|

市场调查报告书

商品编码

1636421

法国电动车电池负极:市场占有率分析、产业趋势、成长预测(2025-2030)France Electric Vehicle Battery Anode - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

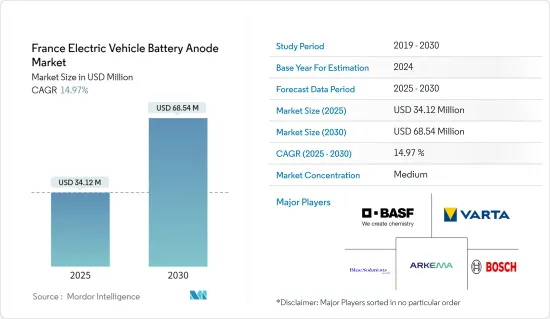

预计2025年法国电动车电池负极市场规模为3,412万美元,2030年预计将达6,854万美元,预测期内(2025-2030年)复合年增长率为14.97%。

主要亮点

- 从中期来看,电动车普及率的提高和阳极材料的技术进步预计将在预测期内推动电动车电池阳极的需求。

- 另一方面,先进的负极材料,尤其是那些仍处于实验阶段的材料,生产成本较高,这会显着抑制德国电动车电池负极市场的成长。

- 对回收和循环经济的日益关注为开发可持续阳极材料提供了机会,回收过程预计将在不久的将来为电动车电池阳极市场提供重大机会。

法国电动车电池负极市场趋势

锂离子电池类型主导市场

- 在德国,锂离子电池,尤其是电动车 (EV) 领域的锂离子电池,对于向永续交通转型至关重要。作为汽车产业的世界领导者,德国政府致力于推进和生产尖端的电动车电池技术,特别重视锂离子电池的关键零件负极。

- 负极对于锂离子电池至关重要,影响容量、寿命和充电速度。此外,这种电池的成本对电动车的定价有重大影响。因此,国内电电动车电池负极市场是更广泛的锂离子电池领域中最重要的市场。

- 例如,根据彭博新能源财经报道,2023年电池价格将降至139美元/kWh,较上年下降13%。持续的技术进步和製造改进预计将进一步将电池组价格在 2025 年降低至 113 美元/kWh,在 2030 年降低至 80 美元/kWh。由于製造效率的提高,锂离子电池的产量增加,预计电池负极的单价将在预测期内下降。

- 此外,阳极材料的技术创新正在提高锂离子电池的性能,使电动车相对于传统内燃机汽车的竞争力日益增强。该地区各国政府正积极支持电动车电池创新,各大公司最近都启动了增强电动车电池负极材料的计划。

- 例如,2023 年 12 月,HPQ Silicon Inc. 宣布其位于法国的子公司 NOVACIUM SAS 获得了 90,000 欧元(约 99,000 美元)的法国科技新兴补助金。这笔津贴旨在支持加强先进二氧化硅基电池负极材料整个价值链的计划。锂电池领域的一个显着趋势是在石墨复合电极中使用 5% 至 10% 的氧化硅 (SiOx) 添加剂。这些进步将支持该地区先进的电池生产,并推动未来几年电池製造中对负极的需求。

- 在法国,负极材料的主要应用是电动车(EV)的锂离子电池。这些电池为从乘用车到商用车和公共运输的各种电动车提供动力。主要企业启动了多个电池製造计划,以满足所有电动车类别快速成长的需求。

- 例如,2024 年 5 月,法国 Blue Solutions 宣布计划在法国东部建造一座超级工厂,投资约 20 亿欧元(21.7 亿美元)。该工厂的目标是生产一种新型电动车固态电池,快速充电时间为 20 分钟,预计 2030 年开始生产。预计此类措施将推动锂离子电池作为清洁能源解决方案的采用,并在预测期内推动对负极材料的需求。

- 这些计划和创新将扩大该地区的锂离子电池产量,并在未来几年大幅增加对电动车电池阳极的需求。

扩大电动车普及率正在推动市场发展

- 在法国,由于消费者偏好的变化和强制性法规,对电动车(EV)的需求迅速增加,推动了电动车电池阳极市场的发展。这一势头得到了政府激励措施和电池开发技术进步的进一步支持,为市场的持续扩张奠定了基础。

- 近年来,该地区电动车的销量激增。例如,国际能源总署(IEA)报告称,2023年法国电动车销量为47万辆,较2022年成长38.2%。预测全部区域电动车销量将大幅成长,电池负极材料的需求也会随之增加。

- 此外,法国政府旨在遏制碳排放和支持电动车的补贴和奖励在推动市场方面发挥关键作用。这些努力包括对电动车购买的财政支持、税收优惠以及增加充电基础设施的投资。总的来说,这些不仅支持了电动车的普及,而且还增加了对电池负极的需求,而电池负极对于锂离子电池的生产至关重要。

- 例如,2024年5月,法国政府与顶级汽车製造商签署协议,制定了2027年销售80万辆电动车的雄心勃勃的目标。此外,政府也拨款15亿欧元(约16亿美元),透过各种措施加强电动车的生产和采购。这些战略倡议不仅将加速电动车的生产,还将扩大对电池阳极材料的需求。

- 此外,向电动车的过渡对于实现零净碳排放的目标至关重要。该地区的主要企业正在积极投资和推出计划,以提高电动车产量。

- 例如,中国着名电动车製造商比亚迪于2024年6月宣布,计划在法国建立电动车生产设施,并在全国推出插电式混合动力汽车(PHEV)。该设施预计将于年终投入营运。这些努力将支持电动车的生产,进而扩大对电池和阳极的需求。

- 总而言之,这些共同努力和策略预计将在短期内加强电动车销售,并相应增加对负极电池材料的需求。

法国电动车电池负极产业概况

法国电动车电池负极市场温和。主要企业(排名不分先后)包括BASF SE、Varta AG、Blue Solutions、Arkema SA 和 Robert Bosch GmbH。

其他好处

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 调查范围

- 市场定义

- 研究场所

第 2 章执行摘要

第三章调查方法

第四章市场概况

- 介绍

- 2029年之前的市场规模与需求预测(单位:美元)

- 最新趋势和发展

- 政府法规和措施

- 市场动态

- 促进因素

- 电动车的扩张

- 负极材料的进展

- 抑制因素

- 生产成本高

- 促进因素

- 供应链分析

- PESTLE分析

- 投资分析

第五章市场区隔

- 电池类型

- 锂离子电池

- 铅酸电池

- 其他的

- 材料类型

- 锂

- 石墨

- 硅

- 其他的

第六章 竞争状况

- 併购、合资、联盟、协议

- 主要企业策略

- 公司简介

- BASF SE

- Varta AG

- Blue Solutions

- Arkema SA

- Robert Bosch GmbH

- TotalEnergies SE

- STMicroelectronics

- NAWA Technologies

- Solvay SA

- 其他知名公司名单

- 市场排名分析

第七章 市场机会及未来趋势

- 循环经济和回收

简介目录

Product Code: 50003596

The France Electric Vehicle Battery Anode Market size is estimated at USD 34.12 million in 2025, and is expected to reach USD 68.54 million by 2030, at a CAGR of 14.97% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, the growing EV adoption and technological advancements in anode materials are expected to drive the demand for electric vehicle battery anode during the forecast period.

- On the other hand, the high production costs of advanced anode materials, particularly those that are still in the experimental phase can significantly restrain the growth of the Germany electric vehicle battery anode market.

- Nevertheless, the growing focus on recycling and the circular economy presents opportunities for developing sustainable anode materials and the recycling processe are expected to create significant opportunities for electric vehicle battery anode market in the near future.

France Electric Vehicle Battery Anode Market Trends

Lithium-Ion Battery Type Dominate the Market

- In Germany, the lithium-ion battery, particularly in the electric vehicle (EV) sector, is crucial to the nation's transition towards sustainable transportation. As a global automotive leader, Germany's government is dedicated to advancing and producing state-of-the-art EV battery technologies, with a special focus on the anode, a vital component of lithium-ion batteries.

- The anode is essential in lithium-ion batteries, influencing their capacity, lifespan, and charging speed. Moreover, the cost of these batteries significantly affects electric vehicle pricing. Consequently, the nation's EV battery anode market is of paramount importance in the broader lithium-ion battery landscape.

- For example, a Bloomberg NEF report highlighted that in 2023, battery prices fell to USD 139/kWh, marking a 13% drop from the prior year. With ongoing technological advancements and manufacturing improvements, battery pack prices are projected to further decline, estimating costs at USD 113/kWh by 2025 and USD 80/kWh by 2030. As lithium-ion battery production ramps up due to enhanced manufacturing efficiencies, the unit cost of battery anodes is expected to decrease during the forecast period.

- Moreover, innovations in anode materials are boosting lithium-ion battery performance, making EVs increasingly competitive against traditional internal combustion engine vehicles. Governments in the region are actively championing EV battery innovations, and major companies have recently embarked on projects to enhance anode materials in EV batteries.

- For instance, in December 2023, HPQ Silicon Inc. revealed that its affiliate, NOVACIUM SAS, based in France, obtained a French Tech Emergence Grant of EUR 90,000 (around USD 99,000). This grant is intended to support projects that enhance the entire value chain of advanced SiOx-based anode materials for batteries. A notable trend in the lithium battery domain is the use of 5% to 10% silicon oxide (SiOx) additives in graphite composite electrodes. Such advancements are poised to boost sophisticated battery production in the region and elevate the demand for anodes in battery manufacturing in the years ahead.

- In France, the primary use of anode materials is in lithium-ion batteries for electric vehicles (EVs). These batteries power a range of EVs, from passenger cars to commercial vehicles and public transport. Leading French companies have initiated multiple battery manufacturing projects to meet the surging demand across all EV categories.

- For example, in May 2024, Blue Solutions, a French firm, unveiled plans for a gigafactory in eastern France, with an investment of about 2 billion euros (USD 2.17 billion). This facility aims to produce a new solid-state battery for EVs, boasting a rapid 20-minute charging time, with production slated to commence by 2030. Such initiatives are set to bolster the adoption of lithium-ion batteries as a clean energy solution and heighten the demand for anode materials in the forecast period.

- Thus, these projects and innovations are poised to amplify lithium-ion battery production in the region and escalate the demand for EV battery anodes in the coming years.

Growing EV adoption drives the Market

- In France, the surging demand for electric vehicles (EVs), driven by changing consumer preferences and regulatory mandates, is propelling the EV battery anode market. This momentum is further bolstered by government incentives and technological strides in battery development, setting the stage for continued market expansion.

- Sales of electric vehicles in the region have seen a meteoric rise in recent years. For instance, the International Energy Agency (IEA) reported that in 2023, France sold 0.47 million electric vehicles, marking a 38.2% increase from 2022. Projections indicate a substantial uptick in electric vehicle sales across the region, subsequently amplifying the demand for battery anode materials.

- Moreover, the French government's subsidies and incentives, aimed at curbing carbon emissions and championing electric mobility, play a crucial role in propelling the market. These initiatives encompass financial backing for EV purchases, tax incentives, and bolstered investments in charging infrastructure. Collectively, they not only boost electric vehicle adoption but also heighten the demand for battery anodes essential for lithium-ion battery production.

- For example, in May 2024, the French government inked a deal with top car manufacturers, setting an ambitious target of 800,000 electric vehicle sales by 2027, a significant leap from 200,000 in 2022. Additionally, the government allocated a substantial 1.5 billion euros (approximately USD 1.6 billion) to bolster electric vehicle production and purchases through diverse initiatives. Such strategic moves are poised to not only accelerate EV production but also amplify the demand for battery anode materials.

- Furthermore, the transition to electric vehicles is pivotal in realizing net-zero carbon emission aspirations. Major companies in the region are actively investing and launching projects to bolster electric vehicle production.

- For instance, in June 2024, BYD Company, a prominent Chinese electric vehicle manufacturer, declared its plans to establish an EV production facility in France, with intentions to introduce plug-in hybrid vehicles (PHEVs) nationwide. This facility is slated to commence operations by the end of next year. Such endeavors are set to boost EV production and, in turn, escalate the demand for battery anodes.

- In summary, these concerted efforts and strategies are anticipated to bolster EV sales and subsequently elevate the demand for anode battery materials in the foreseeable future.

France Electric Vehicle Battery Anode Industry Overview

The France electric vehicle battery anode market is moderate. Some of the key players (not in particular order) are BASF SE, Varta AG, Blue Solutions, Arkema S.A., Robert Bosch GmbH, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Growing Adoption of Electric Vehicles

- 4.5.1.2 Advancements in Anode Materials

- 4.5.2 Restraints

- 4.5.2.1 High Production Costs

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 PESTLE Analysis

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Battery Type

- 5.1.1 Lithium-Ion Batteries

- 5.1.2 Lead-Acid Batteries

- 5.1.3 Others

- 5.2 Material Type

- 5.2.1 Lithium

- 5.2.2 Graphite

- 5.2.3 Silicon

- 5.2.4 Others

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 BASF SE

- 6.3.2 Varta AG

- 6.3.3 Blue Solutions

- 6.3.4 Arkema S.A.

- 6.3.5 Robert Bosch GmbH

- 6.3.6 TotalEnergies SE

- 6.3.7 STMicroelectronics

- 6.3.8 NAWA Technologies

- 6.3.9 Solvay S.A.

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Circular Economy and Recycling

02-2729-4219

+886-2-2729-4219

锂离子电池负极市场:2026-2032 年全球市场预测,材料类型、製造技术、电池形式、表面处理、回收成分、形状、应用和分销管道划分。

锂离子电池负极市场:2026-2032 年全球市场预测,材料类型、製造技术、电池形式、表面处理、回收成分、形状、应用和分销管道划分。 全球硅阳极锂离子电池市场规模、份额、趋势及成长分析报告(2026-2034)

全球硅阳极锂离子电池市场规模、份额、趋势及成长分析报告(2026-2034) 锂离子电池负极材料市场规模、份额及成长分析(按电池产品、製造技术、材料、应用和地区划分)-产业预测(2026-2033)

锂离子电池负极材料市场规模、份额及成长分析(按电池产品、製造技术、材料、应用和地区划分)-产业预测(2026-2033) 硅负极锂离子电池市场规模、份额及成长分析(依产品类型、应用、电池配置、容量及地区划分)-2026-2033年产业预测

硅负极锂离子电池市场规模、份额及成长分析(依产品类型、应用、电池配置、容量及地区划分)-2026-2033年产业预测 全球锂离子电池阳极市场

全球锂离子电池阳极市场 锂离子电池阳极市场(按材料、电池产品、最终用途、生产技术及地区划分)预测(至 2030 年)

锂离子电池阳极市场(按材料、电池产品、最终用途、生产技术及地区划分)预测(至 2030 年) 北美电动车电池负极:市场占有率分析、产业趋势、成长预测(2025-2030)南美洲电动车电池负极:市场占有率分析、产业趋势、成长预测(2025-2030)德国电动车电池负极:市场占有率分析、产业趋势、成长预测(2025-2030)

北美电动车电池负极:市场占有率分析、产业趋势、成长预测(2025-2030)南美洲电动车电池负极:市场占有率分析、产业趋势、成长预测(2025-2030)德国电动车电池负极:市场占有率分析、产业趋势、成长预测(2025-2030) 锂离子电池用硅负极 - 专利形势的分析(2024年)

锂离子电池用硅负极 - 专利形势的分析(2024年)

▼