|

市场调查报告书

商品编码

1636110

欧洲叶轮:市场占有率分析、产业趋势/统计、成长预测(2025-2030)Europe Rotor Blade - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

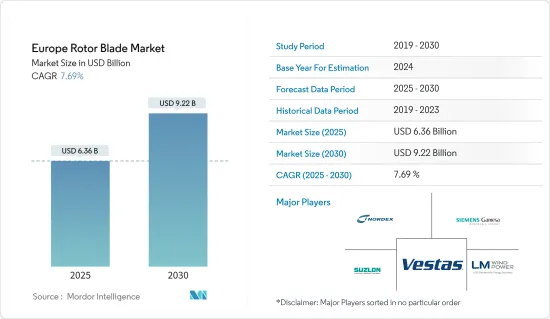

欧洲叶轮市场规模预计到2025年为63.6亿美元,预计2030年将达到92.2亿美元,预测期内(2025-2030年)复合年增长率为7.69%。

主要亮点

- 从中期来看,海上和陆上风力发电装置的增加、风力发电成本的下降以及风力发电领域投资的增加等因素预计将在预测期内推动欧洲叶轮市场的发展。

- 另一方面,运输成本的相关上升以及太阳能和水力发电等替代清洁能源的成本竞争等因素可能会限制预测期内的市场成长。

- 风能产业需要具有成本效益的解决方案,而高效的产品有能力改变产业的动态。旧涡轮机被更换并不是因为它们损坏了,而是因为市场上出现了更有效的叶片。因此,技术进步最终为叶轮市场创造了巨大的机会。

欧洲叶轮市场趋势

近海领域占据市场主导地位

- 2022年欧洲新增风力发电容量为1859千万瓦。疫情结束后,随着工业活动的开始和快速都市化,欧洲的电力需求正在增加。该地区的可再生能源份额也不断增加,以满足不断增长的电力需求。

- 欧洲被认为拥有丰富的可再生能源发电资源,包括太阳能、风能、水力、生质能和地热能。许多欧洲国家处于全球利用可再生能源的前沿。脱碳、电网永续性、雄心勃勃的目标以及向清洁能源的过渡等因素正在推动欧洲风力发电市场的发展。

- 2022年12月,欧盟委员会核准了《2023年再生能源来源法案》,《2023年海上风力发电法案》将聚焦在改善环境、实现欧洲电力市场温室气体中和的电力供应。

- 此外,2022年5月,欧盟委员会宣布了REPowerEU计划。该计划包括一系列旨在逐步淘汰俄罗斯石化燃料和促进欧盟可再生能源生产的具体措施。该计划预计将有助于该地区海上风力发电的进一步发展。

- 随着REPowerEU的宣布,形成了埃斯比尔宣言,以实现离岸风电这一连接比利时、丹麦、德国和荷兰的海上可再生能源系统以及北海150GW的新目标。 ,并决定共同开发其他北海合作伙伴,在某些情况下包括北海能源合作(NSEC) 成员国。

- 据国际可再生能源机构称,欧洲是全球离岸风电市场的领先地区之一。 2022年新增装置4264兆瓦,达3066千万瓦。 2022年3月,法国政府与法国风电产业签署了海上部门协议。该协议认识到离岸风电是一个重要且必不可少的机会,并承诺到2050年在50个风力发电厂开发40GW的离岸风电。预计这将导致海上风力发电的重大发展。

- 此外,2022年6月,基利贝格斯渔业协会和辛巴德海洋服务公司提案在爱尔兰多尼戈尔海岸建造浮动式风力发电,并与瑞典浮动式风力发电开发技术提供商Hexicon签署了谅解备忘录。

- 综上所述,预计离岸风电领域将在预测期内占据市场主导地位。

英国主导市场

- 英国是风力发电发展最快的国家之一。该国被定位为欧洲风力发电的最佳地点。到2022年,英国风电装置容量将达到28.54GW。

- 此外,英国不依赖俄罗斯天然气供应,因此与其他欧盟国家相比,受俄乌衝突影响较小。然而,2022年4月,英国前首相实施了能源安全战略,以减少战争影响,促进国内可再生能源发展。这反过来预计将支持风力发电市场的成长,并进一步支持风力叶轮市场的发展。

- 2016年至2021年间,英国离岸风电投资约257.9亿美元,为离岸风电领域提供了有利的投资环境,因为英国是离岸风发电工程的先驱之一。

- 此外,2022年4月,政府宣布了一项加强英国能源安全的战略计划,目标是到2030年运作离岸风电装置容量提高到50GW。 50GW离岸风电目标包括5GW大型浮体式离岸风电设施。

- 此外,2022年1月,英国政府宣布将投入超过8,250万美元的公共和私人资金,以推动浮体式风电发电工程的研发。作为浮体式离岸风电示范计画的一部分,政府将在 11 个计划上投资 4,190 万美元。

- 因此,鑑于上述几点,预计英国将在预测期内主导市场。

欧洲叶轮产业概况

欧洲叶轮市场较为分散。市场上的主要企业(排名不分先后)包括 Nordex SE、Siemens Gamesa Renewable Energy, SA、Vestas Wind Systems A/S、Suzlon Energy Limited 和 LM Wind Power(GE 再生能源业务)。

2022年2月,Nordex宣布德国罗斯托克GVZ叶轮工厂的叶轮生产将于2022年6月底停止。这项决定主要是由于转向罗斯托克无法製造的更大叶片。

其他好处

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 调查范围

- 市场定义

- 研究场所

第 2 章执行摘要

第三章调查方法

第四章市场概况

- 介绍

- 至2029年市场规模及需求预测(单位:十亿美元)

- 最新趋势和发展

- 政府法规和措施

- 市场动态

- 促进因素

- 海上和陆域风力发电装置的增加

- 降低风电成本

- 抑制因素

- 与替代可再生能源的竞争加剧

- 促进因素

- 供应链分析

- 波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间敌对关係的强度

第五章市场区隔

- 部署地点

- 陆上

- 离岸

- 刀片材质

- 碳纤维

- 玻璃纤维

- 其他刀片材料

- 地区

- 德国

- 法国

- 西班牙

- 英国

- 义大利

- 北欧的

- 土耳其

- 俄罗斯

- 欧洲其他地区

第六章 竞争状况

- 併购、合资、联盟、协议

- 主要企业策略

- 公司简介

- Nordex SE

- Siemens Gamesa Renewable Energy SA

- Vestas Wind Systems A/S

- Suzlon Energy Limited

- Enercon GmbH

- LM Wind Power(GE 再生能源业务)

- BayWa RE AG

- Market Ranking/Share Analysis

第七章 市场机会及未来趋势

- 开发高效能、轻量化风力发电机

The Europe Rotor Blade Market size is estimated at USD 6.36 billion in 2025, and is expected to reach USD 9.22 billion by 2030, at a CAGR of 7.69% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, factors such as the growing number of offshore and onshore wind energy installations, the declining cost of wind energy, and increasing investments in the wind power sector are anticipated to drive the Europe rotor blade market during the forecast period.

- On the other hand, factors such as the accompanying high cost of transportation and cost competitiveness of alternate clean power sources like solar power, hydropower, etc., can potentially restrain the market growth during the forecast period.

- Nevertheless, the wind power business has sought cost-effective solutions, and a highly efficient product has the ability to alter the industry's dynamics. There were instances where old turbines were replaced not owing to damage but because more effective blades were sold in the market. Thus, technological advancements eventually create a wonderful opportunity for the market of rotor blades.

Europe Rotor Blade Market Trends

Offshore Segment to Dominate the Market

- Europe accounted for 18.59 GW of new wind installed capacity in 2022. The electricity demand in Europe has increased after the departure of the pandemic, coupled with the commencement of industrial activities and rapid urbanization. The region has also witnessed a growing share of renewables to fulfill the increasing electricity demand.

- Europe is considered to have ample renewable energy resources to generate electricity, such as solar, wind, hydro, biomass, geothermal, etc. A good number of countries in Europe have become at the forefront of utilizing renewable energy globally. Factors such as decarbonization, sustainability of power systems, ambitious targets, and clean energy transition have driven the offsore wind energy market of Europe.

- In December 2022, the European Commission approved the 2023 Renewable Energy Sources Act, and the 2023 Offshore Wind Energy Act aims to improve the environment and focus on achieving a greenhouse gas-neutral electricity supply in the power market of Europe.

- Further, in May 2022, the European Commission published the REPowerEU plan, which contains a series of concrete measures designed to phase out Russian fossil fuels and boost the production of renewable energy in the EU. This plan would help further develop offshore wind energy in the region.

- With the REPowerEU announcement, the Esbjerg Declaration was formed to achieve the further expansion of offshore wind and decided to jointly develop The North Sea as a Green Power Plant of Europe, an offshore renewable energy system connecting Belgium, Denmark, Germany, and the Netherlands, and possibly other North Sea partners, including the members of the North Seas Energy Cooperation (NSEC) and set out a new target of 150 GW of offshore wind by 2050.

- According to International Renewable Energy Agency, Europe is among the leading regions in the global offshore wind power market. In 2022, it added 4,264 MW, reaching 30.66 GW. In March 2022, the French government entered into an offshore sector agreement with France's wind industry. The agreement recognizes that offshore wind is a significant and vital opportunity and commits to developing 40 GW of offshore wind by 2050 spread over 50 wind farms. This is expected to witness considerable development in offshore wind power.

- Also in June 2022, The Killybegs Fishermen's Organization and Sinbad Marine Services have proposed a floating wind farm to be built offshore Donegal, Ireland, and have signed a Memorandum of Understanding with Swedish floating wind developer and technology provider, Hexicon.

- Therefore, owing to the above points, the offshore segment is anticipated to dominate the market during the forecast period.

United Kingdom to Dominate the Market

- The United Kingdom is one of the growing countries in wind energy generation. The country stands as the best location for wind power in Europe. By 2022, the United Kingdom installed a wind capacity of 28.54 GW.

- Moreover, the United Kingdom is not heavily affected by the Russia-Ukraine conflict compared to the other EU countries, Since the country is not dependent on the Russian gas supply. However, in April 2022, the former UK Prime Minister implemented an energy security strategy to lessen the war impact and boost renewable energy development within the country. This will, in turn, support the growth of the wind energy market and further aid the development of the wind rotor blade market.

- Since the country is one of the forerunners in offshore wind projects, between 2016 and 2021, nearly USD 25.79 billion was invested in offshore wind in the United Kingdom, witnessing a favorable investment environment in the offshore wind sector.

- Furthermore, in April 2022, the government announced a strategic plan to boost Britain's energy security, including an increased target of up to 50 GW of operating offshore wind capacity by 2030. The 50GW offshore wind target includes 5 GW of large-scale floating wind installations.

- Moreover, in January 2022, the UK government announced more than USD 82.5 million of public and private funding to advance research and development in floating offshore wind projects. The government plans to invest USD 41.9 million in 11 projects as part of the Floating Offshore Wind Demonstration Program.

- Therefore, owing to the above points, the United Kingdom is anticipated to dominate the market during the forecast period.

Europe Rotor Blade Industry Overview

The Europe rotor blade market is fragmented in nature. Some of the major players in the market (in no particular order) include Nordex SE, Siemens Gamesa Renewable Energy, SA, Vestas Wind Systems A/S, Suzlon Energy Limited, and LM Wind Power (a GE Renewable Energy business), among others.

In February 2022, Nordex announced that it would cease the production of rotor blades at the Rostock GVZ rotor blade site in Germany by the end of June 2022. The decision has been taken primarily due to a shift towards larger blades that are not manufactured at Rostock.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Growing number of offshore and onshore wind energy installations

- 4.5.1.2 Declining cost of wind energy

- 4.5.2 Restraints

- 4.5.2.1 Increasing Competition from Alternate Renewable Energy Sources

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Location of Deployment

- 5.1.1 Onshore

- 5.1.2 Offshore

- 5.2 Blade Material

- 5.2.1 Carbon Fiber

- 5.2.2 Glass Fiber

- 5.2.3 Other Blade Materials

- 5.3 Geography

- 5.3.1 Germany

- 5.3.2 France

- 5.3.3 Spain

- 5.3.4 United Kingdom

- 5.3.5 Italy

- 5.3.6 NORDIC

- 5.3.7 Turkery

- 5.3.8 Russia

- 5.3.9 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Nordex SE

- 6.3.2 Siemens Gamesa Renewable Energy SA

- 6.3.3 Vestas Wind Systems A/S

- 6.3.4 Suzlon Energy Limited

- 6.3.5 Enercon GmbH

- 6.3.6 LM Wind Power (a GE Renewable Energy business)

- 6.3.7 BayWa R.E AG

- 6.4 Market Ranking/Share Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Development of High Efficiency and light weight wind turbines

全球风力发电机叶片检测服务市场

全球风力发电机叶片检测服务市场 风力涡轮机叶片市场-全球产业规模、份额、趋势、机会及预测(按叶片长度、材料、部署、地区和竞争进行细分,2020-2030 年预测)

风力涡轮机叶片市场-全球产业规模、份额、趋势、机会及预测(按叶片长度、材料、部署、地区和竞争进行细分,2020-2030 年预测) 全球风力发电机叶轮市场规模(按类型、位置、区域、范围和预测)

全球风力发电机叶轮市场规模(按类型、位置、区域、范围和预测) 风力涡轮机转子叶片市场报告,按叶片材料(碳纤维、玻璃纤维等)、叶片长度(45 公尺以下、45-60 公尺、60 公尺以上)、部署位置(陆上、海上)和地区划分,2025 年至 2033 年

风力涡轮机转子叶片市场报告,按叶片材料(碳纤维、玻璃纤维等)、叶片长度(45 公尺以下、45-60 公尺、60 公尺以上)、部署位置(陆上、海上)和地区划分,2025 年至 2033 年 风力发电机叶轮:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)

风力发电机叶轮:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年) 风力涡轮机叶片回收市场报告:趋势、预测和竞争分析(至 2031 年)

风力涡轮机叶片回收市场报告:趋势、预测和竞争分析(至 2031 年) 2025年全球风力发电机叶片检测服务市场报告中国风力发电机叶轮:市场占有率分析、产业趋势/统计、成长预测(2025-2030)亚太地区风力发电机叶轮:市场占有率分析、产业趋势和成长预测(2025-2030)北美叶轮:市场占有率分析、行业趋势和成长预测(2025-2030)

2025年全球风力发电机叶片检测服务市场报告中国风力发电机叶轮:市场占有率分析、产业趋势/统计、成长预测(2025-2030)亚太地区风力发电机叶轮:市场占有率分析、产业趋势和成长预测(2025-2030)北美叶轮:市场占有率分析、行业趋势和成长预测(2025-2030)