|

市场调查报告书

商品编码

1683815

法国工程塑胶市场:份额分析、产业趋势和成长预测(2025-2030 年)France Engineering Plastics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

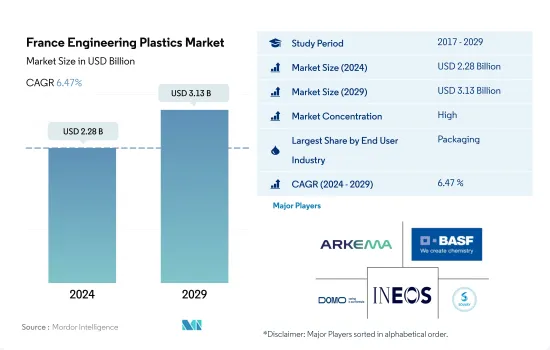

预计 2024 年法国工程塑胶市场规模将达到 22.8 亿美元,到 2029 年将达到 31.3 亿美元,预测期内(2024-2029 年)的复合年增长率为 6.47%。

先进材料的广泛应用推动了工程塑胶的需求

- 工程塑料由于其重量轻、强度高、低疲劳和低可燃性而被用于航太、包装和其他应用的内墙板和门。

- 2022 年,法国工程塑胶市场占欧洲工程塑胶市场的 9%(以金额为准)。消费量增加的主要驱动因素之一是包装和电气电子行业的使用量增加。

- 包装产业是全国最大的工程塑胶消费产业,2022年与前一年同期比较成长8.72%(以金额为准)。由于对即食方便食品的需求增加和忙碌生活方式的兴起,包装材料的消费量增加,从而促进了这些塑胶的销售。预计在预测期内,透过电子商务网站进行网路购物的趋势也将推动包装产业的发展。法国电子商务市场是最大的市场之一,在欧洲排名第二,在全球排名第五。预计将从 2023 年的 1,065 亿美元成长到 2027 年的 1,517 亿美元。

- 航太工业是工程塑胶成长最快的消费产业,预计在预测期内将实现最高的以金额为准,达到 8.22%。预计预测期内该国飞机零件产量的增加将推动这些塑胶的需求。例如,该国的飞机零件产量将从2022年的645亿美元增加到2029年的1,030亿美元。

法国工程塑胶市场趋势

技术创新可能促进电气和电子设备产量的增加

- 电气电子产业技术创新的快速步伐推动着对更新、更快的电气电子产品的持续需求,从而促进了法国的电气电子产品生产。 2022年,法国是欧洲第二大电气和电子产品生产国,占8.1%的市场。

- 2020年,由于全国范围内的封锁和製造工厂的暂时关闭,导致供应链和进出口贸易中断,该国电气和电子产品产量与前一年同期比较减13.7%。 2021年,法国家用电器出口额达13.6亿欧元,比2020年成长16.4%。因此,2021年法国电气和电子产品生产收入与前一年同期比较成长了27.5%。

- 由于政府投资增加,法国电子产业预计将实现成长。预计到2030年将投资超过50亿欧元用于电子技术的开发和工业化。预测期内,对虚拟实境、物联网解决方案、5G 连接和机器人等先进技术的需求预计会增加。由于技术进步,预测期内对消费性电子产品的需求预计会增加。到2027年,该国消费电子产品销售额预计将成长11.9%,市值达193亿美元。

法国工程塑胶产业概况

法国工程塑胶市场相当集中,前五大公司占据100%的市场。市场的主要企业是:阿科玛、BASFSE、道默化学、英力士和索尔维(按字母顺序排列)。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章执行摘要和主要发现

第二章 报告要约

第 3 章 简介

- 研究假设和市场定义

- 研究范围

- 调查方法

第四章 产业主要趋势

- 最终用户趋势

- 航太

- 车

- 建筑和施工

- 电气和电子

- 包装

- 进出口趋势

- 价格趋势

- 回收概述

- 聚酰胺 (PA) 回收趋势

- 聚碳酸酯 (PC) 回收趋势

- 聚对苯二甲酸乙二醇酯 (PET) 的回收趋势

- 苯乙烯共聚物(ABS、SAN)的回收趋势

- 法律规范

- 法国

- 价值链与通路分析

第五章 市场区隔

- 最终用户产业

- 航太

- 车

- 建筑和施工

- 电气和电子

- 工业/机械

- 包装

- 其他最终用户产业

- 树脂类型

- 氟树脂

- 按子类型

- 乙烯-四氟乙烯(ETFE)

- 氟化乙烯丙烯 (FEP)

- 聚四氟乙烯(PTFE)

- 聚氟乙烯 (PVF)

- 聚二氟亚乙烯(PVDF)

- 其他子树脂类型

- 液晶聚合物(LCP)

- 聚酰胺(PA)

- 依树脂类型分

- 芳香聚酰胺

- 聚酰胺(PA)6

- 聚酰胺(PA)66

- 聚邻苯二甲酰胺

- 聚丁烯对苯二甲酸酯(PBT)

- 聚碳酸酯(PC)

- 聚醚醚酮 (PEEK)

- 聚对苯二甲酸乙二醇酯(PET)

- 聚酰亚胺(PI)

- 聚甲基丙烯酸甲酯 (PMMA)

- 聚甲醛(POM)

- 苯乙烯共聚物(ABS 和 SAN)

- 氟树脂

第六章 竞争格局

- 关键策略趋势

- 市场占有率分析

- 业务状况

- 公司简介包括全球概况、市场层级概况、主要业务部门、财务状况、员工人数、关键资讯、市场排名、市场占有率、产品和服务以及最新发展分析。

- Alfa SAB de CV

- Arkema

- BASF SE

- Celanese Corporation

- Domo Chemicals

- INEOS

- Mitsubishi Chemical Corporation

- Radici Partecipazioni SpA

- Rohm GmbH

- Solvay

- Teijin Limited

- Trinseo

- Victrex

第七章:执行长的关键策略问题

第 8 章 附录

- 世界概况

- 概述

- 五力分析框架(产业吸引力分析)

- 全球价值链分析

- 市场动态(DRO)

- 资讯来源和进一步阅读

- 图片列表

- 关键见解

- 资料包

- 词彙表

简介目录

Product Code: 5000156

The France Engineering Plastics Market size is estimated at 2.28 billion USD in 2024, and is expected to reach 3.13 billion USD by 2029, growing at a CAGR of 6.47% during the forecast period (2024-2029).

Rising adoption of advanced materials to drive the demand for engineering plastics

- Engineering plastics are used in interior wall panels and doors in aerospace, packaging, and other applications due to their lightweight nature, high strength, low fatigue, and low flammability.

- The French engineering plastics market accounted for 9% (by value) of the European engineering plastics market in 2022. One of the primary drivers of the increasing consumption is their increased use in the packaging and electrical and electronics industries.

- The packaging industry is the country's largest consumer of engineering plastics, accounting for 8.72% (by value) in 2022 compared to the previous year. Packaging material consumption increased due to increased demand for ready-to-eat convenience foods and the emerging trend of on-the-go lifestyles, thus boosting sales of these plastics. The growing trend of online shopping via e-commerce websites is also expected to propel the packaging industry during the forecast period. The French e-commerce market is one of the largest markets, ranking second in Europe and fifth in the world. It is projected to reach USD 151.7 billion in 2027 from USD 106.5 billion in 2023.

- The aerospace industry is expected to be the fastest-growing consumer of engineering plastics, with the highest CAGR of 8.22% in terms of value during the forecast period. The rising aircraft component production in the country is projected to drive the demand for these plastics during the forecast period. For instance, the country's aircraft component production reached USD 103 billion in 2029 from USD 64.5 billion in 2022.

France Engineering Plastics Market Trends

Technological innovations may increase electrical and electronics production

- The rapid pace of technological innovation in the electrical and electronics industry is driving consistent demand for newer and faster electrical and electronic products, thus boosting their production in France. In 2022, France was the second-largest producer of electrical and electronic products, accounting for 8.1% of the European market.

- In 2020, the country's electrical and electronic production decreased by 13.7% in terms of revenue compared to the previous year, owing to country-wide lockdowns and the temporary shutdown of manufacturing facilities, leading to disruptions in supply chains and import and export trade. In 2021, France's consumer electronics exports reached EUR 1.36 billion, 16.4% higher than in 2020. As a result, electrical and electronic production in France recorded a growth rate of 27.5% by revenue in 2021 compared to the previous year.

- The French electronics industry is expected to grow due to rising government investments. It is expected to receive more than EUR 5 billion in investment by 2030 for the development and industrialization of electronic technologies. The demand for advanced technologies such as virtual reality, IoT solutions, 5G connectivity, and robotics is expected to grow during the forecast period. Due to technological advancements, the demand for consumer electronics is expected to rise during the forecast period. By 2027, the sales of consumer electronics in the country are projected to grow by 11.9% and generate a market value of USD 19.3 billion.

France Engineering Plastics Industry Overview

The France Engineering Plastics Market is fairly consolidated, with the top five companies occupying 100%. The major players in this market are Arkema, BASF SE, Domo Chemicals, INEOS and Solvay (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End User Trends

- 4.1.1 Aerospace

- 4.1.2 Automotive

- 4.1.3 Building and Construction

- 4.1.4 Electrical and Electronics

- 4.1.5 Packaging

- 4.2 Import And Export Trends

- 4.3 Price Trends

- 4.4 Recycling Overview

- 4.4.1 Polyamide (PA) Recycling Trends

- 4.4.2 Polycarbonate (PC) Recycling Trends

- 4.4.3 Polyethylene Terephthalate (PET) Recycling Trends

- 4.4.4 Styrene Copolymers (ABS and SAN) Recycling Trends

- 4.5 Regulatory Framework

- 4.5.1 France

- 4.6 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

- 5.1 End User Industry

- 5.1.1 Aerospace

- 5.1.2 Automotive

- 5.1.3 Building and Construction

- 5.1.4 Electrical and Electronics

- 5.1.5 Industrial and Machinery

- 5.1.6 Packaging

- 5.1.7 Other End-user Industries

- 5.2 Resin Type

- 5.2.1 Fluoropolymer

- 5.2.1.1 By Sub Resin Type

- 5.2.1.1.1 Ethylenetetrafluoroethylene (ETFE)

- 5.2.1.1.2 Fluorinated Ethylene-propylene (FEP)

- 5.2.1.1.3 Polytetrafluoroethylene (PTFE)

- 5.2.1.1.4 Polyvinylfluoride (PVF)

- 5.2.1.1.5 Polyvinylidene Fluoride (PVDF)

- 5.2.1.1.6 Other Sub Resin Types

- 5.2.2 Liquid Crystal Polymer (LCP)

- 5.2.3 Polyamide (PA)

- 5.2.3.1 By Sub Resin Type

- 5.2.3.1.1 Aramid

- 5.2.3.1.2 Polyamide (PA) 6

- 5.2.3.1.3 Polyamide (PA) 66

- 5.2.3.1.4 Polyphthalamide

- 5.2.4 Polybutylene Terephthalate (PBT)

- 5.2.5 Polycarbonate (PC)

- 5.2.6 Polyether Ether Ketone (PEEK)

- 5.2.7 Polyethylene Terephthalate (PET)

- 5.2.8 Polyimide (PI)

- 5.2.9 Polymethyl Methacrylate (PMMA)

- 5.2.10 Polyoxymethylene (POM)

- 5.2.11 Styrene Copolymers (ABS and SAN)

- 5.2.1 Fluoropolymer

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Alfa S.A.B. de C.V.

- 6.4.2 Arkema

- 6.4.3 BASF SE

- 6.4.4 Celanese Corporation

- 6.4.5 Domo Chemicals

- 6.4.6 INEOS

- 6.4.7 Mitsubishi Chemical Corporation

- 6.4.8 Radici Partecipazioni SpA

- 6.4.9 Rohm GmbH

- 6.4.10 Solvay

- 6.4.11 Teijin Limited

- 6.4.12 Trinseo

- 6.4.13 Victrex

7 KEY STRATEGIC QUESTIONS FOR ENGINEERING PLASTICS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

工程塑胶:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

工程塑胶:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 2026年全球工程塑胶市场报告

2026年全球工程塑胶市场报告 5G专用工程塑胶:按树脂类型、製程、应用和最终用途产业分類的全球预测,2026-2032年PA66工程塑胶市场依製造流程、产品类型、等级及最终用途产业划分-2026-2032年全球预测

5G专用工程塑胶:按树脂类型、製程、应用和最终用途产业分類的全球预测,2026-2032年PA66工程塑胶市场依製造流程、产品类型、等级及最终用途产业划分-2026-2032年全球预测 先进工程聚合物市场预测至2032年:按聚合物类型、形态、性能、技术、最终用户和地区分類的全球分析

先进工程聚合物市场预测至2032年:按聚合物类型、形态、性能、技术、最终用户和地区分類的全球分析 日本工程塑胶市场报告(按树脂类型、最终用途产业和地区划分,2026-2034年)

日本工程塑胶市场报告(按树脂类型、最终用途产业和地区划分,2026-2034年) 工程塑胶市场规模、份额和成长分析(按树脂类型、最终用途和地区划分)-2026-2033年产业预测

工程塑胶市场规模、份额和成长分析(按树脂类型、最终用途和地区划分)-2026-2033年产业预测 改质塑胶市场规模、占有率、预测及趋势分析:依产品类型、改质类型和应用划分 - 全球预测至 2035 年

改质塑胶市场规模、占有率、预测及趋势分析:依产品类型、改质类型和应用划分 - 全球预测至 2035 年 工程塑胶市场规模、占有率、成长及全球产业分析:依类型、应用和地区划分的洞察与预测(2024-2032 年)

工程塑胶市场规模、占有率、成长及全球产业分析:依类型、应用和地区划分的洞察与预测(2024-2032 年) PEEK特种工程塑胶:全球市场占有率及排名、总收入及需求预测(2025-2031年)

PEEK特种工程塑胶:全球市场占有率及排名、总收入及需求预测(2025-2031年)

▼