|

市场调查报告书

商品编码

1519919

全球氢氧化锂市场:市场占有率分析、产业趋势/统计、成长预测(2024-2029)Lithium Hydroxide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

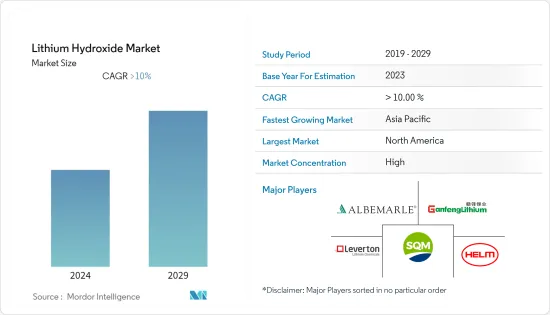

预计2024年全球氢氧化锂市场规模将达196.5LCE千吨,2024年至2029年复合年增长率为23.51%,2029年将达564.78LCE千吨。

COVID-19 阻碍了氢氧化锂市场。疫情导致电动车和消费性电子产品中使用的锂离子电池的需求下降。汽车产量下降,非必需消费品支出下降,工业活动放缓,导致对氢氧化锂和其他电池材料的需求减少。不过,各地区的封锁措施已经解除,经济活动也逐渐恢復。因此,电动车和家用电器的需求增加,带动了氢氧化锂的需求。

推动氢氧化锂市场的主要因素是使用锂离子电池的电动车需求的增加以及使用氢氧化锂NCA正极的电动工具的需求的增加。

然而,对氢氧化锂毒性和高生产成本的日益担忧预计将限制氢氧化锂市场的成长。

锂矿床的开拓和对行动电子设备日益增长的需求预计将在未来为市场相关人员提供各种机会。

由于电动车产业的需求不断增长,亚太地区在氢氧化锂市场上占据主导地位。

氢氧化锂市场趋势

电池领域占据市场主导地位

- 氢氧化锂的主要消费者是锂离子电池,占总消费量的大部分。便携式电子产品、电动车和能源储存系统对锂离子电池的需求不断增长是氢氧化锂市场的主要驱动力。

- 向电动车的过渡是锂离子电池市场最重要的驱动力之一。随着世界各国政府实施更严格的排放法规并鼓励采用电动车,对锂离子电池的需求不断增加,推动了对氢氧化锂的需求。

- 根据国际能源总署(IEA)发布的预测,2022年全球电动车保有量预计约2,590万辆。

- 根据国际能源总署(IEA)预测,电动车市场正在快速成长,预计到2022年销量将超过1,000万辆。三年内,电动车占总销量的份额从 2020 年至 2022 年的 4% 增至 14%。

- 电动车销量的成长预计将持续到 2023 年。第一季购买量超过230万台,比去年同期成长25%。 2023年终,销量将达到1400万台,与前一年同期比较增长35%。因此,到 2023 年,电动车将占所有汽车销量的 18%。

- 透过持续研发努力提高电池性能、能量密度和安全性,锂离子电池在氢氧化锂市场的主导地位进一步加强。技术进步正在推动锂离子电池在广泛的应用中被采用,并巩固其作为氢氧化锂主要消费者的地位。

- 电动车对锂离子电池的高需求正在增加锂离子电池领域在氢氧化锂市场的主导地位。

亚太地区主导市场

- 亚太地区有几家重要的氢氧化锂生产商,包括中国、日本、韩国和澳洲。这些国家已经建立了锂开采和加工业,并供应了世界上大部分的氢氧化锂供应。

- 根据美国地质调查局预测,到2023年,中国将成为全球第三大锂生产国。预计2023年中国锂矿产量将达3.3万吨。

- 中国大部分锂蕴藏量位于西藏自治区、青海省和四川省。然而,儘管拥有大量蕴藏量,但由于国内需求远超过产能,中国仍是锂的净进口国。

- 亚太地区引领全球电动车市场,韩国、日本、中国等国家是电动车的重要生产国和消费国。随着电动车在该地区的不断普及,对锂离子电池和氢氧化锂的需求也在增加。

- 根据中国工业协会预测,2022年中国电池式电动车销量约540万辆,较2021年成长83.95%。同年,中国插电式混合动力汽车销量达约150万辆,与前一年同期比较成长151.91%。

- 亚太地区正在迅速扩大其可再生能源产能,特别是在中国和印度等国家。由氢氧化锂驱动的锂离子电池在再生能源来源的能源储存系统中发挥重要作用,并推动了该地区对氢氧化锂的需求。

- 根据国际可再生能源机构(IRENA)发布的估计,印度可再生能源装置容量已从2018年的118.19吉瓦增加到2022年的162.96吉瓦。

- 因此,受上述因素影响,预计未来亚太地区对氢氧化锂的需求将会增加。

氢氧化锂产业概况

氢氧化锂市场得到巩固。主要企业(排名不分先后)包括 SQM SA、Albemarle Corporation、赣锋锂业集团、Livent 和 LevertonHELM Limited。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章 简介

- 调查先决条件

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场动态

- 促进因素

- 电动车需求增加

- 电动工具需求增加

- 抑制因素

- 人们越来越担心毒性

- 生产成本高

- 产业价值链分析

- 波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章市场区隔(市场规模:基于数量)

- 目的

- 锂离子电池

- 润滑脂

- 精製

- 其他用途

- 地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 马来西亚

- 泰国

- 印尼

- 越南

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 义大利

- 法国

- 西班牙

- 土耳其

- 俄罗斯

- 北欧的

- 欧洲其他地区

- 南美洲

- 巴西

- 阿根廷

- 哥伦比亚

- 南美洲其他地区

- 中东/非洲

- 沙乌地阿拉伯

- 南非

- 奈及利亚

- 卡达

- 埃及

- 阿拉伯聯合大公国

- 其他中东/非洲

- 亚太地区

第六章 竞争状况

- 併购、合资、联盟、协议

- 市场占有率(%)/排名分析

- 主要企业策略

- 公司简介

- SQM SA

- Albemarle Corporation

- Fitz Chem LLC(Nagase America LLC)

- Ganfeng Lithium Group Co., Ltd

- KANTO KAGAKU

- LevertonHELM Limited

- Livent

- Nemaska Lithium

- Shangai China Lithium Industrial Co. Ltd

- SICHUAN BRIVO LITHIUM MATERIALS CO., LTD.

- Tianqi Lithium

第七章 市场机会及未来趋势

- 锂矿床

- 对便携式电子设备的需求增加

The Lithium Hydroxide Market size is estimated at 196.5 LCE kilotons in 2024, and is expected to reach 564.78 LCE kilotons by 2029, growing at a CAGR of 23.51% during the forecast period (2024-2029).

COVID-19 hampered the lithium hydroxide market. The pandemic led to reduced demand for lithium-ion batteries that are used in electric vehicles and consumer electronics. Automotive production declined, consumer spending on discretionary items decreased, and industrial activity slowed down, resulting in lower demand for lithium hydroxide and other battery materials. However, as lockdown measures were lifted, economic activities gradually resumed across regions. This led to increased demand for electric vehicles and consumer electronics, driving the demand for lithium hydroxide.

Major factors driving the lithium hydroxide market are the increasing demand for electric vehicles that use lithium-ion batteries and the increasing demand for power tools that use lithium hydroxide NCA cathode.

However, rising concerns regarding the toxicity of lithium hydroxide and the high production costs are expected to restrain the growth of the lithium hydroxide market.

Development in lithium deposits and the rising demand for portable electronic devices are expected to offer various opportunities to the market players in the upcoming period.

Asia-Pacific dominates the lithium hydroxide market due to the increasing demand from the EV sector.

Lithium Hydroxide Market Trends

Batteries Segment to Dominate the Market

- Lithium-ion batteries are the primary consumer of lithium hydroxide, accounting for a significant portion of its total consumption. The growing demand for lithium-ion batteries in portable electronic devices, electric vehicles, and energy storage systems is a significant driver of the lithium hydroxide market.

- The transition to electric mobility is one of the most significant drivers of the lithium-ion battery market. As governments worldwide implement stricter emissions regulations and incentivize the adoption of electric vehicles, the demand for lithium-ion batteries increases, thereby driving the demand for lithium hydroxide.

- According to the estimate released by the International Energy Agency (IEA), the total estimated number of electric vehicles in use globally will be approximately 25.9 million in 2022.

- According to the estimate released by the International Energy Agency, the electric vehicle market is experiencing exponential growth, with more than 10 million vehicles sold in 2022. Within three years, the share of electrical vehicles in overall sales has increased from 4% to 14% between 2020 and 2022.

- The increase in EV sales was expected to continue through 2023. In the first quarter, over 2.3 million of these vehicles were bought, a 25% increase compared to last year. By the end of 2023, sales had reached 14 million and accounted for a 35% year-on-year increase, while new purchases accelerated in the second half of the year. As a result, in 2023, electric cars accounted for 18% of total car sales.

- The dominance of lithium-ion batteries in the lithium hydroxide market is further strengthened by continued R&D efforts to improve battery performance, energy density, and security. Technological advancements drive the adoption of lithium-ion batteries in a wide range of applications, reinforcing their position as the leading consumer of lithium hydroxide.

- The high demand for lithium-ion batteries in electric vehicles drives the dominance of the lithium-ion batteries segment in the lithium hydroxide market.

Asia-Pacific Region to Dominate the Market

- Asia-Pacific is home to several critical manufacturers of lithium hydroxide, including China, Japan, South Korea, and Australia. These countries have well-established lithium mining and processing industries, providing a significant portion of the global supply of lithium hydroxide.

- According to the US Geological Survey, China will be the world's third-largest lithium-producing nation in 2023 based on production volume. The mine production of lithium in China amounted to an estimated 33,000 metric tons in 2023.

- Most of China's lithium reserves are located in the Tibet Autonomous Region, Qinghai Province, and Sichuan Province. However, despite having substantial reserves, China is a net importer of lithium due to the fact that its domestic demand far exceeds its production capacity.

- Asia-Pacific leads the global electric vehicle market, with countries such as South Korea, Japan, and China being significant producers and consumers of electric vehicles. There is a corresponding increase in demand for lithium-ion batteries and lithium hydroxide as electric vehicles continue to be adopted in the region.

- According to the estimate released by the China Association of Automobile Manufacturers (CAAM), in China, around 5.4 million battery electric vehicles will be sold in 2022, an increase of 83.95 % compared to 2021. In the same year, sales of plugin hybrid vehicles in China increased by 151.91% compared to the previous year and amounted to around 1.5 million units.

- The Asia Pacific region has been rapidly expanding its renewable energy capacity, particularly in countries like China and India. Lithium-ion batteries, powered by lithium hydroxide, play a crucial role in energy storage systems for renewable energy sources that are driving the demand for lithium hydroxide in the region.

- According to the estimate released by the International Renewable Energy Agency (IRENA), India's renewable energy capacity increased from 118.19 gigawatts in 2018 to 162.96 gigawatts in 2022.

- Thus, the factors mentioned above are expected to increase the demand for lithium hydroxide in the Asia-Pacific region in the upcoming period.

Lithium Hydroxide Industry Overview

The lithium hydroxide market is consolidated. The major players (not in any particular order) include SQM S.A., Albemarle Corporation, Ganfeng Lithium Group Co., Ltd, Livent, and LevertonHELM Limited.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand for Electric Vehicles

- 4.1.2 Increasing Demand for Power Tools

- 4.2 Restraints

- 4.2.1 Rising concern About the Toxicity

- 4.2.2 High production Costs

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Application

- 5.1.1 Lithium-ion Batteries

- 5.1.2 Lubricating Greases

- 5.1.3 Purification

- 5.1.4 Other Applications (Polymer Production)

- 5.2 Geography

- 5.2.1 Asia-Pacific

- 5.2.1.1 China

- 5.2.1.2 India

- 5.2.1.3 Japan

- 5.2.1.4 South Korea

- 5.2.1.5 Malaysia

- 5.2.1.6 Thailand

- 5.2.1.7 Indonesia

- 5.2.1.8 Vietnam

- 5.2.1.9 Rest of Asia-Pacific

- 5.2.2 North America

- 5.2.2.1 United States

- 5.2.2.2 Canada

- 5.2.2.3 Mexico

- 5.2.3 Europe

- 5.2.3.1 Germany

- 5.2.3.2 United Kingdom

- 5.2.3.3 Italy

- 5.2.3.4 France

- 5.2.3.5 Spain

- 5.2.3.6 Turkey

- 5.2.3.7 Russia

- 5.2.3.8 NORDIC

- 5.2.3.9 Rest of Europe

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Colombia

- 5.2.4.4 Rest of South America

- 5.2.5 Middle-East and Africa

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 South Africa

- 5.2.5.3 Nigeria

- 5.2.5.4 Qatar

- 5.2.5.5 Egypt

- 5.2.5.6 UAE

- 5.2.5.7 Rest of Middle-East and Africa

- 5.2.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 SQM S.A.

- 6.4.2 Albemarle Corporation

- 6.4.3 Fitz Chem LLC (Nagase America LLC)

- 6.4.4 Ganfeng Lithium Group Co., Ltd

- 6.4.5 KANTO KAGAKU

- 6.4.6 LevertonHELM Limited

- 6.4.7 Livent

- 6.4.8 Nemaska Lithium

- 6.4.9 Shangai China Lithium Industrial Co. Ltd

- 6.4.10 SICHUAN BRIVO LITHIUM MATERIALS CO., LTD.

- 6.4.11 Tianqi Lithium

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Development in Lithium deposits

- 7.2 Rising Demand for Portable Electronic Devices

2025年锂全球市场报告

2025年锂全球市场报告 六氟磷酸锂市场规模、份额及成长分析(按形式、产品类型、应用和地区)-产业预测,2025-2032

六氟磷酸锂市场规模、份额及成长分析(按形式、产品类型、应用和地区)-产业预测,2025-2032 氯化锂市场规模、份额、成长分析(按类型、应用、最终用途产业和地区)- 产业预测(2025-2032)2025年锂电气设备全球市场报告

氯化锂市场规模、份额、成长分析(按类型、应用、最终用途产业和地区)- 产业预测(2025-2032)2025年锂电气设备全球市场报告 直接锂开采的全球市场(2026年~2036年)

直接锂开采的全球市场(2026年~2036年) 全球六氟磷酸锂市场:按产品、应用、地区和国家分析和预测(2025-2034 年)

全球六氟磷酸锂市场:按产品、应用、地区和国家分析和预测(2025-2034 年) 锂市场规模、份额和趋势分析报告:2025 年至 2030 年按产品、应用、地区和细分市场预测

锂市场规模、份额和趋势分析报告:2025 年至 2030 年按产品、应用、地区和细分市场预测 2032 年锂市场预测:按产品、来源类型、应用、最终用户和地区进行的全球分析氢氧化锂市场机会、成长动力、产业趋势分析及2025-2034年预测2032 年六氟磷酸锂市场预测:按产品类型、分销管道、应用、最终用户和地区进行的全球分析

2032 年锂市场预测:按产品、来源类型、应用、最终用户和地区进行的全球分析氢氧化锂市场机会、成长动力、产业趋势分析及2025-2034年预测2032 年六氟磷酸锂市场预测:按产品类型、分销管道、应用、最终用户和地区进行的全球分析