|

市场调查报告书

商品编码

1549956

汽车保固管理:市场占有率分析、产业趋势/统计、成长预测(2024-2029)Automotive Warranty Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

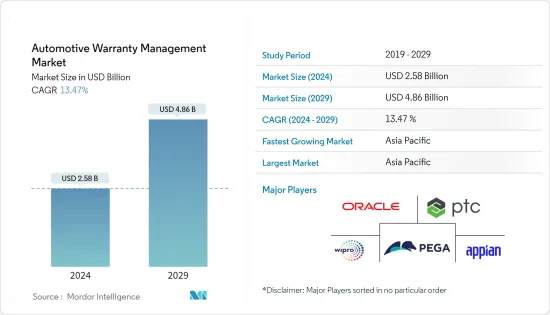

汽车保固管理市场规模预计到 2024 年为 25.8 亿美元,预计到 2029 年将达到 48.6 亿美元,在预测期内(2024-2029 年)复合年增长率为 13.47%。

汽车产业产量的增加是推动市场的关键因素,因为汽车和供应链产业在保证软体的采用中占据最大份额。此外,消费者采用连网型汽车的趋势也预计将影响全球汽车需求并推动市场。

如今,OEM在保固管理方面的主要关注点是遵守其政策和程序,确保按时进行维修,并保持车辆品质和可靠性。但实现成本节约同样重要。因此,OEM越来越多地采用保固管理解决方案,以提高盈利、提高客户满意度并保持竞争优势。

汽车公司不断努力提高产品质量,以降低保固成本、提高客户满意度并增强财务绩效。然而,品质往往受到新产品需求快速成长、竞争加剧、技术进步和供应链中断等因素的影响。平均而言,汽车和工业公司的保固索赔成本占年销售额的 1.5% 至 2.5%,导致收益大幅损失并降低客户满意度。公司经常加快保固服务和零件更换,以缓解这些挑战,从而保持客户忠诚度。考虑到这些挑战,汽车製造商必须将人工智慧 (AI) 和机器学习 (ML) 等技术整合到传统的保固管理系统中。

作为回应,一些市场参与者正在实施基于人工智慧和机器学习的解决方案。例如,2023 年 8 月,总部位于加利福尼亚州、为汽车行业提供人工智慧和决策分析解决方案的软体公司 FrogData 推出了一家旨在优化经销商保固申请流程的软体公司,并宣布推出 WarrantyMind AI。到端的远端保固管理服务。

然而,这些解决方案处理敏感的客户和车辆资料,使得安全漏洞对于品牌声誉和客户信任至关重要。因此,资料和身分盗窃挑战正在阻碍市场成长,需要投资网路安全措施来保护资料。

COVID-19 大流行期间,全球汽车保固管理市场面临挑战与机会。封锁和供应链中断导致零件短缺和维修延误,造成保固申请积压,并使保固管理系统紧张。此外,这场危机凸显了资料主导决策的价值,以及对具有资料分析功能的汽车保固系统的需求,以识别趋势并提高服务中心效率。

汽车保固管理市场趋势

云端基础的保固管理系统预计将显着推动市场成长

由于 COVID-19 大流行,云端基础的保固管理解决方案促进了远端工作,并确保保固团队在锁定期间持续存取资料。这些云端采用趋势预计将在疫情后继续下去,推动汽车产业采用云端基础的保固管理解决方案。

汽车行业越来越多地采用云端技术有很多好处,包括可扩展性、节省成本以及改善全球团队、设计师和製造部门的协作,以即时存取和共用资料。开发。这些优势预计将进一步推动云端基础的保固管理解决方案的采用。

汽车产业的产业云采用率正在上升,为企业提供了重组价值链的机会。一个着名的例子是德国汽车製造商大众汽车,它与 AWS 和保时捷旗下的 IT 顾问 MHP 合作,于 2023 年 6 月建立了专门针对汽车製造的产业云。云端采用的成长预计将在未来几年推动对云端基础的汽车保固管理解决方案的需求。

此外,包括汽车在内的整个製造业快速采用云端服务,预计将推动采用已建立的云端基础设施的云端基础的保固管理解决方案。例如,根据内务部,日本製造企业使用云端服务的比例将从 2022 年的 71.6% 上升到 2023 年的 79.2%。

亚太地区预计将创下最高成长率

亚太地区正在推动全球汽车产业的成长,中国、印度、日本和韩国等国家的汽车销售量大幅成长。这种快速成长,尤其是配备先进功能和电子设备的新型车辆,需要更复杂的保固管理和复杂的系统来处理日益复杂的保固申请。

根据国际汽车工业协会(OICA)统计,2023年包括中东在内的亚太地区乘用车销量约4,260万辆,其中中国销量超过2,600万辆。同时,2022 年亚太地区乘用车销量约 3,750 万辆。汽车销售的成长给製造商和经销商带来了维护保固记录和改善客户体验的挑战。

不断变化的客户期望和更长的保固期正在推动市场成长。该地区的消费者越来越精通技术,并要求无缝的保固体验。这包括高效的索赔处理、透明的沟通以及线上查询保固资讯。因此,汽车製造商正在推出延长保固选项以保持竞争力,从而推动对支援更长索赔期限的高级保固管理解决方案的需求。

此外,由于维修成本和零件价格上涨,汽车製造商和经销商正面临售后服务利润的压力。实施保固管理系统有助于简化流程、降低管理成本并识别诈欺索赔。因此,汽车製造商和经销商越来越注重降低成本和提高业务效率,从而越来越多地采用汽车保固管理解决方案。

汽车保固管理产业概述

汽车保固管理市场的整合程度较低,只有少数市场参与者拥有较大的市场占有率。拥有重要市场份额的领先公司正致力于透过合作、扩张和併购等策略措施扩大其全球基本客群,以获得有竞争力的市场占有率。

2024 年 6 月 - 服务生命週期管理解决方案提供商 Tavant 与北美重型卡车製造商和中型卡车和特种商用车生产商戴姆勒卡车北美有限责任公司合作,共同改善客户体验和经销商生产力。建立合作伙伴关係,以改造戴姆勒卡车的服务业务。此次合作是戴姆勒卡车集团与 Tavant 长期全球技术合作关係的延伸。

其他好处

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买家/消费者的议价能力

- 新进入者的威胁

- 竞争公司之间的敌对关係

- 替代品的威胁

- 产业相关人员分析

- 宏观经济趋势的影响(经济衰退、俄罗斯-乌克兰战争等)

第五章市场动态

- 市场驱动因素

- 引进人工智慧、机器学习、物联网和巨量资料等技术

- 市场整合与订阅模式

- 保险申请管理自动化和节省时间的需求日益增加

- 市场挑战

- 资料和身份盗窃/资料洩露

第六章 市场细分

- 按服务

- 软体

- 服务

- 按配置

- 本地

- 云端基础

- 按组织规模

- 中小企业 (SME)

- 大公司

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东/非洲

第七章 竞争格局

- 公司简介

- Oracle Corporation

- PTC Inc.

- Wipro Limited

- Appian Corporation

- Pegasystems Inc.

- MSX International

- Annata

- SKYLYZE

- IFS Americas Inc.

- SYNCRON HOLDING AB

第八章投资分析

第九章 市场未来展望

The Automotive Warranty Management Market size is estimated at USD 2.58 billion in 2024, and is expected to reach USD 4.86 billion by 2029, growing at a CAGR of 13.47% during the forecast period (2024-2029).

The growing production in the automotive sector is a significant factor driving the market, as the automotive and supply chain industries account for the largest share in the adoption of warranty software. Moreover, the consumer propensity toward adopting connected vehicles is also expected to influence the global demand for automobiles, thereby driving the market.

Nowadays, the primary focus of OEMs when it comes to warranty management is compliance with their policies and procedures, ensuring repairs are performed as prescribed and maintaining the quality and reliability of their vehicles. However, achieving cost savings is equally important for them. Thus, the adoption of warranty management solutions among OEMs is growing to improve profitability, enhance customer satisfaction, and remain competitive.

Automotive companies are constantly striving to boost product quality, aiming to reduce warranty costs, elevate customer satisfaction, and bolster financial performance. However, the quality is frequently hampered by factors like surging new product demands, heightened competition, technological advancements, and disruptions in the supply chain. On average, automotive and industrial firms witness warranty claims expenses between 1.5-2.5% of their annual revenue, translating to significant revenue losses and poor customer satisfaction. Companies frequently expedite warranty services and part replacements to mitigate these challenges to uphold customer loyalty. Given these challenges, it becomes imperative for automakers to integrate technologies like artificial intelligence (AI) and machine learning (ML) into their traditional warranty management systems.

In response, some market players are introducing AI- and ML-based solutions. For instance, in August 2023, FrogData, a software company based in California that offers artificial intelligence and decision analytics solutions to the automotive industry, introduced WarrantyMind AI, an end-to-end remote warranty administration service designed to optimize the warranty claims process for dealerships.

However, as these solutions handle sensitive customer and vehicle data, security breaches become essential to brand reputation and customer trust. Thus, data and identity theft challenges are hampering market growth, necessitating investment in cybersecurity measures to protect data.

The global automotive warranty management market faced challenges as well as opportunities amid the COVID-19 pandemic. Lockdowns and supply chain disruptions led to a shortage of parts and delays in repair, creating a backlog of warranty claims that strained warranty management systems. Moreover, the crisis underscored the value of data-driven decisions, highlighting the demand for automotive warranty systems equipped with data analytics capabilities to identify trends and enhance service center efficiency.

Automotive Warranty Management Market Trends

Cloud-based Warranty Management Systems is Expected to Drive Market Growth Significantly

As a result of the COVID-19 pandemic, the cloud-based warranty management solutions facilitated remote work and ensured continued access to data for warranty teams during lockdowns. This trend toward cloud adoption is expected to continue post-pandemic, driving the adoption of cloud-based warranty management solutions in the automotive industry.

The growing adoption of the cloud in the automotive industry, owing to several benefits such as scalability, reduced costs, and improved collaboration between globally located teams, designers, and manufacturing units to access and share data in real time, is driving innovation and faster product development cycles. Such advantages are further expected to drive the adoption of cloud-based warranty management solutions.

The adoption of industry cloud in the automotive sector is on the rise, offering enterprises an opportunity to reconstruct their value chains. A notable example is Volkswagen, the German automaker that collaborated with AWS and MHP, an IT consultant under Porsche, to establish its industry cloud tailored for automobile manufacturing in June 2023. These advancements in cloud adoption are anticipated to drive the demand for cloud-based automotive warranty management solutions in the coming years.

Furthermore, the rapidly growing adoption of cloud services across the manufacturing industries, including automotive, is expected to support the adoption of cloud-based warranty management solutions with established cloud infrastructure. For instance, according to the Ministry of Internal Affairs and Communications Japan, the share of manufacturing companies in Japan that use cloud services reached 79.2% in 2023 from 71.6% in 2022.

Asia-Pacific is Expected to Register the Highest Growth Rate

Asia-Pacific leads the global automobile industry in growth, driven by countries such as China, India, Japan, and South Korea, witnessing a significant surge in vehicle sales. This surge has resulted in a larger pool of vehicles, particularly modern cars equipped with advanced features and electronics, necessitating more intricate warranty management and sophisticated systems to handle the rising complexity of warranty claims.

According to the International Organization of Motor Vehicle Manufacturers (OICA), in 2023, about 42.6 million passenger cars were sold within Asia-Pacific, including the Middle East, of which over 26 million were sold in China. Comparatively, approximately 37.5 million passenger cars were sold in Asia-Pacific in 2022. This rise in vehicle sales challenges manufacturers and dealers to maintain warranty records and enhance customer experience.

Evolving customer expectations and longer warranty durations are bolstering market growth. Consumers in the region are becoming increasingly tech-savvy, so they now demand a seamless warranty experience. This includes efficient claim processing, transparent communication, and online access to warranty information. Consequently, automakers are rolling out extended warranty options to stay competitive, driving the demand for advanced warranty management solutions to handle these longer claim lifespans.

In addition, automakers and dealers are experiencing pressure on after-sales margins due to rising repair costs and parts prices. Implementing warranty management systems is helping them streamline processes, reduce administrative costs, and identify fraudulent claims. Thus, automakers and dealers are increasingly focusing on cost reduction and operational efficiency, leading to increased adoption of automotive warranty management solutions.

Automotive Warranty Management Industry Overview

The automotive warranty management market is moderately consolidated, with few market players holding significant market share. The major players with prominent shares in the market are focusing on expanding their global customer base through strategic initiatives such as collaboration, expansion, mergers & acquisitions, and others to gain competitive market share.

June 2024 - Tavant, a provider of Service Lifecycle Management solutions, and Daimler Truck North America LLC, the heavy-duty truck manufacturer in North America and a producer of medium-duty trucks and specialized commercial vehicles, formed a partnership to transform Daimler Truck's service operations to enhance customer experience and dealer productivity. This partnership marks the expansion of a longer global technology partnership between Daimler Truck Group and Tavant.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHT

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers/Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Intensity of Competitive Rivalry

- 4.2.5 Threat of Substitute Products

- 4.3 Industry Stakeholder Analysis

- 4.4 Impact of Macroeconomic Trends (Recession, Russia-Ukraine war, etc.)

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Implementation of Technologies Such as AI, ML, IoT and Big Data

- 5.1.2 Market Consolidation and Subscription-based Model

- 5.1.3 Rising Automation and Need for Hassle-free Claim Management

- 5.2 Market Challenges

- 5.2.1 Data and Identity Theft/Data Breaches

6 MARKET SEGMENTATION

- 6.1 By Offering

- 6.1.1 Software

- 6.1.2 Services

- 6.2 By Deployment

- 6.2.1 On Premise

- 6.2.2 Cloud-based

- 6.3 By Organization Size

- 6.3.1 Small and Medium Enterprises (SMEs)

- 6.3.2 Large Enterprises

- 6.4 By Geography

- 6.4.1 North America

- 6.4.2 Europe

- 6.4.3 Asia-Pacific

- 6.4.4 Latin America

- 6.4.5 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Oracle Corporation

- 7.1.2 PTC Inc.

- 7.1.3 Wipro Limited

- 7.1.4 Appian Corporation

- 7.1.5 Pegasystems Inc.

- 7.1.6 MSX International

- 7.1.7 Annata

- 7.1.8 SKYLYZE

- 7.1.9 IFS Americas Inc.

- 7.1.10 SYNCRON HOLDING AB

8 INVESTMENT ANALYSIS

9 FUTURE OUTLOOK OF THE MARKET

2026年全球房屋保固服务市场报告

2026年全球房屋保固服务市场报告 保固管理系统市场 - 全球产业规模、份额、趋势、机会及预测(按解决方案、应用、地区和竞争格局划分,2021-2031年)家庭保固服务市场-全球产业规模、份额、趋势、机会和预测:按承保类型、物业类型、服务提供者、地区和竞争格局划分,2021-2031年

保固管理系统市场 - 全球产业规模、份额、趋势、机会及预测(按解决方案、应用、地区和竞争格局划分,2021-2031年)家庭保固服务市场-全球产业规模、份额、趋势、机会和预测:按承保类型、物业类型、服务提供者、地区和竞争格局划分,2021-2031年 全球汽车保固管理市场全球住宅保固服务市场:2034 年之前的市场机会与策略

全球汽车保固管理市场全球住宅保固服务市场:2034 年之前的市场机会与策略 欧洲保固管理系统:市场占有率分析、行业趋势和统计数据、成长预测(2025-2030 年)

欧洲保固管理系统:市场占有率分析、行业趋势和统计数据、成长预测(2025-2030 年) 保固管理系统市场(按解决方案、应用和区域划分)保固管理系统:市场占有率分析、产业趋势/统计、成长预测(2025-2030)

保固管理系统市场(按解决方案、应用和区域划分)保固管理系统:市场占有率分析、产业趋势/统计、成长预测(2025-2030)