|

市场调查报告书

商品编码

1636545

亚太地区充电电池:市场占有率分析、产业趋势与统计、成长预测(2025-2030)Asia-Pacific Rechargeable Battery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

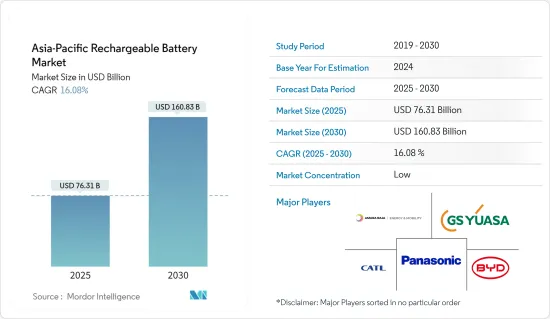

亚太地区充电电池市场规模预估至2025年为763.1亿美元,预估至2030年将达1,608.3亿美元,预测期间(2025-2030年)复合年增长率为16.08%。

主要亮点

- 从中期来看,锂离子电池价格的下降、电动车渗透率的提高以及可再生能源领域的扩张预计将在预测期内推动亚太二次电池市场的发展。

- 另一方面,原材料供需不匹配预计将阻碍预测期内的市场成长。

- 由于新电池技术和先进电池化学物质的不断发展,亚太二次电池市场可能会产生巨大的商机。

- 在该地区的国家中,由于电动车、家用电子电器产品和可再生计划越来越多地采用能源储存系统,印度预计将出现强劲成长。

亚太二次电池市场趋势

锂离子电池成长迅速

- 在各种电池技术中,锂离子电池(LIB)在二次电池市场中占据主导地位,预计在预测期内将快速成长。锂离子电池因其优越的容量重量比、较长的保质期、较低的维护要求以及不断下降的价格而变得比其他类型的电池更受欢迎。

- 与传统铅酸电池相比,锂离子电池具有多项技术优势。铅酸电池通常可持续 400 到 500 次循环,而可充电锂离子电池可持续超过 5,000 次循环。此外,锂离子电池需要较少的维护和更换。它还可以在整个放电週期中保持稳定的电压,从而提高所连接电气组件的效率。

- 亚太地区的主要企业正在大力投资锂离子电池,并专注于研发和规模经济。这种竞争的加剧正在压低锂离子电池的价格。由于技术进步、製造优化以及原材料成本降低,锂离子电池的平均价格已从2013年的780美元/千瓦时暴跌至2023年的139美元/千瓦时。预计2025年将进一步降至113美元/度左右,2030年将进一步降至80美元/度左右。按地区划分,2023年中国电池组平均价格将创下最低纪录,为126美元/度。中国国内激烈的竞争促使製造商增加产量,以满足快速成长的电池需求。电池成本的这种下降趋势很可能使锂电池成为所有电池中的有利选择。

- 从历史上看,锂离子电池曾为行动电话和笔记型电脑等家用电子电器产品提供动力。近年来,它已被应用于混合动力汽车、各类纯电动车(BEV)、可再生能源中的电池能源储存系统(BESS)等。

- 例如,电网规模的电池储能係统对于实现净零排放至关重要。我们列出了从短期平衡和电网稳定性到长期能源储存和断电后恢復的基本服务。国际能源总署(IEA)预测,电网规模的电池将引领能源储存的成长。 2022年,每年系统规模蓄电池扩容1,121万千瓦中,中国占比将超过42%,总合超过481万千瓦。中国计划在 2025 年安装超过 30 GW 的 BESS(主要使用锂离子电池),中国的雄心壮志表明 BESS 的未来将蓬勃发展,从而导致亚太地区对二次电池的需求激增。

- 2023年12月,韩国财政部宣布计画未来5年向锂电池产业注入38兆韩元。韩国将设立1兆韩元的促进基金,并投资736亿韩元的研发费用,以加强国内锂电池生产所需的矿产蕴藏量。这些倡议,再加上培育电池再利用和回收生态系统的努力,将重振锂离子电池产业并强化二次电池市场。

- 2024年3月,松下集团宣布与印度石油公司(IOCL)成立合资企业,生产圆柱形锂离子电池。该合资企业基于印度对两轮车、三轮车和 BESS 的需求预测,凸显了该地区锂离子二次电池製造的成长趋势。

- 由于锂离子电池重量轻、充电快、充电週期长、成本下降和工业进步,预计在预测期内将成为亚太地区成长最快的二次电池市场。

印度正在经历显着的成长

- 在电动车 (EV) 普及率不断提高、家用电子电器需求迅速增长以及政府支持能源储存解决方案的倡议的推动下,印度可充电电池市场有望实现显着增长。对市场扩张至关重要的二次电池需求激增,很大程度上是由于家用电子电器领域智慧型手机、笔记型电脑和其他行动装置的激增。

- 此外,印度政府大力推广电动车,这增加了对二次电池的需求,特别是在电动车领域。国际能源总署 (IEA) 的资料凸显了这一趋势,预计 2023 年印度纯电动车 (BEV) 销量将激增至 82,000 辆左右,与前一年同期比较大幅增长 70%。印度政府制定了雄心勃勃的目标,即到 2030 年,新登记的私家车 30%、巴士 40%、商用车 70%、两轮和三轮车 80% 为电动车。的需求预计将快速成长。

- 为了加强国内生产并减少电动车电池的进口依赖,印度政府于2021年初推出了生产连结奖励(PLI)计画。该计划将在五年内投资21.2亿美元,旨在在该国建立具有竞争力的ACC电池製造系统,产能达到50 GWh,另外5 GWh的利基ACC技术将重点发展。 PLI计划提供每1KWh补贴以及根据实际销售增加价值额实现率确定的产量挂钩补贴。到 2022 年,信实新能源太阳能有限公司、现代全球汽车有限公司、Ola Electric Mobility Private Limited 和 Rajesh Exports Limited 等四家知名公司将获得该计划的激励措施,政府承诺支持扩大国内电池生产。了。

- 利用印度对能源储存不断增长的需求以及向永续解决方案的转变,国内外参与企业正在大力投资印度充电电池市场。例如,2022年4月,电池领域领导企业Exide Industries宣布计画在卡纳塔克邦兴建锂离子电池製造工厂,投资约7.18亿美元。该工厂的初始产能为 6GWh,预计将于 2024 年投入运作,并计划在未来几年内扩建至 12GWh 的综合锂离子电池工厂。

- 另一个值得注意的倡议是,电池技术新兴企业Log9 Materials 于 2023 年 4 月在班加罗尔贾库尔开设了印度第一家锂离子电池製造工厂。 Log9 的产能从 50MWh 开始,雄心勃勃地规划到 2025 年第一季将电池製造能力扩大到 1GWh,电池组製造能力扩大到 2GWh。 2024 年 3 月,GoodEnough Energy 宣布计划于 2024 年 10 月在查谟和克什米尔开始营运印度第一家电池超级工厂。 GoodEnough 的工厂投资15 亿印度卢比(1,807 万美元)建造初始7GWh 工厂,并计划到2027 年投资30 亿印度卢比(3,700 万美元)将产能增加到20GWh,GoodEnough 的工厂将产生重大影响,并有可能排放重大影响。该超级工厂符合印度雄心勃勃的目标,即到 2030 年将可再生能源产能提高到 500 吉瓦,较 2023 年的 176 吉瓦左右大幅成长。为了进一步加强这些努力,印度政府正在向致力于推广电池储存计划的公司提供价值 4.52 亿美元的激励措施。

- 凭藉庞大的消费群、政府的支持措施以及电池製造的进步,印度充电电池市场在可预见的未来将实现强劲成长。

亚太充电电池产业概况

亚太地区充电电池市场较为分散。该市场的主要企业包括(排名不分先后)松下公司、宁德时代新能源科技有限公司、比亚迪有限公司、GS汤浅公司和Amara Raja Energy & Mobility Ltd.。

其他好处

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 调查范围

- 市场定义

- 研究场所

第 2 章执行摘要

第三章调查方法

第四章市场概况

- 介绍

- 2029年之前的市场规模与需求预测(单位:美元)

- 最新趋势和发展

- 政府法规和措施

- 市场动态

- 促进因素

- 电动车的扩张

- 锂离子电池成本下降

- 抑制因素

- 原料供需不匹配

- 促进因素

- 供应链分析

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代产品/服务的威胁

- 竞争公司之间的敌对关係

- 投资分析

第五章市场区隔

- 科技

- 铅酸电池

- 锂离子

- 其他技术(NiMh、Nicd 等)

- 目的

- 汽车电池

- 工业电池(用于电源、固定电池(电信、UPS、能源储存系统(ESS) 等)

- 可携式电池(家用电子电器产品等)

- 其他的

- 地区

- 印度

- 中国

- 日本

- 韩国

- 泰国

- 印尼

- 越南

- 其他亚太地区

第六章 竞争状况

- 併购、合资、联盟、协议

- 主要企业策略

- 公司简介

- Panasonic Corporation

- Contemporary Amperex Technology Co. Limited

- BYD Co.Ltd.

- GS Yuasa Corporation

- Samsung SDI Co. Ltd

- LG Chem Ltd.

- Clarios, LLC.

- Amara Raja Energy & Mobility Ltd

- Exide Industries Ltd

- Duracell Inc.

- Saft Groupe SA

- Tianjin Lishen Battery Joint-Stock Co. Ltd.

- Tesla Inc.

- 其他知名公司名单(公司名称、总部地点、相关产品及服务、联络等)

- 市场排名/份额(%)分析

第七章 市场机会及未来趋势

- 新型电池技术与先进电池化学材料的开发进展

简介目录

Product Code: 50004021

The Asia-Pacific Rechargeable Battery Market size is estimated at USD 76.31 billion in 2025, and is expected to reach USD 160.83 billion by 2030, at a CAGR of 16.08% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, declining lithium-ion battery prices, increasing adoption of electric vehicles, and the growing renewable energy sector are expected to drive the Asia-Pacific rechargeable battery market during the forecast period.

- On the other hand, the demand-supply mismatch of raw materials is expected to hinder the market's growth during the forecast period.

- Nevertheless, the growing progress in developing new battery technologies and advanced battery chemistries will likely create vast opportunities for the Asia-Pacific rechargeable battery market.

- Among the countries in the region, India is expected to have significant growth due to the rise in the adoption of electric vehicles, consumer electronics, and energy storage systems in renewable projects.

Asia-Pacific Rechargeable Battery Market Trends

Lithium-ion Battery to be the Fastest Growing

- Among various battery technologies, lithium-ion batteries (LIBs) are poised to dominate the rechargeable battery market, showcasing rapid growth during the forecast period. Their rising popularity over other battery types can be attributed to their superior capacity-to-weight ratio, extended shelf life, reduced maintenance needs, and plummeting prices.

- Li-ion batteries boast several technical advantages over traditional lead-acid batteries. While lead-acid batteries typically offer 400-500 cycles, rechargeable Li-ion batteries can exceed 5,000 cycles. Moreover, Li-ion batteries demand less frequent maintenance and replacements. They also maintain consistent voltage throughout their discharge cycle, ensuring prolonged efficiency for connected electrical components.

- Major players in the Asia-Pacific region are heavily investing in lithium-ion batteries, focusing on R&D and economies of scale. This surge in competition has driven down lithium-ion battery prices. Thanks to technological advancements, manufacturing optimizations, and falling raw material costs, the average price of lithium-ion batteries plummeted from USD 780/kWh in 2013 to USD 139/kWh in 2023. Projections suggest a further drop to around USD 113/kWh by 2025 and USD 80/kWh by 2030. Regionally, China recorded the lowest average battery pack prices at USD 126/kWh in 2023. Intense local competition in China saw manufacturers ramping up production to capture the burgeoning battery demand. Such declining trends in battery costs are likely to make it a lucrative choice among all batteries.

- Historically, lithium-ion batteries powered consumer electronics like mobile phones and laptops. Recently, they've been adapted for hybrids, the full range of battery electric vehicles (BEVs), and battery energy storage systems (BESS) in renewable energy, largely due to their reduced environmental impact.

- Grid-scale BESS, for instance, is pivotal in achieving Net Zero Emissions. They provide essential services, from short-term balancing and grid stability to long-term energy storage and post-blackout restoration. The International Energy Agency (IEA) forecasts that grid-scale battery energy storage will spearhead energy storage growth. In 2022, China contributed over 42% of the 11.21 GW annual grid-scale battery storage additions, totaling over 4.81 GW. With plans to install over 30 GW of BESS by 2025, predominantly using lithium-ion batteries, China's ambitions signal a booming future for BESS and, consequently, a surging demand for rechargeable batteries in the Asia-Pacific.

- In December 2023, South Korea's Ministry of Finance unveiled a plan to inject KRW 38 trillion into the lithium battery industry over the next five years, with formal implementation set for 2024. Alongside establishing a KRW 1 trillion promotion fund, South Korea is channeling KRW 73.6 billion into R&D and bolstering reserves of critical minerals for domestic lithium battery production. These moves, coupled with efforts to foster a battery reuse and recycling ecosystem, are set to invigorate the lithium-ion battery sector and bolster the rechargeable battery market.

- March 2024 saw Panasonic Group announce a joint venture with Indian Oil Corporation Ltd (IOCL) for cylindrical lithium-ion battery production. This venture, driven by anticipated demand for two and three-wheel vehicles and BESS in India, underscores the region's growing lithium-ion battery manufacturing trend.

- Given their lightweight nature, rapid charging capabilities, extended charging cycles, declining costs, and industry advancements, lithium-ion batteries are set to emerge as the fastest-growing battery technology in the Asia-Pacific rechargeable battery market during the forecast period.

India to Witness Significant Growth

- Driven by the rising adoption of electric vehicles (EVs), surging demand for consumer electronics, and government initiatives championing energy storage solutions, the Indian rechargeable battery market is on the brink of significant growth. The surge in demand for rechargeable batteries, pivotal for the expansion of the market, is largely attributed to the widespread adoption of smartphones, laptops, and other portable devices in the consumer electronics sector.

- Moreover, the Indian Government's aggressive push towards electric mobility is amplifying the demand for rechargeable batteries, especially in the EV segment. Data from the International Energy Agency (IEA) highlights this trend, noting that battery electric vehicle (BEV) sales in India soared to approximately 82,000 units in 2023, marking a remarkable 70% uptick from the previous year. With the Indian Government setting ambitious targets for 2030 - envisioning 30% of newly registered private cars, 40% of buses, 70% of commercial cars, and a staggering 80% of two-wheelers and three-wheelers to be electric - the demand for rechargeable batteries, particularly lithium-ion variants, is set to surge.

- In a bid to bolster local manufacturing and reduce reliance on imported Advance Chemistry Cell (ACC) batteries for electric vehicles, the Indian Government rolled out a Production Linked Incentive (PLI) Scheme in early 2021. With a substantial outlay of USD 2.12 billion spread over five years, the scheme aims to establish a competitive ACC battery manufacturing setup in the country, targeting a capacity of 50 GWh, with an additional focus on 5 GWh of niche ACC technologies. The PLI Scheme offers a production-linked subsidy, determined by the applicable subsidy per KWh and the achieved percentage of value addition based on actual sales. By 2022, four prominent companies - Reliance New Energy Solar Limited, Hyundai Global Motors Company Limited, Ola Electric Mobility Private Limited, and Rajesh Exports Limited - secured incentives under this scheme, underscoring the government's commitment to boosting local battery cell production.

- Capitalizing on India's growing energy storage demands and its shift towards sustainable solutions, both local and international players are making significant investments in the Indian rechargeable battery market. For instance, in April 2022, Exide Industries, a major player in the battery sector, unveiled plans for a lithium-ion cell manufacturing plant in Karnataka, with an investment of approximately USD 718 million. The facility, starting with a 6 GWh capacity, is set to become operational by 2024, with plans to expand to a 12 GWh integrated lithium-ion battery facility in subsequent years.

- In another notable move, battery technology startup Log9 Materials inaugurated India's inaugural lithium-ion cell manufacturing facility in Jakkur, Bengaluru, in April 2023. Starting with a capacity of 50 MWh, Log9 has ambitious plans to scale up to 1 GWh for cell manufacturing and 2 GWh for battery pack manufacturing by Q1 2025. March 2024 saw GoodEnough Energy announcing its plans to commence operations at India's first battery energy storage gigafactory in Jammu and Kashmir by October 2024. With an investment of INR 1.5 billion (USD 18.07 million) for the initial 7 GWh facility and a projected spend of INR 3 billion (USD 37 million) by 2027 to elevate capacity to 20 GWh, GoodEnough's facility aims to significantly impact the industry, potentially cutting over 5 million tons of carbon emissions annually. This gigafactory aligns with India's ambitious goal to ramp up its renewable energy capacity to 500 GW by 2030, a significant leap from around 176 GW in 2023. To further bolster these efforts, the Indian government is extending incentives worth USD 452 million to companies engaged in promoting battery storage projects.

- With a vast consumer base, supportive governmental policies, and strides in battery manufacturing, the Indian rechargeable battery market is set for robust growth in the foreseeable future.

Asia-Pacific Rechargeable Battery Industry Overview

The Asia-Pacific rechargeable battery market is fragmented. Some of the key players in the market (not in any particular order) include Panasonic Corporation, Contemporary Amperex Technology Co. Limited, BYD Company Ltd., GS Yuasa Corporation, and Amara Raja Energy & Mobility Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast, in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing Adoption of Electric Vehicles

- 4.5.1.2 Declining Lithium-ion Battery Cost

- 4.5.2 Restraints

- 4.5.2.1 Demand-Supply Mismatch of Raw Materials

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Technology

- 5.1.1 Lead-Acid

- 5.1.2 Lithium-Ion

- 5.1.3 Other Technologies (NiMh, Nicd, etc.)

- 5.2 Application

- 5.2.1 Automotive Batteries

- 5.2.2 Industrial Batteries (Motive, Stationary (Telecom, UPS, Energy Storage Systems (ESS), etc.)

- 5.2.3 Portable Batteries (Consumer Electronics, etc.)

- 5.2.4 Other Applications

- 5.3 Geography

- 5.3.1 India

- 5.3.2 China

- 5.3.3 Japan

- 5.3.4 South Korea

- 5.3.5 Thailand

- 5.3.6 Indonesia

- 5.3.7 Vietnam

- 5.3.8 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Panasonic Corporation

- 6.3.2 Contemporary Amperex Technology Co. Limited

- 6.3.3 BYD Co.Ltd.

- 6.3.4 GS Yuasa Corporation

- 6.3.5 Samsung SDI Co. Ltd

- 6.3.6 LG Chem Ltd.

- 6.3.7 Clarios, LLC.

- 6.3.8 Amara Raja Energy & Mobility Ltd

- 6.3.9 Exide Industries Ltd

- 6.3.10 Duracell Inc.

- 6.3.11 Saft Groupe SA

- 6.3.12 Tianjin Lishen Battery Joint-Stock Co. Ltd. Source: https://www.mordorintelligence.com/industry-reports/southeast-asia-battery-market

- 6.3.13 Tesla Inc.

- 6.4 List of Other Prominent Companies (Company Name, Headquarter, Relevant Products & Services, Contact Details, etc.)

- 6.5 Market Ranking/Share (%) Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Progress in Developing New Battery Technologies and Advanced Battery Chemistries

02-2729-4219

+886-2-2729-4219

全球先进可充电电池回收市场(2026-2046)

全球先进可充电电池回收市场(2026-2046) 日本可充电电池市场规模、份额、趋势及预测(按电池类型、容量、应用和地区划分,2026年至2034年)

日本可充电电池市场规模、份额、趋势及预测(按电池类型、容量、应用和地区划分,2026年至2034年) 柔性锂陶瓷电池市场按类型、应用和最终用户划分,全球预测(2026-2032年)

柔性锂陶瓷电池市场按类型、应用和最终用户划分,全球预测(2026-2032年) 充电灯市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

充电灯市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测 东南亚充电电池:市场占有率分析、产业趋势/统计、成长预测(2025-2030)中东/北非二次电池市场占有率分析、产业趋势、成长预测(2025-2030)中东充电电池:市场占有率分析、产业趋势与成长预测(2025-2030)中东和非洲二次电池市场占有率分析、产业趋势、成长预测(2025-2030)中国充电电池:市场占有率分析、产业趋势/统计、成长预测(2025-2030)义大利二次电池:市场占有率分析、产业趋势与成长预测(2025-2030 年)

东南亚充电电池:市场占有率分析、产业趋势/统计、成长预测(2025-2030)中东/北非二次电池市场占有率分析、产业趋势、成长预测(2025-2030)中东充电电池:市场占有率分析、产业趋势与成长预测(2025-2030)中东和非洲二次电池市场占有率分析、产业趋势、成长预测(2025-2030)中国充电电池:市场占有率分析、产业趋势/统计、成长预测(2025-2030)义大利二次电池:市场占有率分析、产业趋势与成长预测(2025-2030 年)

▼