|

市场调查报告书

商品编码

1636175

亚太地区电动车锂离子电池:市场占有率分析、产业趋势与成长预测(2025-2030)Asia-Pacific Lithium-ion Battery For Electric Vehicle - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

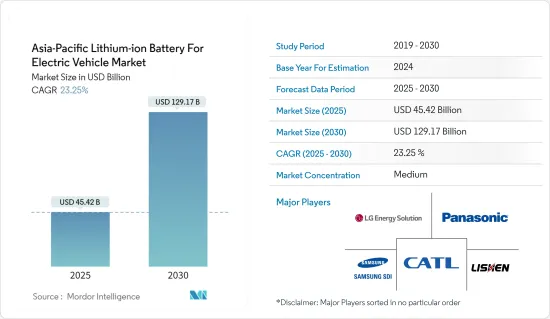

预计2025年亚太地区电动车锂离子电池市场规模为454.2亿美元,预测期内(2025-2030年)复合年增长率为23.25%,到2030年预计将达到1291.7亿美元。

主要亮点

- 锂离子电池价格的下降、电动车渗透率的提高以及政府的支持措施和倡议预计将在预测期内推动亚太电动汽车锂离子电池市场的成长。

- 另一方面,替代电池技术的兴起可能会阻碍预测期内的市场成长。

- 新兴国家混合动力电动车(HEV)应用对锂离子电池的需求预计将为亚太地区电动车锂离子电池市场创造巨大机会。

亚太地区电动车锂离子电池市场趋势

纯电动车 (BEV) 领域出现显着成长

- 纯电动车(BEV)通常也称为带有马达的电动车。纯电动车是全电动汽车,这意味着它们没有内燃机 (ICE)、燃料箱或排气管,而是依靠电力来推进。车辆的能量来自电池组并透过电网充电。纯电动车是零排放车,这意味着它们不会产生传统汽油动力汽车造成的有害废气和空气污染。

- 多年来,随着电动车,尤其是纯电动车 (BEV) 的发展和普及,亚太地区的汽车产业正在经历转型。随着技术的进步、政府的支持以及人们对环境问题认识的提高,纯电动车已成为应对气候变迁挑战和减少对石化燃料依赖的有前景的解决方案。

- 近年来,纯电动车的采用在全球范围内显着增长。电池技术的改进增加了续航里程,充电基础设施的普及也开始克服最初的进入障碍。此外,特斯拉、比亚迪、塔塔、丰田和本田等汽车製造商在推动纯电动车采用方面发挥关键作用,提供价格实惠的车款来吸引广大消费者。

- 根据国际能源总署(IEA)预测,2023年中国纯电动车(BEV)保有量约1,600万辆。同样,同年印度、日本和韩国的纯电动车保有量分别约为15万辆、29万辆和46万辆。同样,2023年中国纯电动车销量将超过540万辆。印度的纯电动车销量约为8.2万辆,而日本和韩国的纯电动车销量分别为8.8万辆和12万辆。随着纯电动车销量的持续成长,对锂离子电池等电动车电池的需求变得越来越重要。

- 此外,亚太地区是纯电动车最大的市场之一,也是全球最大的电动车电池製造地区。 2023年中国电动车电池需求量约为每年417GWh,约占全球需求量的54%,较2022年大幅成长32%以上。这凸显了该地区在电动车电池技术方面的主导地位的重要性。同样,根据国际能源总署(IEA)的数据,在中国的带动下,亚太地区的锂离子电池製造能力预计在未来几年将大幅成长。该机构预计,中国锂离子电池製造能力将从2022年的约1.20太瓦时增加到2030年的4.65太瓦时。

- 为了加速纯电动车的普及,各国正实施各种措施和奖励。例如,为了减少电动车对先进化学电池(ACC)的进口依赖,印度政府于2021年初核准了针对ACC国内製造的生产挂钩奖励(PLI)计画。该计划五年内总成本为 21.2 亿美元。该计划设想在日本建立具有竞争力的ACC电池製造系统(50GWh)。此外,5GWh利基ACC技术也被纳入该计划。这些措施支持了电动车应用对锂离子电池的需求。

- 此外,由于电动车普及率的提高以及政府加速电动车使用的倡议,预计泰国、印尼、新加坡、马来西亚和菲律宾等东南亚国家锂离子电池的采用将迅速增加。例如,印尼有一个雄心勃勃的目标,即到2025年电动车占所有汽车销量的20%,印尼政府的目标是到2030年在国内生产60万辆电动车。这些目标转化为电动车供应链(包括锂离子电池市场)内的各种里程碑。

- 2024年初,泰国电动车委员会将推出第二阶段电动车封装EV3,以促进电动车产业的持续发展,并鼓励新参与企业在泰国投资电动车製造5年核准,为期四年(2024-2027年)。该包装旨在鼓励涵盖整个电动车产业生态系统的投资。作为一揽子计划的一部分,泰国政府根据车型和电池容量列出了购买电动车、电动皮卡和电动摩托车的补贴。自2017年以来,由于持续的电动车推广包装,泰国已在电动车产业投资18亿美元用于纯电动车、纯电动两轮车、电动车零件和充电站的製造。

- 因此,由于上述因素,BEV细分市场很可能在预测期内主导电动车(EV)锂离子电池市场。

印度正在经历快速成长

- 印度已成为锂离子电池成长最快的市场之一,大力推动电动车 (EV) 的采用。例如,根据国际能源总署(IEA)的数据,2023年印度纯电动车(BEV)销量将达到约82,000辆,较2022年成长70%以上。此外,印度政府的目标是到2030年,新登记的私家车30%、巴士40%、商用车70%、二轮车和三轮车80%为电动车。由于这些因素,未来对锂离子电池等电动车电池的需求可能会大幅增加。

- 此外,政府还采取了各种措施和奖励,鼓励从传统内燃机汽车转向电动车,大大增加了对锂离子电池的需求。 FAME(混合动力汽车和电动车的更快采用和製造)等倡议使印度在充电基础设施、电池製造和电动车购买者补贴方面进行了大量投资,我们正在创造一个有利于市场成长的环境。

- 最近,2024 年 3 月,印度政府核准了一项价值 5 亿美元的新电动车计划,旨在吸引全球电动车公司的投资并将印度定位为领先的电动车製造中心提供了奖励。其他目标包括为印度消费者提供先进的电动车车型、扩大印度製造生态系统、降低生产成本以及培育具有竞争力的国内汽车製造业等。

- 许多国内外公司正在投资印度的锂离子电池市场,旨在利用对能源储存不断增长的需求以及向永续解决方案的转变。例如,2022年4月,电池巨头Exide Industries宣布计画投资约7.18亿美元在卡纳塔克邦建立锂离子电池製造工厂。第一阶段将在 2024 年运作6GWh 锂离子电池製造工厂,并在未来几年内逐步扩建至 12GWh 综合锂离子电池工厂。

- 此外,2023 年 4 月,电池技术新兴企业Log9 Materials 在班加罗尔贾库尔开设了该国第一家锂离子电池製造工厂。该工厂初始产能为50MWh。该公司还计划在2025年第一季将锂离子电池产能扩大至1GWh,电池组产能扩大至2GWh。

- 总体而言,由于庞大的消费群、支援措施以及电池製造的不断进步,印度电动车(EV)锂离子电池市场预计将在未来几年进一步成长。

亚太地区电动汽车锂离子电池产业概况

亚太地区电动车锂离子电池市场已腰斩。该市场的主要企业包括(排名不分先后)松下公司、宁德时代新能源科技有限公司、天津力神电池股份有限公司、三星SDI和LG能源解决方案有限公司。

其他好处

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 调查范围

- 市场定义

- 研究场所

第 2 章执行摘要

第三章调查方法

第四章市场概况

- 介绍

- 2029年之前的市场规模与需求预测(单位:美元)

- 最新趋势和发展

- 政府法规和措施

- 市场动态

- 促进因素

- 锂离子电池价格下降

- 电动车的扩张

- 政府支持措施和倡议

- 抑制因素

- 新的替代电池技术

- 促进因素

- 供应链分析

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间敌对关係的强度

第五章市场区隔

- 按车型

- 客车

- 商用车

- 其他(摩托车、Scooter等)

- 依推进类型

- 纯电动车(BEV)

- 插电式混合动力汽车(PHEV)

- 混合动力电动车(HEV)

- 按地区

- 印度

- 中国

- 日本

- 韩国

- 泰国

- 印尼

- 越南

- 其他亚太地区

第六章 竞争状况

- 併购、合资、联盟、协议

- 主要企业策略及SWOT分析

- 公司简介

- Panasonic Corporation

- Samsung SDI Co. Ltd

- Contemporary Amperex Technology Co. Ltd(CATL)

- BYD Company Limited

- Tianjin Lishen Battery Joint-Stock Co. Ltd

- Trontek Electronics Pvt. Ltd

- Greenfuel Energy Solutions Pvt. Ltd

- LG Energy Solution Ltd

- SK Innovation Co Ltd

- AESC Group Ltd

- Tesla Inc.

- 其他知名公司名单(公司名称、总部地点、相关产品及服务、联络等)

- 市场排名分析

第七章 市场机会及未来趋势

- 电动车采用固体锂离子电池

The Asia-Pacific Lithium-ion Battery For Electric Vehicle Market size is estimated at USD 45.42 billion in 2025, and is expected to reach USD 129.17 billion by 2030, at a CAGR of 23.25% during the forecast period (2025-2030).

Key Highlights

- Declining lithium-ion battery prices, the increasing adoption of electric vehicles, and supportive government policies and initiatives are expected to drive the growth of the Asia-Pacific lithium-ion battery for electric vehicle market over the medium term of the forecast period.

- On the other hand, emerging alternative battery technologies are likely to hinder market growth during the forecast period.

- Nevertheless, the need for lithium-ion batteries for hybrid electric vehicle (HEV) applications in emerging economies is expected to create vast opportunities for lithium-ion batteries for the electric vehicle market in Asia-Pacific.

Asia-Pacific Lithium-ion Battery for Electric Vehicle Market Trends

The Battery Electric Vehicle (BEV) Segment to Witness Significant Growth

- Battery electric vehicles (BEVs) are also commonly referred to as electric vehicles with an electric motor. BEVs are fully electric vehicles that typically do not include an internal combustion engine (ICE), fuel tank, or exhaust pipe and rely on electricity for propulsion. The vehicle's energy comes from a battery pack, which is recharged from the grid. BEVs are zero-emission vehicles, as they do not generate harmful tailpipe emissions or air pollution hazards caused by traditional gasoline-powered vehicles.

- The automotive industry in Asia-Pacific has been transforming over the years, with electric vehicles, particularly battery electric vehicles (BEVs), gaining momentum and popularity. With growing technological advancements, government support, and increasing environmental concerns, BEVs have emerged as a promising solution to address the challenges of climate change and reduce reliance on fossil fuels.

- In recent years, the adoption of battery-electric vehicles has grown significantly worldwide. The improvement of battery technology has led to extended driving ranges and a surge in charging infrastructure that is helping overcome the initial entry barriers. Further, automakers such as Tesla, BYD, Tata, Toyota, and Honda have been playing a vital role in popularizing BEVs, offering affordable models that appeal to a broader range of consumers.

- According to the International Energy Agency (IEA), the battery electric vehicle (BEV) car stocks in China stood at around 16 million units in 2023. Similarly, in the same year, countries such as India, Japan, and South Korea had approximately 0.15 million, 0.29 million, and 0.46 million units of BEV car stock, respectively. Similarly, in 2023, BEV sales in China stood at over 5.4 million. India sold around 82,000 units of BEV cars, while Japan and South Korea sold 88,000 and 120,000 units of BEV cars, respectively. As the sales of BEVs continue to rise, the demand for EV batteries, such as lithium-ion batteries, has become increasingly vital.

- Moreover, being one of the largest markets for BEV vehicles, Asia-Pacific is also the largest EV battery manufacturing region in the world. China led from the front with an EV battery demand of about 417 GWh per year, or about 54% of the world demand in 2023, recording a surge of over 32% from 2022. This highlights the importance of the region's dominance in EV battery technologies. Similarly, as per the International Energy Agency (IEA), the lithium-ion battery manufacturing capacity in the Asia-Pacific region is expected to grow significantly in the coming years, with China leading the way. The agency estimated that the Chinese lithium-ion battery manufacturing capacity will rise to 4.65 TWh in 2030 from around 1.20 TWh in 2022.

- To accelerate the adoption of BEVs, countries have been implementing various initiatives and incentives. For example, to reduce dependency on imported advanced chemistry cell (ACC) batteries for electric vehicles, the Indian government approved a Production Linked Incentive (PLI) Scheme in early 2021 for the manufacturing of ACCs in the country. The total outlay of the Scheme is USD 2.12 billion for five years. The scheme envisages establishing a competitive ACC battery manufacturing setup in the country (50 GWh). In addition, 5 GWh of niche ACC technologies is also covered under the scheme. Such initiatives are supporting the demand for lithium-ion batteries for EV applications.

- Further, Southeast Asian countries such as Thailand, Indonesia, Singapore, Malaysia, and the Philippines are expected to see rapid growth in the adoption of lithium-ion batteries due to the increasing prevalence of EVs and government initiatives to accelerate EV use. For example, Indonesia has an ambitious target of having EVs make up 20% of all car sales by 2025, and the Indonesian government aims for 600,000 EVs to be domestically produced by 2030. Such targets are translated into different milestones within the EV supply chain, including the lithium-ion batteries market.

- In early 2024, the EV Board in Thailand approved the second phase of the EV Package, known as EV 3.5, for four years (2024-2027) to promote the EV industry's continuous progress and facilitate investment opportunities in EV manufacturing in Thailand for new players. The package aims to boost investments covering the entire EV industry ecosystem. As part of the package, the Thai government will offer subsidies for the purchase of electric cars, electric pickup trucks, and electric motorcycles based on the vehicle types and battery capacities. Thailand's continuous EV promotion package since 2017 has resulted in investments in the EV industry worth USD 1.8 billion in manufacturing BEVs, battery electric motorcycles, EV parts and components, and charging stations.

- Therefore, due to the factors mentioned above, the BEV segment is likely to dominate the lithium-ion battery for electric vehicle (EV) market during the forecast period.

India to Witness Fastest Growth

- India is emerging as one of the fastest-growing markets for lithium-ion batteries, driven by a strong push toward the adoption of electric vehicles (EVs). For example, according to the International Energy Agency (IEA), battery electric vehicle (BEV) sales in India reached around 82,000 units in 2023, an increase of over 70% from 2022. Additionally, the Indian government aims for an EV target of 30% of newly registered private cars, 40% of buses, 70% of commercial cars, and 80% of 2-wheelers and 3-wheelers by 2030. These are likely to create a substantial demand for EV batteries, such as lithium-ion batteries, in the coming years.

- Besides, the government has also implemented a range of policies and incentives to encourage the shift from traditional internal combustion engine vehicles to EVs, significantly boosting the demand for lithium-ion batteries. With initiatives such as the Faster Adoption and Manufacturing of Hybrid and Electric Vehicles (FAME) scheme, India is making substantial investments in charging infrastructure, battery manufacturing, and subsidies for EV buyers, creating a conducive environment for market growth.

- More recently, in March 2024, the Indian government approved a new USD 500-million-worth EV Policy, offering a range of incentives to draw investments from global EV companies and position India as a prime manufacturing hub for state-of-the-art EVs. Other objectives include providing Indian consumers with access to cutting-edge EV models, expanding the Make in India ecosystem, lowering costs of production, and fostering a competitive domestic auto manufacturing industry.

- Various local and international players are investing in the Indian lithium-ion battery market, aiming to capitalize on the country's burgeoning energy storage needs and its transition toward sustainable solutions. For example, in April 2022, battery behemoth Exide Industries announced plans to invest about USD 718 million to set up a lithium-ion cell manufacturing plant in Karnataka. In its first phase, a 6 GWh lithium-ion cell manufacturing facility is likely to become operational by 2024, gradually expanding to a 12 GWh capacity integrated lithium-ion battery facility over the next few years.

- Furthermore, in April 2023, the battery technology startup Log9 Materials inaugurated the country's first lithium-ion cell manufacturing facility in Jakkur, Bengaluru. The plant has an initial capacity of 50 MWh. The company is also working on expanding its lithium-ion cell manufacturing capacity to 1 GWh and its battery pack manufacturing capacity to 2 GWh by the first quarter of 2025.

- Overall, with a large consumer base, supportive policies, and increasing progress in the batteries manufacturing, the lithium-ion battery for electric vehicle (EV) market in India is poised for further growth in the coming years.

Asia-Pacific Lithium-ion Battery for Electric Vehicle Industry Overview

The Asia-Pacific lithium-ion battery market for electric vehicles is semi-fragmented. Some of the key players in the market (not in any particular order) include Panasonic Corporation, Contemporary Amperex Technology Co. Limited, Tianjin Lishen Battery Joint-Stock Co. Ltd, Samsung SDI Co. Ltd, and LG Energy Solution Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD until 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Declining Lithium-ion Battery Prices

- 4.5.1.2 Increasing Adoption of Electric Vehicles

- 4.5.1.3 Supportive Government Policies and Initiatives

- 4.5.2 Restraints

- 4.5.2.1 Emerging Alternative Battery Technologies

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Vehicle Type

- 5.1.1 Passenger Vehicles

- 5.1.2 Commercial Vehicles

- 5.1.3 Other Vehicle Types (Bikes, Scooters, etc.)

- 5.2 By Propulsion Type

- 5.2.1 Battery Electric Vehicle (BEV)

- 5.2.2 Plug-in Hybrid Electric Vehicle (PHEV)

- 5.2.3 Hybrid Electric Vehicle (HEV)

- 5.3 By Geography

- 5.3.1 India

- 5.3.2 China

- 5.3.3 Japan

- 5.3.4 South Korea

- 5.3.5 Thailand

- 5.3.6 Indonesia

- 5.3.7 Vietnam

- 5.3.8 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted & SWOT Analysis for Leading Players

- 6.3 Company Profiles

- 6.3.1 Panasonic Corporation

- 6.3.2 Samsung SDI Co. Ltd

- 6.3.3 Contemporary Amperex Technology Co. Ltd (CATL)

- 6.3.4 BYD Company Limited

- 6.3.5 Tianjin Lishen Battery Joint-Stock Co. Ltd

- 6.3.6 Trontek Electronics Pvt. Ltd

- 6.3.7 Greenfuel Energy Solutions Pvt. Ltd

- 6.3.8 LG Energy Solution Ltd

- 6.3.9 SK Innovation Co Ltd

- 6.3.10 AESC Group Ltd

- 6.3.11 Tesla Inc.

- 6.4 List of Other Prominent Companies (Company Name, Headquarter, Relevant Products & Services, Contact Details, etc.)

- 6.5 Market Ranking Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Adoption of Solid-state Lithium-ion Batteries for Electric Vehicles

汽车锂离子电池市场:电池类型、驱动系统、电芯形状、容量范围、电压与容量、车辆类型、销售管道、最终用途 - 全球市场预测 2026-2032

汽车锂离子电池市场:电池类型、驱动系统、电芯形状、容量范围、电压与容量、车辆类型、销售管道、最终用途 - 全球市场预测 2026-2032 汽车锂离子电池市场规模、份额和成长分析(按类型、车辆类型、应用、容量和地区划分)—2026-2033年产业预测

汽车锂离子电池市场规模、份额和成长分析(按类型、车辆类型、应用、容量和地区划分)—2026-2033年产业预测 北美电动车锂离子电池:市场占有率分析、产业趋势和成长预测(2025-2030 年)中东和非洲电动车用锂离子电池:市场占有率分析、产业趋势和成长预测(2025-2030)欧洲电动车锂离子电池:市场占有率分析、产业趋势、成长预测(2025-2030)法国电动车用锂离子电池市场占有率分析、产业趋势、成长预测(2025-2030)电动汽车用锂离子电池:市场占有率分析、产业趋势、成长预测(2025-2030)英国电动车锂离子电池:市场占有率分析、产业趋势、成长预测(2025-2030)

北美电动车锂离子电池:市场占有率分析、产业趋势和成长预测(2025-2030 年)中东和非洲电动车用锂离子电池:市场占有率分析、产业趋势和成长预测(2025-2030)欧洲电动车锂离子电池:市场占有率分析、产业趋势、成长预测(2025-2030)法国电动车用锂离子电池市场占有率分析、产业趋势、成长预测(2025-2030)电动汽车用锂离子电池:市场占有率分析、产业趋势、成长预测(2025-2030)英国电动车锂离子电池:市场占有率分析、产业趋势、成长预测(2025-2030) 汽车用锂离子电池组的全球市场:产业分析,规模,占有率,成长,趋势,预测(2024年~2031年)

汽车用锂离子电池组的全球市场:产业分析,规模,占有率,成长,趋势,预测(2024年~2031年) 汽车用锂离子电池的印度市场评估:各类型,结构,各容量,各流通管道,各地区,机会,预测(2018年度~2032年度)

汽车用锂离子电池的印度市场评估:各类型,结构,各容量,各流通管道,各地区,机会,预测(2018年度~2032年度)