|

市场调查报告书

商品编码

1630442

南美洲船用燃料:市场占有率分析、产业趋势与成长预测(2025-2030)South America Bunker Fuel - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

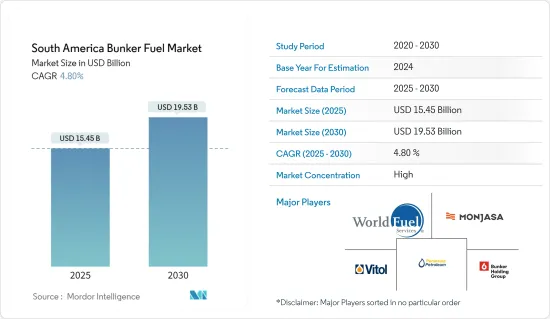

南美洲船用燃料市场规模预计到2025年为154.5亿美元,预计2030年将达到195.3亿美元,预测期内(2025-2030年)复合年增长率为4.8%。

主要亮点

- 从中期来看,关键货物海上运输的增加以及更严格的环境法规的实施推动了对清洁船用燃料的需求等因素将推动南美船用燃料市场的成长。

- 另一方面,石油市场的波动预计将对船用燃料市场产生重大影响,因为它可能会影响船用燃料供应商的盈利,并使规划和投资变得困难。

- 也就是说,越来越多地使用更清洁的船用燃料为南美船用燃料市场创造了巨大的机会。

- 由于原油产量大幅增加以及该国出口稳定成长等因素,预计巴西将主导该地区船用燃料油市场。

南美洲船用燃料油市场趋势

极低硫燃料油(VLSFO)大幅成长

- 近年来,由于国际海事组织 (IMO) 要求减少船舶硫排放,南非船用燃料油市场对浅硫燃料油 (VLSFO) 的需求大幅增加。

- 截至2023年4月,南非船用燃料油市场使用的VLSFO大部分都是进口的,使得国内船用燃料油市场的VLSFO供应尤为紧张。德班港、伊莉莎白港、开普敦港和阿尔戈亚湾(伊丽莎白港和恩古库拉附近)的海上燃料库可提供低硫燃油。

- 2022年12月至2023年4月的价格变动约为5%。相比之下,VLSFO 的价格波动更大,这进一步增加了对该燃料的需求。

- 2022 年 10 月,专门从事船用燃料行业的商品公司FUEL &MARINE OIL CORP (FAMOIL) 在秘鲁的业务中增加了一艘燃油输送船。该公司已将 Ecomar II 号油轮添加到其船队中。该船将在塔拉拉、派塔、巴伊巴鲁、萨拉伯里、钦博特皮斯科港、圣尼古拉斯、马塔拉尼和洛供应极低硫燃油(VLSFO)和高硫燃油。

- 此外,南美市场对VLSFO的需求也受到该地区营运船舶数量不断增加的推动。关于这些燃料对海洋生物的环境影响的严格监管也推动了对 VLSFO 的需求。

- 总体而言,由于国际海事组织限硫令实施后需求增加等因素,预计市场在预测期内将显着成长。

巴西主导市场

- 巴西是该地区最大的经济体,预计将成为预测期内成长最快的经济体。由于人口增长、工业化和都市化,该国是世界上成长最快的国家之一。

- 巴西石油出口的增加预计将在推动南美船用燃料市场方面发挥关键作用。巴西是主要石油生产国,正在扩大石油产量,出口增加为该地区的船用燃料市场创造了重大机会。

- 随着国际航线经过南美水域,船舶使用的船用燃料的需求预计将激增。巴西作为主要石油出口国的战略地位使其成为影响南美洲船用燃料供应和价格趋势的关键参与者。

- 例如,2022年11月,挪威Kanfer Shipping AS与Nimofast Brasil SA签署伙伴关係协议,从2025年起在巴西建立中小型液化天然气运输船和液化天然气燃料库解决方案。液化天然气运输船和液化天然气加註船将透过 FSU 进行装载,该 FSU 将永久位于巴拉那州的 Nemofast 液化天然气进口和发行终端。

- 此外,巴西石油出口的增加与该地区海上贸易活动活性化的更广泛趋势是一致的。随着船舶运输量的增加,作为船舶主要能源来源的船用燃料的需求预计也会相应增加。

- 船用燃料需求的激增不仅反映了南美洲在全球贸易中日益重要的地位,而且还反映了巴西等石油出口国对船用燃料等相关行业趋势产生重大影响的潜力,这凸显了能源市场的相互关係联性。

- 巴西拥有全球最大的可采超深层石油蕴藏量,巴西96.7%的石油产量来自海上。 2022 年石油产量为 1.631 亿吨,高于 2021 年的 1.569 亿吨。

- 因此,随着石油和天然气产量预计增加,巴西与世界其他地区之间的贸易活动预计将进一步增加。由于主要的国际贸易是透过海上航线进行的,预计巴西将在不久的将来成为船用燃料的新兴市场。

- 所有上述因素预计将有助于该国在预测期内在船用燃料方面占据该地区的主导地位。

南美船用燃料油产业概况

南美船用燃料市场已减少一半。主要企业(排名不分先后)包括 Bunker Holding A/S、Monjasa Holding A/S、AP Moeller Maersk A/S、World Fuel Services Corp 和 Peninsula Petroleum Ltd。

其他好处:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第一章简介

- 调查范围

- 市场定义

- 研究场所

第 2 章执行摘要

第三章调查方法

第四章市场概况

- 介绍

- 2029年之前的市场规模与需求预测(单位:美元)

- 最新趋势和发展

- 政府法规政策

- 市场动态

- 促进因素

- 南美洲必需品海运的增加

- 清洁船用燃料支持政策

- 抑制因素

- 石油市场不稳定

- 促进因素

- 供应链分析

- 波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间的敌对关係

第五章市场区隔

- 按燃料类型

- 高硫燃料油(HSFO)

- 极低硫燃油(VLSFO)

- 船用轻柴油 (MGO)

- 液化天然气(LNG)

- 其他燃料(甲醇、液化石油气、生质柴油)

- 按船舶类型

- 容器

- 油船

- 普货

- 散装货柜

- 其他船舶类型

- 按地区

- 巴西

- 智利

- 阿根廷

- 南美洲其他地区

第六章 竞争状况

- 併购、合资、联盟、协议

- 主要企业策略

- 公司简介

- Fuel Suppliers

- Vitol Holding BV

- Monjasa Holding A/S

- Bunker Holding A/S

- World Fuel Services Corp

- Peninsula Petroleum Ltd

- TotalEnergies SA

- Chevron Corporation

- Ship Owners

- AP Moeller Maersk A/S

- Mediterranean Shipping Company SA

- China COSCO Holdings Company Limited

- CMA CGM Group

- Hapag-Lloyd AG

- Ocean Network Express

- Fuel Suppliers

- Market Ranking/Share(%)Analysis

第七章 市场机会及未来趋势

- 使用无污染燃料

简介目录

Product Code: 71505

The South America Bunker Fuel Market size is estimated at USD 15.45 billion in 2025, and is expected to reach USD 19.53 billion by 2030, at a CAGR of 4.8% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, factors such as the ever-rising marine transportation of essential commodities and implementation of stricter environmental regulations driving the demand for cleaner bunker fuels drive the growth in the South American bunker fuel market.

- On the other hand, the oil market's volatility is significantly expected to affect the bunker fuel market as it can impact the profitability of bunker fuel suppliers and make planning and investing difficult.

- Nevertheless, the increase in the use of clean bunker fuels creates a significant opportunity for the South American bunker fuel market.

- Brazil is expected to dominate the bunker fuel market in the region owing to factors like substantial crude oil production and a steady rise in exports from the country.

South America Bunker Fuel Market Trends

Very Low Sulfur Fuel Oil (VLSFO) to Witness Significant Growth

- The demand for shallow sulfur fuel oil (VLSFO) in the South African Bunker fuel market has seen a significant rise in recent years, following the International Maritime Organization's (IMO) mandate on reducing sulfur emissions from ships.

- As of April 2023, VLSFO availability is particularly strained in the domestic bunker fuel market, as most of the VLSFO used in the South Africa bunker fuel market is imported. Low-sulfur fuel oil is available in the ports of Durban, Port Elizabeth, and Cape Town, as well as at offshore bunkering in AlgoaBay (off Port Elizabeth and Ngqura).

- Moreover, the price fluctuations for VLSFO in the region are lesser compared to their counterparts, as between December 2022 and April 2023, the changes in prices were recorded at around 5%. In contrast, the counterparts have registered more variance, which further adds to the demand for this fuel.

- In October 2022, FUEL & MARINE OIL CORP (FAMOIL), a commodity trading house specializing in the marine fuel industry, added a bunker delivery vessel to its operation in Peru. The company added the tanker Ecomar II to its fleet. The vessel supplies Very Low Sulfur Fuel Oil (VLSFO) and High Sulfur Fuel Oil at Talara, Paita, Bayovar, Salaverry, Chimbote ports Pisco, San Nicolas, Matarani, and Llo.

- Moreover, the demand for VLSFO in the South American market is also driven by the growing number of vessels operating in the region. The stricter regulations on the environmental impact of these fuels on marine life have consequently driven the demand for VLSFO.

- Overall, the market is expected to witness significant growth during the forecast period owing to factors like increasing demand, which spurred up after the implementation of the IMO sulfur cap.

Brazil to Dominate the Market

- Brazil is the largest economy in the region and is expected to be the fastest-growing economy in the forecast period. The country is one of the fastest-growing countries worldwide because of the increasing population, industrialization, and urbanization.

- The increasing exports of oil from Brazil are anticipated to play a pivotal role in driving the market for bunker fuel in South America. Brazil, as a major oil-producing nation, has been expanding its oil output, and the growing exports present a significant opportunity for the bunker fuel market in the region.

- As international shipping routes pass through South American waters, the demand for bunker fuel used by marine vessels is expected to surge. Brazil's strategic location as a prominent exporter of oil makes it a crucial player in influencing the availability and pricing dynamics of bunker fuel in South America.

- For instance, In November 2022, Norwegian company Kanfer Shipping AS signed a partnership deal with Nimofast Brasil S.A. to establish small and medium-scale LNG shipping and LNG bunkering solutions in Brazil from 2025 onwards. The LNG vessels and LNG bunker ships will be loaded via the permanently based FSU at the Nimofast LNG import- and distribution terminal in the state of Parana.

- Moreover, the rise in oil exports from Brazil aligns with the broader trend of increased maritime trade activities in the region. As shipping traffic intensifies, the demand for bunker fuel as the primary energy source for marine vessels is expected to witness a corresponding uptick.

- This surge in demand for bunker fuel not only reflects the growing importance of South America in global trade but also underscores the interconnected nature of energy markets, where oil-exporting countries like Brazil can significantly impact the dynamics of related sectors such as marine fuels.

- Brazil owns the largest recoverable ultra-deep oil reserves in the world, with 96.7% of Brazil's oil production produced offshore. In 2022, the oil production was 163.1 million tonnes, increased from 156.9 million tonnes in 2021.

- Hence, with the expected increase in oil and gas production, trading activities between Brazil and the rest of the world are expected to increase further. With major international trading activities carried out through the marine route, Brazil is expected to become the emerging market for bunker fuel in the near future.

- All of the above factors are expected to help the country dominate the region in terms of bunker fuel during the forecast period.

South America Bunker Fuel Industry Overview

The South American bunker fuel market is semi-fragmented. Some of the major companies (in no particular order) are Bunker Holding A/S, Monjasa Holding A/S, AP Moeller Maersk A/S, World Fuel Services Corp, and Peninsula Petroleum Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Rising Marine Transportation of Essential Commodities in South America

- 4.5.1.2 Supportive Policies for Cleaner Bunker Fuel

- 4.5.2 Restraints

- 4.5.2.1 Volatile Nature of Oil Market

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Fuel Type

- 5.1.1 High Sulfur Fuel Oil (HSFO)

- 5.1.2 Very Low Sulfur Fuel Oil (VLSFO)

- 5.1.3 Marine Gas Oil (MGO)

- 5.1.4 Liquefied Natural Gas (LNG)

- 5.1.5 Other Fuel Types (Methanol, LPG, and Biodiesel)

- 5.2 Vessel Type

- 5.2.1 Containers

- 5.2.2 Tankers

- 5.2.3 General Cargo

- 5.2.4 Bulk Container

- 5.2.5 Other Vessel Types

- 5.3 Geography

- 5.3.1 Brazil

- 5.3.2 Chile

- 5.3.3 Argentina

- 5.3.4 Rest of South America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Fuel Suppliers

- 6.3.1.1 Vitol Holding BV

- 6.3.1.2 Monjasa Holding A/S

- 6.3.1.3 Bunker Holding A/S

- 6.3.1.4 World Fuel Services Corp

- 6.3.1.5 Peninsula Petroleum Ltd

- 6.3.1.6 TotalEnergies SA

- 6.3.1.7 Chevron Corporation

- 6.3.2 Ship Owners

- 6.3.2.1 AP Moeller Maersk A/S

- 6.3.2.2 Mediterranean Shipping Company SA

- 6.3.2.3 China COSCO Holdings Company Limited

- 6.3.2.4 CMA CGM Group

- 6.3.2.5 Hapag-Lloyd AG

- 6.3.2.6 Ocean Network Express

- 6.3.1 Fuel Suppliers

- 6.4 Market Ranking/Share (%) Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Utilization of Clean Bunker Fuels

02-2729-4219

+886-2-2729-4219

船用燃料市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)

船用燃料市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年) 全球船用燃料市场(按燃料类型、应用、最终用户和分销管道)预测 2025-2032

全球船用燃料市场(按燃料类型、应用、最终用户和分销管道)预测 2025-2032 美国船用燃料市场:市场规模、份额、趋势分析(按类型和应用)、细分市场预测(2025-2030 年)

美国船用燃料市场:市场规模、份额、趋势分析(按类型和应用)、细分市场预测(2025-2030 年) 船用燃料市场:2025-2030 年预测

船用燃料市场:2025-2030 年预测 2025 年至 2033 年船用燃料市场规模、份额、趋势及预测(依燃料类型、船舶类型、卖家及地区)

2025 年至 2033 年船用燃料市场规模、份额、趋势及预测(依燃料类型、船舶类型、卖家及地区) 2025-2029年全球船用燃料市场

2025-2029年全球船用燃料市场 船用燃料的全球市场:类别,各终端用户,各地区,机会,预测,2018年~2032年船用燃料市场规模、份额、趋势分析报告:按类型、应用、地区、细分市场预测,2025-2030 年船用燃料市场按燃料类型、船舶类型、私人经销商和地区划分(2026 年至 2032 年)

船用燃料的全球市场:类别,各终端用户,各地区,机会,预测,2018年~2032年船用燃料市场规模、份额、趋势分析报告:按类型、应用、地区、细分市场预测,2025-2030 年船用燃料市场按燃料类型、船舶类型、私人经销商和地区划分(2026 年至 2032 年) 2025年全球船用燃料市场报告

2025年全球船用燃料市场报告

▼