|

市场调查报告书

商品编码

1521777

汽车被动电子元件:市场占有率分析、产业趋势/统计、成长预测(2024-2029)Automotive Passive Electronic Components - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

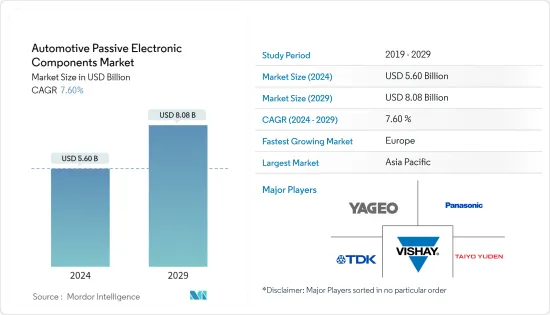

汽车被动电子元件市场规模预计到2024年为56亿美元,预计到2029年将达到80.8亿美元,在预测期内(2024-2029年)复合年增长率为7.60%。

主要亮点

- 汽车产业在被动元件需求不断增长方面处于领先地位。各种应用对汽车电子系统的需求不断增长,包括引擎盖下的电控系统(ECU)、资讯娱乐系统和高级驾驶员辅助系统 (ADAS)。汽车电子系统需要高品质的元件来确保可靠的性能,包括用于滤波和储能的电容器、用于电路保护的压敏电阻、用于小型ECU的连接器以及用于连接支援所需的射频和微波被动元件和天线。

- 汽车製造商越来越多地将电子元件整合到传统内燃机汽车中,以提高燃油效率、减少排放气体并提高车辆的整体性能。这一趋势正在推动对电阻器、电容器和电感器等被动电子元件的需求。例如,根据SIAM India的数据,2023财年国内市场乘用车销量超过389万辆。

- ADAS(高级驾驶辅助系统),例如防撞系统和主动式车距维持定速系统,严重依赖电容器等被动电子元件来进行感测器讯号处理、滤波和资料传输。现代车辆配备了先进的资讯娱乐系统、远端讯息和连接解决方案,需要被动元件来进行无线通讯、讯号处理和资料传输。

- 随着汽车电子变得越来越小、整合度越来越高,被动元件必须满足日益严格的尺寸和重量要求。小型化挑战(例如在缩小封装尺寸的同时保持性能)可能会限制市场成长。此外,设计和製造汽车级被动电子元件需要大量的研究、开发和测试。高开发成本限制了市场创新。

- 永续性和气候变迁等环境议题影响着汽车产业的趋势和法规。对生态永续性的日益重视可能会推动汽车中采用节能环保的电子元件。此外,贸易政策、关税和贸易协定也会影响汽车零件的成本和可得性。贸易政策的变化可能会扰乱供应链、影响定价并影响市场竞争。

汽车被动电子元件市场趋势

电容器正在经历显着成长

- 电容器技术的进步正在开发更小、更轻、更有效率的电容器。这使得汽车製造商能够设计更小、更轻的电子系统,从而减轻车辆总重量并提高燃油效率。 ADAS(高级驾驶辅助系统)、资讯娱乐系统和汽车连接功能的日益普及需要强大且可靠的电子元件。电容器透过提供稳定的电源并确保感测器、摄影机和通讯模组的平稳运作来支援这些功能的实现。

- 例如,2023年8月,TDK公司在印度(Nasik)提高了产能,并开启了业务前景。纳西克的这项特殊工厂扩大了生产能力,并引进了占地约 23,000平方公尺的新建筑。未来四年,将增加更多用于汽车领域的直流电容器生产线。这些电容器是为印度国内市场製造并出口国外的。产能的增加创造了支持公司中期成长策略的新前景。

- 严格的政府法规和燃油经济性标准正在推动对节能车辆系统的需求。电容器有助于优化能源使用并最大限度地减少功率损耗,满足监管要求和永续性目标。电容器对于汽车电子系统的功能至关重要,随着汽车电气化、互联化和自动化趋势的加速,预计需求将持续成长。

- 例如,2024 年 5 月,现代汽车计划利用其在美国已获得的投资,在其电动车工厂生产混合动力汽车。这家全球第三大汽车製造商及其附属公司起亚汽车公司打算利用专门用于其位于乔治亚的电动车和电池製造工厂的资金来生产混合动力汽车。拥有现代汽车和起亚汽车的韩国现代汽车集团宣布,计划投资126亿美元在乔治亚建设新的电动车和电池生产工厂。

欧洲占主要市场占有率

- 欧洲拥有一些世界上最大的汽车市场,包括英国、德国和法国。欧洲占世界汽车产量和销售量的大部分。这些国家对商用车和乘用车的需求不断增长,为各种汽车系统中使用的被动电子元件市场做出了贡献。

- 在欧洲,电动车 (EV)、纯电动车 (BEV) 和混合动力电动车 (HEV) 的引进进展迅速。欧洲政府的激励措施和技术进步正在促进动力传动系统电气化的过渡。这种转变将增加对电动传动系统、电池管理系统和汽车电子中使用的电容器、电感器和电阻器等被动电子元件的需求。例如,根据KBA的一份报告,到2023年,包括纯电动车和插电式混合动力车在内的电动车将占德国乘用车的约4.8%。在规定的时间内,电动车的比例每年都在稳定成长,特别是纯电动车车型。

- 英国、德国、法国等欧洲国家的汽车工业走在技术创新的前沿,致力于发展先进的汽车技术。这包括智慧功能、连接解决方案和 ADAS 整合。这些技术需要各种被动电子元件来支援车辆网路等功能。

- 例如,2023 年 11 月,英国政府宣布投资 1.5 亿欧元(1 亿美元),作为 45 亿欧元(570 万美元)重大投资的一部分,以支持英国製造业并刺激经济扩张(8,900 万美元)。这笔资金的目标是到 2030 年连网型和自动化移动 (CAM) 领域。分配给支持 CAM 的预算将得到行业捐款的补充。这将使英国连网型和自动驾驶汽车中心(CCAV)巩固英国作为自动驾驶技术、产品和服务的创造、进步、实施和生产的全球领导者的地位。

汽车无源电子元件产业概况

汽车被动电子元件市场竞争激烈。市场高度集中,参与企业规模各异。所有主要公司都占有重要的市场占有率,并致力于扩大其全球消费群。该市场的主要企业包括国巨公司、松下公司、TDK公司、Vishay Intertechnology Inc.和太阳诱电公司。公司正在透过建立多个联盟、合作伙伴关係、收购和投资新产品推出来增加其市场占有率,以获得在预测期内的竞争优势。

2024 年 3 月 JF Kilfoil 公司扩大 Knowles 产品的经销范围,将 Cornell Dubilier 品牌纳入中西部市场。此次合作是在 Knowles 收购 Cornell Dubilier 之际达成的,后者现在提供更广泛的薄膜、电解和特殊电容器。产品系列包括单层电容器、微调电容器、电解电容器、铝聚合物电容器、薄膜电容器、云母电容器和超级电容。这些产品以其高可靠性、长寿命以及在恶劣条件下的优异性能而闻名。

2023 年 9 月 Knowles Precision Devices 以 2.63 亿美元现金收购 Cornell Dubilier。此次收购包括薄膜、电解和云端母电容器产品,预计到 2024 年将增加非 GAAP 每股收益。 Cornell Dubilier 的各种电源薄膜、电解电容器和云母电容器与 Knowles 的精密装置部门结合,为目前和未来的客户提供了价值提案和扩展的产品系列。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行概述

第四章市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 新进入者的威胁

- 买家/消费者的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争公司之间的敌对关係

- 技术简介

- COVID-19 和其他宏观经济因素对市场的影响

第五章市场动态

- 市场驱动因素

- 先进电子设备在工业上的使用增加

- 对较小设计的偏好增加

- 市场限制因素

- 用于生产被动电子元件的重要金属的价格波动/各种被动元件生产中的挑战

第六章 市场细分

- 按类型

- 冷凝器

- 陶瓷电容器

- 钽电容

- 电解电容器

- 纸/塑膜电容器

- 超级电容

- 电感器

- 电阻器

- 表面黏着技术晶片

- 网路和阵列

- 其他特殊物品

- EMC滤波器

- 冷凝器

- 按地区*

- 北美洲

- 欧洲

- 亚洲

- 澳洲/纽西兰

- 中东/非洲

- 拉丁美洲

第七章 竞争格局

- 公司简介

- Yageo Corporation

- Panasonic Corporation

- TDK Corporation

- Vishay Intertechnology Inc.

- Taiyo Yuden Corporation

- Kyocera Corporation(includes AVX Corporation)

- Knowles Precision Devices

- Murata Manufacturing Co. Ltd

- Samsung Electro-Mechanical

- KOA Corporation

- Rubycon Corporation

- Nippon Chemi-Con Corporation

第八章投资分析

第9章市场的未来

The Automotive Passive Electronic Components Market size is estimated at USD 5.60 billion in 2024, and is expected to reach USD 8.08 billion by 2029, growing at a CAGR of 7.60% during the forecast period (2024-2029).

Key Highlights

- The automotive industry is leading the way in the increasing need for passive components. The demand for electronic vehicle systems is rising for various uses, such as electronic control units (ECUs) under the hood, infotainment systems, and advanced driver assistance systems (ADASs). Automotive electronic systems require high-quality components to guarantee dependable performance, like capacitors for filtering and storing energy, varistors for circuit protection, connectors for small ECUs, and RF and microwave passive components and antennas for connectivity support.

- Automobile manufacturers increasingly integrate electronic components into traditional combustion engine vehicles to enhance fuel efficiency, reduce emissions, and improve overall vehicle performance. This trend drives the demand for passive electronic components like resistors, capacitors, and inductors. For instance, according to SIAM India, during the fiscal year 2023, more than 3.89 million passenger vehicles were sold in the domestic market.

- ADAS (advanced driver assistance systems), such as collision avoidance systems and adaptive cruise control, rely heavily on passive electronic components like capacitors for sensor signal processing, filtering, and data transmission. Modern vehicles feature advanced infotainment systems, telematics, and connectivity solutions that require passive components for wireless communication, signal processing, and data transmission.

- As automotive electronics become more compact and integrated, passive components must meet increasingly stringent size and weight requirements. Miniaturization challenges, such as maintaining performance while reducing package size, can limit market growth. In addition, designing and manufacturing automotive-grade passive electronic components require significant research, development, and testing. High development costs limit innovation in the market.

- Environmental concerns, including sustainability and climate change, influence automotive industry trends and regulations. Growing emphasis on ecological sustainability may drive the adoption of vehicles' energy-efficient and environmentally friendly electronic components. Moreover, trade policies, tariffs, and trade agreements can impact the cost and availability of automotive components. Changes in trade policies may disrupt supply chains, affect pricing, and influence market competition.

Automotive Passive Electronic Components Market Trends

Capacitors to Witness Significant Growth

- Advancements in capacitor technology have led to the development of smaller, lighter, and more efficient capacitors. This enables automotive manufacturers to design compact and lightweight electronic systems, reducing overall vehicle weight and improving fuel efficiency. The increasing adoption of ADAS (advanced driver assistance systems), infotainment systems, and automobile connectivity features require robust and reliable electronic components. Capacitors support implementing these features by providing a stable power supply and ensuring the smooth operation of sensors, cameras, and communication modules.

- For instance, in August 2023, TDK Corporation in India (Nasik) was set for business prospects as it has enhanced its capacity. This specific facility in Nashik is growing its production capabilities and has introduced a new structure spanning approximately 23,000 square meters. In the coming four years, more production lines will be established for DC capacitors used in automotive sectors. These capacitors will be manufactured for the local market in India and overseas export. The increase in capacity creates new prospects that will support the company's medium-term growth strategy.

- Stringent government regulations and fuel economy standards drive the demand for energy-efficient automotive systems. Capacitors help optimize energy usage and minimize power losses, aligning with regulator requirements and sustainability goals. Capacitors are integral to the functioning of automotive electronic systems, and the demand is expected to continue growing as vehicle electrification, connectivity, and automation trends accelerate.

- For instance, in May 2024, Hyundai Motor Co. planned to utilize the investment already set aside for the United States to manufacture hybrid vehicles at its EV plant. The third-largest automaker globally, along with affiliate Kia Corp, intends to use funds allocated for EV and battery manufacturing facilities in Georgia to produce hybrid cars. Hyundai Motor Group of South Korea, which includes Hyundai Motor and Kia, announced plans to invest USD 12.6 billion in building new electric vehicle and battery production plants in Georgia, marking its most significant investment outside of South Korea.

Europe to Hold Significant Market Share

- Europe is home to some of the world's largest automotive markets, including the United Kingdom, Germany, and France. Europe accounts for a significant portion of worldwide vehicle production and sales. The rising demand for commercial and passenger vehicles in these countries contributes to the market for passive electronic components used in various automotive systems.

- Europe is experiencing rapid growth in the adoption of electric vehicles (EVs), battery electric vehicles (BEVs), and hybrid electric vehicles (HEVs). European government incentives and technological advancements are driving the shift toward electrified powertrains. This transition increases the demand for passive electronic components such as capacitors, inductors, and resistors used in electric drivetrains, battery management systems, and onboard electronics. For instance, in 2023, electric cars, including both BEV and PHEV, accounted for approximately 4.8& of passenger cars in Germany, as reported by KBA. The proportion of electric vehicles has steadily risen each year within the specified time frame, particularly for BEV models.

- The automotive industry in European countries like the United Kingdom, Germany, and France is at the forefront of innovation, strongly focusing on developing advanced vehicle technologies. This includes the integration of smart features, connectivity solutions, and ADAS. These technologies require various passive electronic components to support functions such as vehicle networking.

- For instance, in November 2023, the United Kingdom government allocated EUR 150 million (USD 189 million) as part of a larger EUR 4.5 billion (USD 5.7 million) investment to support British manufacturing and stimulate economic expansion. This funding is aimed at the connected and automated mobility (CAM) sector up to 2030. The budget allocated to help CAM will be supplemented by industry contributions, which will allow the United Kingdom's Centre for Connected and Autonomous Vehicles (CCAV) to solidify the UK's position as a global leader in the creation, advancement, implementation, and production of self-driving technologies, products, and services.

Automotive Passive Electronic Components Industry Overview

The automotive passive electronic components market is very competitive. The market is highly concentrated due to various small and large players. All the major players account for a significant market share and focus on expanding the global consumer base. Some significant players in the market are Yageo Corporation, Panasonic Corporation, TDK Corporation, Vishay Intertechnology Inc., Taiyo Yuden Corporation, and many more. Companies are increasing their market share by forming multiple collaborations, partnerships, and acquisitions and investing in introducing new products to earn a competitive edge during the forecast period.

March 2024: JF Kilfoil Company expanded its representation of Knowles' products to include the Cornell Dubilier brand in the Midwest market. This partnership was established due to Knowles' acquisition of Cornell Dubilier, which allowed the company to offer a broader range of film, electrolytic, and specialty capacitors. The product range comprises single-layer capacitors, trimmers, aluminum electrolytic capacitors, aluminum polymer capacitors, film capacitors, mica capacitors, and supercapacitors. These items are known for their reliability, longevity, and excellent performance in challenging situations.

September 2023: Knowles Precision Devices acquired Cornell Dubilier for USD 263 million in cash. This acquisition will include film, electrolytic, and mica capacitor products and is anticipated to enhance non-GAAP EPS by 2024. Cornell Dubilier's diverse range of power film, electrolytic, and mica capacitors, combined with Knowles' Precision Devices segment, will offer a valuable proposition and expanded product portfolio to current and potential customers.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyers/Consumers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Technology Snapshot

- 4.4 Impact of COVID-19 Aftereffects and Other Macroeconomic Factors on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Usage of Advanced Electronic Devices in the Industry

- 5.1.2 Increasing Preference for Miniaturized Designs

- 5.2 Market Restraints

- 5.2.1 Fluctuating Prices of Critical Metals Used in Manufacturing of Passive Electronic Components/ Challenges in the manufacturing of various Passive Components

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Capacitors

- 6.1.1.1 Ceramic Capacitors

- 6.1.1.2 Tantalum Capacitors

- 6.1.1.3 Aluminum Electrolytic Capacitors

- 6.1.1.4 Paper and Plastic Film Capacitors

- 6.1.1.5 Supercapacitors

- 6.1.2 Inductors

- 6.1.3 Resistors

- 6.1.3.1 Surface-mounted Chips

- 6.1.3.2 Network and Array

- 6.1.3.3 Other Specialty

- 6.1.4 EMC Filters

- 6.1.1 Capacitors

- 6.2 By Geography***

- 6.2.1 North America

- 6.2.2 Europe

- 6.2.3 Asia

- 6.2.4 Australia and New Zealand

- 6.2.5 Middle East and Africa

- 6.2.6 Latin America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles*

- 7.1.1 Yageo Corporation

- 7.1.2 Panasonic Corporation

- 7.1.3 TDK Corporation

- 7.1.4 Vishay Intertechnology Inc.

- 7.1.5 Taiyo Yuden Corporation

- 7.1.6 Kyocera Corporation (includes AVX Corporation)

- 7.1.7 Knowles Precision Devices

- 7.1.8 Murata Manufacturing Co. Ltd

- 7.1.9 Samsung Electro-Mechanical

- 7.1.10 KOA Corporation

- 7.1.11 Rubycon Corporation

- 7.1.12 Nippon Chemi-Con Corporation

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

被动电子元件市场规模、份额、趋势及预测(按类型、最终用途产业及地区划分),2026-2034年

被动电子元件市场规模、份额、趋势及预测(按类型、最终用途产业及地区划分),2026-2034年 被动式和互连式电子元件市场-全球产业规模、份额、趋势、机会、预测:按类型、应用、地区和竞争格局划分,2021-2031年

被动式和互连式电子元件市场-全球产业规模、份额、趋势、机会、预测:按类型、应用、地区和竞争格局划分,2021-2031年 欧洲航太与国防领域被动电子元件:市场份额分析、产业趋势、统计数据和成长预测(2026-2031 年)

欧洲航太与国防领域被动电子元件:市场份额分析、产业趋势、统计数据和成长预测(2026-2031 年) 被动电子元件市场-2025-2030年预测

被动电子元件市场-2025-2030年预测 全球汽车无源电子元件市场全球被动电子元件市场

全球汽车无源电子元件市场全球被动电子元件市场 被动电子元件:全球市场的展望 (2025-2030年)无源电子元件市场:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)

被动电子元件:全球市场的展望 (2025-2030年)无源电子元件市场:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年) 被动及互连电子元件市场机会、成长动力、产业趋势分析及 2025-2034 年预测

被动及互连电子元件市场机会、成长动力、产业趋势分析及 2025-2034 年预测 被动和互连电子元件市场,按元件、应用、国家和地区 - 2024-2032 年行业分析、市场规模、市场份额和预测

被动和互连电子元件市场,按元件、应用、国家和地区 - 2024-2032 年行业分析、市场规模、市场份额和预测