|

市场调查报告书

商品编码

1630205

保固管理系统:市场占有率分析、产业趋势/统计、成长预测(2025-2030)Warranty Management System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

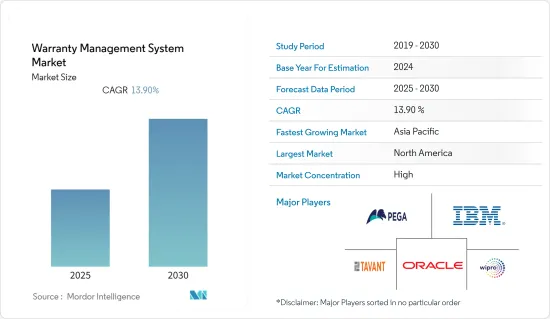

保固管理系统市场预计在预测期内复合年增长率为 13.9%。

主要亮点

- 保固管理系统透过自动化保固索赔处理和装置量资产跟踪,帮助服务提供者在整个生命週期中设计、管理、跟踪和处理保固、索赔和资产。创新的保固管理系统 (WMS) 与人工智慧和机器学习功能相结合,确保客户满意度。

- 透过保固索赔处理和装置量资产追踪的自动化,保固管理解决方案主要使服务组织能够在整个生命週期中建立、管理、追踪和处理保固、索赔和资产。

- 因此,第三方可以提交有效的索赔并获得积分。此外,客户服务可以审查保固并启动恢復,现场技术人员可以追踪资产历史记录并更换保固期内的零件。这些解决方案最大限度地降低保固成本、自动化保固索赔、简化保固管理系统并最大限度地提高业务收益。该软体使所有相关人员受益,包括製造商、服务提供者、供应商、经销商和最终用户。因此,它们在世界各地的各个最终用户产业中都有很大的需求。

- 现代保固管理系统 (WMS) 融合了先进技术、机器学习 (ML) 和人工智慧 (AI) 功能,可提高客户满意度。因此,由于人工智慧和机器学习的发展,保固生命週期管理系统在评估期间显示出强劲的成长。基于人工智慧的系统采用影像识别来快速、经济地识别诈欺索赔。机器学习演算法经过数万张照片的训练,可以从 Photoshop 图像和旧投诉中识别出真正的问题。

- 汽车产业的产量扩张是推动市场成长的关键因素,因为汽车和供应链产业在保固软体的采用中占据最大份额。此外,消费者采用连网汽车的趋势也预计将影响全球汽车需求并推动市场。

- COVID-19 大流行严重影响了保固管理系统市场的成长,因为许多国家的製造业务暂时停止以遏制病毒。结果,消费性电子产品的产量减少,而市场对保固管理系统的需求增加。然而,随着新冠肺炎 (COVID-19) 的爆发,整个全部区域向自动化技术的转变变得明显。上述巨大的采用优势正在吸引客户广泛采用由人工智慧和机器学习驱动的自动化保固管理系统,从而促进市场成长。

保固管理系统的市场趋势

云端业务预计将占据很大份额

- 在云端上实施保固管理系统可提供高扩充性、灵活性以及具有定义权限的共用功能。公司正在利用这个机会渗透市场,并分析市场在预测期内会扩大。

- 构成物联网 (IoT) 的连接/智慧型装置和感测器的激增,以及各种机器对机器 (M2M)通讯网路产生的元资料量,正在使保固索赔流程智慧更新和它有潜力为製造商提供交付客户体验所需的新层次的洞察力。

- 随着工业 4.0 和物联网 (IIoT) 等概念推动全球製造业的进步,服务供应商在预测期内拥有巨大的业务扩展机会。製造业中各种技术的融合,例如预测分析、巨量资料、云端运算、数位双胞胎和智慧工厂,也可能推动云端基础的保固管理系统的采用。

- 云端基础的物联网平台可让您根据收集的资料采取行动,包括预测建模、模拟、测试假设和彙报。该行业的领先企业正在提供云端基础的解决方案,这可能会促进预测期内的市场成长。

- 此外,公司正在积极投资各行业的云端运算,预计这将对预测期内的市场成长产生积极影响。例如,根据Platform9的报告,到2022年,单一公共云端(32.1%)、混合云端(29.8%)和本地云(14.1%)将成为企业运行工作负载的主要环境。

北美占有很大的市场份额

- 就大规模最终用户采用保固管理系统而言,北美是领先市场之一。由于中小型企业资料安全意识的增强,该地区也正在经历健康成长。此外,该地区主要市场供应商的存在和持续的技术创新正在增加对保固管理系统的需求。

- 该地区保固管理系统市场成长的主要趋势包括智慧型设备的兴起和智慧住宅的采用增加,包括音讯和视讯设备、穿戴式装置和智慧家庭设备,预计将促进保固管理的采用提供客户体验的解决方案。

- 因此,数位服务和技术进步的激增,加上云端运算、人工智慧、物联网和机器学习等新兴技术在各个领域的早期采用,正在补充该地区的市场成长。该地区的保固管理公司还在整个保固流程中利用资料分析和人工智慧,透过识别缺陷模式、改善索赔审查和端到端管理供应商扣回争议帐款来提高产品品质。

- 此外,该地区还在保固管理系统方面进行了大量投资和技术进步。零售业保固管理系统的引进也在取得进展。有组织的零售业正在发生巨大转变,透过分析应用来改善客户的行为体验。

保固管理系统产业概况

保固管理系统市场适度整合,少数市场参与者占了重要的市场占有率。在这个市场上拥有大量份额的主要公司正在专注于扩大海外基本客群。公司正在利用战略合作计划来增加市场占有率和盈利。

2022 年 11 月,数位产品和解决方案公司、服务生命週期管理的全球领导者之一 Tabant 将与全球最大的商用车製造商之一戴姆勒卡车股份公司 (DTAG) 合作开发其欧洲品牌。它将提供保固和索赔管理解决方案

2022 年 5 月,Opteven 将透过为 WMS 经销商和维修商创建一个高度可访问且市场领先的线上索赔平台,推动 WMS Group (UK) Ltd (WMS) 雄心勃勃的业务转型和转型策略。该平台旨在大幅简化和加快保固索赔流程。新平台减少了管理时间,同时提供全面且卓越的客户服务体验。

其他好处

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买家/消费者的议价能力

- 新进入者的威胁

- 竞争公司之间的敌对关係

- 替代品的威胁

- COVID-19 市场影响评估

第五章市场动态

- 市场驱动因素

- 製造和汽车行业越来越多地采用保固管理系统

- 在下一代保固管理系统中更多地采用人工智慧和机器学习功能,以确保客户满意度

- 市场限制因素

- 价格敏感市场中独立服务供应商之间的激烈竞争

第六章 市场细分

- 依部署类型

- 本地

- 云

- 依软体类型

- 保障情报

- 理赔管理

- 服务合约

- 合约管理

- 按成分

- 解决方案

- 服务(专业服务、主机服务)

- 按最终用户产业

- 工业设备(重型机械/机器)

- 汽车/运输设备

- 耐用消费品(主要住宅设备、空调系统)

- 建筑/建筑材料

- 其他最终用户产业(医疗设备、航太和国防等)

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 世界其他地区

第七章 竞争格局

- 公司简介

- Pegasystems Inc.

- Oracle Corporation

- Wipro Limited

- IBM Corporation

- Tavant

- Tech Mahindra Limited

- Evia Information Systems Pvt Ltd

- PTC Inc.

- IFS Americas Inc.

- Syncron AB

第八章投资分析

第9章市场的未来

The Warranty Management System Market is expected to register a CAGR of 13.9% during the forecast period.

Key Highlights

- The warranty management system helps service businesses to design, administer, track, and process warranties, claims, and assets through their lifecycles through the automation of warranty claim handling and installed base asset tracking. Innovative warranty management systems (WMS) are linked with AI and machine learning capabilities to guarantee customer satisfaction.

- Through the automation of warranty claim handling and installed base asset tracking, warranty management solutions primarily enable service organizations to create, administer, track, and process warranties, claims, and assets through their full lifecycles.

- As a result, third parties can submit their valid claims and receive credits. Customer service can also verify the coverage and initiate recovery, and field technicians can track asset history and replace the in-warranty parts. These solutions reduce the warranty cost to a minimum, automate warranty claims, streamline the warranty management system, and increase service revenue to the maximum. This software benefits all stakeholders, including manufacturers, service providers, suppliers, dealers, and end-users. This has resulted in significant demand in various end-user industries across the world.

- Modern warranty management systems (WMS) incorporate advanced technologies, machine learning (ML), and artificial intelligence (AI) capabilities to enhance customer satisfaction. As a result, warranty lifecycle management systems have shown strong growth during the assessment period because of AI and ML developments. AI-based systems employ image recognition to quickly and economically identify fraudulent claims. Machine learning algorithms are trained using tens of thousands of photographs, and they can identify actual problems with photoshopped images or old claims.

- The growing production in the automotive sector is a significant factor driving the market growth, as the automotive and supply chain industries account for the largest share in the adoption of warranty software. Moreover, the consumer propensity toward adopting connected vehicles is also expected to influence the global demand for automobiles, thereby driving the market.

- The COVID-19 pandemic significantly impacted the growth of the warranty management system market as manufacturing operations were temporarily suspended across many countries to contain the virus. This increased the need for more warranty management systems in the market, caused by less production of consumer electronic devices. However, with COVID-19, the shift toward automated technologies was significant across the region. The considerable advantages of the adoption mentioned above are luring the customers into the broad adoption of automated warranty management systems with AI and ML and contributing to the market growth.

Warranty Management System Market Trends

Cloud Segment is Expected to Hold Significant Share

- Implementing a warranty management system on the cloud provides a high intensity of scalability, flexibility, and sharing capabilities with defined authority. The players are leveraging this opportunity to penetrate the market further, which is analyzed to proliferate the market over the forecast period.

- The proliferation of connected/smart devices and sensors that comprise the Internet of Things (IoT), as well as the amounts of metadata generated by different machine-to-machine (M2M) communications networks, may offer manufacturers a new level of insight needed to intelligently update the warranty claims process and deliver a seamless customer experience.

- With advancements in the global manufacturing sector with Industry 4.0 and concepts, such as the Industrial Internet of Things (IIoT), the service providers have a massive opportunity to expand their business over the forecast period. The convergence of various technologies in the manufacturing sector, such as predictive analytics, Big Data, cloud computing, digital twin, and smart factories, may also drive the adoption of cloud-based warranty management systems.

- The cloud-based IoT platform enables actions to be taken from the collected data, such as predictive modeling, simulation, test hypothesis, and reporting. The leading industry players are offering cloud-based solutions that could boost market growth over the forecast period.

- In addition, organizations actively invest in cloud computing across various industries, which is expected to positively impact market growth over the forecast period. For instance, according to the Platform9 report, in 2022, single public (32.1%), hybrid (29.8%), and on-premises clouds (14.1%) were organizations' dominant environments to run their workloads.

North America to Hold Significant Share in the Market

- North America is one of the leading markets in terms of adopting warranty management systems across significant end users. The region is also witnessing healthy growth due to the rising acceptance of data security among small- and medium-scale firms. In addition, the presence of major market vendors in the region and continuous innovation in their market offerings resulted in the growing demand for warranty management systems in the region.

- The major trends that are responsible for the growth of the warranty management system market in the region include the growing number of smart devices and the increase in the adoption of intelligent residential devices, which contain audio and video devices, as well as wearables and smart home devices, which creates the adoption of a warranty management solution to provide the best customer experience.

- Therefore, the proliferation of digital services and technological advancements, coupled with the early adoption of the latest technologies such as cloud computing, AI, IoT, and ML in various sectors, supplement the market growth in the region. Warranty management companies in the region are also using data analytics and AI throughout their warranty procedures to improve product quality by identifying defect patterns, improving claims screening, and end-to-end control of supplier chargebacks.

- In addition, the region is also experiencing many investments and technological advancements in warranty management systems. The adoption of a warranty management system in retail space is also emerging. There is a vast shift to organized retail to improve customer behavior experience through analytics applications.

Warranty Management System Industry Overview

The warranty management systems market is moderately consolidated, with few market players holding significant market share. The major players with prominent shares in the market are focusing on expanding their customer base across foreign countries. The companies are leveraging strategic collaborative initiatives to increase their market shares and profitability.

In November 2022, Tavant, a digital products and solutions company and one of the global leaders in service lifecycle management, announced that it partnered with Daimler Truck AG (DTAG), one of the world's largest commercial vehicle manufacturers, to provide warranty and claim management solutions for its European brands.

In May 2022, driving forward with its ambitious business transformation and change strategy for WMS Group (UK) Ltd (WMS), Opteven introduced its highly accessible and market-leading online claims platform for WMS dealers and repairers. It is designed to significantly simplify and speed up the process of making warranty claims. The new platform will reduce administration time while offering a comprehensive and exceptional customer service experience.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers/Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Intensity of Competitive Rivalry

- 4.2.5 Threat of Substitute Products

- 4.3 Assessment of the COVID-19 Impact on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rising Adoption of Warranty Management System in the Manufacturing and Automotive Industries

- 5.1.2 Increasing Adoption of AI and ML Capabilities in Next-generation Warranty Management Systems to Ensure Customer Satisfaction

- 5.2 Market Restraints

- 5.2.1 Intense Competition Between Independent Service Providers in Price- sensitive Markets

6 MARKET SEGMENTATION

- 6.1 By Deployment Type

- 6.1.1 On-premise

- 6.1.2 Cloud

- 6.2 By Software Type

- 6.2.1 Warranty Intelligence

- 6.2.2 Claim Management

- 6.2.3 Service Contract

- 6.2.4 Administration Management

- 6.3 By Component

- 6.3.1 Solutions

- 6.3.2 Services (Professional and Managed Services)

- 6.4 By End-user Industry

- 6.4.1 Industrial Equipment (Heavy Equipment and Machinery)

- 6.4.2 Automotive and Transportation

- 6.4.3 Consumer Durable (Major Residential Appliances and HVAC Systems)

- 6.4.4 Construction/Building Materials

- 6.4.5 Other End-user Industries (Medical Devices, Aerospace and Defense, etc.)

- 6.5 Geography

- 6.5.1 North America

- 6.5.2 Europe

- 6.5.3 Asia-Pacific

- 6.5.4 Rest of the World

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Pegasystems Inc.

- 7.1.2 Oracle Corporation

- 7.1.3 Wipro Limited

- 7.1.4 IBM Corporation

- 7.1.5 Tavant

- 7.1.6 Tech Mahindra Limited

- 7.1.7 Evia Information Systems Pvt Ltd

- 7.1.8 PTC Inc.

- 7.1.9 IFS Americas Inc.

- 7.1.10 Syncron AB

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

2026年全球房屋保固服务市场报告

2026年全球房屋保固服务市场报告 保固管理系统市场 - 全球产业规模、份额、趋势、机会及预测(按解决方案、应用、地区和竞争格局划分,2021-2031年)家庭保固服务市场-全球产业规模、份额、趋势、机会和预测:按承保类型、物业类型、服务提供者、地区和竞争格局划分,2021-2031年

保固管理系统市场 - 全球产业规模、份额、趋势、机会及预测(按解决方案、应用、地区和竞争格局划分,2021-2031年)家庭保固服务市场-全球产业规模、份额、趋势、机会和预测:按承保类型、物业类型、服务提供者、地区和竞争格局划分,2021-2031年 全球汽车保固管理市场全球住宅保固服务市场:2034 年之前的市场机会与策略

全球汽车保固管理市场全球住宅保固服务市场:2034 年之前的市场机会与策略 欧洲保固管理系统:市场占有率分析、行业趋势和统计数据、成长预测(2025-2030 年)

欧洲保固管理系统:市场占有率分析、行业趋势和统计数据、成长预测(2025-2030 年) 保固管理系统市场(按解决方案、应用和区域划分)汽车保固管理:市场占有率分析、产业趋势/统计、成长预测(2024-2029)

保固管理系统市场(按解决方案、应用和区域划分)汽车保固管理:市场占有率分析、产业趋势/统计、成长预测(2024-2029)