|

市场调查报告书

商品编码

1640630

欧洲 3D 列印 -市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Europe 3D Printing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

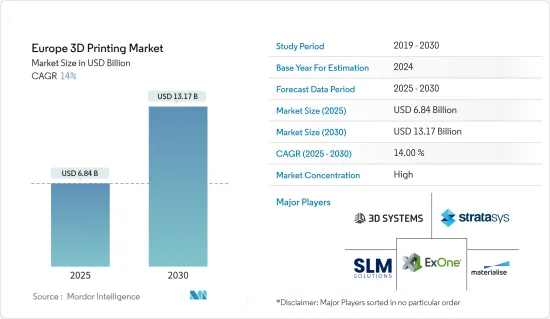

预计 2025 年欧洲 3D 列印市场规模为 68.4 亿美元,到 2030 年将达到 131.7 亿美元,预测期内(2025-2030 年)的复合年增长率为 14%。

欧洲是3D列印技术的领先中心。在欧洲,大多数需求来自需要快速、稳定且价格实惠的原型的中小型企业。

关键亮点

- 3D列印技术将从根本上颠覆许多领域的传统生产,因为它可以以更低的成本提供差异化的产品和解决方案。由于政府的倡议和投入,以及 3D 列印为客製化产品、提高效率和改善产品品质提供的机会,该技术在欧洲的发展主导。

- 3D 列印技术在工业产品、航太、汽车、国防、医疗、教育和研究等各个应用领域的应用日益广泛,推动 3D 列印市场的成长。

- 不过,有人指出,采用3D列印技术的一大障碍是初始成本高。这些支出包括软体、硬体、材料、积层製造和製造专业知识、认证和工人培训。建立3D系统所需的资金和人力远远超过标准列印技术所需的。然而,随着商用桌面 3D 列印机的推出,该公司正在帮助最终用户避免高昂的前期成本。

- 3D列印技术已显着渗透至医疗、航空等关键产业领域,并以可观的成长率成长。飞机製造商正在投资数十亿美元开发这项技术,利用金属粉末製造涡轮叶片、喷射发动机燃烧喷嘴和结构部件。

- 阻碍市场成长的主要因素包括缺乏标准流程控制、可用性有限以及 3D 列印材料成本高。

欧洲 3D 列印市场趋势

3D 原型零件在汽车产业的采用率很高

- 欧洲汽车工业蓬勃发展,已成为各国发展和财富的先驱和推动力量。过去几年里,欧洲汽车产业已跃居全球产业前列。

- 欧洲是许多全球汽车OEM的所在地,3D 列印技术已广泛应用于汽车产业的设计、研发应用。 BMW、宾士、奥迪、捷豹路虎和大众等汽车产业的主要企业正在欧洲市场为 3D 技术和印表机创造潜在空间。

- 根据OICA预测,2023年德国将成为欧洲最大的乘用车生产国,产量达411万辆。排名第二的是西班牙,乘用车产量为191万辆。

- 2022年4月,黑石科技公司製定了销售电动车3D列印钠离子电池的计画。该公司计划在德国多伯恩的一个原型工厂投资 3,200 万欧元(33,905,316 美元),并在本世纪中叶推出 3D 列印固态电池。固态电池将首先安装在柏林的电动公车上,并在真实场景中进行测试。

- 此外,位于德国梅尔肯尼格的福特快速技术中心采用了多种 3D 列印技术来在短时间内生产原型。工程师和设计师无需前置作业时间将工作发送给公司,而是可以在几小时内获得他们的设计。设计师可以在快速技术中心创建当天原型,并在几个小时内创建多个设计迭代。福特增材製造专家 Bruno Alves 表示,实体原型比数位模型具有优势:

德国可望占据主要份额

- EOS、Renishaw、SLM Solutions、Ultimaker 和 Photocentric 等来自各行各业的老字型大小企业因其在增材製造领域的技术专长而闻名于整个欧洲。 3D列印机主要集中在西欧,其中德国、英国、义大利、法国等国家推动AM的发展和应用。

- 此外,该地区各国对市场的投资不断增加可能会进一步创造巨大的需求。据德国贸易投资署 (GTAI) 称,德国拥有欧洲最先进的 3D 列印和积层製造业务,包括航太、汽车、家电和牙科。

- 根据德国联邦统计局预测,2023年德国汽车产业收益将达4,576亿欧元(4,936亿美元),较前一年有所成长。

- 德国三分之一的大型工业公司已经在使用 3D 列印机,三分之二的公司已开始利用这项技术。这可能为市场参与企业创造有利可图的机会,以扩大他们在该国的影响力,从而促进市场成长。

- 例如,2022年12月,德国3D列印技术供应商Headmade Materials宣布有意加入冷金属融合联盟(Cold Metal Fusion Alliance)和其他重要的市场参与企业。 ColdMetalFusion 是产业领导者的伙伴关係,拥有几代烧结、积层製造和传统工业製造经验。联盟合作伙伴共同为金属製造客户提供服务、材料、设备和技术。

欧洲3D列印产业概况

欧洲拥有大量影响3D列印市场的全球性和地区性公司,但欧洲市场的大部分由主要企业主导。因此,预计 3D 列印市场将呈现整合趋势。 3D Systems Corporation、Materialise NV、Stratasys Ltd.、ExOne Co.、SLM Solutions Group AG 等是欧洲市场的主要企业。所有这些参与企业都参与了竞争策略,包括收购、合作、新产品开发和市场开发,以巩固主导地位。

2022年10月,赛峰集团将在法国开设一个新的积层製造园区。赛峰集团新建的 12,500平方公尺工厂汇集了透过积层製造生产零件所需的所有步骤,从研发到工程和製造。该工厂配备了最先进的设备,例如3D列印机,利用3D数位影像将金属粉末转化为飞机和引擎零件,目前工厂运作100多名顶尖工程师、科学家和技术人员,齐心协力製造所有部分。

2022年7月,一家欧洲汽车公司推出了一款SLM Solutions金属3D列印机。该客户拥有超过 10 台 3D持有,其中包括多台 SLM 500 和 SLM 250 系统。该公司可能会使用金属 AM 来製造汽车零件,重点是连续製造。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买家的议价能力

- 供应商的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 产业价值链分析

- COVID-19 工业影响评估

第五章 市场分析

- 市场驱动因素

- 政府措施和支出

- 轻鬆开发客製化产品

- 市场问题

- 启动成本高,技术纯熟劳工短缺

第六章 市场细分

- 按组件

- 硬体

- 按服务

- 依技术分类

- 立体光刻技术(SLA)

- 熔融沉积建模(FDM)

- 电子束熔炼

- 数位光处理

- 选择性雷射烧结 (SLS)

- 其他的

- 按最终用户产业

- 车

- 航太和国防

- 医疗

- 建筑学

- 活力

- 食物

- 其他的

- 按国家

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 荷兰

第七章 竞争格局

- 公司简介

- Stratasys Ltd.

- 3D Systems Corporation

- EOS GmbH

- General Electric Company(GE Additive)

- Sisma SPA

- ExOne Co.

- SLM Solutions Group AG

- Hewlett Packard Inc.

- Ultimaker BV

- Materialise NV

第八章投资分析

第九章:市场的未来

The Europe 3D Printing Market size is estimated at USD 6.84 billion in 2025, and is expected to reach USD 13.17 billion by 2030, at a CAGR of 14% during the forecast period (2025-2030).

Europe is a major hub for 3D printing technology. In Europe, the majority of demand is coming from SMEs that need high-speed, robust, and reasonably priced prototypes.

Key Highlights

- The use of 3D printing technology will radically disrupt conventional production in many sectors, as it is capable of delivering differentiated products and solutions at a lower cost. This technology is taking the lead in Europe, thanks to initiatives and spending of governments, opportunities for offering customized products through 3D printing, increased efficiency as well and higher product quality.

- The increase in the rate of adoption of 3D printing technology in various application segments, such as industrial products, aerospace, automotive, defense, healthcare, education & research, are facilitating the growth of the 3D printing market.

- However, the significant barrier to implementing 3D printing technology has been identified as expensive initial costs. This expenditure includes software, hardware, materials, additive and manufacturing expertise, certification, and worker training. The cash and manpower necessary to build a three-dimensional system are significantly more than those needed for standard printing technologies. However, with the commercial desktop 3D printer launch, companies are assisting end-customers in lowering the expensive initial expenses.

- The significant penetration of 3D printing technology was observed in important industry segments like health and aeronautics, where growth is increasing at a promising rate. 3D printing is helping to create more efficient processes in the aerospace sector; aircraft manufacturers have invested billions in developing the use of metal powders through this technology to make turbine blades, jet engine combustion nozzles, and structural parts.

- Nonetheless, some of the major factors inhibiting market growth include lack of standard process control and limited availability or significant costs in terms of 3D printing materials.

Europe 3D Printing Market Trends

High Adoption of 3D Prototype Parts in Automotive Industry

- The European automotive sector has been thriving and has emerged as a pioneer and driving force behind the country's development and wealth. In past years, the European automotive sector has risen to the forefront of the global industry.

- With the presence of many global automotive OEMs, Europe enjoys the broad-scale implementation of 3D printing technology for design formulation and R&D applications in the automotive industry. Top automotive leaders such as BMW, Mercedes, Audi, Jaguar Land Rover, Volkswagen, and many others have created a potential space for 3D technology and printers in the European market.

- According to OICA, in 2023, Germany produced the most significant passenger cars in Europe, 4.11 million. Spain ranked second, with almost 1.91 million passenger cars produced.

- In April 2022, Blackstone Technology formulated a plan to market 3D-printed sodium-ion cells for electric cars. The business plans to launch its 3D-printed solid-state battery in the middle of the decade after investing EUR 32 million (USD 33,900,531.60 Million) in a prototype facility in Dobeln, Germany. The solid-state batteries would first be put in the electric buses in Berlin to be tested in a real-world scenario.

- Moreover, several 3D printing methods are employed to manufacture prototypes with rapid turnaround times at Ford's Rapid Technologies Center in Merkenich, Germany. Instead of sending a task out to a business with a several-week lead time, engineers and designers can have their designs in their hands within hours. Designers can create same-day prototypes in the Rapid Technology Center, iterating on numerous designs in a matter of hours. According to Bruno Alves, an additive manufacturing expert at Ford, physical prototypes can have advantages over digital models.

Germany is Expected to Hold the Major Share

- A wide range of established industry players, including EOS, Renishaw, SLM Solutions, Ultimaker, and Photocentric, are well-known throughout Europe for their technical expertise in the field of additive manufacturing. The majority of 3D printers are located in Western Europe, with countries such as Germany, the United Kingdom, Italy, and France driving AM development and applications.

- Moreover, increasing investments in the market studied by various countries in the region may further create significant demand. According to GTAI (Germany Trade & Investment), Germany is home to some of Europe's most advanced 3D printing and additive manufacturing businesses, including aerospace, automotive, equipment, and dentistry.

- According to Statistisches Bundesamt, in 2023, the German automobile industry generated revenues of EUR 457.6 billion (USD 493.6 billion) in the motor vehicles segment, an increase from the previous year.

- One in every three big German industrial companies already uses 3D printing, and two out of every three have already used the technology. This, in turn, may create lucrative opportunities for the market players to expand their footprint in the country, thus boosting market growth.

- For instance, in December 2022, HeadmadeMaterials, a German 3D printing technology provider, intended to enter the ColdMetalFusionAlliance and other significant market players. ColdMetalFusion is a partnership of industry leaders with generations of sintering, additive manufacturing, and traditional industrial production experience. Partners of the Alliance collaborate to provide services, materials, equipment, and technology to clients in the metal production business.

Europe 3D Printing Industry Overview

Though the presence of many regional as well as global players in the European region is influencing the 3D printing market, the major chunk of the European market is captured by prominent players. Hence, the market for 3D printing is expected to be consolidated in nature. 3D Systems Corporation, Materialise NV, Stratasys Ltd., ExOne Co., and SLM Solutions Group AG, among others, are some major players in the European market. All these players are involved in competitive strategic developments such as acquisition, partnership, new product development, and market expansion to augment their leadership position in the European 3D printing market.

In October 2022, Safran opened a new additive manufacturing campus in France. Safran's new 12,500 m2 facility houses all the procedures required to create parts utilizing additive manufacturing, from R&D through engineering and production. With cutting-edge equipment, including 3D printers that employ 3D digital images to transform metallic powders into airplane and engine parts, more than 100 top-tier engineers, scientists, and technicians are currently operating at the factory to make components for the whole team.

In July 2022, a European automobile company installed metal 3D printers from SLM Solutions. The customer has over ten machines in its 3D printing fleet, including many SLM 500 and SLM 250 systems. It is believed to be using metal AM to build car elements, emphasizing serial manufacturing.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of New Entrants

- 4.2.5 Threat Of Substitutes

- 4.2.6 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment Of COVID-19 Impact On The Industry

5 MARKET DYANMICS

- 5.1 Market Drivers

- 5.1.1 Initiatives and Spending By Government

- 5.1.2 Ease in Development of Customized Products

- 5.2 Market Challenges

- 5.2.1 High Initial Costs and a Scarcity of Skilled Workers

6 MARKET SEGMENTATION

- 6.1 By Component

- 6.1.1 Hardware

- 6.1.2 Services

- 6.2 By Technology

- 6.2.1 Stereo Lithography (SLA)

- 6.2.2 Fused Deposition Modeling (FDM)

- 6.2.3 Electron Beam Melting

- 6.2.4 Digital Light Processing

- 6.2.5 Selective Laser Sintering (SLS)

- 6.2.6 Other Technologies

- 6.3 By End-user Industry

- 6.3.1 Automotive

- 6.3.2 Aerospace and Defense

- 6.3.3 Healthcare

- 6.3.4 Construction and Architecture

- 6.3.5 Energy

- 6.3.6 Food

- 6.3.7 Other End-user Industries

- 6.4 By Country

- 6.4.1 Germany

- 6.4.2 United Kingdom

- 6.4.3 France

- 6.4.4 Italy

- 6.4.5 Spain

- 6.4.6 Netherlands

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Stratasys Ltd.

- 7.1.2 3D Systems Corporation

- 7.1.3 EOS GmbH

- 7.1.4 General Electric Company (GE Additive)

- 7.1.5 Sisma SPA

- 7.1.6 ExOne Co.

- 7.1.7 SLM Solutions Group AG

- 7.1.8 Hewlett Packard Inc.

- 7.1.9 Ultimaker BV

- 7.1.10 Materialise NV

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

2025年全球金属3D列印市场报告

2025年全球金属3D列印市场报告 3DP/AM市场洞察:2025年第2季

3DP/AM市场洞察:2025年第2季 3D 列印:材料和设备机会、趋势和市场

3D 列印:材料和设备机会、趋势和市场 3D 列印铸件市场(按技术、材料、客製化类型、应用和最终用户)—2025-2030 年全球预测3D列印市场(按组件、技术、材料和应用)—2025-2030年全球预测3D列印机器人市场(按机器人类型、技术、应用、最终用户和分销管道)—2025-2030年全球预测

3D 列印铸件市场(按技术、材料、客製化类型、应用和最终用户)—2025-2030 年全球预测3D列印市场(按组件、技术、材料和应用)—2025-2030年全球预测3D列印机器人市场(按机器人类型、技术、应用、最终用户和分销管道)—2025-2030年全球预测 多喷射融合 3D 列印技术市场:未来预测(2025-2030 年)陶瓷3D列印市场-2025年至2030年预测粉体熔化成型技术3D列印技术市场:2025-2030年预测

多喷射融合 3D 列印技术市场:未来预测(2025-2030 年)陶瓷3D列印市场-2025年至2030年预测粉体熔化成型技术3D列印技术市场:2025-2030年预测 印度的影音市场趋势

印度的影音市场趋势