|

市场调查报告书

商品编码

1629801

真空帮浦:市场占有率分析、产业趋势/统计、成长预测(2025-2030)Vacuum Pump - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

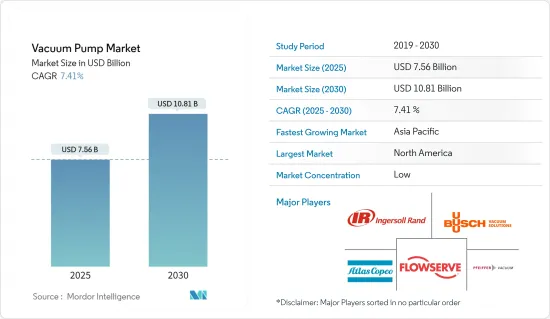

真空帮浦市场规模预估至2025年为75.6亿美元,预估至2030年将达108.1亿美元,预测期间(2025-2030年)复合年增长率为7.41%。

真空帮浦是一种从密封体积中吸入气体颗粒、产生部分真空的帮浦。真空帮浦在众多产业中都有广泛的应用。真空帮浦对各种应用的适应性是全球真空帮浦市场的关键成长引擎。此外,真空帮浦还可用于多种应用,包括清洗、密封等。

主要亮点

- 真空帮浦广泛用于各种工业和科学应用。它用于生产 CRT、真空管、电灯、飞机设备、印刷机、玻璃和石材切割厂、真空医疗应用、电子显微镜、光刻、铀浓缩、复合材料成型等。

- 真空帮浦由于其多功能性而被用于多种应用。石油和天然气行业采用这种机械进行天然气开采和压缩,对市场产生了重大影响。全球真空帮浦市场的主要成长动力是原油产量的增加和新油田的发现。

- 此外,真空帮浦对于半导体装置的製造至关重要。智慧型手机和其他家用电子电器产品、汽车和其他应用程式正在推动对半导体 IC 的需求。这些将由 5G 无线和人工智慧等技术创新驱动。而且,随着目前基于物联网的设备的普及,半导体产业有望对这台机器进行投资。

- 真空泵也对製药业产生重大影响。这些泵浦用于所有製造过程,包括干燥、蒸馏、脱气、结晶、昇华和填充。每个真空帮浦都是用于製造中间产品、原料药和原料药的真空灌注系统的组成部分。真空帮浦是在价值链中执行重要任务的重要组件,因为它们用于各种最终用户产业的这些应用。

- 此外,为了保持市场竞争力,许多供应商继续透过各种联盟、产品发布、收购和其他活动进行投资。例如,阿特拉斯科普柯于 2022 年 1 月完成了对 HHV Pumps Pvt. Ltd 的收购。该业务开发和製造用于多种行业的真空泵和真空系统。 THHV Pumps 是旋片泵的领先供应商,其产品用于製造冷冻和空调、化学和製药行业、电力设备和一般行业的真空泵。

- 此外,由于医疗产业真空帮浦使用的研究和开发不断扩大,市场可能拥有利润丰厚的成长机会。此外,由于真空帮浦在海水淡化中的使用不断增加以及在太阳能价值链中的重要性日益增加,预计真空帮浦将为市场参与企业提供成长机会。

- 由于真空帮浦的广泛应用和优点,预计市场将收到来自多个行业的巨大需求。然而,真空帮浦安装不当、能耗高以及产品运作和维护成本增加可能会限制市场扩张。

- 真空技术市场最初受到 COVID-19 大流行造成的供应链和物流中断的影响。但随后其他解决方案的采用有所增加。阿尔特斯·科普柯表示,设备订单也有所增加,主要是因为半导体产业多个地区对真空设备的需求增加。各行业开始恢復至或高于疫情前水平,市场预计将继续扩大。

真空帮浦市场趋势

旋转真空帮浦预计将占据主要市场占有率

- 旋转真空帮浦是在各种场合使用的帮浦之一,并被各个领域的专业人士使用。该泵浦采用正排量系统,最常用于商业、工业、汽车和商业行业。它也可用于实验室和工业环境。在这些情况下最常被泵送的流体是天然气、石油和水。

- 旋片帮浦最常用于汽车产业。此类型帮浦用于汽车煞车系统、动力方向盘系统、自动变速箱、增压系统等。旋转真空帮浦也用于各种车辆系统,例如飞机。空调、浓缩咖啡和软性饮料分配器也是此类帮浦的应用。

- 此外,转叶真空帮浦最常用于汽车产业,是各种车辆零件的重要组成部分。例如,动力方向盘系统中的液压流体使用旋片泵加压。它也用作自动变速器的固定和可变输出单元。随着汽车工业的成长,旋片帮浦的需求预计将大幅增加。例如,根据SIAM的数据,印度境内派遣的车辆数量从上一财年的1,414,277辆增加到2022-23年的1,706,831辆,增加了21%。

- 除了真空之外,旋转真空帮浦还可以使用清洁空气干运转或泵送液体(例如石油和天然气)。石油和天然气产业是一个显着推动旋转真空帮浦需求的产业。此外,由于有关真空泵整合到石油和天然气行业的持续研究和开发,市场可能会享受利润丰厚的扩张机会。

- 旋转真空帮浦也可用于从封闭或受限空间中抽吸空气或气体。真空泵广泛应用于食品和饮料、加工、化学和製药、汽车、石油和天然气等行业。此外,随着有关真空泵整合到这些行业的研究和开发的不断增加,市场可能会受益于利润丰厚的扩张机会。

北美占据主要市场占有率

- 由于需求未满足、水资源短缺加剧以及对清洁饮用水的需求不断增加,在美国的推动下,预计北美在预测期内将占据真空帮浦市场最大的市场占有率。此外,製药、医疗、工业製造和许多其他行业的大量研究和开发将有助于满足预测期内不断增长的需求。

- 对石油和天然气、化学品和发电等最终用户产业的投资不断增加,对北美地区的真空帮浦市场产生了重大影响。油砂是包括美国和加拿大在内的该地区国家丰富的石油来源。例如,根据加拿大自然资源部的数据,加拿大已探明蕴藏量的 97% 是在油砂中发现的。

- 饮料加工是另一个受益于真空帮浦使用的行业。由于最近的技术趋势和不断上升的投资水平,预计该地区的饮料加工行业将为市场提供许多机会。例如,2023 年 1 月,雀巢宣布斥资 4,300 万美元扩建威斯康辛州工厂,以增加 Boost 和 Carnation Breakfast Essentials 即饮 (RTD) 产品的产量。此类投资预计将增加工业对真空帮浦的需求。

- 此外,美国是开发新的可再生能源技术的领导者之一,并开创了多个太阳能计划。在美国,能源生产持续快速成长。例如,美国主要石油生产商之一埃克森美孚最近宣布,计划在2024年在德克萨斯州州二迭纪盆地生产约100万桶/日石油当量,以扩大其生产业务。这些因素预计将为製造商提供更多机会来满足需求并加速市场扩张。

- 真空帮浦广泛应用于采矿厂,因此随着北美地区煤炭销量的增加,采矿公司的投资可能会增加。

真空帮浦产业概况

真空帮浦市场按知名全球参与企业和参与企业的存在进行细分。此外,全球对发电基础设施研发的投资以及石油和天然气设备升级是竞争对手之间激烈竞争的重要驱动力。主要参与企业包括 Gardner Denver Inc.、阿特拉斯·科普柯集团和福斯公司。

- 2023 年 10 月,阿特拉斯科普柯推出了下一代干爪式真空帮浦 DZS A 系列。这个新系列树立了效能、效率和可靠性的基准。 DZS A 系列在设计时考虑了製造业不断变化的需求,具有显着的优势。

- 2023 年 3 月,Fowserve Corporation 宣布推出 SIHI Boost UltraPLUS 干运转真空帮浦。该新装置旨在将批次的週期时间缩短 50% 或更多。

其他好处

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买方议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间敌对关係的强度

- 产业价值链分析

- 工业措施

- COVID-19 对真空帮浦市场的影响

第五章市场动态

- 市场驱动因素

- 增加石油产量和新油田

- 对干式真空帮浦的需求增加

- 市场问题

- 高成本和相容性问题

第六章 市场细分

- 按类型

- 旋转真空帮浦

- 旋片泵

- 螺旋泵和爪泵

- 罗茨帮浦

- 往復式真空帮浦

- 隔膜泵

- 活塞泵

- 动力真空帮浦

- 喷射帮浦

- 涡轮分子泵浦

- 扩散泵浦

- 动力泵

- 液环帮浦

- 侧吸泵

- 特殊真空帮浦

- 吸气帮浦

- 低温泵

- 旋转真空帮浦

- 按最终用户使用情况

- 石油和天然气

- 电子产品

- 医疗保健

- 化学处理

- 饮食

- 发电

- 其他最终用户应用(木材、纸张/纸浆等)

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东/非洲

第七章 竞争格局

- 公司简介

- Ingersoll Rand Inc.

- Atlas Copco AB(Edwards)

- Flowserve Corporation

- Busch Vacuum Solutions(Busch group)

- Pfeiffer Vacuum GmbH(Pfeiffer Vacuum Technology AG)

- ULVAC Inc.

- Graham Corporation

- Global Vac

- Becker Pumps Corporation

- Ebara Corporation

- Wintek Corporation

- Tsurumi Manufacturing Co. Ltd

第八章投资分析

第9章市场的未来

The Vacuum Pump Market size is estimated at USD 7.56 billion in 2025, and is expected to reach USD 10.81 billion by 2030, at a CAGR of 7.41% during the forecast period (2025-2030).

A vacuum pump is a type of pump that draws gas particles from a sealed volume and leaves a partial vacuum behind. There are numerous applications for vacuum pumps across numerous industries. Vacuum pumps' adaptability in various applications is a crucial growth engine for the global vacuum pump market. Additionally, it is utilized in multiple applications, including cleaning, sealing, and others.

Key Highlights

- Vacuum pumps are used in a wide variety of industrial and scientific applications. They manufacture CRTs, vacuum tubes, electric lamps, flight instruments, print presses, glass and stone cutting factories, suction-based medical applications, electron microscopy, photolithography, uranium enrichment, and composite molding.

- Due to their versatility, vacuum pumps are used in various applications. The oil and gas industry has adopted this machine to extract and compress the gas, which significantly impacts the market. The main growth drivers for the global vacuum pump market are rising crude oil production and the discovery of newer oilfields.

- Additionally, vacuum pumps are crucial to the manufacturing of semiconductor devices. Smartphones and other consumer electronics, automotive, and other applications drive the demand for semiconductor ICs. These are brought on by technological changes, including 5G wireless and artificial intelligence. Additionally, the semiconductor industry is anticipated to invest in this machinery due to the current popularity of Internet of Things-based devices.

- Vacuum pumps also have a significant impact on the pharmaceutical sector. All manufacturing processes use these pumps, including drying, distillation, degassing, crystallization, sublimation, and filling. Each vacuum pump is a component of a vacuum prime system used to create intermediate goods, active pharmaceutical ingredients, and large-scale pharmaceuticals. Vacuum pumps are essential components that perform essential tasks in the value chain because of these applications in various end-user industries.

- Moreover, to maintain a competitive edge in the market, many vendors continuously invest through a range of partnerships, product launches, acquisitions, and other activities. For instance, Atlas Copco completed the acquisition of HHV Pumps Pvt. Ltd in January 2022. The business develops and produces vacuum pumps and systems for use in a variety of industries. THHV Pumps is a top supplier of rotary vane pumps used in the production of refrigeration and air conditioning, vacuum pumps for the chemical and pharmaceutical industries, electrical power equipment, and general industry.

- Additionally, the market may have a profitable opportunity for growth due to growing research and development into the use of vacuum pumps in the medical industry. Additionally, vacuum pumps are expected to present growth opportunities for the market's players due to their increasing use in seawater desalination and their increasing significance in the photovoltaics value chain.

- Due to their wide-ranging applications and advantages, the market is anticipated to experience significant demand from several industries. However, improper vacuum pump installation, high power consumption, and increased product operation and maintenance costs could restrain market expansion.

- Due to supply chain and logistics disruptions brought on by the COVID-19 pandemic, the market for vacuum technologies was initially impacted. Later on, however, it saw a rise in adopting several other solutions. According to Altas Copco, order volumes for equipment also increased, primarily due to an increase in vacuum equipment demand across several regions in the semiconductor industry. The industries have begun to resume operations at levels equal to or higher than before the pandemic, so the market is anticipated to continue to expand.

Vacuum Pump Market Trends

Rotary Vacuum Pump Expected to Hold Significant Market Share

- The rotary vacuum pump is one of these types of pumps that is useful in various situations and used by professionals in multiple fields. These pumps, which use a positive displacement system, are most frequently used in the commercial, industrial, automotive, and Commercial industries. It can be used in laboratory and industrial settings as well. The fluids that are pumped most frequently in these situations are gas, oil, and water.

- The automotive sector is the one that employs rotary vane pumps the most. This kind of pump is used in the car's braking system, power steering system, automatic transmission, and supercharging system, among other places. Rotary vacuum pumps are used in the systems of different vehicle types, such as airplanes. Some air conditioners, espresso, and soft drink dispensers are other applications for this kind of pump.

- Moreover, the automotive industry is where rotary vane vacuum pumps are most frequently used, where they are essential parts of many different vehicle parts. For example, hydraulic fluid in power steering systems is pressurized using rotary vane pumps. Additionally, they are employed as fixed and variable output units in automatic transmissions. The demand for Rotary vane pumps is anticipated to increase significantly with the growth of the automotive industry. For instance, according to SIAM, domestic dispatches in India increased by 21% to 17,06,831 units in 2022-23 from 14,14,277 units in the preceding fiscal year.

- Rotating vacuum pumps can run dry with clean air or pump oil, gas, and other liquids in addition to the vacuum. The oil and gas industry is a sector that significantly boosts demand for Rotary vacuum pumps. Additionally, the market may benefit from a lucrative expansion opportunity due to growing research and development into the integration of vacuum pumps into the oil and gas industry.

- Air and gases can also be pumped out of a sealed or constrained space using rotary vacuum pumps. Food and beverage, processing, chemical and pharmaceutical, automotive, oil and gas, and a wide range of other industries all use them. Additionally, the market may benefit from a lucrative expansion opportunity due to growing research and development into the integration of vacuum pumps into these industries.

North America to Hold Significant Market Share

- North America is expected to hold the largest market share of the Vacuum Pump Market over the forecast period, led by the United States, owing to high unmet needs, growing water scarcity, and increased demand for clean drinking water. Additionally, over the forecasted period, significant research and developments in pharmaceutical, healthcare, industrial manufacturing, and many other industries will help to meet the rising demand.

- The rising investments in end-user industries like oil and gas, chemical, and power generation significantly impact the vacuum pump market in the North American region. Oil sands are a plentiful source of oil for the region's nations, including the US and Canada. For instance, 97% of Canada's proven oil reserves are found in the oil sands, according to Natural Resource Canada.

- The processing of beverages is yet another industry that gains from using vacuum pumps. The beverage processing industry in the region is expected to offer the market plenty of opportunities due to recent technological developments and rising investment levels. For instance, Nestle announced in January 2023 that it would expand a Wisconsin factory by USD 43 million in an effort to increase production of its Boost and Carnation Breakfast Essentials ready-to-drink (RTD) products. Such investments will increase the demand for vacuum pumps in the industry.

- Additionally, the US has been one of the leaders in developing new renewable energy technologies and has pioneered several solar energy projects. In the United States, energy production is still rising quickly. For instance, ExxonMobil, one of the major oil producers in the nation, recently announced plans to increase production activity in the West Texas Permian Basin by producing roughly 1 million BPD of oil equivalent by 2024. Such factors will accelerate market expansion by giving manufacturers more opportunities to meet demand.

- Due to their widespread use in mining plants, vacuum pumps may see an increase in investment by mining companies as coal sales in the North American region increase.

Vacuum Pump Industry Overview

The vacuum pump market is fragmented due to the presence of prominent global and local players. Also, global investment in R&D in power generation infrastructure and facility upgrades in the oil and gas are the essential drivers that are giving intense rivalry among competitors. Key players are Gardner Denver Inc., Atlas Copco Group, Flowserve Corporation, etc.

- October 2023: Atlas Copco, has announced its next generation of dry claw vacuum pumps - the DZS A series. This new series sets a benchmark for performance, efficiency, and reliability. Designed with the evolving needs of manufacturing industries in mind, the DZS A series offers significant advantages.

- March 2023: Fowserve Corporation has announced the release of the SIHI Boost UltraPLUS dry-running vacuum pump. The new unit is designed to reduce cycle times for batch processes by up to 50 percent or more.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Industry Policies

- 4.5 Impact of COVID-19 on the Vacuum Pumps Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rising Crude Oil Production and the Newer Oilfields

- 5.1.2 Increasing Demand for Dry Vacuum Pump

- 5.2 Market Challenges

- 5.2.1 High Cost and Compatibility Issues

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Rotary Vacuum Pumps

- 6.1.1.1 Rotary Vane Pumps

- 6.1.1.2 Screw and Claw Pumps

- 6.1.1.3 Roots Pumps

- 6.1.2 Reciprocating Vacuum Pumps

- 6.1.2.1 Diaphragm Pumps

- 6.1.2.2 Piston Pumps

- 6.1.3 Kinetic Vacuum Pumps

- 6.1.3.1 Ejector Pumps

- 6.1.3.2 Turbomolecular Pumps

- 6.1.3.3 Diffusion Pumps

- 6.1.4 Dynamic Pumps

- 6.1.4.1 Liquid Ring Pumps

- 6.1.4.2 Side Channel Pumps

- 6.1.5 Specialized Vacuum Pumps

- 6.1.5.1 Getter Pumps

- 6.1.5.2 Cryogenic Pumps

- 6.1.1 Rotary Vacuum Pumps

- 6.2 By End-user Application

- 6.2.1 Oil and Gas

- 6.2.2 Electronics

- 6.2.3 Medicine

- 6.2.4 Chemical Processing

- 6.2.5 Food and Beverage

- 6.2.6 Power Generation

- 6.2.7 Other End-user Applications (Wood, Paper and Pulp, etc.)

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia-Pacific

- 6.3.4 Latin America

- 6.3.5 Middle-East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Ingersoll Rand Inc.

- 7.1.2 Atlas Copco AB (Edwards)

- 7.1.3 Flowserve Corporation

- 7.1.4 Busch Vacuum Solutions (Busch group)

- 7.1.5 Pfeiffer Vacuum GmbH (Pfeiffer Vacuum Technology AG)

- 7.1.6 ULVAC Inc.

- 7.1.7 Graham Corporation

- 7.1.8 Global Vac

- 7.1.9 Becker Pumps Corporation

- 7.1.10 Ebara Corporation

- 7.1.11 Wintek Corporation

- 7.1.12 Tsurumi Manufacturing Co. Ltd

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

2025年全球工业真空帮浦市场报告2025年全球液环真空帮浦市场报告2025年全球真空帮浦市场报告

2025年全球工业真空帮浦市场报告2025年全球液环真空帮浦市场报告2025年全球真空帮浦市场报告 流量控制市场-全球产业规模、份额、趋势、机会及预测(按设备类型、应用、地区和竞争细分,2020-2030 年)

流量控制市场-全球产业规模、份额、趋势、机会及预测(按设备类型、应用、地区和竞争细分,2020-2030 年) 全球液环真空帮浦市场全球干式真空帮浦市场

全球液环真空帮浦市场全球干式真空帮浦市场 真空帮浦市场规模、份额、成长分析(按机制、按泵类型、按润滑方式、按压力、按真空介质、按最终用途、按地区)- 行业预测,2025 年至 2032 年全球涡轮分子帮浦市场全球真空帮浦市场:2034 年的机会与策略工业真空帮浦市场机会、成长动力、产业趋势分析及2025-2034年预测

真空帮浦市场规模、份额、成长分析(按机制、按泵类型、按润滑方式、按压力、按真空介质、按最终用途、按地区)- 行业预测,2025 年至 2032 年全球涡轮分子帮浦市场全球真空帮浦市场:2034 年的机会与策略工业真空帮浦市场机会、成长动力、产业趋势分析及2025-2034年预测