|

市场调查报告书

商品编码

1683433

无源电子元件市场:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)Passive Electronic Components - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

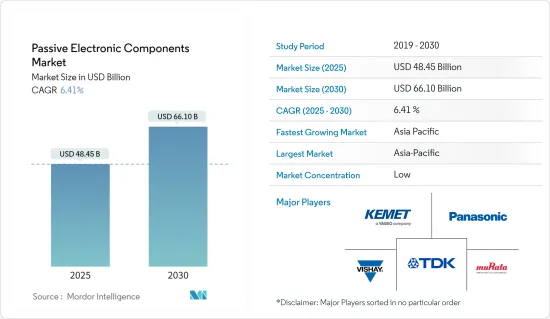

预计 2025 年被动电子元件市场规模为 484.5 亿美元,到 2030 年将达到 661 亿美元,预测期内(2025-2030 年)的复合年增长率为 6.41%。

被动电子元件是所有电子元件的基础,以物理设计和电路建模的语言来描述复杂系统的电气行为。积体电路包含这些元件,而电路基板包含分离式被动元件。电子设备需求的不断增长预计将推动被动电子元件市场的成长。

关键亮点

- 由于产品发布的增加、家用电子电器领域的发展、汽车电子中电感器的使用增加以及智慧电网的采用,电感器的成长目前保持强劲。在全球范围内,平板电脑、智慧型手机、笔记型电脑、机上盒和掌上游戏机等家用电子电器的需求不断增长是推动电感器需求的主要因素。

- 随着技术的进步,电子设备和装置变得越来越复杂,这主要是由于消费者对更小或更薄的设备的需求不断增加。现在,消费者对这些装置有一定的标准,例如时尚、纤薄的设计以及无边框萤幕。

- 此外,由于成本低、体积小、重量轻,MEMS 陀螺仪在智慧型手机中取得了巨大的成功。过去几年中,语音智慧型设备等功能的普及率也不断提高。预计到 2023年终,Amazon Echo、Google Home 和 Sonos 等智慧型装置的普及率将大幅提升。年轻一代将这些设备视为执行日常活动的更聪明、更快捷、更轻鬆的方式。

- 过去几年,穿戴式装置在医疗保健领域的应用日益受到关注,进而成为影响研究市场的关键因素之一。穿戴式连线装置的主要趋势包括用于疼痛管理的穿戴式装置的需求不断增加,以及在心血管疾病管理中穿戴式装置的使用不断增加。

- 镍对工业国家至关重要,因为它是钢铁工业中必不可少的元素。印尼是最大的矿产和镍出口国,由于对中国的供应受到限制,该国已禁止镍出口,希望提高镍价。

- 新冠肺炎疫情对全球产业供应链造成严重破坏。为了防止病毒传播,全球许多企业已暂停或缩减营运。疫情影响了被动电子元件市场,导致整个供应链的原料和元件生产层面的营运水准下降。这导致各个地区和国家的销售额下降。

- 疫情过后,家用电子电器产业需求增加预计将推动无源电子元件市场的需求。例如,根据产业机构印度蜂窝和电子协会 (ICEA) 的数据,2022 年 4 月至 2023 年 2 月期间,智慧型手机出口额比前一年翻了一番,徘徊在 45 亿美元左右。此外,由于製造商加大了产量和外部出货量,印度的行动电话出口(主要受苹果和三星的推动)在 2023 年前两个月突破了 20 亿美元,自 2022 年 4 月以来的整体出口额超过 90 亿美元。

被动电子元件市场趋势

电感器领域、消费性电子和计算行业预计将占据主要市场占有率

- 电感器在电路中扮演调节电压、滤除杂讯、控制电流等重要角色。由于它们高度依赖直流电,因此广泛应用于家用电子电器。在各种消费性产品中的开关电源设备中,电感器用作能源储存元件来产生直流电。家用电子电器领域的扩张和产业投资的增加预计将推动市场需求。

- 电感器在家用电子电器领域最为重要,因为它们有多种用途。它用于电源管理、讯号滤波和电磁干扰抑制。电感器在电视、数位机上盒、智慧型手錶、印表机、音响设备等家用电子电器中发挥重要作用。其主要作用是确保电源稳定、消除杂讯、实现可靠的讯号传输。精心挑选和设计电感器可优化家用电子电器产品的效能,最终改善整体使用者体验。将电感器加入这些设备可提高效率、稳定性和可靠性。

- 近年来,许多技术进步导致家用电子电器的使用量激增。各种技术改进的结合正在吸引客户,从而导致电感器的需求增加。家用电子电器中触控萤幕和其他先进功能的引入进一步增加了产业对电感器的需求。随着家用电子电器领域产品的不断推出,对电感器的需求也增加。

- 智慧型手机已经成为使用电感器不可或缺的部件。高频电感一般应用在行动电话中,已经成为我们日常生活中不可或缺的元件。内建高频电感,让网路浏览速度更快、更稳定,让您随时随地了解最新社会动态,提升通话质量,提升整体行动电话用户体验。

- 由于智慧型手机技术对消费者需求的依赖性很强,因此其成长速度比其他技术更快。随着每代行动通讯网路的发展,行动电话中电感的数量都大大增加。随着智慧型手机的不断发展和普及,特别是在开发中国家,其扩展管道将进一步扩大。 5G智慧型手机的普及以及5G行动电话製造投资的不断增长预计将增加对电感器的需求。

- 根据爱立信的最新报告,全球智慧型手机行动网路用户数量预计将在2022年达到近64亿,到2028年将超过77亿人。值得注意的是,中国、印度和美国在智慧型手机和行动网路用户数量方面处于领先地位。儘管预计 2022 年销量将趋于平稳,但智慧型手机的平均售价正在上涨,预计将在未来几年推动市场发展。

亚太地区电感器市场预计将显着成长

- 日本、中国、韩国和台湾等许多国家和地区都拥有大型无源电子巨头和代工厂。受智慧家用电子电器、创新高阶产品和新型智慧型手机的推动,亚太消费电子市场预计将持续成长。因此,受该地区销售额成长的推动,电感器的需求预计会增加。

- 工业和资讯化部表示,中国在创新和品牌建立方面表现出色,巩固了其在家用电子电器产品生产和销售领域的全球领先地位。随着该地区不断增加的投资以提高生产能力,消费性电子市场有望实现成长。

- 印度电子与资讯技术部(MeitY)预测,到2026年,该国电子製造业的价值将达到3,000亿美元,其中行动电话销售将引领市场。据 ICEA 称,2022 年行动电话销售额预计将达到 400 亿美元,预计到 2026 年将成长到 800 亿美元。这些政府旨在提高该地区行动电话製造能力的措施预计将带来对电感器的需求。

- 根据GSMA的报告,印度可望成为亚太地区领先的国家,到2030年智慧型手机连线数将达到13亿。该地区拥有成长最快的5G市场,爱立信预测,到2028年,5G将占印度行动用户的57%,总合用户数将达到6.998亿。因此,预计市场将受到行动电话需求、网路广泛普及和创新影像技术的推动。

- 爱立信预测,到2028年终,东南亚和大洋洲的5G用户数将达到约6.2亿,这意味着5G将超越其他技术,成为用户的压倒性选择,渗透率将达到48%。此外,预计到 2022 年该地区的 5G 用户数将接近 3,000 万。 5G倡议的不断增加预计将增加市场机会。

无源电子元件市场概况

无源电子元件市场主要分为台达电子股份有限公司、松下电器产业株式会社、TDK 株式会社、Vishay Intertechnology Inc. 和村田製作所等主要企业。该市场的参与企业正在采用合作和收购等策略来增强其产品供应并获得可持续的竞争优势。

- 2023 年 10 月,TDK 公司宣布推出 PLEA85,这是专为电池供电的穿戴式装置和其他装置开发的一系列高效能功率电感器,可延长运作时间。新系列采用TDK新开发的低损耗磁性材料和薄膜加工技术,实现了业界最薄的尺寸。

- 2023 年 10 月,Vishay Intertechnology Inc. 推出了一系列采用密封玻璃金属密封的湿钽电容器。对于航空电子和航太,STH电解电容器具有 Vishay SuperTan 扩展系列元件的所有优点,同时采用高可靠性设计,提高了军用 H 级衝击和振动能力,并将热衝击能力提高到 300 次循环。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

- 产业价值链分析

- 新冠肺炎疫情及其他宏观经济因素对市场的影响

- 2022 年钯和钌的需求和供应情况以及 2023 年预测

第五章 市场动态

- 市场驱动因素

- 电子产品日益复杂

- 设计越来越趋向小型化

- 市场问题

- 金属价格上涨影响零件製造成本

第六章 市场细分

- 电容器

- 按类型

- 陶瓷电容器

- 钽电容器

- 电解电容器

- 纸/塑胶薄膜电容器

- 超级电容

- 按最终用户产业

- 车

- 工业的

- 航太和国防

- 活力

- 通讯/伺服器/资料存储

- 消费性电子产品

- 医疗

- 按地区

- 美洲

- 欧洲、中东和非洲

- 亚太地区(日本和韩国除外)

- 日本和韩国

- 按类型

- 电感器

- 按类型

- 力量

- 按频率

- 按最终用户产业

- 车

- 航太和国防

- 通讯

- 家用电子电器与计算机

- 其他的

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 其他的

- 按类型

- 电阻器

- 按类型

- 表面黏着技术晶片

- 网路

- 绕线

- 薄膜/氧化膜/箔

- 碳

- 按最终用户产业

- 车

- 航太和国防

- 通讯

- 家用电子电器与计算机

- 其他的

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 其他的

- 按类型

第七章 竞争格局

- 公司简介

- Delta Electronics Inc.

- Panasonic Corporation

- TDK Corporation

- Vishay Intertechnology Inc.

- Murata Manufacturing Co. Ltd

- AVX Corporation(Kyocera Corporation)

- Taiyo Yuden Co. Ltd

- Sagami Elec Co. Ltd

- WIMA GmbH & Co. KG

- Cornell Dubilier Electronics Inc.

- Yageo Corporation

- Lelon Electronics Corp.

- United Chemi-Con(Nippon Chemi-con Corporation)

- Bourns Inc.

- Wurth Elektronik Group

- API Delevan(Fortive Corporation)

- Eaton Corporation

- Coilcraft Inc.

- TT Electronics PLC

- KOA Speer Electronics Inc.

- TE Connectivity Ltd

- Ohmite Manufacturing Company

- Susumu Co. Ltd

- Viking Tech Corporation

- Honeywell International Inc.

第八章 中国厂商名单

第九章投资分析

第 10 章:投资分析市场的未来

The Passive Electronic Components Market size is estimated at USD 48.45 billion in 2025, and is expected to reach USD 66.10 billion by 2030, at a CAGR of 6.41% during the forecast period (2025-2030).

Passive electronic components are the cornerstone of all electronics, in physical design and circuit models' language, representing electrical behavior in complicated systems. Integrated circuits include these components, and circuit boards contain discrete passive components. The increasing demand for electronic devices is anticipated to boost the passive electronic components market's growth.

Key Highlights

- The growth of inductors is presently steady, owing to the increasing number of product launches, the developments in the consumer electronics sector, the rising use of inductors in automotive electronics, and the adoption of smart grids. Globally, the rising demand for consumer electronics, such as tablets, smartphones, laptops, set-top boxes, and portable gaming consoles, is the major factor boosting the need for inductors.

- With the advent of technological advancements, electronics, and electronic devices are getting more complex, primarily due to the increasing consumer demand for small or slim devices. Customers have a specific standard for these devices nowadays, such as a sleek, thin design, with the screen going from edge to edge.

- Moreover, smartphones have witnessed the great success of MEMS gyroscopes owing to their low cost, miniature size, and lightweight nature. Features like voice-enabled smart devices have also been witnessing increased adoption over the past few years. The adoption of smart devices, such as the Amazon Echo, Google Home, and Sonos, was estimated to be aggressive by the end of 2023. The younger generation views these devices as the smarter, faster, and easier way to perform everyday activities.

- The adoption of wearables in the healthcare sector has been gaining traction in recent times, which, in turn, has been one of the significant factors influencing the market studied. The major trends in wearable connected devices include the increasing demand for pain management wearable devices and the increasing use of wearables for cardiovascular disease management.

- As nickel is an essential element for steel industries and, therefore, crucial to industrial countries, in recent times, the price of the element has been most affected by continuing lockdowns in some parts of the world, coupled with supply-side restraints. Indonesia, the largest miner and nickel exporter, banned metal exports in the hopes of a price rise in the wake of limited supplies to China.

- The COVID-19 pandemic led to immense disruptions in supply chains across industries globally. Many businesses globally halted or reduced operations to help combat the spread of the virus. The pandemic impacted the passive electronic components market, leading to decreased operation levels across the supply chain on the raw material and component production levels. This denoted a fall in sales in a range of regions and countries.

- The demand from consumer electronics industries has increased post-pandemic and is anticipated to boost the demand in the passive electronic components market. For instance, according to the industry body India Cellular and Electronics Association (ICEA), smartphone exports in the April 2022-February 2023 years doubled from a year ago when exports hovered around USD 4.5 billion. In addition, India's mobile phone exports crossed USD 2 billion in the first two months of 2023, driven mainly by Apple and Samsung, taking the entire export value to over USD 9 billion since April 2022, as manufacturers stepped up production and external shipments.

Passive Electronic Components Market Trends

The Consumer Electronics and Computing Industry in the Inductors Segment is Expected to Hold a Significant Market Share

- Inductors have a significant function in the regulation of voltage, noise filtration, and current control within electrical circuits. Their usage is widespread in consumer electronics due to their strong reliance on DC power. In switched-mode power devices in various consumer products, inductors serve as energy storage components to generate DC current. The market is anticipated to experience increased demand due to the expanding consumer electronics sector and growing investments in the industry.

- Inductors are of utmost importance in the consumer electronics sector as they serve multiple purposes. They are utilized for power management, signal filtering, and suppressing electromagnetic interference. In consumer electronic devices like televisions, digital set-top boxes, smartwatches, printers, and audio equipment, inductors act as crucial components. Their primary function is to ensure a steady power supply and eliminate noise, thereby ensuring reliable signal transmission. By carefully selecting and designing inductors, the performance of consumer electronics is optimized, ultimately enhancing the overall user experience. The incorporation of inductors in these devices leads to improved efficiency, stability, and reliability.

- Due to numerous technological advancements, there has been a significant surge in the utilization of consumer electronic devices in recent years. The incorporation of various technological enhancements has captivated customers, leading to a higher demand for inductors. The introduction of touch screens and other advanced functionalities in consumer electronics has further fueled the need for inductors within the industry. With the increasing number of product launches in the consumer electronics sector, there is a growing demand for inductors in the industry.

- Smartphones have become integral components for the utilization of inductors. Typically, high-frequency inductors find their application in mobile phones, which have now become indispensable in day-to-day lives. The incorporation of high-frequency inductors enables faster and more stable internet browsing, facilitates staying updated with the latest social events at any time and place, enhances call quality, and elevates the overall mobile phone user experience.

- Smartphone technology is experiencing rapid growth in comparison to other technologies due to its strong reliance on consumer demand. The quantity of inductors in mobile phones experiences a substantial rise with every successive generation of the mobile communication network. As smartphones continue to evolve and their adoption rate expands, particularly in developing nations, additional avenues for expansion arise. The surge in 5G smartphones and the escalating investments in the manufacturing of 5G mobile phones are projected to amplify the need for inductors.

- Ericsson's most recent report disclosed that the global count of smartphone mobile network subscriptions nearly reached 6.4 billion in 2022, and it is projected to surpass 7.7 billion by 2028. It is noteworthy that China, India, and the United States are at the forefront, boasting the highest number of smartphone mobile network subscriptions. Although sales plateaued in 2022, the rising average selling price of smartphones is anticipated to propel the market in the forthcoming years.

Asia-Pacific is Expected to Witness Significant Growth in the Inductors Segment

- The demand for inductors is primarily felt in Asia-Pacific, with many countries, like Japan, China, South Korea, and Taiwan, hosting massive companies and foundries for several major passive electronic powerhouses. The consumer electronics market in Asia-Pacific is expected to witness consistent growth, driven by the popularity of smart appliances, innovative high-end products, and new smartphones. As a result, the demand for inductors is also expected to increase, fueled by the expanding sales in the region.

- China, in particular, has excelled in innovation and brand building, securing its position as the global leader in the production and sales of consumer electronics, as stated by the Ministry of Industry and Information Technology. With increasing investments in the region to enhance production capabilities, the consumer electronics market is poised for growth.

- The Ministry of Electronics and Information Technology (MeitY) in India has forecasted that the electronics manufacturing sector in the country will achieve a worth of USD 300 billion by 2026, with mobile phone sales taking the lead in the market. As per ICEA, mobile phone sales were estimated at USD 40 billion in 2022 and are anticipated to rise to USD 80 billion by 2026. These governmental efforts to enhance the mobile phone production capabilities in the region are expected to consequently generate demand for inductors.

- As per the GSMA report, India is anticipated to emerge as the leading country in Asia-Pacific by 2030, with 1.3 billion smartphone connections. The region boasts some of the most rapidly expanding 5G markets, and by 2028, Ericsson predicts that 5G will constitute 57% of mobile subscriptions in India, totaling 699.8 million subscriptions. Consequently, the market is anticipated to be propelled by the demand for mobile phones, facilitated by extensive internet penetration and innovative imaging technology.

- Ericsson predicts that by the end of 2028, the number of 5G subscriptions in Southeast Asia and Oceania will reach approximately 620 million. This indicates that 5G will surpass other technologies and become the dominant choice for subscribers, with a penetration rate of 48%. Furthermore, it is projected that the region will have nearly 30 million 5G subscriptions by 2022. Such increasing 5G deployment initiatives are expected to enhance the market opportunities.

Passive Electronic Components Market Overview

The passive electronic components market is fragmented with the presence of major players like Delta Electronics Inc., Panasonic Corporation, TDK Corporation, Vishay Intertechnology Inc., and Murata Manufacturing Co. Ltd. Players in the market are adopting strategies such as partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

- In October 2023, TDK Corporation announced the launch of its new PLEA85 series of high-efficiency power inductors developed for battery-powered wearables and other devices, improving operating times. The new series has the lowest profile in the industry, owing to the use of TDK's newly developed low-loss magnetic material and its thin-film processing techniques.

- In October 2023, Vishay Intertechnology Inc. launched a new series of wet tantalum capacitors with hermetic glass-to-metal seals. For avionics and aerospace applications, the STH electrolytic capacitors provide all the advantages of Vishay's SuperTan extended series devices while offering a higher reliability design for improved military H-level shock and vibration capabilities and increased thermal shock up to 300 cycles.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Degree of Competition

- 4.3 Industry Value Chain Analysis

- 4.4 Impact of COVID-19 and Other Macroeconomic Factors on the Market

- 4.5 Demand and Supply of Palladium and Ruthenium Till 2022 and Forecast for 2023

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Complexity of Electronics

- 5.1.2 Increasing Miniaturized Design Preferences

- 5.2 Market Challenges

- 5.2.1 Rising Metal Prices Impacting Component Production Costs

6 MARKET SEGMENTATION

- 6.1 Capacitors

- 6.1.1 By Type

- 6.1.1.1 Ceramic Capacitors

- 6.1.1.2 Tantalum Capacitors

- 6.1.1.3 Aluminum Electrolytic Capacitors

- 6.1.1.4 Paper and Plastic Film Capacitors

- 6.1.1.5 Supercapacitors

- 6.1.2 By End-user Industry

- 6.1.2.1 Automotive

- 6.1.2.2 Industrial

- 6.1.2.3 Aerospace and Defense

- 6.1.2.4 Energy

- 6.1.2.5 Communications/Servers/Data Storage

- 6.1.2.6 Consumer Electronics

- 6.1.2.7 Medical

- 6.1.3 By Geography

- 6.1.3.1 Americas

- 6.1.3.2 Europe, Middle East and Africa

- 6.1.3.3 Asia-Pacific (Excl. Japan and Korea)

- 6.1.3.4 Japan and South Korea

- 6.1.1 By Type

- 6.2 Inductors

- 6.2.1 By Type

- 6.2.1.1 Power

- 6.2.1.2 Frequency

- 6.2.2 By End-user Industry

- 6.2.2.1 Automotive

- 6.2.2.2 Aerospace and Defense

- 6.2.2.3 Communications

- 6.2.2.4 Consumer Electronics and Computing

- 6.2.2.5 Other End-user Industries

- 6.2.3 By Geography

- 6.2.3.1 North America

- 6.2.3.2 Europe

- 6.2.3.3 Asia-Pacific

- 6.2.3.4 Rest of the World

- 6.2.1 By Type

- 6.3 Resistors

- 6.3.1 By Type

- 6.3.1.1 Surface-mounted Chips

- 6.3.1.2 Network

- 6.3.1.3 Wirewound

- 6.3.1.4 Film/Oxide/Foil

- 6.3.1.5 Carbon

- 6.3.2 By End-user Industry

- 6.3.2.1 Automotive

- 6.3.2.2 Aerospace and Defense

- 6.3.2.3 Communications

- 6.3.2.4 Consumer Electronics and Computing

- 6.3.2.5 Other End-user Industries

- 6.3.3 By Geography

- 6.3.3.1 North America

- 6.3.3.2 Europe

- 6.3.3.3 Asia-Pacific

- 6.3.3.4 Rest of the World

- 6.3.1 By Type

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Delta Electronics Inc.

- 7.1.2 Panasonic Corporation

- 7.1.3 TDK Corporation

- 7.1.4 Vishay Intertechnology Inc.

- 7.1.5 Murata Manufacturing Co. Ltd

- 7.1.6 AVX Corporation (Kyocera Corporation)

- 7.1.7 Taiyo Yuden Co. Ltd

- 7.1.8 Sagami Elec Co. Ltd

- 7.1.9 WIMA GmbH & Co. KG

- 7.1.10 Cornell Dubilier Electronics Inc.

- 7.1.11 Yageo Corporation

- 7.1.12 Lelon Electronics Corp.

- 7.1.13 United Chemi-Con (Nippon Chemi-con Corporation)

- 7.1.14 Bourns Inc.

- 7.1.15 Wurth Elektronik Group

- 7.1.16 API Delevan (Fortive Corporation)

- 7.1.17 Eaton Corporation

- 7.1.18 Coilcraft Inc.

- 7.1.19 TT Electronics PLC

- 7.1.20 KOA Speer Electronics Inc.

- 7.1.21 TE Connectivity Ltd

- 7.1.22 Ohmite Manufacturing Company

- 7.1.23 Susumu Co. Ltd

- 7.1.24 Viking Tech Corporation

- 7.1.25 Honeywell International Inc.

8 LIST OF CHINESE MANUFACTURERS

9 INVESTMENT ANALYSIS

10 FUTURE OF THE MARKET

2026年全球电阻垫市场报告

2026年全球电阻垫市场报告 被动和互连电子元件市场:2026-2032年全球市场预测(按元件类别、安装方式、介质材料、频宽、应用领域、终端用户产业和分销管道划分)

被动和互连电子元件市场:2026-2032年全球市场预测(按元件类别、安装方式、介质材料、频宽、应用领域、终端用户产业和分销管道划分) 全球被动电子元件市场:市场展望(2026-2031年)

全球被动电子元件市场:市场展望(2026-2031年) 被动电子元件市场规模、份额、趋势及预测(按类型、最终用途产业及地区划分),2026-2034年

被动电子元件市场规模、份额、趋势及预测(按类型、最终用途产业及地区划分),2026-2034年 被动式和互连式电子元件市场-全球产业规模、份额、趋势、机会、预测:按类型、应用、地区和竞争格局划分,2021-2031年

被动式和互连式电子元件市场-全球产业规模、份额、趋势、机会、预测:按类型、应用、地区和竞争格局划分,2021-2031年 欧洲航太与国防领域被动电子元件:市场份额分析、产业趋势、统计数据和成长预测(2026-2031 年)

欧洲航太与国防领域被动电子元件:市场份额分析、产业趋势、统计数据和成长预测(2026-2031 年) 被动电子元件市场-2025-2030年预测

被动电子元件市场-2025-2030年预测 全球汽车无源电子元件市场全球被动电子元件市场

全球汽车无源电子元件市场全球被动电子元件市场 被动及互连电子元件市场机会、成长动力、产业趋势分析及 2025-2034 年预测

被动及互连电子元件市场机会、成长动力、产业趋势分析及 2025-2034 年预测