|

市场调查报告书

商品编码

1645035

中国医药仓储:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)China Pharmaceutical Warehousing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

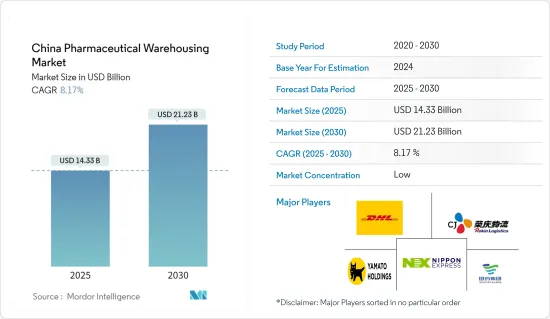

2025年中国医药仓储市场规模预估为143.3亿美元,预计2030年将达212.3亿美元,预测期间(2025-2030年)复合年增长率为8.17%。

在生物技术和创新药物发展的推动下,中国医药市场正经历重大转型。这项变革很大程度上受到中国政府战略倡议的推动,特别是旨在加强公共卫生和促进科技创新的「健康中国2030」计画。

由于大量研发投入和有利的监管环境,中国生技产业正快速成长。该市场拥有一个充满活力的生态系统,生物技术新兴企业、大型製药公司和学术机构齐心协力,不断突破医学研究的界限并开拓新的治疗方法。

中国生物技术领域的一个显着趋势是将人工智慧(AI)和巨量资料分析引入药物开发。药明康德等公司正在利用人工智慧来改善药物研发、简化临床测试并推动精准医疗策略。借助主导平台,药明康德不仅加快了有前景的候选药物的识别,还提高了研发效率。

此外,中国的监管改革,特别是创新药物的快速核准程序,为突破性治疗方法更快地进入市场铺平了道路,营造了鼓励持续创新的环境。生物相似药和生物製剂不仅提供具有成本效益的替代疗法,而且还扩大了获得尖端治疗的机会。

中国政府正在采取措施支持数位健康技术的发展。此外,透过国家医疗资讯化发展规划等倡议,我们正在努力建立统一的医疗资讯系统,无缝整合来自不同数位健康平台的资料,并增强资料互通性和护理协调性。

2023 年 6 月,FDA 正在考虑允许线上药局分发处方笺药。这一潜在的变化可能为阿里巴巴和京东等电子商务巨头进入这个快速成长的市场铺平道路。该措施的讨论自去年年中开始,一旦核准,将开放一个规模超过 1 兆元(约 1,610 亿美元)的市场。此举不仅将使销售从传统医院转向线上药局,还将挑战国有医院和经销商长期以来在市场上的主导地位。

中国医药市场的转型也正在延伸至仓储业。製药业的快速成长导致对先进仓储解决方案的需求增加,以确保药品的有效储存和分配。

中国的医药仓储市场正在透过采用自动储存和搜寻系统 (AS/RS)、温控环境和即时库存管理系统等最尖端科技来满足这些需求。

这些进步对于维持整个供应链中药品的完整性和品质至关重要。随着市场不断扩大,完善的仓储基础设施的发展将对支持中国医药产业的整体成长和效率发挥至关重要的作用。

中国医药仓储市场趋势

加大低温运输仓库建设

2024年上半年低温运输物流量达2.2亿吨,成长4.4%。同时,低温运输物流收益达到2,779亿元人民币(389亿美元),较去年同期成长3.4%。

至2024年6月,我国冷资料储存容量将扩大至2.37亿立方米,年增7.73%。今年以来,我国冷库容量新增942万立方公尺。 2024年上半年,全国冷库租赁量预计将超过2,900万立方米,年增8%以上。

生技药品、疫苗和特殊药物等温度敏感物品的生产和消费不断增加,增加了对大型冷藏仓库的需求。生技药品与传统药物不同,它是来自生物实体(包括人类和动物)的复杂物质。这些生技药品涵盖频谱广泛,从疫苗到血液成分。

生技药品经常用于先进的治疗方法,对物理环境中的微小变化都高度敏感。因此,为了满足这些产品需求的突然成长,製药和医疗保健公司必须重视快速可靠的供应链解决方案。

2024年10月,中国国家药品监督管理局(NMPA)宣布了一项检查倡议,允许生技药品的非端到端製造。此前,国家药监局要求生技药品必须在单一製造地进行端到端生产。

本质上,这意味着理想情况下原料药及其相应的产品都在同一家工厂生产。然而,国内生物製药界一直呼吁放宽这项规定,特别是考虑到外国生物製药製造商自由裁量权在不同地点生产原料药和成品。

低温运输仓储建设的大幅成长,凸显了高效医药仓储在中国日益增长的重要性。随着对温度敏感产品的需求不断增加,冷资料储存设施的扩建将在确保这些关键产品的完整性和可用性方面发挥关键作用。这一趋势凸显了对低温运输物流持续投资和创新的必要性,以支持製药业不断变化的需求。

药厂加大开发力度

中国政策制定者正积极寻求透过放鬆管制来促进创新,以吸引外资。这与先前对跨境研发施加限制的立场不同。值得注意的是,今年政府首次将聚焦在「创新药物」。光是2023年,创新药物许可和合作交易就将超过220项,价值2,660亿元人民币(约370亿美元)。

中国政府已推出多项倡议加强医疗卫生领域发展并促进国际合作。参与企业CGT 领域的国际企业正寻求透过投资、成立新业务、合併、收购甚至迁至四个指定的 FTZ 来抓住机会。这些企业涵盖了广泛的 CGT 相关领域,从 iPSC 和 CAR-T 到 mRNA、基因序列测定和体外诊断 (IVD/LDT)。

根据新《通知》,中国生物製药公司现在可以直接吸引外国投资。透过在这些自由贸易区内设立或迁移子公司,公司可以避免先前要求的可变利益营业单位(VIE)结构。

作为一项重要倡议,这家总部位于印地安那波里斯的公司计划在 2024 年 11 月投资 2.12 亿美元扩建其苏州工厂。此次扩建使苏州自1996年以来的累积投资金额达到150亿元人民币(21亿美元)。此前,该公司的主要减重药物 Zepbound 已于 2024 年 7 月在中国核准。此后不久,拜耳在北京开设了医疗研发中心,并宣布计划在美国以外建立首个创新培养箱Gateway Labs。

2024年9月,德国製药巨头拜耳在上海开设生命科学培养箱,称讚中国的创新能力「位居世界前两位」。就在一个月前,瑞士巨头罗氏诊断公司的一个部门宣布了一项价值 4.2 亿美元的巨额计划,以加强其在苏州的生产工厂,这是迄今为止其最大的投资。

此类战略投资凸显了中国市场的独特机会。儘管面临经济放缓、国内竞争激烈和地缘政治紧张等挑战,製药业仍然是一个亮点,而从高科技到汽车等各个领域都出现了犹豫。许多外国公司仍在寻找与本土生物技术公司进行有利可图且富有成效的合作的途径。

北京方面推动医疗卫生领域自由化的倡议部分是出于让老龄人口能够获得全球顶尖药品的愿望。这项自由化措施也刺激了製药生产设施的快速发展,对中国的医药仓储市场产生了重大影响。

中国医药仓储产业概况

中国医药仓储市场是全球竞争最激烈、成长最快的市场之一。这是在该国医疗保健产业不断发展、药品生产不断扩大和分销策略不断变化背景下发生的。随着中国製药业的持续成长,能够提供无缝仓储、高效物流和先进解决方案的公司将在这个竞争激烈的市场中占据优势。市场高度分散,有许多本地和国际参与企业,包括国药物流、DHL和CJ荣庆物流。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 调查前提条件

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态与洞察

- 市场概况(当前市场和经济的市场状况)

- 政府法规和倡议

- 科技趋势

- 市场动态

- 市场驱动因素

- 快速发展的製药业

- 人口成长是仓储市场的主要驱动力之一

- 市场限制/挑战

- 供应链中断

- 温度和低温运输管理

- 市场机会

- 技术创新

- 市场驱动因素

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 购买者/消费者的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争强度

- 地缘政治与疫情将如何影响市场

第五章 市场区隔

- 按服务类型

- 贮存

- 分配

- 库存管理

- 包装

- 其他的

- 按模式

- 低温运输仓库

- 非低温运输仓库

- 按最终用户

- 製药公司

- 医院和诊所

- 研究和政府组织

- 其他的

第六章 竞争格局

- 公司简介

- Sinopharm Logistics

- SF Express

- Kerry Logistics

- Yunda Holding

- CJ Rokin Logistics

- DHL Supply Chain

- DB Schenker

- Nippon Express

- Yamato Holdings

- CJ Rokin Logistics

- SF Express

- JD Logistics*

- 其他公司

第七章:市场的未来

第 8 章 附录

- 宏观经济指标(GDP分布,依活动划分)

- 经济统计 - 运输及仓储业对经济的贡献

- 相关药品进出口统计

The China Pharmaceutical Warehousing Market size is estimated at USD 14.33 billion in 2025, and is expected to reach USD 21.23 billion by 2030, at a CAGR of 8.17% during the forecast period (2025-2030).

Driven by biotechnology and innovative drug development, the Chinese pharmaceutical market is undergoing a significant transformation. This shift is largely propelled by strategic initiatives from the Chinese government, notably the "Healthy China 2030" plan, which seeks to bolster public health and champion scientific innovation.

China's biotechnology sector is on a rapid ascent, buoyed by hefty investments in research and development (R&D) and a supportive regulatory landscape. The market boasts a vibrant ecosystem where biotech startups, major pharmaceutical firms, and academic institutions collaborate, pushing the boundaries of medical research and pioneering new therapies.

A notable trend in China's biotechnology landscape is the infusion of artificial intelligence (AI) and big data analytics into drug development. Companies such as WuXi AppTec harness AI to refine drug discovery, streamline clinical trials, and bolster precision medicine strategies. Thanks to AI-driven platforms, WuXi AppTec has not only sped up the identification of promising drug candidates but also heightened the efficiency of its R&D endeavors.

Moreover, China's regulatory reforms, notably the expedited approval process for innovative drugs, have paved the way for swifter market entry of groundbreaking therapies, fostering an environment ripe for continuous innovation. The market is increasingly gravitating towards biosimilars and biopharmaceuticals, which not only provide cost-effective treatment alternatives but also broaden access to cutting-edge therapeutics.

Policies backing the expansion of digital health technologies have been rolled out by the Chinese government. Furthermore, initiatives such as the National Health Informatization Development Plan are working towards a unified health information system, seamlessly integrating data from diverse digital health platforms to boost data interoperability and healthcare coordination.

In June 2023, the FDA was contemplating a move to allow online pharmacies to dispense prescription drugs. This potential shift could pave the way for e-commerce giants like Alibaba and JD to tap into a burgeoning market. Discussions about this policy have been circulating since mid-last year, and its approval could unlock a market exceeding CNY 1 trillion (approximately USD 161 billion). Such a move would not only divert sales from traditional hospitals to online pharmacies but also challenge the longstanding dominance of state-run hospitals and distributors in the market.

The transformation of the Chinese pharmaceutical market also extends to the warehousing sector. With the rapid growth of the pharmaceutical industry, there is an increasing demand for advanced warehousing solutions to ensure the efficient storage and distribution of pharmaceutical products.

The Chinese pharmaceutical warehousing market is evolving to meet these needs, incorporating state-of-the-art technologies such as automated storage and retrieval systems (AS/RS), temperature-controlled environments, and real-time inventory management systems.

These advancements are crucial for maintaining the integrity and quality of pharmaceutical products throughout the supply chain. As the market continues to expand, the development of sophisticated warehousing infrastructure will play a pivotal role in supporting the overall growth and efficiency of the Chinese pharmaceutical industry.

China Pharmaceutical Warehousing Market Trends

Increase In Cold Chain Warehouse Development

In the first half of 2024, the volume of cold chain logistics hit 220 million tons, a rise of 4.4%. Concurrently, revenue from cold chain logistics climbed to CNY 277.9 billion (USD 38.9 billion), reflecting a 3.4% uptick compared to the same timeframe last year.

By June 2024, China's cold storage capacity expanded to 237 million cubic meters, showcasing a year-on-year growth of 7.73%. This year alone saw the addition of 9.42 million cubic meters in new cold storage capacity. In the first half of 2024, the leasing volume for cold storage across the nation surpassed 29 million cubic meters, marking an increase of over 8%.

The rising production and consumption of temperature-sensitive items, such as biologics, vaccines, and specialty drugs, underscore the need for expansive cold storage facilities. Biologics, unlike conventional drugs, are intricate substances sourced from biological entities, including humans and animals. These biological products encompass a wide spectrum, from vaccines to blood components.

Frequently utilized in advanced treatments, biologics exhibit heightened sensitivity to even minor fluctuations in their physical environment. Consequently, to cater to the surging demand for these products, pharmaceutical and healthcare firms must emphasize swift and dependable supply chain solutions.

In October 2024, the China National Medical Products Administration (NMPA) unveiled a pilot initiative permitting non-end-to-end manufacturing of biologics. Historically, the NMPA mandated that biologics undergo end-to-end production at a singular manufacturing site.

Essentially, this means both the drug substance and its corresponding product should ideally be produced within the same facility. However, the domestic biopharmaceutical sector has been pushing for a relaxation of this rule, particularly in light of the fact that foreign biologics manufacturers have been granted the leeway to produce the drug substance and its product at distinct locations.

The significant increase in cold chain warehouse development highlights the growing importance of efficient pharmaceutical warehousing in China. As the demand for temperature-sensitive products continues to rise, the expansion of cold storage facilities will play a crucial role in ensuring the integrity and availability of these critical products. This trend underscores the need for ongoing investment and innovation in cold chain logistics to support the pharmaceutical industry's evolving requirements.

Increase in Development of Pharmaceutical Manufactures

Chinese policymakers are actively working to attract foreign investment by relaxing regulations, a move aimed at fostering innovation. This marks a departure from their previous stance, which imposed restrictions on cross-border research and development. Notably, the government spotlighted "innovative drugs" in its work report for the first time this year. In 2023 alone, there were over 220 licensing and partnership deals for innovative drugs, amounting to a substantial RMB 266 billion (approximately USD 37 billion).

The Chinese government has rolled out several initiatives to bolster the healthcare sector and promote international collaboration. International players in the CGT arena are eyeing opportunities and considering actions like investments, establishing new entities, mergers, and acquisitions, or even relocating to four designated FTZs. These ventures span a wide array of CGT-related domains, from iPSCs and CAR-T to mRNA, gene sequencing, and in vitro diagnostics (IVD/LDT).

Thanks to the new Circular, biopharmaceutical firms in China can now directly draw foreign investments. By setting up or moving subsidiaries to the four FTZs, they sidestep the previously mandatory variable interest entity (VIE) structure.

In a significant move, an Indianapolis-based firm is set to invest a whopping USD 212 million in November 2024, expanding its Suzhou plant. This expansion will elevate its cumulative investment in Suzhou since 1996 to a staggering 15 billion yuan (USD 2.1 billion). This decision follows China's green light for its major weight loss drug, Zepbound, in July 2024. Shortly after, the firm launched a medical innovation center in Beijing and announced plans for a Gateway Labs, marking its inaugural innovation incubator outside the U.S.

In September 2024, Bayer, the German pharmaceutical giant, inaugurated a life science incubator in Shanghai, lauding China's innovation prowess as "among the world's top two." Just a month earlier, Roche Diagnostics, a Swiss behemoth's division, unveiled a massive USD 420 million project - its largest investment to date - to enhance its manufacturing facility in Suzhou.

These strategic investments shine a light on a unique opportunity within the Chinese market. Despite challenges like an economic slowdown, stiff domestic competition, and geopolitical strains causing hesitance in sectors from tech to automotive, the pharmaceutical realm remains a beacon. Many foreign entities still perceive avenues for profit and fruitful collaborations with local biotechs.

Part of Beijing's initiative to liberalize the healthcare sector is driven by a desire to ensure its aging populace has access to premier global medicines. This liberalization has also spurred an increase in the development of pharmaceutical manufacturing facilities, significantly impacting the Chinese pharmaceutical warehousing market.

China Pharmaceutical Warehousing Industry Overview

China's pharmaceutical warehousing market is one of the most competitive and fastest-growing in the world. It is due to the country's growing healthcare sector, growing pharmaceutical manufacturing, and changing distribution strategies. As the pharmaceutical industry in China continues to grow, companies that can provide seamless warehousing, effective distribution, and cutting-edge solutions will gain a competitive advantage in this highly competitive market. The market is highly fragmented, with many local and International players operating in the market, such as Sinopharm Logistics, DHL, CJ Rokin Logistics, etc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS AND DYNAMICS

- 4.1 Market Overview (Current Market Scenario of Market and Economy)

- 4.2 Government Regulations and Initiatives

- 4.3 Technological Trends

- 4.4 Market Dynamics

- 4.4.1 Market Drivers

- 4.4.1.1 Rapidly Expanding Pharmaceutical Industry

- 4.4.1.2 Population Growth is one of the main drivers for the warehousing market

- 4.4.2 Market Restraints/ Challenges

- 4.4.2.1 Supply Chain Disruptions

- 4.4.2.2 Temperature Controlled and Cold Chain Management

- 4.4.3 Market Opportunities

- 4.4.3.1 Technological Innovations

- 4.4.1 Market Drivers

- 4.5 Industry Attractiveness - Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Powers of Buyers/Consumers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Impact of Geopolitics and Pandemic on the Market

5 MARKET SEGMENTATION

- 5.1 By Service Type

- 5.1.1 Storage

- 5.1.2 Distribution

- 5.1.3 Inventory Management

- 5.1.4 Packaging

- 5.1.5 Others

- 5.2 By Mode

- 5.2.1 Cold Chain Warehouse

- 5.2.2 Non-Cold Chain Warehouse

- 5.3 By End User

- 5.3.1 Pharmaceutical Companies

- 5.3.2 Hospital and Clinics

- 5.3.3 Research Institiutes and Government Agencies

- 5.3.4 Others

6 COMPETITIVE LANDSCAPE

- 6.1 Overview (Market Concentration and Major Players)

- 6.2 Company Profiles

- 6.2.1 Sinopharm Logistics

- 6.2.2 SF Express

- 6.2.3 Kerry Logistics

- 6.2.4 Yunda Holding

- 6.2.5 CJ Rokin Logistics

- 6.2.6 DHL Supply Chain

- 6.2.7 DB Schenker

- 6.2.8 Nippon Express

- 6.2.9 Yamato Holdings

- 6.2.10 CJ Rokin Logistics

- 6.2.11 SF Express

- 6.2.12 JD Logistics*

- 6.3 Other Companies

7 FUTURE OF THE MARKET

8 APPENDIX

- 8.1 Macroeconomic Indicators (GDP Distribution, By Activity)

- 8.2 Economic Statistics - Transport and Storage Sector Contribution to Economy

- 8.3 Export and Import Statistics of Related Pharmaceutical Products

美国药品仓储业:市场占有率分析、产业趋势与统计及成长预测(2026-2031 年)

美国药品仓储业:市场占有率分析、产业趋势与统计及成长预测(2026-2031 年) 医药仓储市场:按温度类型、服务类型、储存类型、自动化程度、产品类型和最终用户划分 - 全球预测(2026-2032 年)

医药仓储市场:按温度类型、服务类型、储存类型、自动化程度、产品类型和最终用户划分 - 全球预测(2026-2032 年) 医药仓储市场规模、份额及成长分析(依服务类型、运输方式、最终用户及地区划分)-2026-2033年产业预测

医药仓储市场规模、份额及成长分析(依服务类型、运输方式、最终用户及地区划分)-2026-2033年产业预测 2025年全球医药仓储市场报告

2025年全球医药仓储市场报告 医药仓储市场-全球产业规模、份额、趋势、机会和预测(按类型、应用、地区和竞争细分,2020-2030 年)

医药仓储市场-全球产业规模、份额、趋势、机会和预测(按类型、应用、地区和竞争细分,2020-2030 年) 全球医药仓储市场(2025-2029)德国医药仓储:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)欧洲医药仓储:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)

全球医药仓储市场(2025-2029)德国医药仓储:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)欧洲医药仓储:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年) 全球药品仓库市场

全球药品仓库市场 全球药品仓储市场规模研究,按类型(冷链仓储、非冷链仓储)、按应用(药厂、药房、医院等)以及 2022-2032 年区域预测

全球药品仓储市场规模研究,按类型(冷链仓储、非冷链仓储)、按应用(药厂、药房、医院等)以及 2022-2032 年区域预测