|

市场调查报告书

商品编码

1630280

全球 MEMS 封装 -市场占有率分析、产业趋势/统计、成长预测(2025-2030 年)Global MEMS Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

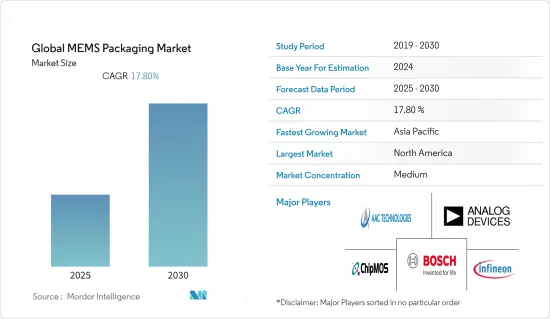

全球MEMS封装市场预计在预测期间内复合年增长率为17.8%

主要亮点

- 随着MEMS元件的应用范围显着扩大,MEMS封装已从MEMS元件封装发展到MEMS系统封装。创新和高效的包装技术变得越来越重要,新的包装材料也是如此。

- CMOS 相容的 MEMS 製造流程(例如低温晶圆键合技术和其他单晶片整合)的最新技术发展正在推动 MEMS 封装市场的创新。另一个新兴趋势是将裸晶圆堆迭应用于低成本无铅半导体封装。这使得低成本的小引脚封装能够用于大量生产。

- MEMS 的日益普及也促进了嵌入式晶片封装市场的新需求。儘管该技术并非该市场独有,但由于高成本、产量比率低,已多元化至利基应用,但未来发展潜力巨大。蓝牙和射频模组的进步以及 WiFi-6 的兴起预计将进一步加速对该技术的投资。

- MEMS 设备的日益普及也鼓励 MEMS 封装供应商进一步开发创新封装技术,以提高这些设备的效率和运作效能。例如,主要企业T-SMART于2021年宣布,正致力于针对热电堆感测器采用异构整合的新型MEMS封装技术。

- 此外,根据 IEEE 的说法,由于 MEMS 装置的多样性以及需要同时暴露和保护许多装置免受环境影响,MEMS 封装比IC封装更具挑战性。此外,MEMS 封装还存在一些挑战,例如晶粒处理、晶粒附着、界面张力和排气。这些新的 MEMS 封装挑战需要紧急的研究和开发工作。

- 随着世界各地的科技公司在对抗 COVID-19 大流行的过程中加速创新,MEMS 在晶片行业的使用经历了巨大的增长。对微型设备的需求正在推动电子技术的进步,从更快的热感成像和就地检验到基于微流体的聚合酵素链锁反应(PCR) 工具和 SARS-CoV-2 检测技术。然而,疫情改变了人们对全球製造业供应链的看法,我们现在看到更多的在地化价值链和本土化。

MEMS封装市场趋势

智慧型手机和连网型设备的普及预计将推动需求

- 全球智慧型手机用户数量正在显着增加。消费者正在转向智慧型手机来存取其提供的各种功能,包括连接、付款、游戏、摄影、GPS 等。智慧型手机用户的增加预计将对所研究市场的成长产生积极影响,因为智慧型手机硬体中整合了多个感测器以实现此类功能。

- 根据爱立信行动报告,印度智慧型手机用户数量预计将从2020年的8.1亿增加到2026年的12亿。农村地区正在推动连网行动电话的销售,随着网路连线的日益普及,对智慧型手机的需求预计也会增加。

- 此外,MEMS 装置也正在彻底改变消费性电子市场。透过结合所有智慧型手机和平板电脑中的 MEMS 麦克风和 CMOS 影像感测器,家用电子电器製造商正在将传统设备转变为可以透过智慧型手机轻鬆远端控制的连接设备。

- 健康意识的提高,尤其是在 COVID-19 爆发之后,正在推动使用感测器追踪用户生物识别资料的连网型穿戴式装置设备市场的发展。由于 MEMS 装置在这些装置中发挥重要作用,因此不断增长的需求预计将对研究市场产生积极影响。例如,根据思科系统公司的预测,到 2022 年,全球穿戴式装置的总数预计将达到 11 亿台。

北美占据主要市场占有率

- 北美地区传统上是全球电子产业的主要股东,因其研发能力强,拥有英特尔、戴尔等主要半导体和高科技公司,以及电子设备、物联网和先进技术的存在。高渗透率。例如,该地区被认为是采用 ADAS 车辆和自动交通解决方案的先驱之一。德意志银行预计,到2021年,美国ADAS汽车产量预计将成长至1,845万辆。

- 汽车製造商越来越多地采用 MEMS 装置来为其车辆添加独特的功能。例如,基于MEMS的雷射雷达已经取代了自动驾驶/无人驾驶汽车、工业机器人、无人机等。 2021 年 9 月,通用汽车选择 Cepton 供应基于 MEME 的雷射雷达,用于 2023 年的生产。通用汽车将使用 Cepton LiDAR 为自动紧急煞车和行人侦测等 ADAS 功能提供支持,以支援其即将推出的 Ultra Cruise 系统。

- 这些公司也专注于最新的感测器创新,并因其创新产品而受到认可。例如,2022 年 4 月,北美和全球半导体组装和测试服务供应商Unisem 凭藉其 MEMS 腔体封装在 MEMS 和感测器技术大会 (MSTC) 上赢得了封装製程对决。

- 最近,在全球晶片短缺的情况下,当地半导体产业的提振正迫使北美地区政府增加对半导体及相关产业的投资。例如,加拿大政府承诺在2022年初投资2.4亿美元,与当地研究人员和公司合作,进一步加强加拿大在半导体产业的地位。预计此类案例将为所研究市场的成长创造有利的市场情景。

- 此外,智慧型手机和家用电子电器产品也是推动MEMS装置需求的关键产业之一,这反过来又对该地区的封装服务需求产生正面影响。例如,根据消费者技术协会(CTA)的数据,预计2021年美国5G智慧型手机出货量将达到1.06亿支。

MEMS封装产业概况

MEMS封装市场竞争温和。由于该行业是资本密集型行业,市场上领先的供应商因其多样化的产品系列和产品开发而具有优势。供应商的创新能力很大程度取决于其研发投入。此外,该行业的资本密集性质对新进入者构成了进入障碍。该市场的主要企业包括 ChipMos Technologies Inc.、AAC Technologies、Bosch Sensortec GmbH、Infineon Technologies AG 和 Analog Devices, Inc.。

- 2022 年 8 月 - 领先的 MEMS 技术解决方案供应商美新 (MEMSIC) 发布首款 MEMS 6 轴惯性感测器 (IMU) MIC6100HG。该产品整合了三轴加速器和3轴陀螺仪,可支援具有高灵敏度感测的体感互动系统,例如智慧遥控器和游戏控制器。此外,MIC6100HG 6轴IMU感测器配备大容量FIFO,支援I2C/I3C/SPI通讯模式。 LGA封装尺寸为2.5x3x0.83mm,资料输出频率为2,200Hz。

- 2022 年 2 月-义法半导体宣布推出第三代 MEMS 感测器。该公司表示,这款新型感测器旨在实现智慧工业、消费行动、医疗和零售领域性能和功能的下一次飞跃。新推出的 LPS22DF 和防水 LPS28DFW 气压感知器的工作电流为 1.7μA,绝对压力精度为 0.5hPa,并且采用最小的封装之一 (2.0 x 2.0 x 0.74mm)。

其他好处

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买方议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间的敌对关係

- 技术简介

- COVID-19 市场影响评估

第五章市场动态

- 市场驱动因素

- 不断成长的智慧汽车市场

- 智慧型手机普及率和连网型设备的增加

- 感测器在工业上的应用

- 市场限制因素

- 复杂的製造工艺

第六章 市场细分

- 依感测器类型

- 惯性感测器

- 光学感测器

- 环境感测器

- 超音波感测器

- RF MEMS

- 其他的

- 按最终用户

- 车

- 行动电话

- 家用电子电器

- 医疗系统

- 工业的

- 其他的

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 其他的

第七章 竞争格局

- 公司简介

- ChipMos Technologies Inc.

- AAC Technologies Holdings Inc.

- Bosch Sensortec GmbH

- Infineon Technologies AG

- Analog Devices, Inc.

- Texas Instruments Incorporated.

- Taiwan Semiconductor Manufacturing Company Limited

- MEMSCAP SA

- Orbotech Ltd.

- TDK Corporation

- MEMSIC Semiconductor Co., Ltd

- STMicroelectronics

第八章投资分析

第九章 市场未来展望

The Global MEMS Packaging Market is expected to register a CAGR of 17.8% during the forecast period.

Key Highlights

- MEMS packaging has evolved from packaging MEMS devices to packaging MEMS systems as the application of MEMS devices has expanded significantly. Innovative and efficient packaging technology is becoming increasingly important, as are new packaging materials.

- The recent technological development of CMOS-compatible MEMS manufacturing processes for low-temperature wafer bonding and other single-chip integration are among the driving innovations in the MEMS packaging market. Another emerging trend is the application of bare wafer stacks for low-cost lead-free semiconductor packages. This enables a low-cost, small-pin package for high-volume production.

- The increasing adoption of MEMS is also contributing to new demand in the embedded die packaging market. The technology is not unique to the market, but its high cost and low yields have diversified it into niche applications, but the potential for future development is immense. Advancements in Bluetooth and RF modules and the rise of WiFi-6 will likely accelerate investment in this technology further.

- The growing adoption of MEMS devices is also encouraging the MEMS packaging vendors to develop innovative packaging techniques further to enhance these devices' efficiency and operational performances. For instance, in 2021, T-SMART, a leading semiconductor manufacturing company, announced that it is working towards a new MEMS packaging technology based on Heterogeneous Integration for the thermopile sensor.

- Furthermore, according to IEEE, MEMS packaging is more challenging than IC packaging due to the diversity of MEMS devices and the need for many devices to be in contact with and protected from the environment simultaneously. In addition, there are also challenges within MEMS packaging, such as die handling, die attachment, interfacial tension, and outgassing. These new MEMS packaging challenges require urgent R&D efforts.

- The usage of MEMS in the chip industry has witnessed immense growth as technology companies around the world accelerated innovation in the fight against the COVID-19 pandemic. The need for tiny devices drives advances in electronics, ranging from thermal imaging and faster point-of-care testing to microfluidics-based polymerase chain reaction (PCR) tools and techniques to detect SARS-CoV-2. However, the pandemic has changed the perception of the global supply chain in manufacturing, where more localized value chains and regionalization have come into the picture.

MEMS Packaging Market Trends

Growing Adoption of Smartphones and Connected Devices is Expected to Drive the Demand

- The number of smartphone users is rising enormously worldwide. Consumers are switching to smartphones to access various functionality they offer, including connectivity, payment, gaming, photography, and GPS. As multiple sensors are integrated into the smartphone's hardware to enable such functionality, the growing number of smartphone users is expected to positively impact the studied market growth.

- According to Ericsson Mobility Report, smartphone subscription in India is expected to grow from 810 million in 2020 to 1.2 billion in 2026. With rural areas driving the sale of internet-enabled phones, demand for smartphones is expected to increase as Internet connectivity spreads further.

- Moreover, MEMS devices are also revolutionizing the consumer electronics market. Combining the MEMS microphones and CMOS image sensors found in all smartphones and tablets, the consumer electronic device manufacturing companies are turning the traditional devices into connected ones that can easily be remotely controlled through smartphones.

- The increasing health consciousness, especially after the outbreak of COVID-19, drives the market for connected wearable devices that use sensors to track users' biological data. As MEMS devices play an integral role in these devices, the increasing demand is expected to impact the studied market positively. For instance, according to CISCO Systems, the total number of wearable devices is expected to reach 1.1 billion globally by 2022.

North America to Hold Significant Market Share

- The North American region traditionally has been a major shareholder of the global electronics industry owing to factors such as higher R&D capabilities, the presence of some of the biggest semiconductor and tech companies such as Intel, Dell, etc., along with higher penetration of electronic devices, IoT, and advanced automotive technologies. For instance, the region is considered one of the pioneers in adopting ADAS-enabled vehicles and autonomous transportation solutions. According to Deutsche Bank, ADAS vehicle production in the US is expected to grow to 18.45 million by 2021.

- Automotive companies are increasingly adopting MEMS devices to add unique functionality to their vehicles. For instance, MEMS-based LiDARs were an alternative to autonomous/driverless cars, industrial robots, UAVs, etc.; in September 2021, General Motors selected Cepton for the supply of MEME-based LiDAR for 2023 production. General Motor is expected to use the Cepton LiDAR to enhance ADAS capabilities for automatic emergency braking and pedestrian detection and to enable its upcoming Ultra Cruise system.

- Companies are also focused on innovating the latest sensors and are receiving recognition for their innovative products. For instance, in April 2022, Unisem, a North American and global semiconductor assembly and test services provider, won the Packaging Process Showdown at MEMS and SENSORS Technical Congress (MSTC) for its presentation, MEMS Cavity Packages.

- The recent push to the local semiconductor industry amid the global chip shortage has forced the governments in the North American region to increase their investment in the semiconductor and related industries. For instance, through a USD 240 million investment in early 2022, the government Canadian government has committed to work with local researchers and companies to strengthen Canada's position in the industryfurther. Such instances are expected to create a favorable market scenario for the growth of the studied market.

- Furthermore, the smartphone and consumer electronics also are among the leading industries driving the demand for MEMS devices which n turn is positively impacting the demand for packaging services in the region. For instance, according to the Consumer Technology Association (CTA), the 5G smartphone shipments in the United States was expected to reach 106 million in 2021.

MEMS Packaging Industry Overview

The MEMS packaging market is moderately competitive. As the industry is capital intensive, major vendors in the market are banking on diverse product portfolios and product development to gain an edge. The innovation capabilities of the vendors are highly dependent on their R&D investments. Additionally, the industry's capital-intensive nature poses an entry barrier to new entrants. Some key players operating in the market are ChipMos Technologies Inc., AAC Technologies, Bosch Sensortec GmbH, Infineon Technologies AG, and Analog Devices, Inc., among others.

- August 2022 - MEMSIC, a leading MEMS technology solution provider, releases the first MEMS 6-axis inertial sensor (IMU) MIC6100HG. The product integrates a 3-axis accelerometer and a 3-axis gyroscope, which can support motion-sensing interactive systems such as smart remote controls and game controllers with sensitive sensing. Additionally, the MIC6100HG 6-axis IMU sensor has a large FIFO and supports I2C/I3C/SPI communication mode. The LGA package size is 2.5x3x0.83mm, and the data output frequency is 2200Hz.

- February 2022 - STMicroelectronics introduced its third generation of MEMS sensors. According to the company, the new sensors are designed to enable the next leap in performance and features for smart industries, consumer mobiles, healthcare, and retail sectors. The newly launched LPS22DF and waterproof LPS28DFW barometric pressure sensors, which operate from 1.7µA and have absolute pressure accuracy of 0.5hPa and are packed in one of the smallest footprints (2.0 x 2.0 x 0.74mm).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Force Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Technology Snapshot

- 4.4 Assessment of the Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Smart Automotive Market

- 5.1.2 Increasing Smart Phone Adoption Rate & Connected Devices

- 5.1.3 Sensor Usage in Industries

- 5.2 Market Restraints

- 5.2.1 Complex Manufacturing Process

6 MARKET SEGMENTATION

- 6.1 By Sensor Type

- 6.1.1 Inertial Sensors

- 6.1.2 Optical Sensors

- 6.1.3 Environmental Sensors

- 6.1.4 Ultrasonic Sensors

- 6.1.5 RF MEMS

- 6.1.6 Others

- 6.2 By End User

- 6.2.1 Automotive

- 6.2.2 Mobile Phones

- 6.2.3 Consumer Electronics

- 6.2.4 Medical Systems

- 6.2.5 Industrial

- 6.2.6 Others

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia Pacific

- 6.3.4 Rest of the World

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 ChipMos Technologies Inc.

- 7.1.2 AAC Technologies Holdings Inc.

- 7.1.3 Bosch Sensortec GmbH

- 7.1.4 Infineon Technologies AG

- 7.1.5 Analog Devices, Inc.

- 7.1.6 Texas Instruments Incorporated.

- 7.1.7 Taiwan Semiconductor Manufacturing Company Limited

- 7.1.8 MEMSCAP S.A.

- 7.1.9 Orbotech Ltd.

- 7.1.10 TDK Corporation

- 7.1.11 MEMSIC Semiconductor Co., Ltd

- 7.1.12 STMicroelectronics

8 INVESTMENT ANALYSIS

9 FUTURE OUTLOOK OF THE MARKET

MEMS构装基板市场:全球预测至2030年(按基板类型、应用、产业和地区划分)

MEMS构装基板市场:全球预测至2030年(按基板类型、应用、产业和地区划分) 半导体底部填充材料:全球市场份额和排名、总销售额和需求预测(2025-2031 年)

半导体底部填充材料:全球市场份额和排名、总销售额和需求预测(2025-2031 年) 3-D TSV:关键问题洞察与市场分析

3-D TSV:关键问题洞察与市场分析 半导体原型製作和封装市场分析及预测(至 2034 年):类型、产品、服务、技术、应用、材料类型、组件、流程、最终用户、设备

半导体原型製作和封装市场分析及预测(至 2034 年):类型、产品、服务、技术、应用、材料类型、组件、流程、最终用户、设备 高密度封装(MCM、MCP、SIP、3D-TSV):市场分析与技术趋势

高密度封装(MCM、MCP、SIP、3D-TSV):市场分析与技术趋势 3D半导体封装市场按整合类型、应用、产品类型和基板材料划分-全球预测,2025-2032年

3D半导体封装市场按整合类型、应用、产品类型和基板材料划分-全球预测,2025-2032年 全球 3D 半导体封装市场:未来预测(至 2032 年)—材料、技术、最终用户和地区分析

全球 3D 半导体封装市场:未来预测(至 2032 年)—材料、技术、最终用户和地区分析 2025年先进晶片封装全球市场报告2025年全球3D半导体封装市场报告半导体先进封装市场(按平台、材料类型、组件、间距、应用和最终用途行业)- 全球预测,2025 年至 2030 年

2025年先进晶片封装全球市场报告2025年全球3D半导体封装市场报告半导体先进封装市场(按平台、材料类型、组件、间距、应用和最终用途行业)- 全球预测,2025 年至 2030 年