|

市场调查报告书

商品编码

1637758

北美无菌包装:市场占有率分析、行业趋势和成长预测(2025-2030)North America Aseptic Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

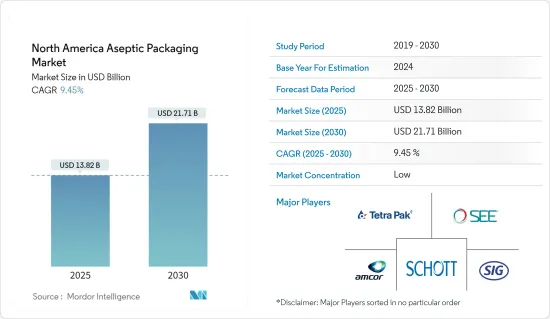

北美无菌包装市场规模预计到2025年为138.2亿美元,预计2030年将达到217.1亿美元,预测期内(2025-2030年)复合年增长率为9.45%。

由于对更长保质期以及无需冷藏的食品和饮料的保存的需求不断增加,该市场正在经历显着增长。此外,提高产品安全性和品质的包装技术进步在推动市场发展方面发挥着至关重要的作用。

主要亮点

- 随着远距运输需求的快速增加,延长保质期已成为当务之急。随着製造现场和最终用户之间的距离增加,包装必须变得更加耐用和具有保护性。在北美,对包装即食食品的偏好正在推动无菌包装的采用。

- 食品和饮料等终端用户行业正在优先考虑可持续包装和延长保质期。考虑到成本和环境效益,尤其是常温运输和储存,许多地区食品和饮料供应商都倾向于无菌包装。此外,无菌包装采用可回收纸箱及环保袋。这些选择通常会吸引那些喜欢少量且频繁购买的消费者,从而推动该地区对这些产品的强劲需求。

- 消费者的健康意识越来越强。消费者更愿意投资符合这种健康心态的产品,从早晨果汁到能量饮料。因此,饮料包装领域对具有成本效益的包装解决方案的需求激增。此外,人们越来越喜欢无菌纸盒,特别是在牛奶和乳类饮料领域,预计这将提振市场。这些纸箱便于堆迭并延长产品的保质期。

- 根据包装和加工技术研究所 (PMMI) 饮料报告,到 2028 年,北美饮料产业预计将成长约 4.5%。这个快速成长的饮料市场有望推动研究市场的成长。该地区的製药业,尤其是美国,对无菌包装的需求大幅增加。这一增长主要是由于透过生物技术提高药品的可用性和消费量以及对各种液体药品的无菌填充的需求。

- 为了满足日益增长的客户需求以及降低储存和配送成本的需要,公司正在投资尖端技术,利用感测器、RFID 和 NFC 等互联技术。这些投资旨在显着降低或消除从製造商到零售商的产品管理相关成本。

- 然而,无菌包装市场面临一些挑战,可能会阻碍收益成长。无菌包装的初始资本支出可能比传统生鲜食品生产方法高出两到三倍。此外,重要的是从一开始就让研究团队参与进来,以便能够对无菌加工特定的配方进行微调。然而,与传统方法相比,这项要求会显着增加无菌包装的成本。

北美无菌包装市场趋势

饮料领域预计将占据主要市场占有率

- 随着消费者越来越重视健康和保健,对水果即饮饮料的需求激增,特别关注具有成本效益的包装。预计这一趋势在预测期内将进一步加强。无菌包装不仅延长了这些饮料的保质期,还引入了保质期果汁等创新技术。

- 便利性正成为北美即饮饮料和健康意识类别的主导趋势。消费者倾向于即饮鸡尾酒,因为自製饮料需要大量的准备。这一转变凸显了一个重要趋势。消费者被这些鸡尾酒的独特风味所吸引,并且重视在户外享用它们的便利性。

- 乳製品行业的全球趋势揭示了透过创新包装实现产品差异化的动力。现今的乳製品包装通常拥有引人注目的设计和先进的无菌功能。这种对包装创新的重视是对北美主要市场激烈竞争的回应。

- 经过超高温灭菌处理的无菌奶,有效去除有害细菌。乳製品品类多种多样,不仅包括白奶及其製品,如牛酪油、酪乳和酸奶饮料,还包括前景广阔的调味奶领域。不含防腐剂的无菌加工和包装大大提高了保质期和新鲜度,这对于牛奶等生鲜食品非常重要。

- 乳製品行业对无菌包装日益增长的需求表明了更广泛的趋势。随着原乳产量的增加,新的全球市场机会即将出现。就背景而言,美国农业部预计,美国牛奶产量将从 2018 年的 2,176 亿磅增加到 2024 年的约 2,282 亿磅。此外,消费者的一个显着转变是对超高温灭菌牛奶的需求激增,超高温灭菌牛奶因其保质期长而受到重视,使消费者能够减少去商店的次数。此外,与传统包装的生乳或散装乳相比,疫情导致超高温灭菌乳明显偏好无菌包装,凸显了乳製品消费模式的重大转变。

加拿大市场预计将成长

- 对加拿大酪农行业的投资仍在继续,增强了该国的经济。为了满足当地需求,加拿大政府正在推广采用先进的包装技术,特别是无菌包装。注重健康的千禧世代和加拿大年轻人越来越多地转向牛奶、果汁和能量饮料,因为他们越来越意识到过量糖果零食、苏打水和人造甜味剂的风险。

- 在加拿大,消费者越来越多地选择牛奶盒而不是玻璃瓶和塑胶替代品。根据 StatCan 2024 年 5 月发布的报告,加拿大标准 3.25% 牛奶产量从 2020 年的约 438,380 千升增加到 2023 年的 468,070 千升。在乳製品饮料行业,无菌液体包装是易腐物品的首选。鑑于乳製品的性质,包装品质对于这些极易腐烂的流质食品和饮料至关重要。

- 无菌解决方案供应商正在应对乳製品包装领域的挑战。近 60% 使用无菌包装的产品是乳製品,包括汤匙式优格、起司、奶油和冰淇淋。儘管乳製品的消费多种多样,包括天然奶酪、粉状奶酪和加工起士,但易腐烂仍然是一个紧迫的问题。无菌包装可以将起司的保存期限延长多达60天。

- 因此,最终用户在包装上投入大量资金。乳製品因暴露于氧气而容易发生香气转移和分解,因此包装必须具有优良的阻隔性。 StatCan资料显示加拿大乳製品销售大幅成长。 2024 年 1 月至 5 月,製造商月度销售额从 13.9 亿加元(10.3 亿美元)跃升至 16.7 亿加元(12.4 亿美元)。

- 此外,无菌药品製造(通常称为填充-完成製造)对于疫苗、生技药品、注射、癌症治疗以及各种形式的耳、鼻和眼药水的生产至关重要。这种方法显着降低了药物被细菌和其他有害物质污染的风险。在加拿大,製药业是该国最具创新性的行业之一。除了非处方药外,名单还包括开发和製造独特学名药的公司。

北美无菌包装产业概况

无菌包装透过使用纸盒和环保袋来推动需求,迎合喜欢较小、更频繁购买的消费者。此外,随着消费者对不含防腐剂的有机产品的需求日益增长,製造商正在透过投资优质包装解决方案来应对,以保持新鲜度并延长保质期。

北美无菌包装市场竞争激烈,因为多家供应商向国内和国际市场供应产品。市场是细分的,领先的公司采用各种策略来扩大影响力并保持竞争力。该市场的主要参与企业包括 Amcor Group、DS Smith Plc 和 Schott AG。

其他好处

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场洞察

- 市场概况

- 产业价值链分析

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买方议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间的敌对关係

- 技术简介

第五章市场动态

- 市场驱动因素

- 低温运输物流降低成本的需求日益增加

- 产品长期储存的需求不断增加

- 市场限制因素

- 製造复杂性增加,投资收益降低

第六章 市场细分

- 产品类型

- 塑胶瓶

- 预充注射器

- 管瓶和安瓿

- 袋子和小袋

- 纸盒

- 杯子

- 玻璃瓶

- 最终使用者类型

- 药品

- 饮料

- 水果型

- 乳类饮料

- 准备喝

- 其他饮料

- 食物

- 以水果为主

- 乳製品

- 加工食品

- 婴儿食品

- 汤/高汤

- 其他食品工业

- 国家名称

- 美国

- 加拿大

第七章 竞争格局

- 公司简介

- Tetra Pak International SA

- Amcor Group

- Sealed Air Corporation

- SIG Combibloc Group

- WestRock Company

- Schott AG

- Scholle IPN

- DS Smith PLC

- Elopak AS

- Mondi PLC

第八章投资分析

第九章 市场机会及未来趋势

The North America Aseptic Packaging Market size is estimated at USD 13.82 billion in 2025, and is expected to reach USD 21.71 billion by 2030, at a CAGR of 9.45% during the forecast period (2025-2030).

The market is witnessing significant growth, driven by the rising need for extended shelf life and the preservation of food and beverages without refrigeration. Furthermore, technological advancements in packaging that bolster product safety and quality play a pivotal role in propelling the market forward.

Key Highlights

- As demand for long-distance transportation surges, extending shelf life has become paramount. Packaging must enhance its durability and protective features with growing distances between manufacturing sites and end users. North America's penchant for packaged and ready-to-eat meals is driving the adoption of aseptic packaging.

- The end-user industries, such as food and beverage, prioritize sustainable packaging and extended shelf life. Many regional food and beverage vendors are leaning towards aseptic packaging, weighing both cost and environmental benefits, particularly for ambient shipping and storage. Furthermore, aseptic packaging utilizes recyclable cartons and eco-friendly pouches. These options often appeal to consumers favoring smaller quantities and more frequent purchases, driving significant demand for such products in the region.

- Consumer health and wellness consciousness is on the rise. They are willing to invest more in products that align with this wellness trend, from morning juices to energy drinks. Therefore, there's a surging demand for cost-effective packaging solutions in the beverage packaging segment. Furthermore, the growing preference for aseptic cartons, especially from the milk and dairy beverage sectors, is set to invigorate the market. These cartons facilitate easy stacking and extend the product's shelf life.

- As per the Beverage Report by the Association for Packaging and Processing Technologies (PMMI), North America's beverage industry is projected to expand by approximately 4.5% by 2028. This burgeoning beverage market is poised to propel the growth of the studied market. In the region's pharmaceutical sector, particularly in the United States, there's been a significant surge in demand for aseptic packaging. This uptick is primarily driven by the increasing availability and consumption of biotechnology-based drugs and various liquid pharmaceuticals' aseptic filling needs.

- In response to rising customer demands and the imperative to control storage and distribution costs, companies are leveraging connected technologies like sensors, RFID, and NFC and channeling investments into advanced technologies. These investments aim to substantially cut down or eliminate costs associated with managing products from manufacturers to retailers.

- However, several challenges loom over the aseptic packaging market, potentially hindering its revenue growth. The initial capital outlay for aseptic packaging can be two to three times higher than that of conventional fresh production methods. Furthermore, involving research teams from the beginning is crucial, enabling formula tweaks specific to aseptic processing. Yet, this necessity can significantly escalate the costs of aseptic packaging when posed with traditional methods.

North America Aseptic Packaging Market Trends

Beverages Segment is Expected to Hold a Significant Market Share

- As consumers increasingly prioritize health and wellness, the demand for fruit-based ready-to-drink beverages is surging, especially with a focus on cost-effective packaging. This trend is expected to intensify over the forecast period. Aseptic packaging not only extends the shelf life of these beverages but also introduces innovations like shelf-stable fruit juices.

- Convenience is emerging as a dominant trend in ready-to-drink beverages and health-focused categories across North America. Given the extensive preparation required for homemade beverages, consumers gravitate towards ready-to-drink cocktails. This shift highlights a significant trend: consumers are drawn to the unique flavors of these cocktails and value the ease of enjoying them outside the home.

- Global trends in the dairy industry reveal a push towards product differentiation through innovative packaging. Today's dairy product packaging often boasts eye-catching designs and advanced aseptic features. This emphasis on packaging innovation is a response to fierce competition in key North American markets.

- Aseptic milk, treated with ultra-high-temperature pasteurization, effectively eliminates harmful bacteria. The dairy category is diverse, encompassing not just white milk and its byproducts like ghee, buttermilk, and yogurt-based beverages but also the promising realm of flavored milk. Aseptic processing and packaging, free from preservatives, significantly enhance shelf life and freshness-vital attributes for perishable items like milk.

- The dairy industry's growing appetite for aseptic packaging signals a broader trend. With rising milk production, new global market opportunities are on the horizon. For context, the USDA projects U.S. cow milk production to increase from 217,600 million pounds in 2018 to approximately 228,200 million in 2024. Additionally, a notable consumer shift has been the surging demand for UHT milk, prized for its extended shelf life, allowing consumers to reduce store visits. Furthermore, with the effect pandemic, there was a marked preference for the sterile packaging of UHT milk over traditional packaged fresh and bulk milk, underscoring a significant evolution in dairy consumption patterns.

Canada is Expected to Witness Growth in the Market

- Investments continue to flow into the Canadian dairy sector, bolstering the nation's economy. Responding to regional demands, the Canadian government is championing the adoption of advanced packaging technologies, particularly aseptic packaging. Health-conscious millennials and the younger generation in Canada increasingly gravitate towards milk, juices, and energy drinks, driven by a heightened awareness of the risks of excessive sweets, carbonated sodas, and artificial sugars.

- In Canada, consumers are increasingly opting for milk cartons over glass bottles and plastic alternatives, driven by eco-friendly concerns and the cost-effectiveness of cartons. A report from StatCan in May 2024 highlighted that Canada's production of standard 3.25% milk rose from about 438.38 thousand kiloliters in 2020 to 468.07 thousand kiloliters in 2023. Aseptic liquid packaging is preferred for perishable items in the dairy-based beverages sector. Given the nature of dairy products, the quality of packaging is paramount for these highly perishable liquid foods and beverages.

- Aseptic solution providers are addressing challenges in the dairy packaging arena. Nearly 60% of products using aseptic packaging are dairy items, including spoonable yogurt, cheese, cream, and ice cream. Dairy consumption spans natural, powdered, and processed cheese, but perishability remains a pressing concern. Aseptic packaging can extend cheese's shelf life by an impressive 60 days.

- Consequently, end users are channeling substantial investments into packaging. Given dairy's vulnerability to fragrance transfer and decomposition from oxygen exposure, packaging must boast superior barrier qualities. Data from StatCan reveals a notable uptick in Canada's dairy product sales: from January to May 2024, monthly manufacturer sales surged from CAD 1.39 billion (USD 1.03 billion) to CAD 1.67 billion (USD 1.24 billion).

- Further, aseptic pharmaceutical manufacturing, often termed fill-finish manufacturing, is crucial in producing vaccines, biologics, injectable drugs, cancer treatments, and various forms of ear, nasal, and eye drops. This method significantly reduces the risk of contaminating medications with germs or other harmful substances. In Canada, the pharmaceutical sector stands out as one of the nation's most innovative industries. It encompasses companies developing and producing creative and generic medicines alongside over-the-counter drug products.

North America Aseptic Packaging Industry Overview

Aseptic packaging utilizes cartons and eco-friendly pouches and caters to consumers who favor smaller, more frequent purchases, driving demand. Furthermore, as consumers increasingly seek organic products without preservatives, manufacturers are responding by investing in premium packaging solutions that preserve freshness and extend shelf life.

The North America Aseptic Packaging Market is competitive owing to the presence of multiple vendors in the market supplying their products in domestic and international markets. The market appears fragmented, with major players adopting various strategies to expand their reach and stay competitive. Some of the major players in the market are Amcor Group, DS Smith Plc, Schott AG, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness- Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Technology Snapshot

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Demand to Reduce the Cost of Cold Chain Logistics

- 5.1.2 Increasing Demand for the Longer Shelf Life of Products

- 5.2 Market Restraint

- 5.2.1 Manufacturing Complications and Lower Return on Investments

6 MARKET SEGMENTATION

- 6.1 Product Type

- 6.1.1 Plastic Bottles

- 6.1.2 Prefillabe Syringes

- 6.1.3 Vials and Ampoules

- 6.1.4 Bags and Pouches

- 6.1.5 Cartons

- 6.1.6 Cups

- 6.1.7 Glass Bottles

- 6.2 End- User Type

- 6.2.1 Pharmaceutical

- 6.2.2 Beverage

- 6.2.2.1 Fruit-based

- 6.2.2.2 Milk and Other Dairy Beverages

- 6.2.2.3 Ready-to-Drink

- 6.2.2.4 Other Beverage Industry Types

- 6.2.3 Food

- 6.2.3.1 Fruit-based

- 6.2.3.2 Dairy Food

- 6.2.3.3 Processed Foods

- 6.2.3.4 Baby Foods

- 6.2.3.5 Soups and Broths

- 6.2.3.6 Other Food Industry Types

- 6.3 Country

- 6.3.1 United States

- 6.3.2 Canada

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Tetra Pak International S.A.

- 7.1.2 Amcor Group

- 7.1.3 Sealed Air Corporation

- 7.1.4 SIG Combibloc Group

- 7.1.5 WestRock Company

- 7.1.6 Schott AG

- 7.1.7 Scholle IPN

- 7.1.8 DS Smith PLC

- 7.1.9 Elopak AS

- 7.1.10 Mondi PLC

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

无菌包装市场预测至2032年:按包装类型、材料、应用和地区分類的全球分析

无菌包装市场预测至2032年:按包装类型、材料、应用和地区分類的全球分析 无菌包装市场按应用、技术、材料、产品类型、最终用户和分销管道划分-2025-2032 年全球预测

无菌包装市场按应用、技术、材料、产品类型、最终用户和分销管道划分-2025-2032 年全球预测 2025年无菌包装全球市场报告2025年植物来源食品包装全球市场报告

2025年无菌包装全球市场报告2025年植物来源食品包装全球市场报告 无菌包装市场-全球产业规模、份额、趋势、机会与预测,按类型、材料、应用、地区和竞争细分,2020-2030 年

无菌包装市场-全球产业规模、份额、趋势、机会与预测,按类型、材料、应用、地区和竞争细分,2020-2030 年 2025-2033年无菌包装市场报告(按类型、材料、应用和地区)

2025-2033年无菌包装市场报告(按类型、材料、应用和地区) 无菌包装:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030 年)

无菌包装:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030 年) 无菌包装市场规模、份额及成长分析(按材料、类型、应用和地区)-2025-2032 年产业预测灭菌包装市场:按包装类型、材料、应用和地区划分医疗植入无菌包装市场:依产品类型、依材料类型、依应用、按地区

无菌包装市场规模、份额及成长分析(按材料、类型、应用和地区)-2025-2032 年产业预测灭菌包装市场:按包装类型、材料、应用和地区划分医疗植入无菌包装市场:依产品类型、依材料类型、依应用、按地区