|

市场调查报告书

商品编码

1639420

中国资料中心冷却:市场占有率分析、产业趋势与统计、成长预测(2025-2031)China Data Center Cooling - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

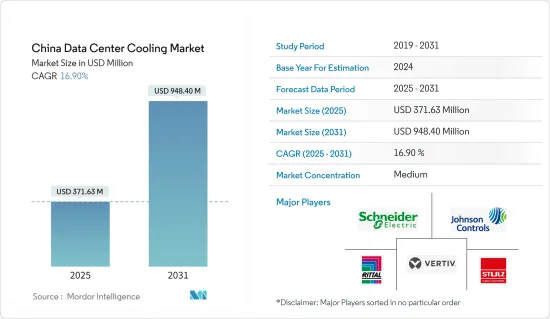

预计2025年中国资料中心冷却市场规模为3.7163亿美元,预估至2031年将达9.484亿美元,预测期间(2025-2031年)复合年增长率为16.9%。

主要亮点

- 中小企业越来越多地采用云端运算、政府对资料安全的严格要求以及国内企业加大投资等因素是推动中国资料中心需求的关键因素。

- 预计2030年,中国资料中心市场未来IT负载容量将达到4,000MW以上。此外,到 2030 年,中国的占地面积预计将超过 1,200 万平方英尺。

- 到2030年,预计全国将安装超过60万个机架。北京、广东、河北、江苏和上海在机架安装方面处于领先地位。珠江流域年平均气温超过20℃,影响资料中心设施的冷却需求。

- 中国已有近 19 个海底电缆系统投入运作,还有多个正在建设中。值得注意的是,2023年4月,中国官方通讯宣布了价值5亿美元的大规模海底光纤网路的计画。该网络连接亚洲、中东和欧洲,定位为对美国类似倡议的直接挑战。

中国资料中心散热市场趋势

液体冷却将成为预测期内成长最快的领域之一

- 技术进步简化了液体冷却的维护、可扩展性和经济性。这使得热带地区的资料中心流体消费量减少了 15% 以上,在温暖地区则减少了 80%。此外,在液冷运作期间利用的能量可以重新用于建筑和水加热。此外,先进合成冷媒的引入有助于减少与空调系统相关的碳排放。

- 水冷却在控制排放和减缓气候变迁方面发挥着至关重要的作用。与风冷资料中心相比,使用水冷却的资料中心消耗的能源大约减少 10%,二氧化碳排放减少 10%。此外,2023年11月,中国开始在海南省三亚市沿海建设最先进的商业水下资料中心。这项开创性计划旨在透过利用深海、节约能源和土地来实现工业转型。随着中国资料中心数量的增加,越来越多地采用液体冷却来防止机架伺服器过热。

- 直接液体冷却解决方案的部分电源使用效率 (PUE) 为 1.02 至 1.03,略高于最高效的空气冷却系统。令人惊讶的是,直接液体冷却 (DLC) 系统的能源效率并不是主要取决于 PUE。在传统设定中,伺服器风扇从机架获取电力,并且此电力消耗会计入 PUE 计算的 IT 电力部分。

IT 和通讯将对 2023 年的市场占有率做出重大贡献

- 到2024年初,中国的网路用户数量将超过印度和美国,领先全球。中国网路用户规模达10.9亿,普及率已超过75%。此外,中国社群媒体用户规模已达10.6亿,占总人口的74%以上。中国正积极加强5G网路建设,推动6G研究,打造製造业和数位经济强国。随着这些技术的扩展,对资料中心冷却的需求随着对资料中心的依赖的增加而增加。

- 网路对中国的影响是巨大的。网路技术在推动研发、增强中国经济以及连接广大人口方面发挥着至关重要的作用。根据工信部报告,截至2023年6月,中国已部署5G基地台超过293万个。此次推出恰逢 5G 智慧型手机用户数量激增至超过 6.76 亿,物联网连接设备数量激增至 21.2 亿。

- 人工智慧的兴起正在增加资料中心冷却水的消费量。为此,中国政府于2020年推出了「东方资料、西方计算」倡议。该措施旨在将资料中心从人口稠密的沿海地区转移到该国的西部地区。自然冷却、较低的电费、绿色能源的可用性和较低的土地成本等因素正在推动这项策略转变。这些措施是为了满足资料中心不断增长的冷却需求。

中国资料中心冷冻产业概况

中国资料中心冷却市场的竞争并不激烈,但近年来已经出现了重要的竞争对手。从市场占有率来看,该市场由少数大公司主导,包括Stulz GmbH、施耐德电气和Vertiv Group Corp。 STULZ GmbH、Schneider Electric SE 和 Vertiv Group Corp. 等公司提供液体和空气冷却产品。

其他好处

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场洞察

- 市场概况

- 考虑关键的冷却成本

- 从直流冷却角度分析与直流运转相关的主要成本开销

- 透过设计复杂性、PUE 优点、缺点和自然天气条件覆盖范围等关键因素,对与每种冷却技术相关的成本和操作考虑因素进行比较研究。

- 资料中心冷却的关键创新和发展

- 资料中心使用的关键能源效率方法

第五章市场动态

- 市场驱动因素

- 创新的资料中心冷却技术推动市场成长

- 对资料中心的需求不断增长推动市场成长

- 市场问题

- 资料中心冷却的能源消耗增加和水资源短缺阻碍了市场成长

- 市场机会

- 永续性且节能的资料中心冷却解决方案提供市场机会

- 产业生态系分析

第六章 中国资料中心足迹现况分析

- 资料中心IT负载能力与占地面积分析(2017-2030年期间)

- 目前中国DC热点及未来拓展前景分析

- 中国主要资料中心承包商和营运商分析

第七章 市场区隔

- 透过冷却技术

- 空气冷却

- 冷却器和节热器

- CRAH

- 冷却塔(包括直接冷却、间接冷却、两级冷却)

- 其他风冷技术

- 液基冷却

- 浸没式冷却

- 晶片间直接冷却

- 后门热交换器

- 空气冷却

- 按类型

- 超大规模资料中心业者(自有和租赁)

- 企业(本地)

- 搭配

- 按最终用户产业

- 资讯科技和电讯

- 零售/消费品

- 医疗保健

- 媒体娱乐

- 联邦机构

- 其他的

第八章 竞争格局

- 公司简介

- Schneider Electric SE

- Johnson Controls Inc.

- GIGA-BYTE Technology Co. Ltd

- Vertiv Group Corp.

- Carrier Global Corporation

- Rittal Gmbh & Co. KG

- Munters Group

- Stulz GmbH

- Kstar Ltd

- Alfa Laval AB

第九章投资分析

第十章市场机会与未来趋势

第11章 关于出版商

The China Data Center Cooling Market size is estimated at USD 371.63 million in 2025, and is expected to reach USD 948.40 million by 2031, at a CAGR of 16.9% during the forecast period (2025-2031).

Key Highlights

- Factors such as the rising adoption of cloud computing by SMEs, stringent government mandates on local data security, and increased investments by domestic enterprises are key drivers fueling the demand for data centers in the nation.

- The upcoming IT load capacity of the Chinese data center market is expected to reach more than 4,000 MW by 2030. The country's construction of raised floor area is expected to increase to more than 12 million sq. ft by 2030.

- By 2030, the country is projected to install over 600,000 racks. Beijing, Guangdong, Hebei, Jiangsu, and Shanghai are poised to lead in rack installations. The Pearl River Valley maintains an average annual temperature exceeding 20°C, influencing the need for cooling in data center facilities.

- China boasts nearly 19 operational submarine cable systems, with several more in construction. Notably, in April 2023, China's state-owned news agency unveiled plans for a significant undersea fiber optic network valued at USD 500 million. This network is designed to link Asia, the Middle East, and Europe, positioning itself as a direct competitor to analogous US initiatives.

China Data Center Cooling Market Trends

Liquid-based Cooling to be One of the Fastest-growing Segment During the Forecast Period

- Technological advancements have streamlined the maintenance, scalability, and affordability of liquid cooling. This has led to a reduction in data center liquid consumption by over 15% in tropical regions and a substantial 80% in more temperate zones. Moreover, the energy harnessed during liquid cooling operations can be repurposed to heat both buildings and water. Additionally, the deployment of advanced artificial refrigerants is proving instrumental in curbing the carbon footprint associated with air conditioning systems.

- Water cooling plays a pivotal role in curbing emissions and mitigating climate disruptions. Data centers that leverage water for cooling consume roughly 10% less energy than their air-cooled counterparts, resulting in a corresponding 10% reduction in CO2 emissions. Moreover, in November 2023, China began constructing a cutting-edge commercial underwater data center off the coast of Sanya in the Hainan province. This pioneering project seeks to transform the industry by tapping into the ocean's depths, conserving energy and land. With the rising number of data centers in China, the adoption of liquid cooling is on the rise, aiming to safeguard rack servers from overheating.

- Direct liquid cooling solutions boast a partial power usage effectiveness (PUE) ranging from 1.02 to 1.03, edging out the most efficient air cooling systems by a slim margin. Surprisingly, the energy gains of Direct Liquid Cooling (DLC) systems are not primarily attributed to their PUE. In traditional setups, server fans draw power from the rack, and this power consumption is factored into the IT power section of the PUE calculation, as these fans are integral components of the data center's overall energy consumption.

IT and Telecommunication Contributed Significant Market Share in 2023

- By the beginning of 2024, China had led the globe in terms of internet user numbers, outstripping India and the United States. The country boasted a staggering 1.09 billion internet users, with a penetration rate exceeding 75%. Furthermore, China's social media user base reached 1.06 billion, representing over 74% of its population. The country is actively enhancing its 5G network and advancing 6G research to establish China as a manufacturing and digital economic powerhouse. As these technologies expand, the demand for data center cooling rises in tandem with the growing reliance on data centers.

- The internet's influence on China is profound. Internet technologies drive research and development and play a pivotal role in bolstering the nation's economy and linking its vast population. MIIT reported that by June 2023, China had deployed over 2.93 million 5G base stations. This rollout coincided with a surge in 5G smartphone users, surpassing 676 million, and a substantial 2.12 billion Internet of Things-connected devices.

- The rise of AI has led to heightened water consumption for data center cooling. In response, the Chinese government introduced the "Eastern-Data, Western-Computing" initiative in 2020. This initiative aims to relocate data centers from densely populated coastal areas to the country's western regions. Factors such as natural cooling, reduced electricity costs, availability of green energy, and lower land expenses are driving this strategic shift. These measures are designed to meet the escalating demands for data center cooling.

China Data Center Cooling Industry Overview

The Chinese data center cooling market is moderately competitive but has gained a significant competitive edge in recent years. A handful of major players, including Stulz GmbH, Schneider Electric SE, and Vertiv Group Corp., dominate the market in terms of market share. Companies such as STULZ Gmbh, Schneider Electric SE, and Vertiv Group Corp. offer liquid and air-based cooling products.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Key Cost Considerations for Cooling

- 4.2.1 Analysis of the Key Cost Overheads Related to DC Operations with an Eye on DC Cooling

- 4.2.2 Comparative Study of the Cost and Operational Considerations Related to Each Cooling Technology Based on Key Factors Such as Design Complexity, PUE Advantages, Drawbacks, Extent of Utilization of Natural Weather Conditions

- 4.2.3 Key Innovations and Developments in Data Center Cooling

- 4.2.4 Key Energy Efficiency Practices Adopted in Data Centers

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Innovative Data Center Cooling Technologies To Drive Market Growth

- 5.1.2 Increasing Data Center Demand To Drive Market Growth

- 5.2 Market Challenges

- 5.2.1 Higher Energy Consumption And Water Scarcity For Data Center Cooling To Hinder Market Growth

- 5.3 Market Opportunities

- 5.3.1 Sustainability and Energy Efficient Data Center Cooling Solutions To Provide Market Opportunity

- 5.4 Industry Ecosystem Analysis

6 ANALYSIS OF THE CURRENT DATA CENTER FOOTPRINT IN CHINA

- 6.1 Analysis of IT Load Capacity and Area Footprint of Data Centers (for the period of 2017-2030)

- 6.2 Analysis of the current DC hotspots and scope for future expansion in China

- 6.3 Analysis of major Data Center Contractors and Operators in China

7 MARKET SEGMENTATION

- 7.1 By Cooling Technology

- 7.1.1 Air-based Cooling

- 7.1.1.1 Chiller and Economizer

- 7.1.1.2 CRAH

- 7.1.1.3 Cooling Tower (Covers Direct, Indirect, and Two-stage Cooling)

- 7.1.1.4 Other Air-based Cooling Technologies

- 7.1.2 Liquid-based Cooling

- 7.1.2.1 Immersion Cooling

- 7.1.2.2 Direct-to-chip Cooling

- 7.1.2.3 Rear-door Heat Exchanger

- 7.1.1 Air-based Cooling

- 7.2 By Type

- 7.2.1 Hyperscaler (Owned and Leased)

- 7.2.2 Enterprise (On-premise)

- 7.2.3 Colocation

- 7.3 By End-user Industry

- 7.3.1 IT and Telecom

- 7.3.2 Retail and Consumer Goods

- 7.3.3 Healthcare

- 7.3.4 Media and Entertainment

- 7.3.5 Federal and Institutional agencies

- 7.3.6 Other End-user Industries

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles

- 8.1.1 Schneider Electric SE

- 8.1.2 Johnson Controls Inc.

- 8.1.3 GIGA-BYTE Technology Co. Ltd

- 8.1.4 Vertiv Group Corp.

- 8.1.5 Carrier Global Corporation

- 8.1.6 Rittal Gmbh & Co. KG

- 8.1.7 Munters Group

- 8.1.8 Stulz GmbH

- 8.1.9 Kstar Ltd

- 8.1.10 Alfa Laval AB

9 INVESTMENT ANALYSIS

10 MARKET OPPORTUNITIES AND FUTURE TRENDS

11 ABOUT US

全球资料中心 CDU 市场按类型、冷却类型、最终用户和地区划分,预测至 2032 年

全球资料中心 CDU 市场按类型、冷却类型、最终用户和地区划分,预测至 2032 年 全球资料中心浸入式冷却液市场(至 2032 年)按技术(单相 vs. 双相)、资料中心类型(超大规模、AI/ML、加密货币挖矿)、类型(矿物油、氟碳基液体、合成液体)和地区划分

全球资料中心浸入式冷却液市场(至 2032 年)按技术(单相 vs. 双相)、资料中心类型(超大规模、AI/ML、加密货币挖矿)、类型(矿物油、氟碳基液体、合成液体)和地区划分 2025年全球资料中心冷却市场报告

2025年全球资料中心冷却市场报告 全球资料中心液浸冷却市场研究报告 - 产业分析、规模、份额、成长、趋势及2025年至2033年预测

全球资料中心液浸冷却市场研究报告 - 产业分析、规模、份额、成长、趋势及2025年至2033年预测 循环冷却市场按产品类型、冷却类型、安装类型、冷却能力和最终用户划分 - 全球预测 2025-2030资料中心浸入式冷却市场(按组件、技术类型、资料中心规模、部署类型和最终用户划分)- 全球预测,2025 年至 2030 年

循环冷却市场按产品类型、冷却类型、安装类型、冷却能力和最终用户划分 - 全球预测 2025-2030资料中心浸入式冷却市场(按组件、技术类型、资料中心规模、部署类型和最终用户划分)- 全球预测,2025 年至 2030 年 2021-2031 年北美资料中心冷却市场报告(范围、细分、动态和竞争分析)

2021-2031 年北美资料中心冷却市场报告(范围、细分、动态和竞争分析) 2021-2031 年欧洲资料中心冷却市场报告(范围、细分、动态和竞争分析)

2021-2031 年欧洲资料中心冷却市场报告(范围、细分、动态和竞争分析) 2021-2031年亚太地区资料中心冷却市场报告(范围、细分、动态和竞争分析)

2021-2031年亚太地区资料中心冷却市场报告(范围、细分、动态和竞争分析) 全球资料中心冷却市场(至 2032 年)按解决方案(空调、冷却装置、冷却塔、节热器係统、液体冷却系统和控制系统)、服务、冷却类型、资料中心类型、最终用户产业和地区划分

全球资料中心冷却市场(至 2032 年)按解决方案(空调、冷却装置、冷却塔、节热器係统、液体冷却系统和控制系统)、服务、冷却类型、资料中心类型、最终用户产业和地区划分