|

市场调查报告书

商品编码

1549737

永续食品服务包装:市场占有率分析、产业趋势与统计、成长预测(2024-2029)Sustainable Foodservice Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

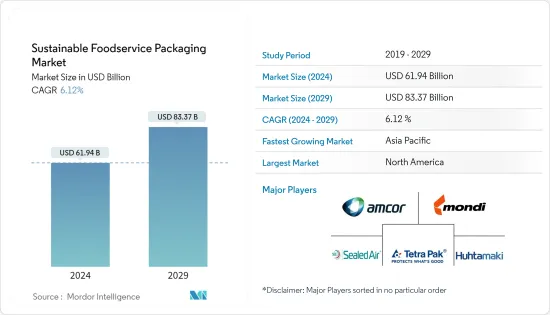

永续食品服务包装市场规模预计到 2024 年为 619.4 亿美元,预计到 2029 年将达到 833.7 亿美元,预测期内(2024-2029 年)复合年增长率为 6.12%

主要亮点

- 随着客户越来越关注环境问题和包装洩漏的影响,包装的永续性已成为塑造产业的关键趋势。因此,各个领域都出现了严格的永续性要求。食品服务业担心塑胶包装对环境的影响,正在转向回收材料,并正在推动市场研究。公司越来越多地采用可回收和生物分解性的材料,这不仅有助于减少碳排放,还迎合了具有环保意识的消费者群体。

- 城市人口的快速成长正在推动对已调理食品和已调理食品的需求,从而导致食品服务业对永续包装解决方案的需求不断增加。因此,食品服务业对永续包装解决方案的需求不断增加。都市化增加了人口向都市区的集中,增加了对方便食品选择的需求。这种趋势在大都会圈尤其明显,忙碌的生活方式需要快速、简单的饮食解决方案,导致对食品包装的依赖增加。

- 在全部区域,都市化、不断变化的生活方式、现代忙碌的工作生活以及对线上食品平台的日益依赖正在重塑食品服务和格局。这种转变增加了该行业对永续包装解决方案的需求。线上食品宅配服务的便利性导致一次性包装的激增,从而促使人们需要更永续的替代品。各公司正透过开发创新包装来应对,这种包装不仅环保,还能在运输过程中保持食品的品质和安全。

- 随着产业转向无废弃物的未来,包装创新(包括新材料、再填充系统和回收解决方案)等挑战日益凸显。雀巢透过雀巢包装科学研究所进行了广泛的内部研究,并设立了 2.5 亿瑞士法郎的永续包装风险基金,以支持专注于这些重要领域的新兴企业。该基金旨在加速尖端永续包装技术的开发和采用,并确保新的解决方案有效且可扩展。

- 值得注意的是,虽然永续包装的好处显而易见,但其成本却明显高于传统食品服务替代品。这种成本差异是由于从原始来源和回收来源采购材料以及该行业仍在发展的供应链和製造流程造成的,所有这些目前都缺乏规模经济,阻碍了市场成长。成本上升也归因于开发满足行业标准和消费者期望的永续包装解决方案所需的先进技术和研究。

永续食品服务包装市场趋势

快餐店可望推动终端用户市场

- 快餐店 (QSR) 优先考虑快速的服务和实惠的价格,这使它们有别于专注于最低限度餐桌服务和自助服务的传统餐厅。然而,该行业对永续性的立场并不一致。

- 传统上,QSR 与不太环保的做法联繫在一起,例如发泡聚苯乙烯杯、塑胶盖、纸板架、基因改造蔬菜和无机肉类,但潮流正在改变。随着客户越来越重视绿色服务,许多快餐店正在转向越来越环保的选择。

- 一些快餐店,尤其是那些以有机食品闻名的快餐店,正在积极采用环保做法来减少碳排放。这些努力包括采购有机和当地农产品、使用生物分解性的包装以及实施节能业务。

- 此外,该领域的合作伙伴关係正在迅速增加,这在很大程度上是由于对永续包装解决方案的需求不断增长所推动的。这些合作伙伴关係通常包括与专门从事环保材料和技术的供应商合作,进一步促进行业内的永续性。例如,2024 年 6 月,包装解决方案公司 Saica Group 与主要企业的快速消费品製造商 Mondelez 合作推出了一款创新纸质产品。该产品专为糖果零食、饼干和巧克力市场的合装包而设计。新包装可在废纸流中回收,并可热封。此外,它还可以根据最终外观灵活地製造涂层或不涂层的产品。

亚太地区占最大市场占有率

- 亚太地区是中国和印度等人口稠密的新兴经济体的所在地,食品服务的需求正在激增。同时,我们看到了向永续包装的显着转变,该地区预计将在未来几年引领这一趋势。这种转变是由消费者对环境问题的意识增强以及政府为减少塑胶废弃物而製定的严格法规所推动的。

- 塑胶长期以来一直是消费者包装便利的基石,但其主导地位正在减弱。儘管具有成本效益,但塑胶在食品工业中正在超越纸板、玻璃和金属等传统材料。但塑胶如此有吸引力的耐用性意味着它无法分解,印度 43% 的污染是由它造成的。塑胶废弃物对环境的影响促使公共和私营部门寻找永续的替代品。

- 认识到这一紧迫性,印度铁路和印度航空等公司已承诺用环保纸张和木製刀叉餐具取代塑料,这标誌着向更广泛行业的转变。这些努力是更大范围的永续性运动的一部分,包括减少碳足迹和促进循环经济。从大公司到本土品牌,抛弃一次性塑胶而转而使用可回收、可重复使用和可堆肥替代品的势头越来越大。这项转变不仅可望减少环境破坏,还能实现全球永续性目标。

永续食品包装产业概述

在永续食品服务包装市场,Amcor Limited、Sealed Air Corporation 和 Mondi PLC 等知名公司正在透过策略合作伙伴关係、联盟和创新措施推动成长。这些努力包括开发环保包装解决方案、投资研发以及扩大产品系列。这些活动正在推动市场发展势头并满足对永续包装选择不断增长的需求。

- 2024 年 3 月,SEE 推出创新的纸质底网,帮助食品加工商和零售商减少塑胶的使用,同时满足消费者对纸包装不断增长的需求。该产品以 CRYOVAC Barrier Formable Paper 品牌销售,由 90% FSC 认证纤维组成。据 SEE 称,用这种阻隔成型纸取代传统的 PET/PE 捲材可以将底部卷材包装中的塑胶使用量显着减少 77%。

其他好处:

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场洞察

- 市场概况

- 产业价值链分析

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买方议价能力

- 新进入者的威胁

- 竞争程度

- 替代品的威胁

- 生态系分析

- 评估微观经济因素对工业的影响

第五章市场动态

- 市场驱动因素

- 线上食品订购服务推动市场

- 消费者偏好转向可回收和环保材料

- 市场限制因素

- 永续食品服务包装所用材料的高回收成本可能会阻碍市场成长

第六章 市场细分

- 依产品类型

- 瓦楞纸箱和纸箱

- 托盘、盘子、食品容器、碗

- 翻盖式

- 其他产品类型

- 按最终用户

- 快速服务餐厅

- 全方位服务餐厅

- 制度性的

- 款待

- 其他最终用户

- 按地区

- 北美洲

- 美国

- 加拿大

- 欧洲

- 英国

- 德国

- 其他欧洲国家

- 亚太地区

- 中国

- 日本

- 印度

- 其他亚太地区

- 拉丁美洲

- 中东/非洲

- 北美洲

第七章 竞争格局

- 公司简介

- Amcor PLC

- Mondi PLC

- Sealed Air Corporation

- Tetra Pak International SA

- Huhtamaki Oyj

- Winpak Limited

- Amhil North America

- Sonoco Products Company

- WestRock Company

- Dart Container Corporation

第八章投资分析

第9章 市场的未来

The Sustainable Foodservice Packaging Market size is estimated at USD 61.94 billion in 2024, and is expected to reach USD 83.37 billion by 2029, growing at a CAGR of 6.12% during the forecast period (2024-2029).

Key Highlights

- With a rising customer focus on environmental concerns and the repercussions of package leaks, sustainability in packaging emerges as a pivotal trend shaping the industry. Consequently, stringent sustainability mandates are emerging across various sectors. The foodservice industry, alarmed by the environmental impact of plastic containers, is pivoting toward recycled materials, propelling the market studied. Companies are increasingly adopting recycled and biodegradable materials to meet these new standards, which not only help in reducing the carbon footprint but also cater to the eco-conscious consumer base.

- The surge in urban population growth is fueling the demand for prepared and ready-to-eat foods, consequently bolstering the need for sustainable packaging solutions in the foodservice sector. This, in turn, is set to drive the market in the coming years. Urbanization leads to a higher concentration of people in cities, which increases the demand for convenient food options. This trend is particularly evident in metropolitan areas where busy lifestyles necessitate quick and easy meal solutions, thereby increasing the reliance on foodservice packaging.

- Across major regions, urbanization, evolving lifestyles, the rush of modern work life, and a growing reliance on online food platforms are reshaping the food service and landscape. This shift is amplifying the call for sustainable packaging solutions in the sector. The convenience of online food delivery services has led to a surge in single-use packaging, prompting a need for more sustainable alternatives. Companies are responding by developing innovative packaging that is not only eco-friendly but also maintains the quality and safety of food during transit.

- As the industry steers toward a waste-free future, challenges like packaging innovation, encompassing novel materials, refill systems, and recycling solutions, come to the forefront. Nestle, bolstering commitment, conducts extensive in-house research via the Nestle Institute of Packaging Sciences, earmarking a CHF 250 million sustainable packaging venture fund to back startups focusing on these pivotal areas. This fund aims to accelerate the development and adoption of cutting-edge sustainable packaging technologies, ensuring that new solutions are both effective and scalable.

- While the benefits of sustainable packaging are evident, it is crucial to note that its costs are notably higher than traditional foodservice alternatives. This cost disparity is attributed to the sourcing of materials, both virgin and recycled, and the industry's nascent supply chains and manufacturing processes, all of which currently lack economies of scale, thus impeding market growth. The higher costs are also due to the advanced technology and research required to develop sustainable packaging solutions that meet industry standards and consumer expectations.

Sustainable Foodservice Packaging Market Trends

Quick-service Restaurants are Expected to Drive the Market Among End Users

- Quick-service restaurants (QSRs) prioritize fast service and affordability, distinguishing them from traditional dining establishments with their minimal table service and self-service focus. However, the industry's stance on sustainability has been inconsistent.

- While QSRs have historically been associated with less eco-friendly practices, such as styrofoam cups, plastic lids, cardboard holders, genetically modified vegetables, and inorganic meat, the tide is turning. With customers increasingly valuing eco-conscious services, many QSRs are pivoting toward greener, more eco-friendly options.

- Some QSRs, particularly those known for their organic offerings, are actively adopting eco-friendly practices to shrink their carbon footprint. These practices include sourcing organic and locally grown produce, using biodegradable packaging, and implementing energy-efficient operations.

- Moreover, the sector is witnessing a surge in partnerships, largely driven by the growing demand for sustainable packaging solutions. These collaborations often involve working with suppliers who specialize in eco-friendly materials and technologies, further promoting sustainability within the industry. For instance, in June 2024, Saica Group, a packaging solutions company, and Mondelez, a leading fast-moving consumer goods manufacturer, collaborated to introduce an innovative paper-based product. This product is specifically designed for multipack offerings in the confectionery, biscuits, and chocolate markets. The new packaging is recyclable within the paper waste stream and compatible with heat-seal processes. Additionally, it offers the flexibility of being produced either coated or uncoated, depending on the desired final appearance.

Asia-Pacific Accounts for the Largest Market Share

- The Asia-Pacific region, home to densely populated and emerging economies like China and India, is witnessing a surge in the demand for food services. Concurrently, there is a notable shift toward sustainable packaging, with the region poised to lead this trend in the coming years. This shift is driven by increasing consumer awareness about environmental issues and stringent government regulations to reduce plastic waste.

- While plastic has long been the cornerstone of consumer convenience in packaging, its dominance is being challenged. Despite its cost-effectiveness, plastics have edged traditional materials like corrugated paper boards, glass, and metals in the food industry. Yet, the very durability that makes plastic appealing also renders it non-degradable, leading to a concerning 43% pollution contribution in India. The environmental impact of plastic waste has prompted both public and private sectors to seek sustainable alternatives.

- Recognizing the urgency, entities like the Indian Railways and Air India have pledged to swap plastic for eco-friendly paper and wooden cutlery, signaling a broader industry shift. These initiatives are part of a larger movement toward sustainability, which includes efforts to reduce carbon footprints and promote circular economies. From major corporations to local brands, there is a palpable momentum toward ditching single-use plastics in favor of recyclable, reusable, and compostable alternatives. This transition is expected to not only mitigate environmental damage but also align with global sustainability goals.

Sustainable Foodservice Packaging Industry Overview

In the sustainable foodservice packaging market, prominent companies like Amcor Limited, Sealed Air Corporation, and Mondi PLC are driving growth through strategic partnerships, collaborations, and innovative initiatives. These efforts encompass the development of eco-friendly packaging solutions, investment in research and development, and the expansion of product portfolios. Such activities are enhancing the market's momentum and meeting the rising demand for sustainable packaging options.

- March 2024: SEE introduced an innovative paper-based bottom web designed to assist food processors and retailers in reducing plastic usage while meeting the growing consumer demand for paper packaging. Marketed under the CRYOVAC Barrier Formable Paper brand, this product is composed of 90% FSC-certified fibers. According to SEE, replacing traditional PET/PE webs with this Barrier Formable Paper can achieve a significant 77% reduction in plastic usage in bottom web packaging.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Degree of Competition

- 4.3.5 Threat of Substitutes

- 4.4 Industry Ecosystem Analysis

- 4.5 Assessment of the Impact of Microeconomic Factors on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Online Food Ordering Services Will Drive the Market

- 5.1.2 Shift in Consumer Preferences Toward Recyclable and Eco-friendly Materials

- 5.2 Market Restraints

- 5.2.1 The High Recycling Cost for the Materials Used for the Sustainable Foodservice Packaging Might Hinder the Growth of the Market

6 MARKET SEGMENTATION

- 6.1 By Product Type

- 6.1.1 Corrugated Boxes and Cartons

- 6.1.2 Trays, Plates, Food Containers, and Bowls

- 6.1.3 Clamshells

- 6.1.4 Other Product Types

- 6.2 By End Users

- 6.2.1 Quick Service Restaurants

- 6.2.2 Full Service Restaurants

- 6.2.3 Institutional

- 6.2.4 Hospitality

- 6.2.5 Other End Users

- 6.3 By Geography

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.2 Europe

- 6.3.2.1 United Kingdom

- 6.3.2.2 Germany

- 6.3.2.3 Rest of Europe

- 6.3.3 Asia-Pacific

- 6.3.3.1 China

- 6.3.3.2 Japan

- 6.3.3.3 India

- 6.3.3.4 Rest of Asia-Pacific

- 6.3.4 Latin America

- 6.3.5 Middle East & Africa

- 6.3.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Amcor PLC

- 7.1.2 Mondi PLC

- 7.1.3 Sealed Air Corporation

- 7.1.4 Tetra Pak International SA

- 7.1.5 Huhtamaki Oyj

- 7.1.6 Winpak Limited

- 7.1.7 Amhil North America

- 7.1.8 Sonoco Products Company

- 7.1.9 WestRock Company

- 7.1.10 Dart Container Corporation

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

可回收种植袋市场:按材料类型、分销管道、应用分类 - 全球预测 2025-2030

可回收种植袋市场:按材料类型、分销管道、应用分类 - 全球预测 2025-2030 到 2030 年牛皮纸块底袋全球市场预测:按牛皮纸、产能、最终用户和地区进行分析

到 2030 年牛皮纸块底袋全球市场预测:按牛皮纸、产能、最终用户和地区进行分析 永续包装:全球市场

永续包装:全球市场 永续包装:市场占有率分析、产业趋势与统计、成长预测(2024-2029)

永续包装:市场占有率分析、产业趋势与统计、成长预测(2024-2029) 永续塑胶包装市场,按材料类型、按应用、按包装类型、按最终用途行业、按国家和地区 - 2024-2032 年行业分析、市场规模、市场份额和预测

永续塑胶包装市场,按材料类型、按应用、按包装类型、按最终用途行业、按国家和地区 - 2024-2032 年行业分析、市场规模、市场份额和预测 永续塑胶包装:全球市场

永续塑胶包装:全球市场 按类型和地区分類的永续包装市场规模、份额和增长分析 - 行业预测,2024-2031 年

按类型和地区分類的永续包装市场规模、份额和增长分析 - 行业预测,2024-2031 年 永续电子商务包装:市场占有率分析、产业趋势与统计、成长预测(2024-2029)

永续电子商务包装:市场占有率分析、产业趋势与统计、成长预测(2024-2029) 永续的包装市场:2035年前的产业趋势和全球预测 - 各环保型包装形式,各包装形式,各包装容器类型,各终端用户,各主要地区

永续的包装市场:2035年前的产业趋势和全球预测 - 各环保型包装形式,各包装形式,各包装容器类型,各终端用户,各主要地区 永续包装市场:按材料、功能、包装类型、产业划分 - 2024-2030 年全球预测

永续包装市场:按材料、功能、包装类型、产业划分 - 2024-2030 年全球预测