|

市场调查报告书

商品编码

1689977

广播设备:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Broadcast Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

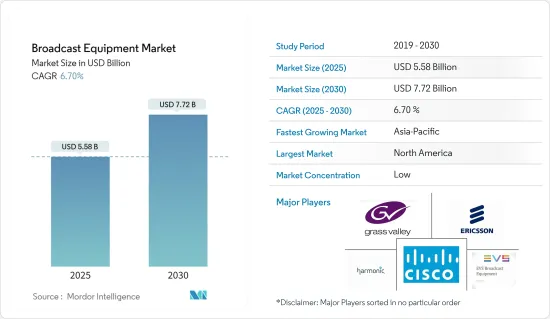

广播设备市场规模预计在 2025 年为 55.8 亿美元,预计到 2030 年将达到 77.2 亿美元,预测期内(2025-2030 年)的复合年增长率为 6.7%。

透过电子大众传播向特定受众传递音讯和影像内容称为广播。这是为了向尽可能多的人传播讯息。广播通常仅限于本地/点网路系统。广播服务仍然很受欢迎,并为广大观众提供最直接、最可靠的资讯来源。由于智慧电子设备的使用日益增多以及对 3D 和高清内容的需求不断增长,广播设备市场正在扩大。

关键亮点

- 过去几十年来,消费者对更高品质音讯和视讯的需求推动了广播设备产品和技术的快速升级。由于现在内容都是以 4K 和 UHD 格式製作的,以相同格式进行广播以提高观看品质导致了 IP 直播製作技术的出现。这对于现场製作至关重要,因为灵活且高效的系统控制是关键。

- 例如,2023 年 11 月,ArcGIS Motion Imagery 团队宣布发布新的 ArcGIS Video Server。 ArcGIS Enterprise 的这个新伺服器角色旨在扩展 ArcGIS 的影片功能。最新的 ArcGIS 视讯伺服器可以将影片作为具有地理空间和时间背景的服务进行索引、发布、搜寻和串流。

- 技术进步鼓励广播公司提供高阶用户超高清输出,刺激市场成长。此外,数位频道的兴起以及以 8K 品质直播体育赛事和 4K 品质直播新闻为特色的尖端广播设备的使用日益增多,正在促进市场加速增长。据8K协会预测,未来8K电视将会越来越受欢迎。 2023 年 8K 电视的出货量将达到约 214 万台,高于前一年的 80 万台。到2026年,这一数字预计将达到440万台以上。

- 体育产业是全球最大的电视观众市场,并且正在寻找大规模提供视讯内容的方法。设备和格式的激增给服务供应商、内容拥有者、广播公司和版权持有者带来了许多挑战。在广播设备市场中,租赁体育广播设备部分也是主要收益来源。国际体育赛事的增加推动了广播设备租赁市场的发展。

- 此外,由于技术不断发展、高速网路基础设施投资不断增加以及透过 OTT 服务对 D2C 产品的需求不断增长,市场正迎来发展机会。根据电讯的数据,截至2023年,小岛屿开发中国家(SIDS)的67%人口将能够使用互联网,而最不开发中国家(LDC)的这一比例为35%,内陆发展中国家人口的互联网普及率为39%。全球线上查询率为67%。

- 此外,收入的增加、耐用消费品购买量的增加以及快速廉价互联网的普及预计将对市场成长产生积极影响。根据印度IBEF预测,到2024年,电视预计将占据印度媒体市场的40%,其次是数位广告(12%)、印刷媒体(13%)、电影(9%)以及OTT和游戏(8%)。到2025年,智慧电视保有量预计将达到4,000万至5,000万台。

- 数位音讯和影像格式的快速发展以及对创建和储存数位影像和视讯的开放、国家或国际认可标准的需求正在推动市场成长。随着数位技术的每一次进步,数位音讯和视讯格式以及压缩方法的规范也在不断发展。

- 新冠疫情迫使广播公司重新思考其内容製作和分发的方式,导致人员配置、技术堆迭和设施发生变化。例如,新闻广播适应了一些国家的封锁要求,世界各地的多个节目透过消费者视讯技术引入专家意见。广播技术也使得疫情期间的演出和音乐会成为可能。例如,Lady Gaga 组织了一场长达八小时的活动,100 名音乐家在她的客厅、卧室和花园里表演。

广播设备市场趋势

编码器预计将经历大幅成长

- 编码器透过将音讯和视讯讯号转换为数位格式以便透过网路传输,在广播中发挥至关重要的作用。随着对高清和串流内容的需求不断增加,广播公司需要先进的编码器来有效地提供高品质的影像。随着广播公司升级其基础设施以跟上不断变化的观众偏好和技术标准,这导致对包括编码器在内的广播设备的需求增加。

- 2024 年 4 月,Net Insights 宣布将透过升级版 Nimbra 414 增强其荣获艾美奖的网路媒体传输产品 Nimbra 400 编码器的功能,以应对更丰富、更具互动性的活动製作的成长。随着最新版本的 Nimbra 414 增加通道密度并支援 UHD 内容,Nimbra 414 编码器/解码器系列完全有能力帮助广播公司提供更具沉浸感的製作,从而提高观众的参与度。

- 对视讯进行编码的目的是创建可以透过网路传输的数位副本。广播公司可以根据串流媒体的目的和预算选择硬体或软体编码器。大多数专业广播公司使用硬体编码器,但由于价格分布较高,大多数初级到中级广播公司使用直播编码器软体。

- 例如,2024 年 4 月,美国字幕公司 Verbit 旗下的 VITAC 与广播解决方案供应商 ENCO 宣布建立策略合作伙伴关係,旨在让广播公司在硬体编码器和云端字幕之间有更多选择。此次合作将为广播公司提供根据其需求客製化的综合字幕工具和服务。

- 此外,随着串流媒体平台的普及,需要高效的编码技术来透过网路传输高品质的影像内容。例如,2023 年 9 月,北欧付费电视和串流平台 Allente 推出了其新的 Allente Stream 多萤幕 OTT 服务。因此,该营运商正在基于 3SS 3Ready 产品平台运作于 Android TV、行动电话、LG 和三星智慧型电视、Apple TV、网路和 iOS 的最新应用程式。

- 此外,由于内容分布在各种平台和装置上,广播公司需要支援适合传输速率串流并与各种转码器和通讯协定相容的编码器。此外,实况活动、体育赛事和新闻报导的流行也使得人们需要能够有效编码和即时传输即时视讯串流的编码器。

- 据Meltwater称,近年来,直播视讯内容已成为线上娱乐和业务中最常见的视讯内容类型之一。 2023 年第三季度,直播覆盖了全球约 28% 的网路用户。此外,2023 年,Netflix 透露其在美国和加拿大拥有 8,013 万付费串流媒体用户。

- 编码器的效率已显着提高,并在 HDTV 等现代格式和 H.264 等压缩标准的成功中发挥关键作用。如今,广播环境中对编码器的需求可分为三个主要领域:贡献、主要分发和家庭分发。

预计亚太地区将出现显着成长

- 亚太地区有中国、印度等人口大国。亚太国家都市化数位化的提高意味着更多的人可以接触到电视和数位媒体内容,这推动了对广播设备的需求。根据 Meltwater 预测,到 2023 年第三季度,菲律宾约有 96% 的 16-64 岁网路用户将每月订阅 Netflix 等订阅视讯点播 (SVOD) 服务。

- 此外,该地区 OTT(Over-The-Top)串流平台的日益普及也推动了对先进广播设备的需求,以支援高品质的串流媒体服务。例如,2024 年 5 月,Prasar Bharati 宣布计划于 8 月推出自己的家庭友善 OTT 平台。政府的公共广播公司将播放关注印度社会和文化的内容。最初,该平台将免费提供。这些市场的发展可能会进一步推动该地区的市场成长。

- 亚太地区是奥运、世界杯和地区性比赛等重大体育赛事的举办地点。为了确保无缝覆盖和传输,此类活动对广播设备的需求激增。同时,4K/UHD 广播、虚拟实境 (VR)、扩增实境(AR) 和身临其境型音讯等广播技术的进步正在推动该地区采用先进的广播设备。

- 根据 GSMA 的报告,不丹、伊朗、孟加拉和越南等国家行动普及率成长最为显着。该地区智慧型设备的普及也推动了对高清音讯和视讯的需求。根据GSMA统计,64%的亚太居民已经拥有智慧型手机,预计到2025年普及率将超过80%。

- 此外,Netflix 于 2023 年 3 月宣布计划在亚太地区投资约 19 亿美元用于本地内容。该公司预计 2023与前一年同期比较收益将年增 12%,超过 40 亿美元,而 2022 年的成长率为 9%。此外,根据国际电信联盟 (ITU) 的数据,到 2023 年,亚太地区 66% 的人口将上网,这将进一步推动市场成长。

- 当地供应商投入大量资金,以利用新冠疫情带来的机会。例如,去年3月,Signiant Inc.宣布收购嵌入式媒体处理软体供应商Kyno。此次收购将有助于扩展其 SaaS 平台软体定义内容交换 (SDCX) 的功能,包括与媒体资产互动的工具。该平台在全球拥有约一百万用户,连接了超过五万家各种规模的媒体和娱乐公司。

广播设备产业概况

广播设备市场中各企业之间的竞争,取决于价格、产品、市场占有率和竞争强度。主要市场参与企业包括思科系统公司、爱立信公司、Harmonic 公司、EVS 广播设备公司和 Grass Valley。

- 2024 年 4 月:全球关键任务即时视讯网路和视觉协作解决方案供应商 Haivision Systems 宣布,Haivision 和索尼公司(「Sony」)已成功使用索尼的云端製作平台 Creators' Cloud for Enterprise 测试了 Haivision 业界领先的视讯编码器、解码器和行动视讯发射器。

- 2024年2月:索尼宣布推出自己的专用可携式资料发射器PDT-FP1,该发射器可透过5G网路实现高速、低延迟的影片和静态影像资料传输。此无线通讯设备可以安装在相机上,用于新闻和事件拍摄以及广播影像製作等需要速度的场合,从拍摄影像到分发、广播、发布。在没有Wi-Fi的室外和室内环境中,5G网路提供高速、低延迟、稳定的行动资料通讯,实现高效、易于理解的工作流程。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 研究范围

第二章调查方法

- 研究框架

- 二次研究

- 初步研究

- 资料三角测量与洞察生成

第三章执行摘要

第四章 市场洞察

- 市场概览

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 价值链分析

- 主要宏观经济趋势的市场影响

第五章市场动态

- 市场驱动因素

- 由于支援多种格式,对编码器的需求不断增加

- 透过OTT服务扩展D2C服务

- SAAS 解决方案的采用率不断提高

- 市场限制

- 广播媒体格式和转码器缺乏标准化

第六章市场区隔

- 依技术

- 类比广播

- 数位广播

- 按产品

- 天线

- 转变

- 影像伺服器

- 编码器

- 发射器和中继器

- 其他的

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

第七章竞争格局

- 公司简介

- Cisco Systems Inc.

- Telefonaktiebolaget LM Ericsson

- Evs Broadcast Equipment SA

- Grass Valley

- Harmonic Inc.

- Clyde Broadcast

- Sencore Inc.

- Eletec Broadcast Telecom Sarl

- AVL Technologies Inc.

- ETL Systems Ltd

第八章投资分析

第九章:市场的未来

The Broadcast Equipment Market size is estimated at USD 5.58 billion in 2025, and is expected to reach USD 7.72 billion by 2030, at a CAGR of 6.7% during the forecast period (2025-2030).

The distribution of audio and video content to a precise audience via electronic mass communication is known as broadcasting. It is a spread of information to a large group of people. Typically, broadcasting is limited to a local spot network system. Broadcasting services, which remain popular, deliver a large audience with the most direct and reliable information mediums. The broadcast equipment market is expanding because of the increased use of smart electronic devices and improved demand for 3D and HD content.

Key Highlights

- Over the last few decades, consumers' demand for better-quality audio and video has rapidly upgraded broadcast equipment products and technology. With content being produced in 4K and UHD formats, broadcasting in the identical format for enhanced viewing quality has resulted in IP live-production technology. This is essential for live production, where a premium is placed on flexible and efficient system control.

- For instance, in November 2023, the ArcGIS Motion Imagery Team announced the release of the new ArcGIS Video Server. This new server role for ArcGIS Enterprise is designed to expand video capabilities across ArcGIS. The latest ArcGIS Video Server allows indexing, publishing, searching, and streaming video as a service with geospatial and temporal context.

- Technological advancements are driving broadcasters to provide UHD output to their premium users, fueling market growth. Moreover, the rise in digital channels and the increasing utilization of cutting-edge broadcasting devices, featuring 8K video quality for sports coverage and 4K quality for news coverage, contribute to the acceleration of market growth. According to the 8K Association, 8K TVs will become increasingly popular in the coming years. Around 2.14 million 8K TV sets were shipped in 2023, up from 800 thousand in the previous year. By 2026, this number is predicted to reach over 4.4 million units.

- The sports section is the biggest market for TV viewers worldwide, and it is finding ways to deliver video content at scale. The increasing number of devices and formats offer several challenges for service providers, content owners, broadcasters, and rights holders. The rental sports broadcast equipment sector is also a significant revenue generator in the broadcast equipment market. The increasing number of international sports tournaments is driving the rental market for broadcast equipment.

- Furthermore, the market is witnessing opportunities for evolution due to evolving technology, increased investments in high-speed internet infrastructure, and growing demand for D2C offerings via OTT services. According to the International Telecommunication Union, as of 2023, 67% of the population in small island developing states (SIDS) used the internet, compared to 35% of the population in least developed countries (LDCs), while the internet penetration rate for those living in landlocked growing counties was at 39%. The global online access rate was 67%.

- Moreover, the rising income, increasing purchases of consumer durables, and the increasing availability of fast and cheap internet are expected to impact the market's growth positively. As per IBEF, India, television is projected to constitute 40% of the Indian media market in 2024, trailed by digital advertising (12%), print media (13%), cinema (9%), and the OTT and gaming industries (8%). By 2025, it is anticipated that the number of linked intelligent televisions will reach around 40 to 50 million.

- The rapidly developing nature of digital audio and video formats and the need for open, domestic, or international agreement norms for generating and preserving digital video and audio are challenging the market's growth. Norms for digital audio and video formats and compression methods are evolving with every new advancement in digital technology.

- The COVID-19 pandemic forced broadcasters to rethink their approach to producing and delivering content - resulting in changes to staffing, technology stacks, and facilities. News broadcasting, for instance, adapted to the lockdown requirements of several nations, with several programs worldwide gathering experts' input through consumer video technology. Broadcasting technologies also enabled programs and concerts during the pandemic. For instance, Lady Gaga organized an eight-hour event involving 100 musicians playing from their living rooms, bedrooms, and gardens.

Broadcast Equipment Market Trends

Encoders are Expected to Witness Significant Growth

- Encoders play a crucial role in broadcasting by converting audio and video signals into digital format for transmission over networks. As demand for high-definition and streaming content grows, broadcasters need advanced encoders to deliver high-quality video efficiently. This drives the demand for broadcast equipment, including encoders, as broadcasters upgrade their infrastructure to meet evolving viewer preferences and technological standards.

- In April 2024, Net Insight announced a boost to the capability of its Emmy Award-winning internet media transport offering, the Nimbra 400 encoders, to meet the growth in more prosperous and more interactive events production with the upgraded Nimbra 414. The latest version of the Nimbra 414 increases channel density and support for UHD content, making the Nimbra 414 encoder/decoder family now ideally placed to help broadcasters deliver more immersive productions that enhance viewer engagement.

- The purpose of encoding a video is to create a digital copy transmitted over the internet. Broadcasters can choose between a hardware or software encoder, depending on the purpose of the stream and the budget. Most professional broadcasters use hardware encoders, but due to the high price point, most beginner-level to mid-experienced broadcasters go with live streaming encoder software.

- For instance, in April 2024, VITAC, a Verbit Company, a US-based captioning company, and ENCO, a provider of broadcasting solutions, announced a strategic partnership aimed at providing broadcasters with expanded choice for hardware encoders and cloud captioning. Through this alliance, broadcasters will access a comprehensive suite of captioning tools and services tailored to meet their specific requirements.

- Furthermore, the increasing popularity of streaming platforms necessitates efficient encoding technologies to deliver high-quality video content over the internet. For instance, in September 2023, Nordic PayTV and streaming platform Allente launched its new Allente Stream multiscreen OTT offering. As a result, the operator has gone live with the latest apps for Android TV and mobiles, LG and Samsung Smart TVs, Apple TV, web, and iOS, based on the 3SS 3Ready product platform.

- Moreover, with content being distributed across different platforms and devices, broadcasters need encoders that support adaptive bitrate streaming and compatibility with different codecs and protocols. Further, the popularity of live events, sports, and news coverage needs encoders that can efficiently encode and transmit live video streams in real time.

- According to Meltwater, in recent years, live-streaming video content has become one of the most popular types of video content consumed online for entertainment and operational purposes. During the third quarter of 2023, live streaming registered an audience reach of almost 28% among internet users worldwide. In addition, in 2023, Netflix revealed that it had 80.13 million paying streaming subscribers in the United States and Canada.

- The effectiveness of encoders has significantly improved, and they play a significant role in the success of modern formats, like HDTV, and compression standards, like H.264. Currently, the demand for encoders in broadcast settings can be categorized into three key domains: contribution, primary distribution, and home distribution.

Asia-Pacific is Expected to Witness Significant Growth Rate

- Asia-Pacific is home to some densely populated countries such as China and India. Increasing urbanization and digitization across Asia-Pacific countries fuel the demand for broadcast equipment as more people access television and digital media content. According to Meltwater, in the third quarter of 2023, about 96% of internet users aged between 16 and 64 years in the Philippines used a subscription video-on-demand (SVOD) service, such as Netflix, each month.

- Further, over-the-top (OTT) streaming platforms are gaining popularity in the region, creating a need for advanced broadcast equipment to support high-quality streaming services. For instance, in May 2024, Prasar Bharati has announced its plans to start its own OTT platform for families in August. The government's public service broadcaster will stream content that will be focused on Indian society and culture. Initially, the platform will be available for free to the public. Such developments may further propel the market's growth in the region.

- Asia-Pacific is home to major sporting events like the Olympics, FIFA World Cup, and regional tournaments. The demand for broadcast equipment surges during such events to ensure seamless coverage and transmission. At the same time, advancements in broadcasting technologies, such as 4K/UHD broadcasting, virtual reality (VR), augmented reality (AR), and immersive audio, are driving the adoption of advanced broadcast equipment in the region.

- Countries such as Bhutan, Iran, Bangladesh, and Vietnam are demonstrating the most significant mobile penetration advances, according to a GSMA report. The implementation of smart devices in the region is another factor fueling the demand for high-definition audio and videos. As per GSMA, 64% of the residents in APAC already possess smartphones, and the adoption is expected to cross 80% in 2025.

- Furthermore, in March 2023, Netflix announced plans to spend approximately USD 1.9 billion on local content in Asia-Pacific. The company was expected to register revenue growth of 12% Y-o-Y in 2023 and exceed USD 4 billion compared to 9% growth in 2022. In addition, according to ITU, 66% of the population in Asia-Pacific reported using the Internet as of 2023, further propelling the market's growth.

- Local vendors invested heavily to capitalize on the opportunities brought by the COVID-19 pandemic. For instance, in March last year, Signiant Inc. announced the acquisition of Kyno, which provides embedded media processing software. The acquisition helps Signiant Inc. extend the functionality of the Software-Defined Content Exchange (SDCX) SaaS platform, incorporating tools for engagement with media assets. With almost 1 million users globally, the platform connects more than 50,000 media and entertainment companies of all sizes.

Broadcast Equipment Industry Overview

The competitive rivalry between various firms in the broadcast equipment market depends on price, product, or market share, along with the intensity with which they compete. Some major market players include Cisco Systems Inc., Telefonaktiebolaget LM Ericsson, Harmonic Inc., EVS Broadcast Equipment SA, and Grass Valley.

- April 2024: Haivision Systems, a global provider of mission-critical, real-time video networking and visual collaboration solutions, announced that Haivision and Sony Corporation (Sony) had successfully tested Haivision's industry-leading video encoders, decoders, and mobile video transmitters with Sony's cloud production platform, Creators' Cloud for Enterprise.

- February 2024: Sony announced the launch of a unique dedicated portable data transmitter, the PDT-FP1, that allows high-speed, low-latency video and still image data transport over 5G networks. When attached to a camera, this wireless communication device will be used when speed is required, from image capture to delivery, broadcasting, and distribution, such as news or events photography and broadcast video production. It provides high-speed, low-latency, and stable mobile data communication over 5G networks in outdoor or indoor environments where a Wi-Fi connection is unavailable, enabling efficient and straightforward workflows.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Research Framework

- 2.2 Secondary Research

- 2.3 Primary Research

- 2.4 Data Triangulation and Insight Generation

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Value Chain Analysis

- 4.4 Impact of Key Macroeconomic Trends on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Demand for Encoders due to Support for Multiple Formats

- 5.1.2 Growing D2C Offerings through OTT Services

- 5.1.3 Increased Adoption of SAAS Solutions

- 5.2 Market Restraint

- 5.2.1 Lack of Standardization of Media Formats and Codecs Used for Broadcasting

6 MARKET SEGMENTATION

- 6.1 By Technology

- 6.1.1 Analog Broadcasting

- 6.1.2 Digital Broadcasting

- 6.2 By Product

- 6.2.1 Dish Antennas

- 6.2.2 Switches

- 6.2.3 Video Servers

- 6.2.4 Encoders

- 6.2.5 Transmitters and Repeaters

- 6.2.6 Other Products

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia-Pacific

- 6.3.4 Latin America

- 6.3.5 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Cisco Systems Inc.

- 7.1.2 Telefonaktiebolaget LM Ericsson

- 7.1.3 Evs Broadcast Equipment SA

- 7.1.4 Grass Valley

- 7.1.5 Harmonic Inc.

- 7.1.6 Clyde Broadcast

- 7.1.7 Sencore Inc.

- 7.1.8 Eletec Broadcast Telecom Sarl

- 7.1.9 AVL Technologies Inc.

- 7.1.10 ETL Systems Ltd

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

2026年全球即时网际网路通讯协定(IP)广播设备市场报告2026年全球广播级动圈USB麦克风市场报告

2026年全球即时网际网路通讯协定(IP)广播设备市场报告2026年全球广播级动圈USB麦克风市场报告 全球即时IP直播设备市场-按产品、应用、地区和竞争格局分類的产业规模、份额、趋势、机会和预测(2021-2031年)

全球即时IP直播设备市场-按产品、应用、地区和竞争格局分類的产业规模、份额、趋势、机会和预测(2021-2031年) 专业直播设备市场:依产品类型、最终用途、解析度、工作流程、分发方式、连接方式和价格范围划分,全球预测(2026-2032年)广播监控市场按监控类型、部署类型、行业垂直领域和最终用户划分 - 全球预测 2026-2032 年广播设备市场-全球产业规模、份额、趋势、机会和预测,依技术、产品、地区和竞争格局划分,2021-2031年预测

专业直播设备市场:依产品类型、最终用途、解析度、工作流程、分发方式、连接方式和价格范围划分,全球预测(2026-2032年)广播监控市场按监控类型、部署类型、行业垂直领域和最终用户划分 - 全球预测 2026-2032 年广播设备市场-全球产业规模、份额、趋势、机会和预测,依技术、产品、地区和竞争格局划分,2021-2031年预测 广播设备市场规模、份额和成长分析(按类型、技术、频段、应用和地区划分)-产业预测,2026-2033年

广播设备市场规模、份额和成长分析(按类型、技术、频段、应用和地区划分)-产业预测,2026-2033年 广播监视器 - 全球市场份额和排名、总收入和需求预测(2025-2031 年)

广播监视器 - 全球市场份额和排名、总收入和需求预测(2025-2031 年) 全球广播设备市场-2025年至2030年预测

全球广播设备市场-2025年至2030年预测 广播天线市场规模、份额、应用成长分析、频段、天线类型和地区 - 产业预测,2025-2032

广播天线市场规模、份额、应用成长分析、频段、天线类型和地区 - 产业预测,2025-2032