|

市场调查报告书

商品编码

1636580

光固化成形法(SLA) 技术 3D 列印 -市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Stereolithography (SLA) Technology 3D Printing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

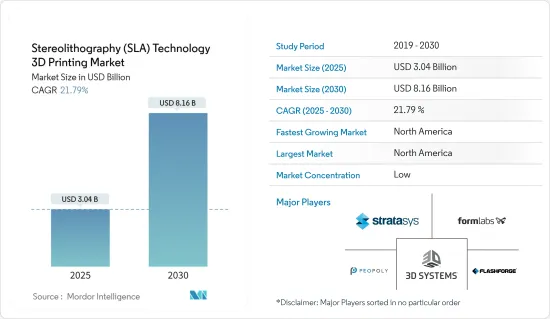

光固化成形法技术3D列印市场规模预计到2025年为30.4亿美元,预计到2030年将达到81.6亿美元,在预测期内(2025-2030年)复合年增长率为21.79%。

主要亮点

- 光固化成形法(SLA) 技术以其精度和製造复杂组件的能力而闻名,是不断扩大的 3D 列印市场的关键组成部分。 SLA 3D 列印领域的一个显着趋势是不断提高印表机速度和效率。製造商正专注于生产更快的雷射系统和微调软体演算法,所有这些都是为了在不影响精度的情况下缩短列印时间。

- 另一个值得注意的趋势是树脂材料的扩展。高强度、耐热、生物相容性和柔性树脂的出现扩大了 SLA 技术的吸引力,服务于医疗、汽车和航太等领域。例如,2024 年 11 月,Formlabs 宣布推出新的 SLA 树脂系列。该系列有两种类型:“Creator Tough Resin”和“Creator Super Clear Resin”,两者都具有优异的断裂伸长率。透过抛光和透明涂层等后处理进一步增强其强度和透明度。

- 此外,桌上型 SLA 印表机的经济性和易用性正在推动小型企业、业余爱好者和教育机构的采用。后处理自动化的发展也是一个重要的进步。自动化树脂清洗和固化的解决方案使生产工作流程更加简化,并增加了 SLA 在大批量製造中的吸引力。 2024 年 9 月,Formlabs 透过引入 SLA 和 SLS后处理工具,在其已经丰富的超过 45 种材料库中添加了两种新材料,丰富了其产品组合。这些新增内容旨在扩展 3D 列印的应用并简化使用者最终获得消费者可接受的零件的路径。

- 然而,3D列印并非没有障碍。一个关键挑战在于工业级 SLA 印表机和相关设备的初始投资较高。这种财务障碍通常会阻碍小型企业采用 SLA 技术。此外,SLA 列印的后处理既费力又耗时。零件列印完成后,会经历几个重要的后处理过程,包括酒精清洗、支撑材料去除和打磨。这些任务通常是手动完成的,存在人为错误的固有风险。

光固化成形法(SLA) 技术 3D 列印市场趋势

医疗产业预计成长最快

- SLA 3D 列印市场在很大程度上受到医疗行业对复杂和客製化医疗解决方案的需求的推动。该技术擅长以无与伦比的精度列印复杂的患者特定模型和设备,重塑医疗原型製作和製造格局。

- SLA 技术对于手术范本、修復体、牙齿矫正器和解剖模型的製造至关重要,可增强术前计划和患者沟通。公司正积极推出牙科和医疗领域的产品。例如,2024 年 4 月,立体光刻技术(SLA) 和选择性雷射烧结 (SLS) 领域的领导者 Formlabs 宣布推出半个世纪以来的首款新型 3D 列印机,其模型专为牙科和医疗应用而设计。

- 利用生物相容性和可灭菌树脂有助于创建患者专用的医疗设备,并确保符合严格的医疗标准。此外,医疗用途树脂配方的创新扩大了 SLA 的应用,特别是在整形外科和客製化植入方面。

- 此外,SLA 技术树脂材料的进步正在推动其在医疗领域的采用。例如,Formlabs 宣布推出六种新树脂。四种改良的通用树脂,一种专为快速原型製作和正畸模型而定制的高速模型树脂,以及专为高精度牙科工作而设计的精密模型树脂。

- 透过利用生物相容性和无菌树脂,该行业生产符合严格医疗标准的患者专用医疗设备。此外,树脂配方的创新,尤其是医疗应用领域的创新,正在将 SLA 的应用扩展到整形外科和自订植入等领域。

北美地区占比最大

- 北美凭藉其强大的工业基础和对先进製造技术的大量投资,在SLA 3D列印市场中占据着举足轻重的地位。该地区是主要 3D 列印公司的所在地,并广泛应用于医疗保健、航太和汽车等关键领域。北美是 3D Systems 和 Formlabs 等行业领导者的所在地,处于 SLA 解决方案持续创新和发展的前沿。

- 在北美,尤其是美国医疗领域已全面采用SLA 3D列印。地区公司正在推出专为医疗用途量身定制的尖端 3D 列印硬体和材料,突显他们对创新解决方案的承诺。

- 例如,总部位于加州的 Proclaim Health 旨在透过 3D 列印彻底改变牙线,创造改善牙齿和牙龈健康的工具。使用 3D 列印,我们对设计进行微调,优先考虑表面品质、生物相容性、半透明度和成本效益等功能方面。

- 市场成长得到监管认可的进一步支持,例如 FDA 对 3D 列印医疗设备的认可。同时,航太和国防领域利用 SLA 技术进行原型製作,生产符合严格精度标准的轻型复杂零件。

- 北美学术和研究机构正处于关键时刻,将 SLA 3D 列印纳入其课程,以推动创新并培养精通增材製造的劳动力。例如,2024年,李大学在其山顶校园开设了最先进的3D列印中心,以满足对3D列印资源快速成长的需求。该中心目前还拥有 10 台长丝印表机和一台最先进的大幅面 SLA 印表机。

立体光刻技术(SLA)技术3D列印产业概述

由创新和客製化驱动的全球和区域参与企业正在主导市场。医疗保健、汽车和航太等行业越来越多地采用这些创新。主要参与企业包括 3D Systems、Formlabs Inc.、Stratasys Ltd.、Peopoly 和 FlashForge。这些公司利用先进的材料相容性、高精度印表机和简化的工作流程来服务工业和消费应用。

创新是竞争策略的基石。该公司正在投资新的树脂配方,以实现更高的列印解析度、提高效率并扩大材料相容性。例如,领先的公司正在与软体供应商、材料供应商和最终用户合作,共同开发特定于应用的解决方案。

凭藉强大的工业基础和积极的研发努力,北美和欧洲引领 SLA 3D 列印市场。相较之下,在政府措施、具成本效益的製造以及不同领域日益普及的推动下,亚太地区正迅速崛起为强大的竞争对手。

其他好处

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间敌对关係的强度

- 评估宏观经济趋势对市场的影响

第五章市场动态

- 市场驱动因素

- 对快速原型製作的需求不断增长

- 树脂材料的进展

- 市场限制因素

- 初期投资成本高

- 需要后处理

第六章 市场细分

- 按用途

- 原型製作

- 巡迴

- 最终用途产品

- 教育/研究

- 按行业分类

- 车

- 医疗保健

- 消费品

- 航太

- 製造业

- 教育

- 按地区

- 北美洲

- 欧洲

- 亚洲

- 澳洲/纽西兰

- 拉丁美洲

- 中东/非洲

第七章 竞争格局

- 公司简介

- 3D Systems Inc.

- Formlabs

- Stratysys

- Peopoly

- XYZ printing

- FlashForge

- Zortrax

- B9Creations

- Shining 3D

- Prusa Research as

- Anycubic

- Phrozen Technology

- Kudo3D

- Asiga

- MiiCraft

- Uniz Technology LLC

第八章投资分析

第9章市场的未来

The Stereolithography Technology 3D Printing Market size is estimated at USD 3.04 billion in 2025, and is expected to reach USD 8.16 billion by 2030, at a CAGR of 21.79% during the forecast period (2025-2030).

Key Highlights

- Stereolithography (SLA) technology stands out as a crucial component of the expansive 3D printing market, celebrated for its precision and capability to craft intricate components. A prominent trend in the SLA 3D printing arena is the relentless push towards enhanced printer speed and efficiency. Manufacturers are channeling efforts into crafting swifter laser systems and fine-tuning software algorithms, all aimed at curtailing print times without compromising on accuracy.

- Another noteworthy trend is the expanding array of resin materials. The availability of high-strength, temperature-resistant, biocompatible, and flexible resins has broadened SLA technology's appeal, serving sectors like healthcare, automotive, and aerospace. For example, in November 2024, Formlabs unveiled a fresh lineup of SLA resins, catering specifically to hobbyists and makers. This lineup features the Creator Tough Resin and Creator Super Clear Resin, both boasting impressive elongation at break. Their strength and transparency can be further accentuated through post-processing methods such as polishing and clear coatings.

- Moreover, the surge in affordability and user-friendliness of desktop SLA printers has spurred their adoption among small businesses, hobbyists, and educational entities. The move towards automation in post-processing is another pivotal advancement. With solutions for automated resin washing and curing, production workflows are becoming more streamlined, enhancing SLA's appeal for high-volume production. In September 2024, Formlabs enriched its portfolio by adding two new materials to its already extensive library of 45+, alongside introducing SLA and SLS post-processing tools. These additions aim to broaden 3D printing applications and simplify the journey for users to attain final, consumer-ready parts.

- However, the landscape isn't without its hurdles. A significant challenge lies in the steep initial investment for industrial-grade SLA printers and their associated equipment. This financial barrier often deters small and medium-sized enterprises from embracing SLA technology. Furthermore, the post-processing demands of SLA printing can be both labor-intensive and time-consuming. Once parts are printed, they undergo several essential post-processing steps: washing with alcohol, support material removal, and sanding. Typically executed manually, these tasks carry an inherent risk of human error.

Stereolithography (SLA) Technology 3D Printing Market Trends

Healthcare Sector is Expected to be the Fastest Growing Segment

- The SLA 3D printing market is being significantly propelled by the healthcare sector's demand for intricate and tailored medical solutions. This technology's prowess in crafting complex, patient-specific models and devices with unparalleled precision is reshaping the landscape of medical prototyping and production.

- SLA technology is pivotal in producing surgical guides, prosthetics, dental aligners, and anatomical models, enhancing both preoperative planning and patient communication. Companies are actively introducing products tailored for the dental and healthcare arenas. For example, in April 2024, Formlabs, a leader in stereolithography (SLA) and selective laser sintering (SLS), unveiled its first new 3D printer in half a decade, alongside a model tailored for dental and healthcare uses.

- Utilizing biocompatible and sterilizable resins has facilitated the creation of patient-specific medical devices, ensuring compliance with rigorous healthcare standards. Moreover, innovations in resin formulations for medical purposes have expanded SLA's applications, notably in orthopedics and bespoke implants.

- Furthermore, advancements in resin materials for SLA technology are propelling its adoption in the healthcare domain. For instance, Formlabs introduced six new resins, featuring four reformulated general-purpose variants, a fast model resin tailored for swift prototypes and orthodontic models, and a precision model resin designed for high-accuracy dental tasks.

- By leveraging biocompatible and sterilizable resins, the industry is producing patient-specific medical devices that adhere to stringent healthcare standards. Additionally, innovations in resin formulations, especially for medical uses, are expanding SLA's applications into fields like orthopedics and custom implants.

North America Holds One of the Largest Share

- North America's robust industrial foundation and substantial investments in advanced manufacturing technologies position it as a pivotal player in the SLA 3D printing market. The region boasts major 3D printing firms and widespread adoption across vital sectors, notably healthcare, aerospace, and automotive. With industry leaders like 3D Systems and Formlabs, North America is at the forefront of continuous innovation and the evolution of SLA solutions.

- In North America, the healthcare sector, especially in the U.S., has wholeheartedly adopted SLA 3D printing. Regional firms are introducing cutting-edge 3D printing hardware and materials tailored for healthcare, emphasizing their commitment to innovative solutions.

- For instance, Proclaim Health, a California-based company is revolutionizing dental flossing through 3D printing, aiming to develop a tool that enhances dental and gum health. Leveraging 3D printing, they're fine-tuning their design to prioritize functional aspects like surface quality, biocompatibility, translucency, and cost-effectiveness.

- Market growth is further bolstered by regulatory endorsements, such as the FDA's support for 3D-printed medical devices. Meanwhile, the aerospace and defense sectors harness SLA technology for prototyping and crafting lightweight, intricate components that adhere to stringent precision standards.

- Academic and research institutions in North America are pivotal, weaving SLA 3D printing into their curricula, driving innovation, and nurturing a workforce skilled in additive manufacturing. For instance, in 2024, Leigh University inaugurated a state-of-the-art 3D printing hub on its Mountaintop campus, responding to the surging demand for 3D printing resources. This hub now boasts an additional 10 filament printers and a cutting-edge, larger-scale SLA printer.

Stereolithography (SLA) Technology 3D Printing Industry Overview

Several global and regional players, driven by innovation and customization, dominate the market. Industries such as healthcare, automotive, and aerospace are increasingly adopting these innovations. Key players include 3D Systems, Formlabs Inc., Stratasys Ltd, Peopoly, FlashForge, etc. These companies utilize advanced material compatibility, high-precision printers, and streamlined workflows to serve both industrial and consumer applications.

Innovation is the cornerstone of competitive strategy. Companies are channeling investments into new resin formulations, achieving higher print resolutions, enhancing efficiency, and broadening material compatibility. Collaborations and partnerships play a pivotal role; for instance, major players are teaming up with software providers, material suppliers, and end-users to co-create application-specific solutions.

North America and Europe lead the SLA 3D printing market, bolstered by robust industrial bases and active R&D endeavors. In contrast, the Asia-Pacific region is swiftly emerging as a formidable contender, fueled by government initiatives, cost-effective manufacturing, and rising adoption across diverse sectors.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 An Assessment of Impact of Macroeconomic Trends on The Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Demand For Rapid Prototyping

- 5.1.2 Advancement in Resin Material

- 5.2 Market Restraints

- 5.2.1 High Initial Investment Costs

- 5.2.2 Post Processing Requirements

6 MARKET SEGMENTATION

- 6.1 By Application

- 6.1.1 Prototyping

- 6.1.2 Tooling

- 6.1.3 End-Use Products

- 6.1.4 Education and Research

- 6.2 By End-User Vertical

- 6.2.1 Automotive

- 6.2.2 Healthcare

- 6.2.3 Consumer Goods

- 6.2.4 Aerospace

- 6.2.5 Manufacturing

- 6.2.6 Education

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia

- 6.3.4 Australia and New Zealand

- 6.3.5 Latin America

- 6.3.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 3D Systems Inc.

- 7.1.2 Formlabs

- 7.1.3 Stratysys

- 7.1.4 Peopoly

- 7.1.5 XYZ printing

- 7.1.6 FlashForge

- 7.1.7 Zortrax

- 7.1.8 B9Creations

- 7.1.9 Shining 3D

- 7.1.10 Prusa Research a.s

- 7.1.11 Anycubic

- 7.1.12 Phrozen Technology

- 7.1.13 Kudo3D

- 7.1.14 Asiga

- 7.1.15 MiiCraft

- 7.1.16 Uniz Technology LLC

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

3D列印市场分析及预测(至2035年):依类型、产品、服务、技术、材料类型、应用、组件、製程及最终用户划分

3D列印市场分析及预测(至2035年):依类型、产品、服务、技术、材料类型、应用、组件、製程及最终用户划分 定向能量沉积 (DED) 3D 列印市场:依能量来源(雷射、电子束、电弧、等离子)、原料(粉末、丝材)、组件(硬体、软体、服务、材料)和终端应用产业划分——全球预测至 2036 年

定向能量沉积 (DED) 3D 列印市场:依能量来源(雷射、电子束、电弧、等离子)、原料(粉末、丝材)、组件(硬体、软体、服务、材料)和终端应用产业划分——全球预测至 2036 年 2026-2034年全球3D列印市场规模、份额、趋势和成长分析报告全球钨粉市场规模、份额、趋势及成长分析报告(2026-2034年,适用于3D列印)

2026-2034年全球3D列印市场规模、份额、趋势和成长分析报告全球钨粉市场规模、份额、趋势及成长分析报告(2026-2034年,适用于3D列印) 3D 列印:材料和设备机会、趋势和市场

3D 列印:材料和设备机会、趋势和市场 数位裁剪系统市场按部署类型、技术平台、服装类型、最终用户和分销管道划分-2026-2032年全球预测

数位裁剪系统市场按部署类型、技术平台、服装类型、最终用户和分销管道划分-2026-2032年全球预测 欧洲3D列印市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031年)

欧洲3D列印市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031年) 3D列印市场-全球产业规模、份额、趋势、机会和预测,按组件、(软体)、印表机类型、技术、製程、垂直产业、地区和竞争格局划分,2021-2031年预测

3D列印市场-全球产业规模、份额、趋势、机会和预测,按组件、(软体)、印表机类型、技术、製程、垂直产业、地区和竞争格局划分,2021-2031年预测 3D列印市场规模、份额和趋势分析报告:按组件、印表机类型、技术、软体、应用、产业、材料、地区和细分市场预测(2026-2033年)粉末层熔融3D列印技术市场-2025-2030年预测

3D列印市场规模、份额和趋势分析报告:按组件、印表机类型、技术、软体、应用、产业、材料、地区和细分市场预测(2026-2033年)粉末层熔融3D列印技术市场-2025-2030年预测