|

市场调查报告书

商品编码

1636173

SLI 电池:市场占有率分析、产业趋势/统计、成长预测(2025-2030 年)SLI Battery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

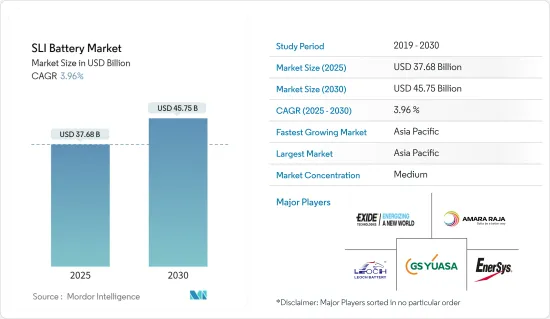

SLI电池市场规模预计到2025年为376.8亿美元,预计到2030年将达到457.5亿美元,预测期内(2025-2030年)复合年增长率为3.96%。

主要亮点

- 从中期来看,汽车的普及以及工业和农业应用对 SLI 电池日益增长的需求预计将在预测期内推动 SLI 电池市场的发展。

- 另一方面,替代电池的扩散和严格的政府监管预计将阻碍预测期内的市场成长。

- 对电池回收的日益关注以及新车和售后市场替换新兴市场的扩张可能会为 SLI 电池市场创造机会。

SLI电池市场趋势

汽车板块实现显着成长

- 由于汽车行业的不断扩张以及对可靠电源的持续需求,汽车领域的启动、照明和点火 (SLI) 电池市场预计将显着增长。 SLI 电池是汽车的重要组成部分,提供启动引擎、运作电气系统以及正确点火汽车所需的电力。

- 随着全球汽车持有持续成长,对 SLI 电池的需求依然强劲。例如,根据国际汽车工业协会(OICA)的数据,2023年全球汽车销售量约为9,272.4万辆,与前一年同期比较2022年成长11.89%。

- 2023年全球汽车销售中,乘用车销量超过65,272,000辆,商用车销量超过27,452,000辆。预计这种趋势将在短期内持续下去,并在预测期内对 SLI 电池产生巨大的需求。此外,SLI 电池技术的进步,例如增强型富液电池 (EFB) 和吸收玻璃毡 (AGM) 电池,可提高性能和耐用性,进一步推动市场成长。

- 儘管前景乐观,但 SLI 电池市场将逐渐开始面临电动车 (EV) 日益普及以及转向更永续能源解决方案的挑战。电动车通常使用锂离子电池,从长远来看,这可能会减少对传统 SLI 电池的需求。

- 在一些国家,汽油和柴油汽车的渗透率在未来几年短期内将继续保持稳定。例如,2023年9月,英国首相确认将计画中的禁令延长五年,从2030年延长至2035年。在英国宣布政策改变之前,政府曾计划在2030年禁止销售新的纯汽油和柴油汽车。目前的计划是从2035年开始禁止。

- 据政府称,根据该禁令,从 2035 年起,只能购买电动车和零排放汽车作为新车。然而,由于大多数驾驶者购买二手车,因此大多数人可能不会受到这项禁令的影响。只有新的汽油和柴油车销售会受到影响;现有车辆不会受到影响。此外,延长禁令将使英国与欧盟保持一致。欧盟也计划在2035年禁止销售新的汽油和柴油汽车。

- 总体而言,SLI电池市场预计将保持适度的成长轨迹。对汽车基础设施的持续投资以及电池设计和製造的技术进步预计将在市场成长中发挥关键作用。此外,我们对环保 SLI 电池开发和回收的承诺符合全球永续性目标,并确保在不断发展的汽车领域的市场相关性。

亚太地区预计将主导市场

- 预计亚太地区的 SLI(启动、照明、点火)电池市场将显着成长。这可能是由多种因素造成的,包括快速都市化、汽车产量增加以及消费者对汽车的需求不断增长。中国、印度、日本和韩国等国家由于其庞大的汽车市场和对汽车製造基础设施的大量投资,对这一增长做出了重大贡献。

- 根据国际汽车工业协会(OICA)预测,2023年中国汽车产量约30,161,000辆,日本超过8,990,000辆,韩国为4,243,000辆,印度超过5,850,000辆。这使得该地区成为全球 SLI 电池的主要市场之一。此外,由于道路上车辆数量众多,SLI电池更换市场也相当大。

- 最近的进展包括几家主要汽车製造商计划在该地区开发和扩大汽油和柴油动力汽车製造设施。例如,2023年11月,日本主要汽车製造商丰田与卡纳塔克邦政府签署谅解备忘录,在印度建立第三家製造工厂,年产能增加10万辆。新工厂将建在班加罗尔附近的比达迪,靠近该公司现有的两座工厂,预计投资约330亿印度卢比。

- 丰田现有的比达迪工厂年产能总计总合4,000辆,新工厂将于2026年投入运作,计划将丰田的产能提高约30%。这项宣布对在印度拥有 25 年历史的丰田品牌来说是一个提振。据该公司介绍,新工厂将成为下一代三排SUV的主要生产基地。丰田计划每年生产6万辆,预计2026年上市。汽车製造领域的此类发展预计将在未来几年推动 SLI 电池的采用。

- 此外,一些主要企业,如GS Yuasa Corporation,包括印度Tata AutoComp GY Batteries Private Ltd (TGY),其子公司GS Yuasa International Ltd (GS Yuasa)的权益法附属公司,部分公司已拥有该公司。 TGY成立于2005年10月,旨在扩大其在亚洲最大摩托车生产国印度的市场份额。

- TGY于2021年在工厂内新扩建的大楼开始生产,并于2022年新增一条生产线并开始全面量产。藉此,TGY将继续扩大产能,目标是建立年产840万隻摩托车铅酸蓄电池的生产体系,较扩产前的420万隻增加一倍。工厂的扩建预计将扩大该公司生产的电池型号范围。 TGY也预计将加强其汽车铅酸电池的生产,重点关注启停汽车等环保汽车的高性能铅酸电池,预计此类电池的需求将持续增长。

- 因此,由于上述因素,预计亚太地区SLI电池市场在预测期内将显着成长。

SLI电池产业概况

SLI 电池市场呈现半分裂状态。市场的主要企业包括(排名不分先后)GS Yuasa International Ltd、Exide Technologies、Amara Raja Energy & Mobility Limited、EnerSys 和 Leoch International Technology Limited Inc。

其他好处

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 调查范围

- 市场定义

- 研究场所

第 2 章执行摘要

第三章调查方法

第四章市场概况

- 介绍

- 2029年之前的市场规模与需求预测(单位:美元)

- 最新趋势和发展

- 政府法规和措施

- 市场动态

- 促进因素

- 汽车普及率不断提高

- 工业和农业应用对 SLI 电池的需求不断增长

- 抑制因素

- 替代电池的扩展

- 促进因素

- 供应链分析

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代产品/服务的威胁

- 竞争公司之间的敌对关係

第五章市场区隔

- 类型

- 电池被淹

- VRLA 电池

- EBF电池

- 最终用户

- 用于汽车

- 其他的

- 地区

- 北美洲

- 美国

- 加拿大

- 北美其他地区

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 北欧的

- 俄罗斯

- 欧洲其他地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 泰国

- 马来西亚

- 印尼

- 越南

- 其他亚太地区

- 中东/非洲

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 南非

- 埃及

- 奈及利亚

- 卡达

- 其他中东/非洲

- 南美洲

- 巴西

- 阿根廷

- 智利

- 南美洲其他地区

- 北美洲

第六章 竞争状况

- 併购、合资、联盟、协议

- 主要企业策略及SWOT分析

- 公司简介

- GS Yuasa International Ltd.

- Exide Technologies

- Amara Raja Energy & Mobility Limited

- EnerSys

- Leoch International Technology Limited Inc.

- East Penn Manufacturing Company

- C&D Technologies Inc.

- Clarios International Inc.

- Trojan Battery Company

- Crown Battery Manufacturing Company

- 其他知名公司名单(公司名称、总部地点、相关产品及服务、联络资讯等)

- 市场排名分析

第七章 市场机会及未来趋势

- 人们越来越关注电池回收

- 拓展新车和售后市场应用的新兴市场

简介目录

Product Code: 50002581

The SLI Battery Market size is estimated at USD 37.68 billion in 2025, and is expected to reach USD 45.75 billion by 2030, at a CAGR of 3.96% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, the increasing adoption of motor vehicles and the growing demand for SLI batteries from industrial and agricultural applications are expected to drive the SLI batteries market during the forecast period.

- On the other hand, the increasing penetration of alternative battery chemistries and the stringent government regulations are expected to hinder the market's growth during the forecast period.

- Nevertheless, the increased focus on battery recycling and the expansion in emerging markets for both new vehicles and after-market replacements will likely create opportunities for the SLI battery market.

SLI Battery Market Trends

Automotive Segment to Witness Significant Growth

- The market for starting, lighting, and Ignition (SLI) batteries in the automotive segment is expected to witness notable growth, driven by the expanding automotive industry and the continuous need for reliable power sources. SLI batteries are essential components in motor vehicles, providing the necessary power to start the engine, run electrical systems, and ensure proper ignition.

- As the global vehicle fleet continues to grow, the demand for SLI batteries remains robust. For example, as per the International Organization of Motor Vehicle Manufacturers(OICA), the total global motor vehicle sales stood at around 92.724 million in 2023, recording over 11.89% growth compared to the previous years in 2022.

- Of the total global motor vehicle sales in 2023, the total passenger vehicles and commercial vehicle sales stood at over 65.272 million and 27.452 million, respectively. Such trends are expected to continue over the short term and create a substantial demand for the SLI battery during the forecast period. In addition, advancements in SLI battery technology, such as enhanced flooded batteries (EFB) and absorbent glass mat (AGM) batteries, are providing improved performance and durability, further propelling market growth.

- Despite the positive outlook, the SLI battery market will gradually start facing challenges from the growing popularity of electric vehicles (EVs) and the shift toward more sustainable energy solutions. EVs typically use lithium-ion batteries, which may reduce the demand for traditional SLI batteries in the long term.

- Nevertheless, several nations continue to experience a stable adoption of petrol and diesel vehicles over the short term in the coming years. For example, in September 2023, the United Kingdom's Prime Minister confirmed the planned ban was being pushed back five years from 2030 to 2035. Before the United Kingdom announced a shift in policy, the government had planned to ban the sale of new, pure petrol and diesel vehicles by 2030. Now, the plan is for the ban to begin in 2035.

- According to the government, under the ban, only electric battery-powered cars and zero-emission vehicles will be able to be bought new from 2035. However, most people will not be impacted by the ban, as most drivers buy vehicles secondhand. Only sales of new petrol and diesel models would be affected, not the existing ones. Moreover, the delay in the ban brings the United Kingdom into line with the European Union, which is also banning sales of new petrol and diesel cars by 2035.

- Overall, the SLI battery market is expected to maintain a growth trajectory, albeit at a moderate pace. Continued investments in automotive infrastructure, coupled with technological advancements in battery design and manufacturing, is expected to play a crucial role in market growth. In addition, the development of eco-friendly SLI batteries and recycling initiatives will align with global sustainability goals, ensuring the market's relevance in the evolving automotive landscape.

Asia-Pacific Region is Expected to Dominate the Market

- The Asia-Pacific region is expected to witness significant growth in the SLI (Starting, Lighting, and Ignition) battery market. This is likely to be driven by a combination of factors, including rapid urbanization, increasing vehicle production, and growing consumer demand for automobiles. Countries such as China, India, Japan, and South Korea are major contributors to this growth due to their large automotive markets and significant investments in automotive manufacturing infrastructure.

- According to the International Organization of Motor Vehicle Manufacturers (OICA), the total number of motor vehicles produced in China stood at around 30.161 million in 2023, Japan produced over 8.99 million, South Korea produced 4.243 million, and India produced over 5.85 million. This makes the region one of the significant markets for SLI batteries worldwide. Moreover, the replacement market for SLI batteries is also substantial due to the high number of vehicles on the road.

- Recently, some of the major automobile manufacturers have also planned to develop and expand automobile manufacturing facilities in the region, where the vehicles are fuelled by petrol and diesel. For example, in November 2023, Toyota, one of the largest Japanese automakers, signed a Memorandum of Understanding (MoU) with the government of Karnataka to set up a third manufacturing plant in India, which would increase its production capacity by 1 lakh units per annum. The upcoming plant will also be situated in Bidadi, near Bangalore, near the existing two, and is expected to attract an investment of around INR 3,300 crores.

- Toyota's existing plants at Bidadi have a combined output of about 4 lakh units per annum, and this new plant operational by 2026 is planned to add about 30% to Toyota's production capacity. This announcement comes on the back of the brand, which has been completing 25 years in India. According to the company, the new plant will be the primary production base for an upcoming three-row SUV. Toyota is planned to produce 60,000 units annually, with a launch likely by 2026. Such developments in automobile manufacturing are expected to boost the adoption of SLI batteries in the coming years.

- Furthermore, some of the leading SLI battery players, such as GS Yuasa Corporation, announced that their India-based company Tata AutoComp GY Batteries Private Ltd (TGY), an equity-method affiliate of subsidiary GS Yuasa International Ltd (GS Yuasa), aims to double its annual production capacity for motorcycle lead-acid batteries to 8.4 million units. TGY, which was established in October 2005, is aiming to boost its market share in India, Asia's largest motorcycle-producing country.

- TGY launched production in a newly added wing at its plant in 2021 and began full-fledged mass production with the addition of a new production line in 2022. With this, TGY aims to continue expanding production capacity and establish a production system capable of producing 8.4 million lead-acid motorcycle batteries per year, double its pre-expansion capacity of 4.2 million units. The plant expansion is expected to enable the company to expand the range of battery models it manufactures. In addition, TGY is expected to strengthen its production of automotive lead-acid batteries, with a focus on high-performance lead-acid batteries for environment-friendly vehicles, such as start & stop vehicles, demand for which is expected to continue growing in the coming years.

- Therefore, owing to the abovementioned factors, the Asia-Pacific region is anticipated to witness notable growth for the SLI battery market during the forecast period.

SLI Battery Industry Overview

The SLI battery market is semi-fragmented. Some of the key players in the market (not in any particular order) include GS Yuasa International Ltd, Exide Technologies, Amara Raja Energy & Mobility Limited, EnerSys, and Leoch International Technology Limited Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing Adoption of Motor Vehicles

- 4.5.1.2 Growing Demand for SLI Batteries from Industrial and Agricultural Applications

- 4.5.2 Restraints

- 4.5.2.1 Increasing Penetration of Alternative Battery Chemistries

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Flooded Battery

- 5.1.2 VRLA Battery

- 5.1.3 EBF Battery

- 5.2 End-User

- 5.2.1 Automotive

- 5.2.2 Others

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Nordic

- 5.3.2.7 Russia

- 5.3.2.8 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Thailand

- 5.3.3.6 Malaysia

- 5.3.3.7 Indonesia

- 5.3.3.8 Vietnam

- 5.3.3.9 Rest of Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 Saudi Arabia

- 5.3.4.2 United Arab Emirates

- 5.3.4.3 South Africa

- 5.3.4.4 Egypt

- 5.3.4.5 Nigeria

- 5.3.4.6 Qatar

- 5.3.4.7 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Chile

- 5.3.5.4 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted & SWOT Analysis for Leading Players

- 6.3 Company Profiles

- 6.3.1 GS Yuasa International Ltd.

- 6.3.2 Exide Technologies

- 6.3.3 Amara Raja Energy & Mobility Limited

- 6.3.4 EnerSys

- 6.3.5 Leoch International Technology Limited? Inc.

- 6.3.6 East Penn Manufacturing Company

- 6.3.7 C&D Technologies Inc.?

- 6.3.8 Clarios International Inc.?

- 6.3.9 Trojan Battery Company

- 6.3.10 Crown Battery Manufacturing Company

- 6.4 List of Other Prominent Companies (Company Name, Headquarter, Relevant Products & Services, Contact Details, etc.)

- 6.5 Market Ranking Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increased Focus on Battery Recycling

- 7.2 Expansion in Emerging Markets for Both New Vehicles and After-Market Replacements

02-2729-4219

+886-2-2729-4219

SLI电池市场-全球产业规模、份额、趋势、机会和预测,按类型(富液式电池、增强型富液式电池)、应用、销售通路、地区和竞争格局划分,2021-2031年预测商用车SLI电池市场-全球产业规模、份额、趋势、机会及预测,依类型、应用、车辆类型、销售通路、地区及竞争格局划分,2021-2031年预测

SLI电池市场-全球产业规模、份额、趋势、机会和预测,按类型(富液式电池、增强型富液式电池)、应用、销售通路、地区和竞争格局划分,2021-2031年预测商用车SLI电池市场-全球产业规模、份额、趋势、机会及预测,依类型、应用、车辆类型、销售通路、地区及竞争格局划分,2021-2031年预测 SLI电池市场规模、份额和成长分析(按类型、应用、电压、容量和地区划分)-产业预测(2026-2033年)

SLI电池市场规模、份额和成长分析(按类型、应用、电压、容量和地区划分)-产业预测(2026-2033年) 美国 SLI 电池市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

美国 SLI 电池市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测 SLI 电池市场,按类型、按应用、按配销通路、按国家和地区 - 2025 年至 2032 年的行业分析、市场规模、市场份额和预测SLI 电池市场机会、成长动力、产业趋势分析和 2025 - 2034 年预测

SLI 电池市场,按类型、按应用、按配销通路、按国家和地区 - 2025 年至 2032 年的行业分析、市场规模、市场份额和预测SLI 电池市场机会、成长动力、产业趋势分析和 2025 - 2034 年预测 中东和非洲的 SLI 电池:市场占有率分析、行业趋势和成长预测(2025-2030 年)中国SLI电池:市场占有率分析、产业趋势/统计、成长预测(2025-2030)义大利SLI电池:市场占有率分析、产业趋势与成长预测(2025-2030年)印度的 SLI 电池:市场占有率分析、行业趋势/统计、成长预测 (2025-2030)

中东和非洲的 SLI 电池:市场占有率分析、行业趋势和成长预测(2025-2030 年)中国SLI电池:市场占有率分析、产业趋势/统计、成长预测(2025-2030)义大利SLI电池:市场占有率分析、产业趋势与成长预测(2025-2030年)印度的 SLI 电池:市场占有率分析、行业趋势/统计、成长预测 (2025-2030)

▼