|

市场调查报告书

商品编码

1644396

中东和非洲商用航空燃料:市场占有率分析、行业趋势、统计数据和成长预测(2025-2030 年)Middle East And Africa Commercial Aircraft Aviation Fuel - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

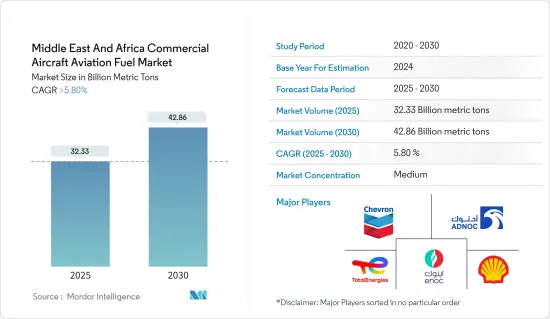

中东和非洲民航机航空燃料市场规模预计在 2025 年为 323.3 亿吨,预计到 2030 年将达到 428.6 亿吨,预测期内(2025-2030 年)的复合年增长率将超过 5.8%。

关键亮点

- 从中期来看,航空公司持有规模预计的增加加上该地区的经济发展将在预测期内推动市场发展。

- 然而,预测期内全球原油价格的波动预计将阻碍市场成长。

- 生质燃料等永续航空燃料的采用预计将为中东和非洲的民航机航空燃料市场创造重大机会。

- 由于沙乌地阿拉伯新兴市场的发展和游客数量的不断增加,预计该国将成为该市场的主导地区。

中东和非洲民航机航空燃料市场趋势

航空生质燃料显着成长

- 在中东和非洲,人们认识到必须将航空营运与全球永续性目标结合,并与航空生质燃料减轻航空旅行对环境影响的潜力完美结合。与传统航空燃料相比,生质燃料能够减少温室气体排放,这与该地区日益增强的环保努力相呼应。

- 此外,中东地区丰富的生物质资源使其具有战略优势。在中东,有潜力利用当地可用的原料(如农业废弃物和藻类)来生产生生质燃料,这符合建立永续供应链和减少对石化燃料依赖的努力。当地资源和航空燃料生产之间的内在匹配促进了航空生质燃料作为在地采购可再生能源解决方案的可行性。

- 例如,根据能源研究所《2023年世界能源统计评论》,该地区的生质燃料消费量在2012年至2022年的年均增长率为11.3%,而到2021年至2022年,这一数字将增长9.3%。这意味着该地区生质燃料消耗量的增加,可以推断出航空业生质燃料使用量的增加。

- 此外,全球伙伴关係和研究计画也正在推动航空生质燃料的发展。航空公司、政府和生质燃料生产商之间的合作将增强生质燃料的应用势头,并鼓励研究、创新和扩大生产。永续航空燃料标准和认证的建立进一步增强了人们对生质燃料作为主流航空燃料的可行性的信心。

- 例如,2022 年 11 月,全球航空公司阿提哈德航空宣布与 Cepsa 建立合作伙伴关係。两家公司正在加快航空生质燃料的研究力道。两家公司计划在 2030年终生产 80 万吨航空生质燃料,以实现永续性目标。

- 因此,如上所述,预计预测期内航空生质燃料的需求将会增加。

沙乌地阿拉伯主导市场

- 沙乌地阿拉伯作为国际中转站的中心地位及其不断发展的世界级机场网络使其成为航空生态系统中越来越重要的组成部分。这项战略优势增强了沙乌地阿拉伯作为向国内外航空公司分销航空燃料的关键枢纽的地位。

- 其中最主要的因素是沙乌地阿拉伯的战略地理位置及其作为全球航空枢纽的地位。沙乌地阿拉伯作为国际航班中转站的中心地位及其不断扩大的世界级机场网络使其在航空生态系统中的重要性日益提高。这个战略位置使沙乌地阿拉伯成为国内外航空公司航空燃料分销的重要枢纽。

- 根据土耳其统计总局 (GASTAT) 的数据,2022 年的乘客人数约为 8,800 万人次,比 2021 年增加 82%。 2022年,国际机场平均每天起降国际国内航班131.29个,国内机场平均每天起降国内航班5.94个。

- 此外,沙乌地阿拉伯能源生质燃料。该国广阔的土地资源和对可再生能源的持续投资为生质燃料原料的生产提供了有利的环境。沙乌地阿拉伯在永续航空燃料生产方面表现出良好的前景,并有可能成为该地区生质燃料供应的中心。

- 此外,沙乌地阿拉伯政府致力于「2030愿景」等变革性经济倡议,旨在提高该国的全球地位并建立知识密集型经济。尖端航空领域解决方案的整合符合「2030愿景」的创新目标。

- 例如,沙乌地阿拉伯根据其「2030愿景」决定利用政府资金扩大其体育基础设施,尤其是足球。沙乌地阿拉伯联赛吸引了大多数国际足球明星来该国踢球。预计富裕程度的提高最终将促进该国的航空旅行,从而进一步推动该地区对航空燃料的需求。

- 因此,如上所述,预计沙乌地阿拉伯将在预测期内占据市场主导地位。

中东和非洲民航机航空燃料产业概况

中东和非洲民航机航空燃料市场中等细分。主要企业(不分先后顺序)包括阿联酋国家石油公司、雪佛龙公司、壳牌公司、道达尔能源公司和阿布达比国家石油公司。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究范围

- 市场定义

- 调查前提

第二章调查方法

第三章执行摘要

第四章 市场概况

- 介绍

- 至2029年的市场规模及需求预测(单位:吨)

- 最新趋势和发展

- 政府法规和政策

- 市场动态

- 驱动程式

- 飞机扩张

- 经济发展

- 限制因素

- 原油价格波动

- 驱动程式

- 供应链分析

- 波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争强度

第五章 市场区隔

- 燃料类型

- 空气涡轮燃料 (ATF)

- 航空生质燃料

- 阿布古斯

- 2028 年市场规模与需求预测(按地区)

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 卡达

- 埃及

- 南非

- 其他中东和非洲地区

第六章 竞争格局

- 併购、合资、合作与协议

- 主要企业策略

- 公司简介

- Emirates National Oil Company

- Repsol SA

- BP PLC

- Shell PLC

- TotalEnergies SE

- Chevron Corporation

- Exxon Mobil Corporation

- Abu Dhabi National Oil Company

- Market Ranking

第七章 市场机会与未来趋势

- 永续航空燃料

简介目录

Product Code: 71525

The Middle East And Africa Commercial Aircraft Aviation Fuel Market size is estimated at 32.33 billion metric tons in 2025, and is expected to reach 42.86 billion metric tons by 2030, at a CAGR of greater than 5.8% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, the increasing airline fleets coupled with economic development in the region are expected to drive the market during the forecasted period.

- On the other hand, global oil price volatility is expected to hinder the market's growth during the forecasted period.

- Nevertheless, the introduction of sustainable aviation fuels like biofuels is expected to create huge opportunities for the Middle-East and African commercial aircraft aviation fuel markets.

- Saudi Arabia is expected to be a dominant region for the market due to the country's increasing economic development and increasing tourism.

MEA Commercial Aircraft Aviation Fuel Market Trends

Aviation Biofuel to Witness Significant Growth

- Middle-East and Africa's recognition of the imperative to align aviation operations with global sustainability goals converge seamlessly with the potential of aviation biofuel to mitigate the environmental impact of air travel. The inherent capacity of biofuels to reduce greenhouse gas emissions as compared to conventional aviation fuels resonates resoundingly with the region's growing commitment to environmental stewardship.

- Moreover, the region's abundant biomass resources offer a strategic advantage. The Middle East's potential to leverage locally available feedstock for biofuel production, such as agriculture waste and algae, aligns with efforts to establish sustainable supply chains and reduce dependence on fossil fuels. This intrinsic alignment between regional resources and aviation fuel production promotes the viability of biofuels for aviation purposes as a locally sourced and renewable energy solution.

- For instance, according to the Energy Institute Statistical Review Of World Energy 2023, biofuel consumption in the region increased by 9.3% between 2021 and 2022, while an annual average growth rate of 11.3% was recorded between 2012 and 2022. This signifies an increase in the consumption of biofuels in the region, which can be extrapolated to the increasing use of biofuels in the aviation industry.

- Furthermore, global partnerships and research initiatives propel aviation biofuel's prominence. Collaborations between airlines, governments, and biofuel producers amplify the momentum towards biofuel adoption, promoting research, technological innovation, and production scale-up. Establishing sustainable aviation fuel standards and certification further bolsters confidence in biofuels' viability as a mainstream aviation fuel.

- For instance, in November 2022, Etihad, a significant global airline company, announced a partnership with Cepsa. Both companies will accelerate the research activities for aviation biofuels. The companies aim to produce 800,000 tons of aviation biofuels by the end of 2030 to meet their sustainability goals.

- Therefore, as discussed above, the demand for aviation biofuels is expected to increase during the forecasted period.

Saudi Arabia to Dominate the Market

- The nation's central positioning as a transit point for international flights and its expanding network of world-class airports bolster its significance in the aviation ecosystem. This strategic vantage point elevates Saudi Arabia's role as a crucial hub for aviation fuel distribution catering to domestic and International Airlines.

- Foremost among these factors is Saudi Arabia's strategic geographical location and role as a global aviation hub. The nation's central positioning as a transit point for international flights and its expanding network of world-class airports bolster its significance in the aviation ecosystem. This strategic vantage point elevates Saudi Arabia's role as a critical hub for aviation fuel distribution catering to domestic and International Airlines.

- According to the General Authority for Statistics (GASTAT), the number of passengers in 2022 was almost 88 million, an increase of 82% over 2021. The average daily flights arriving and departing at international airports for international and domestic flights in 2022 was 131.29, and the average daily flights arriving and departing at domestic airports was 5.94.

- Moreover, Saudi Arabia's visionary commitment to diversifying its energy landscape aligns seamlessly with the potential of aviation biofuel. The nation's vast land resources and ongoing investments in renewable energy offer a conducive environment for biofuel feedstock production. This alignment proposes the viability of sustainable aviation fuel production, positioning Saudi Arabia as a potential epicenter for biofuel supply in the region.

- Furthermore, the Saudi Arabian government's dedication to transformative economic initiatives such as Vision 2030 amplifies the nation's prominence as it strives to enhance its global standing and establish our knowledge-based economy. The integration of cutting-edge aviation field solutions aligns with the innovative-driven aspirations of Vision 2030.

- For instance, under Vision 2030, the country has decided to expand its sports infrastructure, especially football, with the backing of government money resources. The Saudi Arabian league has attracted most international football icons to play in their country. The increase in high-net-worth individuals is consequently expected to drive airplane traffic in the country, which is further expected to drive the demand for aviation fuel in the region.

- Therefore, as mentioned above, Saudi Arabia is expected to dominate the market during the forecasted period.

MEA Commercial Aircraft Aviation Fuel Industry Overview

The Middle-East and African commercial aircraft aviation fuel market is moderately fragmented. Some of the major companies (in no particular order) include Emirates National Oil Company, Chevron Corporation, Shell PLC, TotalEnergies SE, and Abu Dhabi National Oil Company.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of Study

- 1.2 Market Definiton

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in metric ton, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Expanding Airline Fleet

- 4.5.1.2 Economic Development

- 4.5.2 Restraints

- 4.5.2.1 Volatility in Oil Price

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Fuel Type

- 5.1.1 Air Turbine Fuel (ATF)

- 5.1.2 Aviation Biofuel

- 5.1.3 AVGAS

- 5.2 Geography (Regional Market Analysis {Market Size and Demand Forecast till 2028 (for regions only)})

- 5.2.1 The United Arab Emirates

- 5.2.2 Saudi Arabia

- 5.2.3 Qatar

- 5.2.4 Egypt

- 5.2.5 South Africa

- 5.2.6 Rest of the Middle-East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Emirates National Oil Company

- 6.3.2 Repsol SA

- 6.3.3 BP PLC

- 6.3.4 Shell PLC

- 6.3.5 TotalEnergies SE

- 6.3.6 Chevron Corporation

- 6.3.7 Exxon Mobil Corporation

- 6.3.8 Abu Dhabi National Oil Company

- 6.4 Market Ranking

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Sustainable Aviation Fuel