|

市场调查报告书

商品编码

1642094

危险品物流:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Hazardous Goods Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

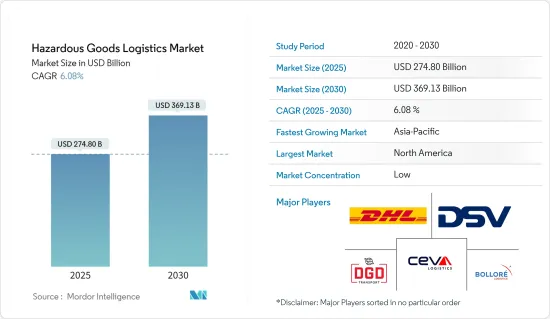

危险品物流市场规模预计在 2025 年为 2,748 亿美元,预计到 2030 年将达到 3,691.3 亿美元,预测期内(2025-2030 年)的复合年增长率为 6.08%。

在散装运输危险物品时,政府机构要求对每件产品进行准确的标记,以符合联邦法规。 2003年,联合国采用了一套全球系统来识别可能对身体、健康或环境造成风险的危险。危险物品分为易燃、腐蚀、气态九个危险类别。 UN编号是一个四位数字,范围从0004到3548,用于识别国际运输中使用的某些危险货物和危险材料。

危险品占国际货物的大部分,包括许多常用产品和物品。据称,这些货物大部分是汽油和其他石油产品。目前的石油繁荣可以归因于过去几年水力压裂带来的空前成长,以及政府为燃料生产所创造的有利环境。美国生产了世界上大部分的石油。

除了每年更新的众多危险物品法规外,运输危险物品的要求也预计将逐年增加。锂电池运输需求的不断增长,以及该地区成熟的天然气和石油业务,将推动危险物品市场创下历史新高,从而增加对联合国包装、培训、标籤和标誌的需求。

此外,还必须使用各种形式的运输工具来运输放射性药物、病毒样本、医疗危险化学品和手术器械等临床废弃物。例如,石油和天然气产业可能会影响全球危险物质的预期扩张。石油和天然气产业仍然是一个利润丰厚的产业,预计未来十年将获得总合2,370 亿美元的投资,占该产业全球投资总额的 25%。

危险品物流市场趋势

易燃液体出货量增加推动市场

医疗、核能、石油和天然气以及石化产业是新兴或已开发经济体中广泛使用危险物质的一些例子。运输危险物品的运输公司必须遵守标准程序,确保其车辆和船舶的安全。其他联邦机构关于危险物质、职场安全和环境保护的规定也适用。

未来几年,危险品物流市场可能会因日益严格的政府监管而受益匪浅。美国运输部部 (DOT) 管线和危险物质安全管理局 (PHMSA) 负责制定和执行危险物质安全运输的国家法规。当向美国、美国美国或在美国境内运送危险物品时,遵守危险物品法规(HMR 49,第 100-185 部分)至关重要。

联合国《危险货物运输示范条例》为各类运输方式製定标准化法规提供了参考。每两年出版一次新版本。为了方便贸易,促进危险货物的安全、高效运输,危险货物必须加贴专门为货船运输危险货物而设计的标籤或标记。更重要的是,它有助于使交通更加安全。

亚太地区占市场主导地位

促进亚太经合组织区域危险品运输安全能力建设课程(包括研讨会)于 2022 年 12 月 1 日至 2 日在普吉岛线上举行。培训班学员共53人,包括来自亚太经合组织11个成员经济体(中国、日本、韩国、马来西亚、秘鲁、菲律宾、新加坡、中国台北、泰国、美国和越南)和3个非成员经济体(柬埔寨、斯里兰卡和法国)的代表,以及相关国际和区域组织、港务局、大学、研究机构、专业协会和私营部门的代表。

2022财年曼谷港危险物品货柜总数为38,545 TEU。危险货物货柜数量最多的是第 9 类(14,034 TEU),其次是第 3 类(9,489 TEU)。同时,危险品货柜数量最少的是6.1类(3083TEU)。同样,林查班港的危险货物货柜总数为174,938 TEU。危险货物货柜数量最多的是第 9 类(59,734 TEU),其次是第 3 类(42,606 TEU)。

大规模的石化开发正在减少对汽油的需求。因此,石油和天然气等危险物质通常使用卡车运输服务在美国境内运输。

预计未来五年内美国将超过沙乌地阿拉伯和俄罗斯,成为世界最大石油生产国。对于石油和天然气行业来说,航运公司对于向世界各地的客户运送货物至关重要。这些市场趋势可能导致危险品物流市场的扩大。适用的法律法规要求危险货物必须包装。在运输危险物品时,在货物装运船隻上使用标籤和其他识别标记也很重要。这大大提高了运输安全性。

危险品物流业概况

危险品物流市场较为分散,既有全球参与者,也有本地参与者。领先的公司包括 DHL、DSV、Ceva Logistics、Bollore Logistics 和 DGD Transport。协议、联盟、合资和伙伴关係是这些参与者为保持竞争优势和满足不断增长的客户需求而实施的众多策略之一。

我们也致力于研发,以加强我们的产品组合併扩大市场占有率。本地企业的技术、产品范围、提供的服务、库存管理等方面的能力都有所提升。随着危险品物流监管力道的不断加强,不少能够独立提供全链条危险品物流服务的货代公司应运而生。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态与洞察

- 当前市场状况

- 产业价值链分析

- 政府法规和倡议

- 危险货物类别概述

- 审查并说明货物运输法规和标准(《危险品运输法》(HMTA)、国际航空运输协会危险物品规则(IATA DGR)等)

- 关注供应链中的关键相关人员(货运代理、地面代理、运输公司、顾问、顾问等)

- 关键资讯 - 文件、特别许可证、安全检查表

- 焦点 - 危险货物运输相关设备及配件(空运、海运及陆运)

- 运输危险货物的潜在风险

- 包装洞察

- 技术简介(数位化和流程优化和管理软体、电子危险品申报(eDGD)等)

- COVID-19 对市场的影响

- 市场动态

- 市场驱动因素

- 国际贸易扩张导致危险货物运输需求增加

- 环保意识的增强推动了人们对环保和永续物流的关注

- 市场限制/挑战

- 确保遵守这些法规是物流公司面临的持续挑战

- 维护货物和设施的安全是一项重大挑战,需要监视、门禁控制和其他安全措施。

- 市场机会

- 有关危险货物运输的严格规定对专门确保合规的公司产生了很高的需求。

- 市场驱动因素

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 购买者/消费者的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争强度

第五章 市场区隔

- 按服务

- 运输

- 仓储和配送

- 附加价值服务

- 目的地

- 国内的

- 国际的

- 按地区

- 亚太地区

- 北美洲

- 欧洲

- 拉丁美洲

- 中东和非洲

第六章 竞争格局

- 公司简介

- Deutsche Post DHL Group

- DSV

- Ceva Logistics

- Bollore Logistics

- DGD Transport

- Toll Group

- YRC Worldwide Inc.

- DB Schenker

- Hellmann Worldwide Logistics

- Agility Logistics

- Kuehne+Nagel

- XPO Logistics

- GEODIS

- Rhenus Logistics*

- 其他公司

第七章:市场的未来

第 8 章 附录

- 主要国家按活动分類的 GDP 分布

- 资本流动洞察 – 主要国家

- 全球危险货物流动统计

- 外贸统计 - 出口和进口,按产品、目的地/原产国划分

The Hazardous Goods Logistics Market size is estimated at USD 274.80 billion in 2025, and is expected to reach USD 369.13 billion by 2030, at a CAGR of 6.08% during the forecast period (2025-2030).

When shipping large quantities of hazardous materials, government agencies require accurate labeling of each product to comply with federal regulations. In 2003, the UN adopted a global system for identifying hazardous materials that may pose physical, health, and environmental risks. Dangerous materials are classified into nine hazard categories: flammable, corrosive, and gaseous. The UN number is a required four-digit number ranging from 0004 to 3548 that identifies specific dangerous goods and hazardous materials for international transportation.

Risky materials comprise the bulk of international cargo, containing many commonly used products and items. Much of this cargo reportedly consists of gasoline and other petroleum products. The current oil boom may result from unprecedented growth over the past few years due to hydraulic fracturing and a government fostering a more conducive environment for fuel production. The United States produces the bulk of the world's oil.

The requirement to ship dangerous goods is anticipated to increase yearly, in addition to the numerous hazardous goods rules being updated annually. The need for UN packaging, training, labels, and placards will rise due to the growing requirement to move lithium batteries and the region's well-established gas and oil businesses, driving the dangerous goods market to record highs.

Additionally, all forms of transportation must be used to convey radioactive medication, virus samples, healthcare hazardous chemicals, and clinical waste such as surgical equipment. For example, the oil and gas industry may impact this expected expansion of dangerous goods around the globe. The oil and gas industry, which is still lucrative, is anticipated to receive investments totaling USD 237 billion over the next 10 years, or 25% of the estimated worldwide investment in this industry.

Hazardous Goods Logistics Market Trends

Increase in Shipment of Flammable Liquids Driving the Market

The medical, nuclear power, oil and gas, and petrochemical industries are examples of the widespread use of hazardous materials in developing or developed economies. Transport companies transporting dangerous goods must follow standard procedures for the safety of their vehicles and vessels. Other federal agencies' regulations on dangerous products, workplace safety, and environmental protection also apply.

Over the next few years, the hazardous product logistics market will benefit significantly from increasingly strict government regulations. The US Department of Transportation's (DOT) Pipeline and Hazardous Materials Safety Administration (PHMSA) is responsible for developing and implementing national regulations for the safe transport of dangerous goods. When transporting dangerous goods to, from, or within the United States, it is critical to comply with the Hazardous Materials Regulations (HMR 49, Part 100-185).

The UN Model Regulations for the carriage of dangerous goods serve as a reference for the development of standardized regulations for all modes of transport. There is a new edition every two years. In order to facilitate trade and facilitate the safe and efficient transportation of dangerous products, labels or marks specifically designed for the carriage of dangerous commodities on cargo vessels must be applied to the dangerous goods. More importantly, they help make transportation safer.

Asia-Pacific Dominates the Market

The Capacity Building Course on Promoting Safety for Dangerous Goods Transportation in the APEC Region, including the workshop, was held online in Phuket from December 1 to 2, 2022. The course was attended by a total of 53 participants from 11 APEC member economies, namely China, Japan, the Republic of Korea, Malaysia; Peru, the Philippines, Singapore, Chinese Taipei, Thailand, the United States; and Vietnam and three Non-APEC economies, namely Cambodia, Sri Lanka, and France, as well as representatives of relevant international organization, regional agencies, port authorities, universities, research institutes, professional associations, and private sectors.

In the fiscal year 2022, the total number of dangerous goods containers in Bangkok Port was 38,545 TEUs. The highest number of hazardous goods containers was in Class 9 (14,034 TEUs), followed by Class 3 (9,489 TEUs). At the same time, the lowest number of dangerous goods containers was in Class 6.1 (3,083 TEUs). Similarly, the total number of hazardous goods containers in Laem Chabang Port was 174,938 TEUs. The highest number of dangerous goods containers was in Class 9 (59,734 TEUs), followed by Class 3 (42,606 TEUs).

Large-scale petrochemical development has decreased the gasoline demand. As a result, more dangerous goods, such as oil and gas, are being transported across the country using trucking services.

The United States is projected to become the largest oil producer in the world within the next five years, overtaking both Saudi Arabia and Russia. Shipping companies are essential for the oil and gas industry to get their goods to customers worldwide. These market trends should lead to the expansion of the hazardous goods logistics market. Applicable laws and regulations should package dangerous materials. It is also important to use labels or other identifying indicators on cargo carriers when transporting hazardous materials. This would significantly enhance transit security.

Hazardous Goods Logistics Industry Overview

The hazardous goods logistics market is fragmented, with a mixture of global and local players. Some of the strong players include DHL, DSV, Ceva Logistics, Bollore Logistics, and DGD Transport. Contracts, collaborations, joint ventures, and partnerships are among many other strategies these players have implemented to stay ahead of the competition and meet the expanding needs of their clients.

Also, they engage in research and development operations to strengthen their portfolios and gain market share. The capabilities of local players in terms of technology, items handled, service offered, and inventory management are all improving. With the tightening of hazardous goods logistics regulations, many freight forwarding businesses that can independently provide dangerous competent goods logistics full-chain services have emerged.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS AND DYNAMICS

- 4.1 Current Market Scenario

- 4.2 Industry Value Chain Analysis

- 4.3 Government Regulations and Initiatives

- 4.4 Brief on Dangerous Goods Classes

- 4.5 Review and Commentary on Goods Transport Regulations and Standards (Hazardous Materials Transportation Act (HMTA), International Air Transport Association Dangerous Goods Regulations (IATA DGR), etc.)

- 4.6 Focus on Key Stakeholders in Supply Chain (Freight Forwarders, Ground Handling Agents, Carriers, Advisors and Consultants, etc.)

- 4.7 Key Information - Documentation, Special Permissions, and Safety Checklists

- 4.8 Spotlight - Equipment and Accessories Associated with Transport of Dangerous Goods (Air, Sea, and Road)

- 4.9 Potential Risk Involved in Shipment of Hazardous Materials

- 4.10 Insights on Packaging

- 4.11 Technology Snapshot (Digitalization and Process Optimization and Management Software, e-Dangerous Goods Declaration (eDGD), etc.)

- 4.12 Impact of COVID-19 on the Market

- 4.13 Market Dynamics

- 4.13.1 Market Drivers

- 4.13.1.1 The growth of international trade has led to an increased demand for the transportation of hazardous materials

- 4.13.1.2 Growing environmental awareness has led to an increased focus on eco-friendly and sustainable logistics practices.

- 4.13.2 Market Restraints/Challenges

- 4.13.2.1 Ensuring compliance with these regulations is a constant challenge for logistics companies.

- 4.13.2.2 Maintaining the security of shipments and facilities is a significant challenge, requiring surveillance, access controls, and other security measures.

- 4.13.3 Market Opportunities

- 4.13.3.1 With strict regulations governing the transportation of hazardous materials, there is a growing demand for companies that specialize in ensuring compliance.

- 4.13.1 Market Drivers

- 4.14 Industry Attractiveness - Porter's Five Forces Analysis

- 4.14.1 Bargaining Power of Suppliers

- 4.14.2 Bargaining Power of Buyers/Consumers

- 4.14.3 Threat of New Entrants

- 4.14.4 Threat of Substitute Products

- 4.14.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Service

- 5.1.1 Transportation

- 5.1.2 Warehousing and Distribution

- 5.1.3 Value-added Services

- 5.2 By Destination

- 5.2.1 Domestic

- 5.2.2 International

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.2 North America

- 5.3.3 Europe

- 5.3.4 Latin America

- 5.3.5 Middle East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Overview (Market Concentration and Major Players)

- 6.2 Company Profiles

- 6.2.1 Deutsche Post DHL Group

- 6.2.2 DSV

- 6.2.3 Ceva Logistics

- 6.2.4 Bollore Logistics

- 6.2.5 DGD Transport

- 6.2.6 Toll Group

- 6.2.7 YRC Worldwide Inc.

- 6.2.8 DB Schenker

- 6.2.9 Hellmann Worldwide Logistics

- 6.2.10 Agility Logistics

- 6.2.11 Kuehne + Nagel

- 6.2.12 XPO Logistics

- 6.2.13 GEODIS

- 6.2.14 Rhenus Logistics*

- 6.3 Other Companies

7 FUTURE OF THE MARKET

8 APPENDIX

- 8.1 GDP Distribution, by Activity - Key Countries

- 8.2 Insights on Capital Flows - Key Countries

- 8.3 Global Dangerous Goods Flow Statistics

- 8.4 External Trade Statistics - Exports and Imports, by Product and by Country of Destination/Origin