|

市场调查报告书

商品编码

1940901

美国药品仓储业:市场占有率分析、产业趋势与统计及成长预测(2026-2031 年)United States Pharmaceutical Warehousing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

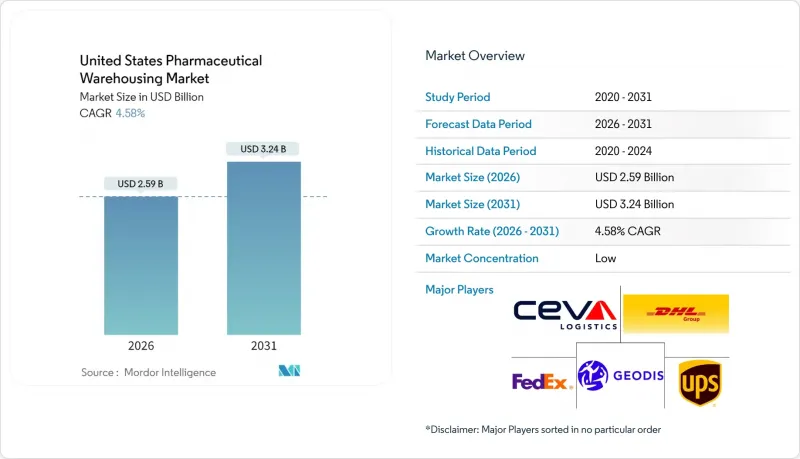

美国药品仓储业市场预计将从 2025 年的 24.8 亿美元成长到 2026 年的 25.9 亿美元,预计到 2031 年将达到 32.4 亿美元,2026 年至 2031 年的复合年增长率为 4.58%。

生物製药产量不断增长、DSCSA序列化规则的全面实施以及履约需求的激增,正推动着新的资金流入温控基础设施和自动化领域。不断扩展的细胞和基因疗法产品线增加了对超低温的要求,从而提高了每平方英尺的收益;同时,21 CFR 211.142强制要求的安全追踪系统正在改变仓库的IT预算结构。儘管能源、房地产和专业劳动力等成本阻力依然显着,但对机器人、物联网感测器和环保低温运输设计的持续投资正在提升营运效率。领先的第三方物流(3PL)供应商之间加速整合的动力,源于它们渴望赢得利润丰厚的医疗保健相关合约,并捍卫市场份额,抵御日益垂直整合的製造商和医疗保健系统的竞争。

美国药品仓储业市场趋势与洞察

美国药品生产强劲成长

2025年,年度资本支出将达到1,600亿美元(比2024年成长15%),每增加10亿美元的投资,将产生230万平方英尺的额外仓储需求。生物製药占新建设的44%,需要采用模组化布局以满足连续生产的需求。 FDA对先进製造技术的支援正在加速即时监控技术的应用,并鼓励各设施采用冗余的电力和数据系统。分散式细胞疗法生产正在治疗中心附近催生微型仓库,从而打破传统的中心辐射式网路。这些变化共同推动了美国医药仓储业市场对安全、高容量储存场所的需求。

对温控储存的需求日益增长

从mRNA疫苗(-80°C)到低温疗法(-196°C),超低温要求正逐渐成为主流。根据美国联邦法规21 CFR 600.15,严格的温度控制比室温基准会增加20-30%的能耗。这就需要采用物联网技术进行验证,并配备冗余的警报系统。永续性目标正在推动可重复使用的运输货柜,从而减少60%的石化燃料依赖。虽然营运商正在对其设施维修,例如安装高效压缩机和LED照明以降低能耗,但高昂的资本投入仍然是参与企业进入该领域的障碍。因此,低温运输能力在美国药品仓储业市场中越来越具有定价权。

严格遵守FDA cGMP和GDP法规的成本

持续的温度记录、电子追踪以及隔离区的设立,将使合规预算在2025年之前增加25%。 DSCSA序列化系统的成本在每个设施50万至200万美元之间,给小规模企业带来了沉重负担,即使在业务稳定后,仍有26%的企业未能合规。处罚措施包括罚款和刑事指控,这加速了行业的整合。日益繁重的文件工作推动了对第三方专业服务的需求,同时也压缩了通用储存的利润空间。这种监管负担正在减缓美国药品仓储业市场的成长动能。

细分市场分析

到2025年,分销和库存管理将占总收入的45.32%,凸显了长期合约对于稳定美国药品仓储业市场现金流的重要性。由于《药品供应链安全法案》(DSCSA)的执行力度加大,附加价值服务(序列化、套件组装和监管文件)正以5.72%的复合年增长率成长。基于云端的仓库管理系统(WMS)解决方案涵盖了90%的设施,提高了可视性和审核。

附加价值服务通常以基本费率的25%至40%收费,以抵销合规相关费用。机器人即服务(RaaS)模式降低了中型业者的进入门槛,加剧了市场分散化,同时也提高了效率。 FDA 21 CFR 205.50 法规规范了安全储存和处理,有利于能够大规模提供合规服务的营运商。这些趋势正在加强美国药品仓储业市场的储存营运基础,同时也增加了服务的复杂性。

儘管非低温运输设施仍占美国药品仓储业市场的 58.05%,但到 2031 年,低温运输产能将继续以 6.01% 的复合年增长率成长。冷藏、冷冻和超低温区域的收费比常温替代方案高出 150-200%,以弥补能源消耗。

为了平衡柔软性和资本支出,营运商正在对现有建筑进行模组化冷却室改造。物联网感测器可将温度偏差风险降低 60%,以避免整个产业每年 350 亿美元的损失。温度控制要求设定了很高的合规门槛,保护了现有企业的利益。随着生物製药产品线的扩展,低温运输在美国药品仓储业市场的份额将逐步增加。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 美国药品生产强劲成长

- 对温控(2-8°C)储存的需求日益增长

- 生物製药和特用药品产量快速成长

- 快速B2B/B2C电子商务履约要求

- DSCSA序列化日期有助于安全仓库管理

- 主要城市附近的城市微型仓配中心

- 市场限制

- 严格遵守FDA cGMP和GDP法规的成本

- 冷藏仓库能源和房地产成本不断上涨

- 高科技仓库技术纯熟劳工短缺

- 日益严重的网路安全/资料完整性风险(潜在威胁)

- 价值/供应链分析

- 监管状态(FDA、DSCSA、DEA、OSHA)

- 技术展望(仓库管理系统、物联网、自动化、机器人技术)

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 地缘政治和疫情对仓储业的影响

第五章 市场规模与成长预测

- 按服务类型

- 贮存

- 经销和库存管理

- 附加价值服务及更多

- 按仓库类型

- 低温运输仓库

- 冷藏(0-5°C)

- 冷冻(-18 至 0°C)

- 环境的

- 超低温冷冻(低于-20°C)

- 非低温运输仓库

- 低温运输仓库

- 依产品类型

- 处方药

- 非处方药

- 生物製药和生物相似药

- 疫苗和血液製品

- 临床试验药物

- 细胞和基因治疗

- 特药(非生物製药)

- 动物用药品

- 其他的

- 最终用户

- 製药公司

- 医疗保健提供者

- 零售商店和药局

- 批发商和经销商

- 其他的

第六章 竞争情势

- 市场集中度

- 策略发展与投资

- 市占率分析

- 公司简介

- United Parcel Service Inc.

- DHL Group

- FedEx Corp.

- GEODIS SA

- CEVA Logistics

- Lineage Logistics

- Americold Logistics

- Cencora

- BioPharma Logistics

- Rhenus SE & Co. KG

- Kuehne+Nagel

- XPO Logistics

- KRC Logistics

- GXO Logistics

- MD Logistics

- Langham Logistics

- Crown LSP Group

- LifeScience Logistics

- Go Freight

- DSV

第七章 市场机会与未来展望

The United States Pharmaceutical Warehousing Market is expected to grow from USD 2.48 billion in 2025 to USD 2.59 billion in 2026 and is forecast to reach USD 3.24 billion by 2031 at 4.58% CAGR over 2026-2031.

Rising biologics output, full enforcement of the DSCSA serialization rule, and surging e-commerce fulfillment volumes are channeling new capital into temperature-controlled infrastructure and automation. Cell and gene therapy pipelines are adding ultra-low temperature requirements that lift revenue per square foot, while secure track-and-trace systems mandated by 21 CFR 211.142 are reshaping warehouse IT budgets. Cost headwinds energy, real estate and specialized labor remain pronounced, yet continuous investment in robotics, IoT sensors and green cold-chain designs is improving operating leverage. Intensifying consolidation among third-party logistics (3PL) leaders aims to capture higher-margin healthcare contracts and defend share against vertically integrating manufacturers and health-system operators.

United States Pharmaceutical Warehousing Market Trends and Insights

Robust Growth of U.S. Pharmaceutical Output

Annual capital spending of USD 160 billion in 2025 up 15% from 2024 couples every USD 1 billion invested with 2.3 million sq ft of extra warehouse need. Biologics represent 44% of new builds, prompting modular layouts that can flex with continuous-manufacturing schedules. FDA support for Advanced Manufacturing Technologies is accelerating real-time monitoring adoption, pushing facilities to embed redundant power and data systems. Decentralized production of cell therapies is spawning micro-warehouses near treatment centers, eroding the legacy hub-and-spoke network. These shifts collectively lift demand for secure, high-throughput storage nodes across the United States pharmaceutical warehousing market.

Expansion of Temperature-Controlled Storage Needs

Ultra-low requirements from mRNA vaccines (-80 °C) to cryogenic therapies (-196 °C) are now mainstream, raising energy use 20-30% above ambient operations rules under 21 CFR 600.15 mandate precise ranges, prompting IoT-enabled validations and alarm redundancies. Sustainability targets are spurring reusable shippers that cut fossil-fuel reliance 60%. Operators retrofit high-efficiency compressors and LED lighting to curb consumption, yet capital intensity remains a barrier for smaller entrants. Consequently, cold-chain capacity garners pricing power within the United States pharmaceutical warehousing market.

Stringent FDA cGMP & GDP Compliance Costs

Continuous temperature logging, electronic tracing and quarantine zones add 25% to 2025 compliance budgets. DSCSA serialization systems cost USD 0.5-2 million per facility, stretching small operators; 26% remain non-compliant post-stabilization. Penalties range from fines to criminal liability, accelerating consolidation. Documentation load drives demand for third-party specialists, yet shrinks margins for commodity storage. This regulatory burden dampens the growth curve of the United States pharmaceutical warehousing market.

Other drivers and restraints analyzed in the detailed report include:

- Surge in Biologics & Specialty-Drug Volumes

- Rapid B2B/B2C E-commerce Fulfillment Requirements

- Rising Energy and Real-Estate Costs for Cold Storage

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Distribution and Inventory Management generated 45.32% of 2025 revenue, a testament to long-term contracts that stabilize cash flows within the United States pharmaceutical warehousing market. Value-added offerings-serialization, kitting and regulatory documentation-are scaling at a 5.72% CAGR as DSCSA enforcement tightens. Cloud-based WMS solutions now cover 90% of facilities, enhancing visibility and audit readiness.

Value-added services typically bill 25-40% above baseline rates, offsetting compliance overhead. Robotics-as-a-Service models lower entry barriers for mid-tier operators, supporting market fragmentation while bolstering efficiency. FDA 21 CFR 205.50 stipulates secure storage and handling, favoring providers that can turnkey compliance at scale. These dynamics reinforce storage as the anchor while upgrading service complexity across the United States pharmaceutical warehousing market.

Non-cold-chain sites still constitute 58.05% of the United States pharmaceutical warehousing market size, but cold-chain capacity is outpacing at a 6.01% CAGR through 2031. Chilled, frozen and ultra-low zones command rates 150-200% higher than ambient alternatives, compensating for energy drain.

Operators retrofit ambient structures with modular cool chambers to balance flexibility and capex. IoT sensors cut temperature excursion risk 60%, curbing USD 35 billion annual losses industry-wide temperature mandates create high compliance hurdles, shielding incumbents. As biologics pipelines swell, cold-chain share will progressively rise within the United States pharmaceutical warehousing market.

The United States Pharmaceutical Warehousing Market Report is Segmented by Service Type (Storage, Distribution and Inventory Management, and More), Warehouse Type (Cold-Chain Warehouse, Non-Cold-Chain Warehouse), Product Type (Prescription Drugs, and More), End User (Pharmaceutical Manufacturers, Healthcare Providers, Retail & Pharmacies, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- United Parcel Service Inc.

- DHL Group

- FedEx Corp.

- GEODIS SA

- CEVA Logistics

- Lineage Logistics

- Americold Logistics

- Cencora

- BioPharma Logistics

- Rhenus SE & Co. KG

- Kuehne + Nagel

- XPO Logistics

- KRC Logistics

- GXO Logistics

- MD Logistics

- Langham Logistics

- Crown LSP Group

- LifeScience Logistics

- Go Freight

- DSV

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Robust growth of U.S. pharmaceutical output

- 4.2.2 Expansion of temperature-controlled (2-8 °C) storage needs

- 4.2.3 Surge in biologics and specialty-drug volumes

- 4.2.4 Rapid B2B/B2C e-commerce fulfillment requirements

- 4.2.5 DSCSA serialization deadline boosting secure warehousing

- 4.2.6 Urban micro-fulfillment hubs near key metros

- 4.3 Market Restraints

- 4.3.1 Stringent FDA cGMP and GDP compliance costs

- 4.3.2 Rising energy and real-estate costs for cold storage

- 4.3.3 Skilled-labor shortages in high-tech warehouses

- 4.3.4 Escalating cybersecurity / data-integrity risks (under-the-radar)

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape (FDA, DSCSA, DEA, OSHA)

- 4.6 Technological Outlook (WMS, IoT, Automation, Robotics)

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Geopolitics and Pandemic on Warehousing

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 By Service Type

- 5.1.1 Storage

- 5.1.2 Distribution and Inventory Management

- 5.1.3 Value-added Services and Others

- 5.2 By Warehouse Type

- 5.2.1 Cold-Chain Warehouse

- 5.2.1.1 Chilled (0-5°C)

- 5.2.1.2 Frozen (-18-0°C)

- 5.2.1.3 Ambient

- 5.2.1.4 Deep-Frozen / Ultra-Low (less than-20 °C)

- 5.2.2 Non-Cold-Chain Warehouse

- 5.2.1 Cold-Chain Warehouse

- 5.3 By Product Type

- 5.3.1 Prescription Drugs

- 5.3.2 OTC Drugs

- 5.3.3 Biologics and Biosimilars

- 5.3.4 Vaccines and Blood Products

- 5.3.5 Clinical Trail Materials

- 5.3.6 Cell and Gene Therapies

- 5.3.7 Specialty Medicine (non-biologic)

- 5.3.8 Veterinary Medicine

- 5.3.9 Others

- 5.4 By End User

- 5.4.1 Pharmaceutical Manufacturers

- 5.4.2 Healthcare Providers

- 5.4.3 Retail and Pharmacies

- 5.4.4 Distributors and Wholesalers

- 5.4.5 Others

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves and Investments

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 United Parcel Service Inc.

- 6.4.2 DHL Group

- 6.4.3 FedEx Corp.

- 6.4.4 GEODIS SA

- 6.4.5 CEVA Logistics

- 6.4.6 Lineage Logistics

- 6.4.7 Americold Logistics

- 6.4.8 Cencora

- 6.4.9 BioPharma Logistics

- 6.4.10 Rhenus SE & Co. KG

- 6.4.11 Kuehne + Nagel

- 6.4.12 XPO Logistics

- 6.4.13 KRC Logistics

- 6.4.14 GXO Logistics

- 6.4.15 MD Logistics

- 6.4.16 Langham Logistics

- 6.4.17 Crown LSP Group

- 6.4.18 LifeScience Logistics

- 6.4.19 Go Freight

- 6.4.20 DSV

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

医药仓储市场:按温度类型、服务类型、储存类型、自动化程度、产品类型和最终用户划分 - 全球预测(2026-2032 年)

医药仓储市场:按温度类型、服务类型、储存类型、自动化程度、产品类型和最终用户划分 - 全球预测(2026-2032 年) 医药仓储市场规模、份额及成长分析(依服务类型、运输方式、最终用户及地区划分)-2026-2033年产业预测

医药仓储市场规模、份额及成长分析(依服务类型、运输方式、最终用户及地区划分)-2026-2033年产业预测 2025年全球医药仓储市场报告

2025年全球医药仓储市场报告 医药仓储市场-全球产业规模、份额、趋势、机会和预测(按类型、应用、地区和竞争细分,2020-2030 年)

医药仓储市场-全球产业规模、份额、趋势、机会和预测(按类型、应用、地区和竞争细分,2020-2030 年) 全球医药仓储市场(2025-2029)

全球医药仓储市场(2025-2029) 中国医药仓储:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)德国医药仓储:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)欧洲医药仓储:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)

中国医药仓储:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)德国医药仓储:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)欧洲医药仓储:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年) 全球药品仓库市场

全球药品仓库市场 全球药品仓储市场规模研究,按类型(冷链仓储、非冷链仓储)、按应用(药厂、药房、医院等)以及 2022-2032 年区域预测

全球药品仓储市场规模研究,按类型(冷链仓储、非冷链仓储)、按应用(药厂、药房、医院等)以及 2022-2032 年区域预测