 章:贸易情景

- 历史进出口分析

- 主要进口国名单

- 主要出口国名单

- 重点

第 8 章:竞争格局

- 公司简介

- International Paper Company

- Eastern Pak Limited

- Mondi Group

- Smurfit Kappa Group

- DS Smith PLC

- WestRock Company

- Packaging Corporation of America

- Cascades Inc.

- Nippon Paper Industries Ltd

- Sonoco Products Company

第 9 章:市场的未来前景

The Global Paper and Paperboard Packaging Market size is estimated at USD 398.65 billion in 2024, and is expected to reach USD 501.08 billion by 2029, growing at a CAGR of 4.68% during the forecast period (2024-2029).

Paperboard, like folding cartons, is the most common material used to make containers. The paperboard must undergo processes such as pulping, optional bleaching, refining, sheet forming, drying, calendaring, and winding to manufacture paper. Paper packaging materials can be easily reused and recycled compared to other materials, such as metals and plastics.

Key Highlights

- Paperboard packaging is the preferred option in the packaged food market. It can be found in various foods, including soups, seasonings, and dairy products. Paperboard is usually covered with polymers or plastics to keep it clean and unspoiled. Compared to glass and metal, it helps reduce the final product's total weight while maintaining the freshness of the food product. Due to its odor and taste neutrality, paperboard is the perfect packing material.

- The expansion of e-commerce sales and the rising demand for folded carton packaging are two major factors driving the market. However, the availability of high-performance substitutes is likely to restrain the growth of the market. Paperboard packaging is one of the most popular eco-friendly packaging options. Compared to other bulkier packaging solutions, this packaging format can be created in various sizes with a small footprint, making it suitable for use in almost all end-user sectors.

- Consumers worldwide are becoming more conscious of the environmental hazards of packaging and are moving their purchasing habits to more environment-friendly options. Consumers, the government, and the media put pressure on manufacturers to make their products, packaging, and processes more environment friendly. People are willing to pay more for environment-friendly packaging. Thus, the paperboard packaging industry is expected to grow due to these trends.

- However, despite an increase in demand for paper packaging, irresponsible deforestation will severely impact the paperboard packaging industry by causing a loss of raw materials soon. According to the Union of Concerned Scientists, "wood products," such as paper, account for around 10% of total deforestation. Other major contributors include cattle, soybeans, and palm oil.

- The COVID-19 pandemic wreaked havoc on the packaging sector, with the impacts of nationwide lockdowns, corporations shifting their sourcing away from China, and materials used in packaging being reconsidered. Although there has been a substantial impact on the supply side of paper packaging, large growth in end-user demand in specific applications has significantly expanded the scope of paper packaging.

Paper & Paperboard Packaging Market Trends

Increase in Demand from the Food and Beverage Sector

- Food and beverage manufacturers are making more significant efforts to provide sustainable materials and packaging, functional and convenient displays, and healthier food options to meet consumer demands. Paper bags are becoming increasingly popular in restaurants, hotels, cafes, and other food establishments. Similarly, the growing popularity of on-the-go meals and online food delivery services has increased the demand for paper bags in food service.

- The same essential element that drives trends in drinks also influences trends in beverage packaging, which is consumer preference. Consumer expectations have changed due to sustainability, customization, and e-commerce, which motivates package innovation.

- In response to consumer demand, leading international food and beverage businesses have set objectives to make all packaging recyclable or biodegradable. For instance, Bacardi stated its intention to eliminate plastic by 2030 by inventing new paper-based beverage bottles, joining the global push against single-use plastics. This dedication to circular economy concepts can result in greater advancements in the paper industry.

- Furthermore, sustainability has gained prominence in the food and beverage industry, with CPGs addressing the significant carbon footprint incurred by product packaging. According to the United Nations, plastic waste has increased from 2 million metric tons in 1950 to 348 million metric tons in 2017, which is expected to double by 2040.

Asia-Pacific is Expected to Hold Significant Share

- The Asia-Pacific region is one of the largest folding carton packaging markets, and the demand is likely to expand due to its significant potential expansion. This is mainly driven by China, a major buyer of folding cartons, as it is in many other industries. It is expected to slow in China as the economy shifts from manufacturing to services.

- The market's demand in some emerging Asian countries is expected to be strong, while growth in older markets, such as North-East Asia, is expected to be slow. The Asia-Pacific region dominates the global folding carton packaging industry. The demand for the market increases due to the rising demand for ready-to-eat meals in China, India, and Southeast Asian countries.

- As the focus is changing to eco-friendly and sustainable practices, folding carton demand has been growing across several industries in the Asia-Pacific, including food and beverage, healthcare, personal care, homecare, retail, and others. Consumer awareness of sustainable packaging preferences, raw material availability, the lightweight, biodegradable, and recyclable characteristics of paper, and deforestation have all contributed to the demand for folding carton packaging in the region.

- Demand for folding carton packaging is likely to rise due to rising consumption in India and Southeast Asia. A small number of significant participants define the market. Recycled-grade packaging is the most popular due to its use in non-contact categories, such as breakfast cereals and tea.

- India, China, Japan, and South Korea are major countries in the Asia-Pacific region experiencing a surge in industrialization, providing substantial opportunities for corrugated packaging product manufacturers. Corrugated boxes are used in numerous industries, such as food and beverage, electronics, and e-commerce. These boxes are witnessing increased demand in the region as people become more aware of ecological and cost-effective packaging options.

- Furthermore, the personal care market in China has been one of the fastest-growing sectors in the last few years, benefitting from an increasingly engaged consumer base, which is augmenting the growth of the market studied.

Paper & Paperboard Packaging Industry Overview

The global market for paperboard packaging is quite fragmented. Nippon Paper Industries Co. Ltd, Mondi, METS BOARD, WestRock Company, and ITC Limited are among the major companies. The corporations continue to innovate and form strategic partnerships to maintain their market share.

In December 2022, in collaboration with FRESH!PACKING, Mondi created a cutting-edge cooler bag for consumers to transport frozen or chilled foods. While boosting cooling protection by up to 2.5 times, the Fresh!Bag's exterior layer is entirely made of sturdy kraft paper from Mondi, replacing the multi-material, non-recyclable packaging that was previously utilized. The cooling portion of the bag is made from pulp. It is enclosed in kraft paper from Mondi, which is certified as completely recyclable in Europe's current paper waste streams. Due to the paper's high stretchability, stitching the many plies together to form a sturdy bag structure was made simple.

In September 2022, Smurfit Kappa disclosed that it had agreed to buy PaperBox, a packaging facility in Saquarema, 70 kilometers east of Rio de Janeiro. Since it already operates in Minas Gerais, Rio Grande do Sul, and Ceara, this acquisition considerably widened Smurfit Kappa's operational base in Brazil.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definitions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHT

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Ecosystem Analysis

- 4.4 Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Demand from the Food and Beverage Sector

- 5.1.2 Regulations on Plastic-based Packaging Products Contribute to Higher Demand

- 5.1.3 Increasing Growth of E-commerce Creates Demand for Various Paper and Paperboard Packaging Types

- 5.2 Market Challenges

- 5.2.1 Increasing Raw Material Costs and Outsourcing

- 5.2.2 Effects of Deforestation on Paper and Paperboard Packaging

6 MARKET SEGMENTATION

- 6.1 North America

- 6.1.1 By Product Type

- 6.1.1.1 Folding Cartons

- 6.1.1.2 Corrugated Boxes

- 6.1.1.3 Other Product Types

- 6.1.2 By End-user Vertical

- 6.1.2.1 Food

- 6.1.2.2 Beverage

- 6.1.2.3 Healthcare

- 6.1.2.4 Personal Care

- 6.1.2.5 Electrical

- 6.1.2.6 Other End-user Verticals

- 6.1.3 By Country

- 6.1.3.1 United States

- 6.1.3.2 Canada

- 6.1.1 By Product Type

- 6.2 Europe

- 6.2.1 By Product Type

- 6.2.1.1 Folding Cartons

- 6.2.1.2 Corrugated Boxes

- 6.2.1.3 Other Product Types

- 6.2.2 By End-user Vertical

- 6.2.2.1 Food

- 6.2.2.2 Beverage

- 6.2.2.3 Healthcare

- 6.2.2.4 Personal Care

- 6.2.2.5 Electrical

- 6.2.2.6 Other End-user Verticals

- 6.2.3 By Country

- 6.2.3.1 United Kingdom

- 6.2.3.2 Germany

- 6.2.3.3 France

- 6.2.3.4 Italy

- 6.2.3.5 Poland

- 6.2.3.6 Rest of Europe

- 6.2.1 By Product Type

- 6.3 Asia-Pacific

- 6.3.1 By Product Type

- 6.3.1.1 Folding Cartons

- 6.3.1.2 Corrugated Boxes

- 6.3.1.3 Other Product Types

- 6.3.2 By End-user Vertical

- 6.3.2.1 Food

- 6.3.2.2 Beverage

- 6.3.2.3 Healthcare

- 6.3.2.4 Personal Care

- 6.3.2.5 Electrical

- 6.3.2.6 Other End-user Verticals

- 6.3.3 By Country

- 6.3.3.1 China

- 6.3.3.2 India

- 6.3.3.3 South Korea

- 6.3.3.4 Japan

- 6.3.3.5 Indonesia

- 6.3.3.6 Thailand

- 6.3.3.7 Australia

- 6.3.3.8 Rest of Asia-Pacific

- 6.3.1 By Product Type

- 6.4 Middle East and Africa

- 6.4.1 By Product Type

- 6.4.1.1 Folding Cartons

- 6.4.1.2 Corrugated Boxes

- 6.4.1.3 Other Product Types

- 6.4.2 By End-user Vertical

- 6.4.2.1 Food

- 6.4.2.2 Beverage

- 6.4.2.3 Healthcare

- 6.4.2.4 Personal Care

- 6.4.2.5 Electrical

- 6.4.2.6 Other End-user Verticals

- 6.4.3 By Country

- 6.4.3.1 Saudi Arabia

- 6.4.3.2 United Arab Emirates

- 6.4.3.3 Egypt

- 6.4.3.4 Israel

- 6.4.3.5 Qatar

- 6.4.3.6 Rest of Middle East and Africa

- 6.4.1 By Product Type

- 6.5 Latin America

- 6.5.1 By Product Type

- 6.5.1.1 Folding Cartons

- 6.5.1.2 Corrugated Boxes

- 6.5.1.3 Other Product Types

- 6.5.2 By End-user Vertical

- 6.5.2.1 Food

- 6.5.2.2 Beverage

- 6.5.2.3 Healthcare

- 6.5.2.4 Personal Care

- 6.5.2.5 Electrical

- 6.5.2.6 Other End-user Verticals

- 6.5.3 By Country

- 6.5.3.1 Brazil

- 6.5.3.2 Mexico

- 6.5.3.3 Argentina

- 6.5.3.4 Colombia

- 6.5.3.5 Rest of Latin America

- 6.5.1 By Product Type

7 TRADE SCENARIO

- 7.1 Historical Import-Export Analysis

- 7.2 List of Major Importing Countries

- 7.3 List of Major Exporting Countries

- 7.4 Key Takeaways

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles

- 8.1.1 International Paper Company

- 8.1.2 Eastern Pak Limited

- 8.1.3 Mondi Group

- 8.1.4 Smurfit Kappa Group

- 8.1.5 DS Smith PLC

- 8.1.6 WestRock Company

- 8.1.7 Packaging Corporation of America

- 8.1.8 Cascades Inc.

- 8.1.9 Nippon Paper Industries Ltd

- 8.1.10 Sonoco Products Company

9 FUTURE OUTLOOK OF THE MARKET

全球原纸包装市场预测(~2030 年):按产品、类型、应用、最终用户和地区进行分析

全球原纸包装市场预测(~2030 年):按产品、类型、应用、最终用户和地区进行分析 全球折迭盒市场 - 2024-2031

全球折迭盒市场 - 2024-2031 2024 年世界纸和纸板包装市场报告

2024 年世界纸和纸板包装市场报告 纸包装市场评估:依纸张类型、来源、包装类型、包装水准、最终用户产业和地区划分的机会和预测(2017-2031)

纸包装市场评估:依纸张类型、来源、包装类型、包装水准、最终用户产业和地区划分的机会和预测(2017-2031) 2024 年纸板包装世界市场报告

2024 年纸板包装世界市场报告 纸包装:市场占有率分析、产业趋势与统计、成长预测(2024-2029)

纸包装:市场占有率分析、产业趋势与统计、成长预测(2024-2029) 纸板包装 -市场占有率分析、产业趋势与统计、成长预测(2024-2029)

纸板包装 -市场占有率分析、产业趋势与统计、成长预测(2024-2029) 2024 年挠性纸包装全球市场报告

2024 年挠性纸包装全球市场报告 2024-2032 年按产品类型、等级、包装水平、最终用途行业和地区分類的纸包装市场报告

2024-2032 年按产品类型、等级、包装水平、最终用途行业和地区分類的纸包装市场报告 可拉伸纸包装市场:按材料类型、产品型态、应用和最终用户划分 - 全球预测 2024-2030

可拉伸纸包装市场:按材料类型、产品型态、应用和最终用户划分 - 全球预测 2024-2030