|

市场调查报告书

商品编码

1644897

美国网路安全:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)US Cybersecurity - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

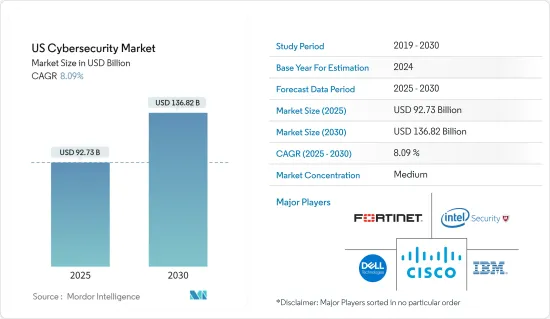

预计 2025 年美国网路安全市场规模为 927.3 亿美元,到 2030 年将达到 1,368.2 亿美元,预测期内(2025-2030 年)的复合年增长率为 8.09%。

防止持续的资讯安全漏洞的挑战是目前美国各行各业的公司面临的问题。为了应对新出现的威胁并保护敏感资料,安全专业人员需要走在危险的前面并运用技术、政策和流程。此外,为了加速数位转型进程,企业需要能够在本地、SDN 和云端环境中快速且安全地更改其核心业务应用程式。这意味着为了管理这些操作,IT 和安全团队需要充分了解对整个网路架构的精细控制。

主要亮点

- 这个市场的扩大是由于网路攻击的日益复杂化。在过去十多年中,网路犯罪和诈骗的数量和严重性不断升级,对企业造成了巨大的损失。随着网路犯罪的急剧升级,企业一直将支出集中在资讯安全解决方案上,以加强其内部安全基础设施。最近,针对性攻击的使用有所增加,这种攻击允许攻击者保持匿名并渗透到受害者的网路基础设施。端点、网路、内部设备、云端基础的应用程式、资料以及更多IT基础设施经常成为攻击者的目标。

- 例如,2021年3月,骇客针对Microsoft Exchange Server电子邮件软体中的四个安全漏洞进行了攻击。他们利用 Exchange 伺服器的一个漏洞,获取了美国至少 30,000 个组织的电子邮件帐户的存取权限,其中包括小型企业、城市、乡镇和地方政府。这次攻击使骇客能够远端控制受影响的系统,从而可能导致资料窃取和进一步入侵。

- 公开呼吁该地区的政府机构与私人公司和学术机构合作,确保医疗设施免受网路威胁。业界正在进行大量合作。例如,2022年3月,美国参议员提出了《医疗保健网路安全法案》。该立法旨在加强网路安全和基础设施安全局 (CISA) 与卫生与公众服务部之间的合作,以加强整个医疗保健和公共卫生部门的网路安全工作。

- 2022 年 1 月,美国联邦银行监管机构宣布了网路安全规则,要求及时通知资料外洩事件。拟议的规则将对重大电脑安全事件提供预警。该规则要求银行公司在确定事件发生后儘快(但不得晚于 36 小时)通知他们。这些规定可以控制美国银行业的网路攻击。

- 据美国国防安全保障部网路安全部门称,使用 COVID-19 主题诱饵、包含冠状病毒或 COVID-19 相关词语的新网域註册以及针对最近快速部署的远端存取和远程办公基础设施的攻击的网路钓鱼和恶意软体传播激增。疫情进一步加速了网路安全的需求,因为公司专注于加强网路安全,并准备数月实施业务永续营运计划(BCP),包括在隔离条件下工作时的资讯安全监控和回应。

美国网路安全市场的趋势

身分和存取管理需求是市场驱动因素之一

- 随着全国数位化的快速发展,数位身分证已成为实施存取控制的关键。因此,身分识别和存取管理 (IAM) 已成为现代企业的首要任务。

- 美国是世界上数字渗透率最高的国家之一,许多用户和组织都依赖物联网设备和运算解决方案。美国各地的组织越来越依赖电脑网路、智慧型装置和电子资料来进行日常业务,导致线上传输和储存的个人和财务资讯量增加。因此,对身分和存取管理解决方案的需求随着时间的推移而增加。

- IAM 曾被视为营运后勤部门问题,但由于组织未能有效管理和控制用户存取而发生了几起重大资料外洩事件,如今已引起了董事会层面的关注。不断变化的监管环境以及自带设备 (BYOD) 和云端采用等趋势进一步增强了 IAM 的重要性。此外,获取资讯和资料的风险也大大增加。

- 据美国联邦贸易委员会称,美国银行和付款行业的身份窃盗有所增加,这可能会推动生物识别解决方案的使用。根据 Pymnts 于 2022 年 3 月发布的《数位身分追踪报告》,在美国营运的道明银行 (TD Bank) 等金融机构正专注于数位身分检验解决方案,以增强其客户入职流程,这对 CIP 和 KYC 程序的检验做出了重大贡献。随着全国各地的金融机构考虑实施各种身分验证工具,软体解决方案预计将变得更加普及。

- 身分管理的网路安全漏洞——无论是由有组织犯罪还是国家支持的军队所为——除了造成重大的经济损失、潜在的生命损失以及对 IT 网路和企业声誉的进一步损害之外,还会影响员工的工作效率和士气。这些风险需要新等级的识别及存取管理解决方案。

BFSI 部门推动网路安全市场成长

- BFSI 产业是面临大量资料外洩和网路攻击的关键基础设施领域之一。由于这是一种利润丰厚的经营模式,具有惊人的回报,以及相对较低的风险和可检测性,网路犯罪分子优化了一系列邪恶的网路攻击,以破坏金融部门。这些攻击的威胁包括木马、恶意软体、ATM 恶意软体、勒索软体、行动银行恶意软体、资料外洩、组织入侵、资料窃取和财务外洩。

- 保护 IT 流程和系统、保护敏感客户资料、遵守政府法规等策略促使公共和私人银行机构专注于采用最新技术来防止网路攻击。此外,客户期望的不断提高、技术力的提高和监管要求的不断提高迫使银行机构采取积极主动的安全措施。随着网路银行和手机银行等科技和数位管道的兴起,网路银行已成为客户首选的银行服务。银行可能需要利用先进的身份验证和存取控制流程。

- 2022 年,针对手动工作较少、自动化程度较高的组织的勒索软体和网路钓鱼攻击也有所增加。 2022 年,全球各地的金融机构都受到了创新型新型勒索软体技术的影响,这些技术可最大限度地提高威胁行为者的投资报酬率。虽然金融机构只占勒索软体攻击直接针对的受害者的一小部分,但它们可能并且会受到针对第三方的攻击的影响,而第三方是它们的主要目标。此类威胁将会增加 BFSI 领域对网路安全解决方案的使用。

- 此外,鑑于俄罗斯和乌克兰之间的衝突以及针对该国的几乎持续不断的威胁宣传活动和漏洞披露,美国政府于 2022 年 4 月成立了一个新机构——网路空间和数位政策办公室 (CDP),负责制定线上防御和隐私保护的政策和方向,寻求将网路安全融入美国的外交关係中。

美国网路安全产业概况

美国网路安全市场适度整合,拥有大量中小型供应商,在市场上占据主导地位。公司不断投资于策略联盟和产品开发以扩大市场占有率。最近的一些市场发展趋势包括:

- 2022 年 5 月-Google计画收购美国网路安全公司 Mandiant。收购后,该公司很可能成为Google云端处理部门的一部分。收购 Mandiant 的倡议源于Google计划加强其网路安全影响力并建立比市场上的竞争对手更强大的产品组合。

- 2022 年 5 月:思科系统公司宣布公开发布思科云端控制框架 (CCF)。思科 CCF 是一个综合框架,整合了国家和国际安全合规性和认证要求。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概况

- 价值链分析

- 波特五力分析

- 新进入者的威胁

- 买家的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

- COVID-19 对市场的影响

第五章 市场动态

- 市场驱动因素

- 数位化和对可扩展IT基础设施日益增长的需求

- 需要因应各种趋势带来的风险,包括第三方供应商风险、MSSP 的发展以及云端优先策略的采用

- 市场限制

- 网路安全专家短缺

- 高度依赖传统身分验证方法且缺乏准备

- 趋势分析

- 泰国越来越多组织使用人工智慧来加强其网路安全战略

- 向云端基础的交付模式的转变将使云端安全呈指数级增长。

第六章 市场细分

- 按服务

- 安全类型

- 云端安全

- 资料安全

- 身分存取管理

- 网路安全

- 消费者安全

- 基础设施保护

- 其他类型

- 按服务

- 安全类型

- 按部署

- 云

- 本地

- 按最终用户

- BFSI

- 卫生保健

- 製造业

- 政府和国防

- 资讯科技/通讯

- 其他最终用户

第七章 竞争格局

- 公司简介

- IBM Corporation

- Cisco Systems Inc

- Dell Technologies Inc.

- Fortinet Inc.

- Intel Security(Intel Corporation)

- F5 Networks, Inc.

- AVG Technologies

- IDECSI Enterprise Security

- FireEye Inc.

- Cyberark Software Ltd

第八章投资分析

第九章:市场的未来

The US Cybersecurity Market size is estimated at USD 92.73 billion in 2025, and is expected to reach USD 136.82 billion by 2030, at a CAGR of 8.09% during the forecast period (2025-2030).

The difficulty of protecting against a persistent information security breach is one that businesses in all industries in the United States are currently confronting. To fight against incoming threats and safeguard sensitive data, security experts are expected to keep ahead of dangers and use technologies, policies, and processes. Additionally, enterprises need to be able to swiftly and securely modify their core business applications across on-premise, SDN, and cloud environments as they speed up their digital transformation activities. This means that to manage these operations, IT and security teams need to have a complete awareness of fine-grained control over their whole network architecture.

Key Highlights

- The market's expansion might be ascribed to the sophistication of cyberattacks, which is rising. Over the past ten years, the number and severity of cybercrimes and scams have escalated, causing enormous losses for enterprises. As cybercrimes have dramatically escalated, businesses have focused their expenditure on information security solutions to bolster their internal security infrastructures. The use of targeted assaults, which penetrate targets' network infrastructure while remaining anonymous, has increased recently. Endpoints, networks, on-premises devices, cloud-based apps, data, and numerous other IT infrastructures are frequently targeted by attackers who have a specific target.

- For instance, in March 2021, Hackers targeted four security flaws in Microsoft Exchange Server email software; they used the bugs on the Exchange servers to access email accounts of at least 30,000 organizations across the United States, which included small businesses, towns, cities, and local governments. The attack allowed the hackers to remotely control the affected systems, allowing them access to potential data theft and further compromise.

- Following a public call asking government agencies in the region to join forces with the private sector and academia to ensure that medical facilities are protected from cyber threats. Various collaborations have been taking place in the industry. For instance, in March 2022, Senators of the United States Parliament introduced Healthcare Cybersecurity Act. The Act aims to promote collaboration between Cybersecurity and Infrastructure Security Agency (CISA) and HHS to enhance cybersecurity efforts across the healthcare and public health sector.

- In January 2022, the federal banking regulators of the United States issued a cybersecurity rule requiring prompt notification of a breach. The proposed rule is poised to provide the agencies with an early warning of considerable computer security incidents. It would need notification as soon as possible and no later than 36 hours after a banking enterprise determines that an incident has occurred. Such regulations could control the cyber attacks in the banking sector of the United States.

- According to the US Department of Homeland Security (DHS) Cybersecurity, there has been a sharp increase in phishing and malware distribution using COVID-19-themed lures, the registration of new domain names containing words related to coronavirus or COVID-19, and attacks against recently and swiftly deployed remote access and teleworking infrastructure. As businesses prepare to implement months-long business continuity plans (BCP), including information security monitoring and response while working under quarantine circumstances, focusing on increasing cybersecurity, the pandemic has further expedited the need for cybersecurity.

US Cybersecurity Market Trends

Need For Identity Access Management is One of the Factor Driving the Market

- With the rapid digitalization across the country, digital identity has become crucial to enforcing access controls. As a result, identity and access management (IAM) has become a significant priority for modern enterprises.

- The United States has one of the highest digital penetration rates globally, with many users and organizations depending upon IoT devices and computing solutions. Organizations all over the US increasingly depend on computer networks, smart devices, and electronic data to conduct their daily operations, which has led to growing pools of personal and financial information transferred and stored online. Hence, the need for identity and access management solutions increased over time.

- IAM, viewed as an operational back-office issue, is now gaining board-level visibility following several high-level breaches that have occurred due to the failure of organizations to manage and control user access effectively. The prominence of IAM has been further elevated by an evolving regulatory landscape and trends, such as Bring your Device (BYOD) and cloud adoption. The risks related to accessing information and data have also increased significantly.

- According to the Federal Trade Commission, the prevalence of identity thefts in the banking and payment industries in the United States would encourage more people to use biometric solutions. Financial institutions like TD Bank that operate in the United States are reportedly focusing on digital identity verification solutions to strengthen the customer onboarding processes, with a significant contribution to verifying the CIP and KYC procedures, according to Pymnts' release of the Digital Identity Tracker Report in March 2022. The software solutions are expected to gain more traction as financial institutions nationwide examine implementing various identity verification tools.

- The impact of an identity management cybersecurity breach by organized crime, state-sponsored militaries, and others is packed with implications that can impact staff productivity and morale, apart from substantial financial and potential life losses and further damage to the IT network and company reputation. These risks demand a new level of identity and access management solutions.

BFSI Segment Is Boosting The Cybersecurity Market Growth

- The BFSI industry is one of the critical infrastructure segments that face multiple data breaches and cyber-attacks, owing to the massive customer base that the sector serves and the financial information that is at stake. Being a highly lucrative operation model with phenomenal returns and the added upside of relatively low risk and detectability, cybercriminals are optimizing a plethora of diabolical cyberattacks to immobilize the financial sector. These attacks' threat landscape ranges from Trojans, malware, ATM malware, ransomware, mobile banking malware, data breaches, institutional invasion, data thefts, fiscal breaches, etc.

- With a strategy to secure their IT processes and systems, secure customer critical data, and comply with government regulations, public and private banking institutes focus on implementing the latest technology to prevent cyber attacks. Besides, with greater customer expectations, rising technological capabilities, and regulatory requirements, banking institutions are pushed to adopt a proactive security approach. With the growing technological penetration and digital channels, such as Internet banking, mobile banking, etc., online banking has become customers' preferred choice for banking services. There is a significant need for banks to leverage advanced authentication and access control processes.

- The country also marked the increase of ransomware and phishing attacks targeted at organizations that involved less manual effort and were highly automated in 2022. In 2022, financial firms worldwide were impacted by innovative new ransomware tactics that maximized ROI for the threat actors. While financial firms represent a small percentage of victims directly targeted by ransomware attacks, they can and have been impacted by attacks on third parties, who are prime targets. Such threats are poised to increase the usage of cybersecurity solutions in the BFSI sector.

- Moreover, in light of Russia - Ukraine conflict and a virtually endless cycle of threat campaigns and vulnerability disclosures towards the country, the US State Department, on April 2022, launched a new agency, the Bureau of Cyberspace and Digital Policy (CDP), responsible for developing online defense and privacy-protection policies and direction as the Biden administration seeks to integrate cybersecurity into America's foreign relations.

US Cybersecurity Industry Overview

The united states cybersecurity market is moderately consolidated, with the presence of a large number of SME vendors and dominant major companies in the market. The companies are continuously investing in making strategic partnerships and product developments to gain more market share. Some of the recent developments in the market are:

- May 2022 - Google plans to acquire Mandiant, a United States-based cybersecurity firm. Post-acquisition the company will most likely join Google's cloud computing division. The move to acquire Mandiant stems from Google's plan to strengthen its cybersecurity footprint and create a robust portfolio compared to its competitors in the market.

- May 2022: Cisco Systems Inc. announced that, it has released the Cisco Cloud Controls Framework (CCF) to the public. Cisco CCF is a comprehensive set of national and international security compliance and certification requirements, aggregated in one framework.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Value Chain Analysis

- 4.3 Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitutes

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Impact of Covid-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Demand for Digitalization and Scalable IT Infrastructure

- 5.1.2 Need to tackle risks from various trends such as third-party vendor risks, the evolution of MSSPs, and adoption of cloud-first strategy

- 5.2 Market Restraints

- 5.2.1 Lack of Cybersecurity Professionals

- 5.2.2 High Reliance on Traditional Authentication Methods and Low Preparedness

- 5.3 Trends Analysis

- 5.3.1 Organizations in Thailand increasingly leveraging AI to enhance their cyber security strategy

- 5.3.2 Exponential growth to be witnessed in cloud security owing to shift toward cloud-based delivery model.

6 MARKET SEGMENTATION

- 6.1 By Offering

- 6.1.1 Security Type

- 6.1.1.1 Cloud Security

- 6.1.1.2 Data Security

- 6.1.1.3 Identity Access Management

- 6.1.1.4 Network Security

- 6.1.1.5 Consumer Security

- 6.1.1.6 Infrastructure Protection

- 6.1.1.7 Other Types

- 6.1.2 Services

- 6.1.1 Security Type

- 6.2 By Deployment

- 6.2.1 Cloud

- 6.2.2 On-premise

- 6.3 By End User

- 6.3.1 BFSI

- 6.3.2 Healthcare

- 6.3.3 Manufacturing

- 6.3.4 Government & Defense

- 6.3.5 IT and Telecommunication

- 6.3.6 Other End Users

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 IBM Corporation

- 7.1.2 Cisco Systems Inc

- 7.1.3 Dell Technologies Inc.

- 7.1.4 Fortinet Inc.

- 7.1.5 Intel Security (Intel Corporation)

- 7.1.6 F5 Networks, Inc.

- 7.1.7 AVG Technologies

- 7.1.8 IDECSI Enterprise Security

- 7.1.9 FireEye Inc.

- 7.1.10 Cyberark Software Ltd

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

2025年旅游安全全球市场报告

2025年旅游安全全球市场报告 全球网路安全市场中的人工智慧 - 2025 至 2032 年

全球网路安全市场中的人工智慧 - 2025 至 2032 年 拉丁美洲网路安全:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)泰国网路安全:市场占有率分析、行业趋势和统计数据、成长预测(2025-2030 年)网路安全-市场占有率分析、产业趋势与统计、成长预测(2024-2029)

拉丁美洲网路安全:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)泰国网路安全:市场占有率分析、行业趋势和统计数据、成长预测(2025-2030 年)网路安全-市场占有率分析、产业趋势与统计、成长预测(2024-2029) 网路安全市场规模、份额及成长分析(按产品、安全类型、部署、组织规模、垂直领域和地区)-2025 年至 2032 年产业预测

网路安全市场规模、份额及成长分析(按产品、安全类型、部署、组织规模、垂直领域和地区)-2025 年至 2032 年产业预测 企业数位通讯管治平台市场按平台类型、组织规模、功能和最终用户产业划分 - 2025-2030 年全球预测按产品类型、产品、部署类型、应用程式和最终用户产业分類的人工智慧数位双胞胎市场 - 全球预测 2025-2030网路资产攻击面管理软体市场按功能、资产类型、部署模式、组织规模和垂直划分 - 2025-2030 年全球预测资料二极体市场按产品类型、最终用户产业和分销管道划分 - 2025-2030 年全球预测

企业数位通讯管治平台市场按平台类型、组织规模、功能和最终用户产业划分 - 2025-2030 年全球预测按产品类型、产品、部署类型、应用程式和最终用户产业分類的人工智慧数位双胞胎市场 - 全球预测 2025-2030网路资产攻击面管理软体市场按功能、资产类型、部署模式、组织规模和垂直划分 - 2025-2030 年全球预测资料二极体市场按产品类型、最终用户产业和分销管道划分 - 2025-2030 年全球预测