|

市场调查报告书

商品编码

1636547

中东和非洲二次电池市场占有率分析、产业趋势、成长预测(2025-2030)Middle East And Africa Rechargeable Battery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

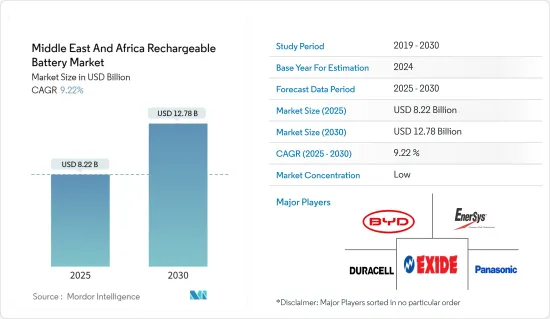

中东和非洲二次电池市场规模预计到2025年为82.2亿美元,预计到2030年将达到127.8亿美元,预测期内(2025-2030年)复合年增长率为9.22%。

主要亮点

- 从中期来看,电动车(EV)产量的增加和锂离子电池价格的下降预计将在预测期内推动二次电池需求。

- 另一方面,蕴藏量的短缺可能会严重限制二次电池市场的成长。

- 智慧型手錶、无线耳机和智慧手环等穿戴式装置的日益普及预计将在不久的将来为可充电电池市场的参与企业创造巨大的商机。

- 预计阿联酋的中东和非洲充电电池市场将显着成长。

中东和非洲充电电池市场趋势

锂离子电池占市场主导地位

- 中东和非洲锂离子二次电池市场是一个充满活力、机会与挑战并存的市场。由于其卓越的容量重量比,锂离子电池比其他技术更受欢迎。长寿命、最少维护、延长保质期和大幅降价等优点进一步推动了锂离子电池的采用。

- 锂离子电池历来比同类电池贵,但市场领导者正在加大投资。对实现规模经济和加强研发力度的关注加剧了竞争并压低了锂离子电池的价格。

- 2023年,电池价格将出现显着下降,稳定在139美元/kWh。随着采矿和精製能的增加,锂价格预计将稳定并到 2026 年达到 100 美元/kWh 大关。

- 随着电动车和永续能源储存解决方案需求激增,中东和非洲国家正在增加对锂电池研发的投资。非洲拥有丰富的锂矿床,正成为全球锂离子电池供应链的重要参与企业。

- 刚果民主共和国、辛巴威和纳米比亚等拥有大量锂蕴藏量的国家正成为主要投资目标。这些国家拥有丰富的锂资源,是快速成长的电动车市场的重要参与企业。

- 此外,世界向清洁能源和交通的转变推动了对电动车(EV)前所未有的需求。电动车的蓬勃发展直接扩大了对锂离子二次电池的需求。 2022 年 4 月,沙乌地阿拉伯与 Lucid Motors(一家由该国公共投资基金 (PIF) 部分资助的上市公司)签署协议,在未来 10 年内采购 10 万辆电动车。

- 同样,2023 年 9 月,肯亚政府与电动两轮车製造商合作部署了超过 100 万辆电动车。该合作伙伴关係还包括 Spiro 安装 3,000 个电池充电和交换站、加强肯亚的电动车基础设施并建立当地製造工厂。

- 此类措施和投资将扩大该地区的电动车产量,并在预测期内增加对锂离子电池的需求。

阿联酋实现显着成长

- 阿拉伯联合大公国已成为中东和非洲充满活力的经济和技术进步中心。随着国家的发展,对可携式电源,尤其是电池能源储存系统(BESS)的需求预计在未来几年将快速成长。

- BESS 对于将太阳能和风能等可再生能源无缝整合到电网中至关重要。 BESS 可以缓解能源生产的波动并确保持续可靠的电力供应。

- 根据国际可再生能源机构(IRENA)的报告,2023年阿联酋可再生能源装置容量将达到605万千瓦,在过去10年中成长了惊人的45倍。值得注意的是,2022年至2023年间成长率接近68%。

- 展望未来,阿联酋政府承诺在2050年投资1,640亿美元,以满足不断增长的能源需求并促进永续经济成长。杜拜2050年能源策略已经实现了2020年7%的能源来自清洁能源来源的目标。该策略的雄心勃勃的目标是到 2030 年达到 25%,到 2050 年达到 75%。这些雄心勃勃的目标将增加该地区对电池储能係统的需求。

- 电动车(EV)在阿拉伯联合大公国稳步普及。国际能源总署(IEA)的资料显示,2023年电动车销量将达28,900辆,与前一年同期比较成长52.9%。预测显示,未来几年电动车销量将大增。

- 为了支持永续交通,阿联酋正在积极推动电动车的采用。随着全球社会迈向绿色未来,阿联酋不仅推广电动车,也大力投资必要的充电基础设施。

- 2023年7月,能源和基础设施部(MoEI)宣布了全面的电动车政策。该措施旨在为电动车充电基础设施建立强有力的监管标准,并有可能加强阿联酋电池市场。

- 此外,MoEI 还制定了一个雄心勃勃的目标,即到 2050 年,阿联酋道路上 50% 的车辆为电动车辆。这符合杜拜到 2030 年持有42,000 辆电动车的目标。

- 鑑于这些措施和预测,预计未来几年阿联酋对二次电池的需求将大幅增加。

中东和非洲二次电池产业概况

中东和非洲的二次电池产业较为分散。主要企业(排名不分先后)包括比亚迪有限公司、金霸王公司、Exide Industries Ltd.、EnerSys 和松下控股公司。

其他好处

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 调查范围

- 市场定义

- 研究场所

第 2 章执行摘要

第三章调查方法

第四章市场概况

- 介绍

- 2029年之前的市场规模与需求预测(单位:美元)

- 最新趋势和发展

- 政府法规和措施

- 市场动态

- 促进因素

- 电动车 (EV) 产量增加

- 锂离子电池价格下降

- 抑制因素

- 原料蕴藏量不足

- 促进因素

- 供应链分析

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代产品/服务的威胁

- 竞争公司之间的敌对关係

- 投资分析

第五章市场区隔

- 技术部分

- 锂离子电池

- 铅酸电池

- 其他(镍氢、镍镉等)

- 目的

- 汽车电池

- 工业电池(用于电源、固定电池(电信、UPS、能源储存系统(ESS) 等)

- 手提电池(家用电子电器产品等)

- 其他的

- 地区

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 奈及利亚

- 卡达

- 埃及

- 南非

- 其他中东/非洲

第六章 竞争状况

- 併购、合资、联盟、协议

- 主要企业策略

- 公司简介

- BYD Company Ltd

- Duracell Inc.

- EnerSys

- Panasonic Holdings Corporation

- Energizer

- Saft Groupe SA

- Exide Industries Ltd

- ABM East Africa

- Amperex Technology Co. Limited

- Murrata Manufacturing Co. Ltd.

- 其他知名公司名单

- 市场排名/份额分析

第七章 市场机会及未来趋势

- 扩大穿戴式装置的采用

简介目录

Product Code: 50004023

The Middle East And Africa Rechargeable Battery Market size is estimated at USD 8.22 billion in 2025, and is expected to reach USD 12.78 billion by 2030, at a CAGR of 9.22% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, rising electric vehicle (EV) production and declining lithium-ion battery prices are expected to drive the demand for the rechargeable batteries during the forecast period.

- On the other hand, the lack of raw material reserves can significantly restrain the growth of the rechargeable battery market.

- Nevertheless, the growing adoption of wearable devices like smartwatches, wireless earphones, smart bands, and more is expected to create significant opportunities for rechargeable battery market players in the near future.

- United Arab Emirates (UAE) is anticpated to witness significant growth in the Middle East and Africa rechargeable battery market.

Middle East And Africa Rechargeable Battery Market Trends

Lithium-Ion Battery to Dominate the Market

- The Middle East and Africa's lithium-ion rechargeable battery market is a dynamic arena, teeming with both opportunities and challenges. Lithium-ion batteries are outpacing other technologies in popularity, thanks to their superior capacity-to-weight ratio. Their adoption is further fueled by advantages like extended lifespan, minimal maintenance, enhanced shelf life, and a notable drop in prices.

- While lithium-ion batteries traditionally commanded a premium over their counterparts, leading market players have been ramping up investments. Their focus on achieving economies of scale and bolstering R&D efforts has intensified competition, subsequently driving down lithium-ion battery prices.

- In 2023, battery prices saw a notable dip, settling at USD 139/kWh - a drop exceeding 13%. With the ramp-up of extraction and refining capacities, lithium prices are projected to stabilize, aiming for the USD 100/kWh mark by 2026.

- As the demand for electric vehicles and sustainable energy storage solutions surges, Middle Eastern and African nations are ramping up investments in lithium battery R&D. With its rich lithium deposits, Africa is positioning itself as a key player in the global lithium-ion battery supply chain.

- Countries like the Democratic Republic of Congo, Zimbabwe, and Namibia, boasting significant lithium reserves, are becoming prime targets for investments. These nations' abundant lithium resources position them as pivotal players in the burgeoning EV market.

- Moreover, the global shift towards cleaner energy and transportation has ignited an unprecedented demand for electric vehicles (EVs). This EV boom directly amplifies the need for lithium-ion rechargeable batteries. A testament to this trend: in April 2022, Saudi Arabia inked a deal with Lucid Motors, a company partly owned by the Kingdom's Public Investment Fund (PIF), to procure 100,000 EVs over the next decade.

- In a similar vein, in September 2023, Kenya's government collaborated with an electric motorbike manufacturer to introduce over a million EVs to the nation. The partnership includes Spiro's commitment to set up 3,000 battery charging and swapping stations, bolstering Kenya's EV infrastructure, and establishing a local manufacturing facility.

- Such initiatives and investments are poised to amplify EV production in the region, driving up the demand for lithium-ion rechargeable batteries during the forecast period.

United Arab Emirates (UAE) to Witness Significant Growth

- The United Arab Emirates (UAE) has emerged as a vibrant center for economic and technological progress in the Middle East and Africa. As the nation evolves, the demand for portable power sources, especially battery energy storage systems (BESS), is poised to surge in the coming years.

- BESS is pivotal in seamlessly integrating renewable energy sources, such as solar and wind, into the power grid. They mitigate fluctuations in energy production, ensuring a consistent and reliable electricity supply.

- As reported by the International Renewable Energy Agency (IRENA), the UAE's installed renewable energy capacity reached 6.05 GW in 2023, marking a staggering 45-fold increase over the past decade. Notably, a growth rate of nearly 68% was observed between 2022 and 2023.

- With an eye on the future, the UAE government has committed to investing USD 164 billion by 2050, aiming to meet the surging energy demand and foster sustainable economic growth. Dubai's Energy Strategy 2050 has already hit its 2020 target of deriving 7% of its energy from clean sources. The strategy ambitiously aims for 25% by 2030 and a remarkable 75% by 2050. Such ambitious targets are set to bolster the demand for BESS in the region.

- The UAE is witnessing a steady uptick in electric vehicle (EV) adoption. Data from the International Energy Agency (IEA) indicates that 28,900 EVs were sold in 2023, marking a 52.9% increase from the previous year. Projections suggest a significant surge in EV sales in the coming years.

- To champion sustainable transportation, the UAE is fervently promoting EV adoption. As the global community pivots towards a greener future, the UAE is not just encouraging EVs but is also heavily investing in the necessary charging infrastructure.

- In July 2023, the Ministry of Energy and Infrastructure (MoEI) unveiled a comprehensive electric vehicle policy. This policy aims to establish robust regulatory standards for EV charging infrastructure, potentially bolstering the battery market in the UAE.

- Furthermore, MoEI has set an ambitious target: by 2050, 50% of all vehicles on UAE roads will be electric. This aligns with Dubai's goal of having 42,000 EVs by 2030.

- Given these initiatives and projections, the demand for rechargeable batteries in the UAE is set to witness a significant upswing in the coming years.

Middle East And Africa Rechargeable Battery Industry Overview

The Middle East and Africa rechargeable Battery is semi-fragmented. Some key players (not in particular order) are BYD Company Ltd, Duracell Inc., Exide Industries Ltd, EnerSys, and Panasonic Holdings Corporation, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast, in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 The Increasing Electric Vehicle (EV) Production

- 4.5.1.2 Declining Lithium-ion Battery Prices

- 4.5.2 Restraints

- 4.5.2.1 Lack of Raw Material Reserves

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Technology

- 5.1.1 Lithium-ion Battery

- 5.1.2 Lead-Acid Battery

- 5.1.3 Others (NiMh, NiCd, etc.)

- 5.2 Application

- 5.2.1 Automotive Batteries

- 5.2.2 Industrial Batteries (Motive, Stationary (Telecom, UPS, Energy Storage Systems (ESS), etc.)

- 5.2.3 Portable Batteries (Consumer Electronics, etc.)

- 5.2.4 Other Applications

- 5.3 Geography

- 5.3.1 United Arab Emirates

- 5.3.2 Saudi Arabia

- 5.3.3 Nigeria

- 5.3.4 Qatar

- 5.3.5 Egypt

- 5.3.6 South Africa

- 5.3.7 Rest of Middle East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 BYD Company Ltd

- 6.3.2 Duracell Inc.

- 6.3.3 EnerSys

- 6.3.4 Panasonic Holdings Corporation

- 6.3.5 Energizer

- 6.3.6 Saft Groupe SA

- 6.3.7 Exide Industries Ltd

- 6.3.8 ABM East Africa

- 6.3.9 Amperex Technology Co. Limited

- 6.3.10 Murrata Manufacturing Co. Ltd.

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking/ Share Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing Adoption of Wearable Devices

02-2729-4219

+886-2-2729-4219

充电电池市场:2026-2032年全球市场预测(按电池类型、电压、外形尺寸、应用和销售管道)

充电电池市场:2026-2032年全球市场预测(按电池类型、电压、外形尺寸、应用和销售管道) 全球先进可充电电池回收市场(2026-2046)

全球先进可充电电池回收市场(2026-2046) 日本可充电电池市场规模、份额、趋势及预测(按电池类型、容量、应用和地区划分,2026年至2034年)柔性锂陶瓷电池市场按类型、应用和最终用户划分,全球预测(2026-2032年)

日本可充电电池市场规模、份额、趋势及预测(按电池类型、容量、应用和地区划分,2026年至2034年)柔性锂陶瓷电池市场按类型、应用和最终用户划分,全球预测(2026-2032年) 全球可充电电池市场(2024-2035 年)- 第 32 版

全球可充电电池市场(2024-2035 年)- 第 32 版 充电灯市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

充电灯市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测 东南亚充电电池:市场占有率分析、产业趋势/统计、成长预测(2025-2030)中东/北非二次电池市场占有率分析、产业趋势、成长预测(2025-2030)中东充电电池:市场占有率分析、产业趋势与成长预测(2025-2030)中国充电电池:市场占有率分析、产业趋势/统计、成长预测(2025-2030)

东南亚充电电池:市场占有率分析、产业趋势/统计、成长预测(2025-2030)中东/北非二次电池市场占有率分析、产业趋势、成长预测(2025-2030)中东充电电池:市场占有率分析、产业趋势与成长预测(2025-2030)中国充电电池:市场占有率分析、产业趋势/统计、成长预测(2025-2030)

▼