|

市场调查报告书

商品编码

1938992

生物有机肥料:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Biological Organic Fertilizer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

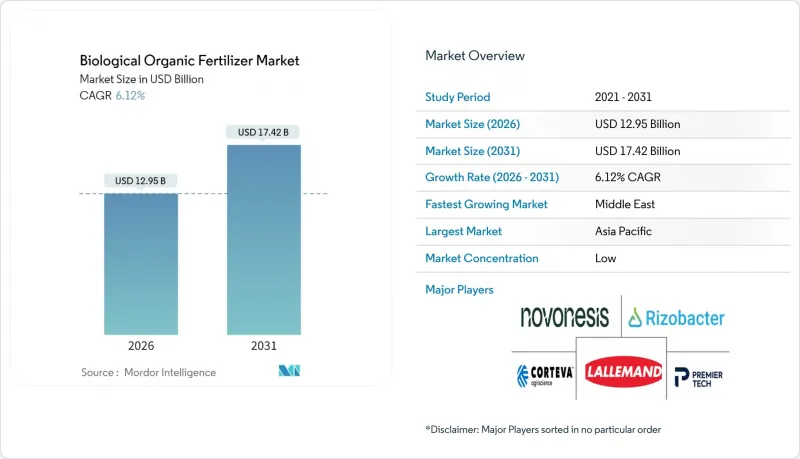

预计到 2026 年,生物有机肥料市场规模将达到 129.5 亿美元,高于 2025 年的 122 亿美元。

预计到 2031 年将达到 174.2 亿美元,2026 年至 2031 年的复合年增长率为 6.12%。

更严格的合成材料法规、不断扩大的排碳权通讯协定以及微生物联合体技术的快速发展正在重塑种植者的经济格局,并推动各类农作物对生物肥料的需求。美国联邦和州政府的激励措施、中国积极的土壤健康政策以及欧盟的碳边境税持续提高传统化肥的机会成本,加速了生物肥料在整个产业的普及。亚太地区凭藉大规模的国家补贴计画保持主导地位,而中东地区则实现了最快增长,这主要得益于优先发展耐盐生物材料的粮食安全投资。目前,竞争优势主要体现在保质期创新、包封技术专利以及将生物肥料整合到再生农业服务方案中。总体而言,生物有机市场正处于结构性成长阶段,监管、气候和消费者等多方面因素共同推动其渗透到特种作物以外的更广泛领域。

全球生物有机肥料市场趋势与洞察

联邦政府对再生农业的奖励措施

政府补贴显着缩短了农民从合成氮肥转向微生物肥料的投资回收期。美国农业部在其「气候智慧型商品伙伴关係计画」下,将于2024年提供31亿美元,用于支付高达50%的生物投入品转型成本。印度的直接转移支付计画也适用于生物肥料,而中国的「十四五」规划要求到2026年,30%的劣化农地使用有机改良剂,从而刺激稳定的需求。这些措施共同降低了农民的资金风险,保护了国家粮食系统免受与天然气价格相关的尿素价格波动的影响,并支持生物有机市场持续成长。

加强对合成肥料的监管

欧盟碳边境调节机制(CBAM)将于2024年全面实施,届时氨基肥料的在地采购成本将上涨高达20%。矿物磷酸盐镉含量上限和中国长江流域氮排放上限的实施,都增加了合规成本,使得生物来源肥料成为经济合理的选择。透过遥感探测审核和许可证吊销等手段进行的即时执法,使得所有农地作物对生物有机肥料的需求激增。

在炎热气候下寿命较短

在35°C培养90天后,微生物群落数量最多可减少80%,进而降低了旱地市场的田间功效。有限的低温运输基础设施和包埋过程导致的高昂配方成本阻碍了小规模农户的采用。 String Bio公司研发的甲烷衍生蛋白载体可在45°C下稳定微生物,但目前仍在等待广泛的监管批准。在出现可扩展的解决方案之前,这项限制将限制生物有机市场在短期内的成长。

细分市场分析

到2025年,根瘤菌将维持31.65%的生物有机肥料市场份额,而菌根真菌的复合年增长率将达到8.53%,在所有产品类型中最高。这些复合配方能够同步释放多种营养物质,使农民能够在不影响产量的前提下减少合成投入品的使用。增强根係发育和提高耐旱性进一步推动了雨养农业系统(尤其是在巴西和美国)的需求。製造商正越来越多地将复合产品与种子披衣结合使用,以确保田间施用均匀,并简化大型农场的物流。由于每种微生物成分都需要单独的申请文件,监管审批仍有延迟。儘管存在这一瓶颈,但日益加剧的大宗商品价格波动正促使主流生产商转向多功能复合产品,从而确保生物有机肥市场这一高价值细分领域的稳定增长。

有机残渣产品能够达到种植者设定的土壤有机质目标,但矿化率的不确定性限制了精准的养分管理。鱼粉和骨粉是饲料市场的关键成分。绿肥施用受益于再生农业的补贴。油粕仍然具有成本效益,但缺乏监管的通路可能导致纯度不稳定。这些截然不同的成长轨迹凸显了产业的变化:先进的微生物添加剂正在从作用缓慢的残渣产品中夺取市场份额,尤其是在高价值的出口园艺领域,可靠及时的养分供应至关重要。

区域分析

亚太地区预计2025年将贡献39.78%的收入,这主要得益于印度的直接转移支付计画和中国的有机农业政策。日本和澳洲正透过出口导向园艺实现稳定成长,而园艺需要经过认证的投入品。市场需求强劲,但仿冒品和小规模分散的耕地面积使得品管和分销变得复杂。印度国家化肥有限公司和古吉拉突邦化肥化工有限公司正在扩大国内微生物投入品的生产,但各邦之间的品质参差不齐,这为提供检验的微生物群落的跨国公司创造了机会。

北美和欧洲正共同支持当前的需求。美国已拨款31亿津贴用于在玉米和大豆种植系统中引入生物材料,加拿大也拨款5000万加元(约合3700万美元)用于一项豆类和菜籽计划,该项目将减少高达40%的温室气体排放。欧盟对矿物磷酸盐的镉含量限制以及碳边境调节税进一步促进了微生物替代疗法的应用,但成员国核准的延误增加了成本和时间。生产者合作社正越来越多地与大型生技药品生产商签订集体供应协议,以确保获得批量折扣和现场支援服务。

中东地区成长率位居全球之首,年复合成长率高达7.52%,这主要得益于阿联酋的国家粮食安全战略和沙乌地阿拉伯耗资100亿沙乌地里亚尔(约27亿美元)的「2030愿景」灌溉现代化计画。耐盐生物材料非常适合海水淡化农业系统,因此在可控环境下得到了广泛应用。在巴西和阿根廷的主导,南美洲凭藉着数十年来在大豆根瘤菌方面的丰富经验,以及阿根廷根瘤菌公司等区域生产商不断扩大的产能,正蓬勃发展。捐助者资助的试验计画正在推动非洲的成长,但低温运输不足和培训基础设施落后限制了其近期成长潜力。这些区域性的发展势头正在增强全球韧性,使已开发经济体和新兴经济体的成长引擎更加多元化。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 联邦政府对再生农业的奖励措施

- 加强对合成肥料的监管

- 有机加工食品製造商的需求迅速成长

- 微生物群落混合物的快速传播

- 将排碳权货币化用于改善土壤微生物组

- 专利生物刺激剂和生物肥料配方加速测试

- 市场限制

- 在炎热气候下保存期限短

- 各国註册障碍分散

- 除特色作物种植区外,其他地区农民的意识程度较低

- 排碳权定价模型的不确定性

- 监管环境

- 技术展望

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 按类型

- 微生物

- 根瘤菌

- 固氮菌

- 固氮螺菌

- 蓝藻

- 磷酸盐溶解细菌

- 菌根

- 其他微生物

- 有机残留物

- 绿肥

- 鱼粉

- 骨粉

- 油饼

- 其他的

- 微生物

- 透过使用

- 谷物和谷类

- 豆类和油籽

- 水果和蔬菜

- 经济作物

- 草坪和观赏植物

- 按地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 北美其他地区

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 亚太其他地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中东

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 其他中东地区

- 非洲

- 南非

- 奈及利亚

- 其他非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Novonesis A/S

- Rizobacter Argentina SA

- Lallemand Inc.

- Premier Tech

- Symborg(Corteva Agriscience)

- National Fertilizers Limited

- Madras Fertilizers Limited

- T Stanes and Company Limited

- Gujarat State Fertilizers and Chemicals Ltd

- String Bio

- Rashtriya Chemicals and Fertilizers Ltd

- Agrinos

- Biomax Naturals

- Agri Life

- Biofosfatos do Brasil

- Kiwa Bio-Tech Products Group Corporation

- Protan AG

- Mapleton Agri Biotech Pty Limited

- Bio Nature Technology PTE Ltd.

- Kribhco

- Bio Ark Pte Ltd

- Savio BIO Organic and Fertilizers Private Limited

- ACI Biolife

第七章 市场机会与未来展望

Biological organic fertilizer market size in 2026 is estimated at USD 12.95 billion, growing from 2025 value of USD 12.2 billion with 2031 projections showing USD 17.42 billion, growing at 6.12% CAGR over 2026-2031.

Strengthening synthetic-input regulations, expanding carbon-credit protocols, and rapid gains in microbial-consortia technology are reshaping producer economics and spurring demand across row-crop acreage. Federal and state incentives in the United States, aggressive soil-health mandates in China, and the European Union's carbon-border tariffs continue to raise the opportunity cost of conventional fertilizers, accelerating industry adoption. The Asia-Pacific region retains its primacy through large-scale national subsidy programs, while the Middle East registers the fastest growth, thanks to food-security investments that favor saline-tolerant biological inputs. Competitive differentiation now pivots on shelf-life innovation, encapsulation patents, and the integration of biofertilizers into bundled regenerative-agriculture service packages. Overall, the biological organic fertilizer market is on a structural growth path, with regulatory, climatic, and consumer forces aligning to deepen penetration far beyond specialty crops.

Global Biological Organic Fertilizer Market Trends and Insights

Federal Incentives for Regenerative Farming

Government subsidies are significantly reducing the payback periods for growers transitioning from synthetic nitrogen to microbial alternatives. The United States Department of Agriculture committed USD 3.1 billion under its Partnerships for Climate-Smart Commodities program in 2024, covering up to 50% of biological-input transition costs . India's direct-benefit-transfer scheme extends to biofertilizers, while China's 14th Five-Year Plan requires organic amendments on 30% of degraded farmland by 2026, ensuring steady demand. These measures collectively lower growers' capital risk, insulate national food systems from volatile natural-gas-linked urea prices, and underpin consistent volume growth for the biological organic fertilizer market.

Escalating Restrictions on Synthetic Fertilizers

The European Union's Carbon Border Adjustment Mechanism, fully effective in 2024, raised the landed cost of ammonia-based inputs by up to 20% . Cadmium caps on mineral phosphorus and China's nitrogen ceilings in the Yangtze River basin are increasing compliance costs, making biological substitutes the economically rational choice. Remote-sensing audits and license revocations provide real-time enforcement, creating a decisive pull for the biological organic fertilizer market across all row-crop segments.

Short Shelf-Life in High-Temperature Climates

Microbial populations decline by up to 80% after 90 days at 35 °C, eroding field efficacy in arid markets . Limited cold-chain infrastructure and higher formulation costs for encapsulation impede accessibility for smallholder growers. String Bio's methane-derived protein carrier stabilizes microbes at 45 °C but awaits widespread regulatory clearance. Until scalable solutions emerge, this restraint trims near-term gains for the biological organic fertilizer market.

Other drivers and restraints analyzed in the detailed report include:

- Soaring Demand from Organic Packaged-Food Processors

- Rapid Adoption of Microbial Consortia Blends

- Fragmented, Country-Specific Registration Hurdles

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Rhizobium retains a 31.65% biological organic fertilizer market share in 2025, while Mycorrhiza is expanding at an 8.53% CAGR, the highest among all product categories. These blended formulations synchronize the release of multiple nutrients, enabling growers to reduce synthetic inputs without incurring yield penalties. Enhanced root colonization and drought resilience further boost demand in rain-fed systems, particularly in Brazil and the United States. Manufacturers increasingly bundle consortia with seed coatings, ensuring uniform field application and simplifying logistics for large farms. Regulatory delays, persist because each microbial component requires a separate dossier. Despite that bottleneck, rising commodity-price volatility is nudging mainstream growers toward versatile consortia, guaranteeing steady growth for this high-value niche within the biological organic fertilizer market size.

Organic-residue products meeting growers' soil organic matter targets, but face unpredictability in mineralization rates that limit precision nutrient management. Fish meal and bone meal are key raw materials for aquaculture feed markets. Green manure application benefits from subsidies in regenerative agriculture. Oil cakes remain cost-effective but suffer from variable purity in unregulated channels. The contrast in growth trajectories underscores an industry shift: advanced microbial inputs increasingly capture share from slower-acting residue products, especially in high-value export horticulture where reliable nutrient timing is paramount.

The Biological Organic Fertilizer Market Report is Segmented by Type (Microorganism and Organic Residues), Application (Grains and Cereals, Pulses and Oilseeds, Fruits and Vegetables, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

The Asia-Pacific region generated 39.78% of 2025 revenue, anchored by India's direct-benefit-transfer system and China's organic-matter mandates. Japan and Australia achieve incremental growth through export-driven horticulture, which requires certified inputs. Despite strong uptake, counterfeit products and fragmented smallholder plots complicate quality control and distribution. National Fertilizers Limited and Gujarat State Fertilizers and Chemicals Ltd. are scaling domestic microbial production, but consistency varies across state lines, creating opportunities for multinational entrants offering validated consortia.

North America and Europe jointly contribute to the current demand. The United States allocates USD 3.1 billion in grant funding to integrate biological inputs into corn and soybean systems, while Canada earmarks CAD 50 million (approximately USD 37 million) for pulse and canola projects that reduce greenhouse-gas emissions by up to 40%. The European Union's cadmium limits on mineral phosphate and carbon border tariffs further incentivize microbial substitution, although delays in member-state approval add cost and time. Grower cooperatives are increasingly negotiating collective supply agreements with leading biological manufacturers, securing volume discounts and field-support services.

The Middle East logs a robust 7.52% CAGR, the fastest worldwide, driven by the UAE's National Food Security Strategy and Saudi Arabia's SAR 10 billion (USD 2.7 billion) Vision 2030 irrigation upgrade. Biological inputs capable of tolerating saline conditions are well-suited for desalinated-water farming systems, thereby boosting adoption in controlled environments. South America, led by Brazil and Argentina, is leveraging decades of experience with soybean-based Rhizobium and new capacity expansions by regional producers, such as Rizobacter Argentina. Donor-funded pilot programs drive Africa's growth, although gaps in the cold chain and training deficits limit its near-term potential. Collectively, regional momentum reinforces the global resilience of the biological organic fertilizer market, diversifying its growth engines across both developed and emerging economies.

- Novonesis A/S

- Rizobacter Argentina S.A.

- Lallemand Inc.

- Premier Tech

- Symborg (Corteva Agriscience)

- National Fertilizers Limited

- Madras Fertilizers Limited

- T Stanes and Company Limited

- Gujarat State Fertilizers and Chemicals Ltd

- String Bio

- Rashtriya Chemicals and Fertilizers Ltd

- Agrinos

- Biomax Naturals

- Agri Life

- Biofosfatos do Brasil

- Kiwa Bio-Tech Products Group Corporation

- Protan AG

- Mapleton Agri Biotech Pty Limited

- Bio Nature Technology PTE Ltd.

- Kribhco

- Bio Ark Pte Ltd

- Savio BIO Organic and Fertilizers Private Limited

- ACI Biolife

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Federal incentives for regenerative farming

- 4.2.2 Escalating restrictions on synthetic fertilizers

- 4.2.3 Soaring demand from organic packaged-food processors

- 4.2.4 Rapid adoption of microbial consortia blends

- 4.2.5 Carbon-credit monetization for soil microbiome improvement

- 4.2.6 Biostimulant-biofertilizer co-formulation patents accelerating trials

- 4.3 Market Restraints

- 4.3.1 Short shelf-life in high-temperature climates

- 4.3.2 Fragmented, country-specific registration hurdles

- 4.3.3 Low farmer awareness outside specialty crops

- 4.3.4 Uncertainty around carbon-credit pricing models

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Microorganism

- 5.1.1.1 Rhizobium

- 5.1.1.2 Azotobacter

- 5.1.1.3 Azospirillum

- 5.1.1.4 Blue-green Algae

- 5.1.1.5 Phosphate Solubilizing Bacteria

- 5.1.1.6 Mycorrhiza

- 5.1.1.7 Other Microorganisms

- 5.1.2 Organic Residues

- 5.1.2.1 Green Manure

- 5.1.2.2 Fish Meal

- 5.1.2.3 Bone Meal

- 5.1.2.4 Oil Cakes

- 5.1.2.5 Others

- 5.1.1 Microorganism

- 5.2 By Application

- 5.2.1 Grains and Cereals

- 5.2.2 Pulses and Oilseeds

- 5.2.3 Fruits and Vegetables

- 5.2.4 Commercial Crops

- 5.2.5 Turf and Ornamentals

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Spain

- 5.3.2.5 Italy

- 5.3.2.6 Russia

- 5.3.2.7 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Rest of Middle East

- 5.3.6 Africa

- 5.3.6.1 South Africa

- 5.3.6.2 Nigeria

- 5.3.6.3 Rest of Africa

- 5.3.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Novonesis A/S

- 6.4.2 Rizobacter Argentina S.A.

- 6.4.3 Lallemand Inc.

- 6.4.4 Premier Tech

- 6.4.5 Symborg (Corteva Agriscience)

- 6.4.6 National Fertilizers Limited

- 6.4.7 Madras Fertilizers Limited

- 6.4.8 T Stanes and Company Limited

- 6.4.9 Gujarat State Fertilizers and Chemicals Ltd

- 6.4.10 String Bio

- 6.4.11 Rashtriya Chemicals and Fertilizers Ltd

- 6.4.12 Agrinos

- 6.4.13 Biomax Naturals

- 6.4.14 Agri Life

- 6.4.15 Biofosfatos do Brasil

- 6.4.16 Kiwa Bio-Tech Products Group Corporation

- 6.4.17 Protan AG

- 6.4.18 Mapleton Agri Biotech Pty Limited

- 6.4.19 Bio Nature Technology PTE Ltd.

- 6.4.20 Kribhco

- 6.4.21 Bio Ark Pte Ltd

- 6.4.22 Savio BIO Organic and Fertilizers Private Limited

- 6.4.23 ACI Biolife

7 Market Opportunities and Future Outlook

生物肥料:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

生物肥料:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 2026年全球根瘤菌肥料市场报告

2026年全球根瘤菌肥料市场报告 根瘤菌接种剂市场按作物类型、形态、应用方法、最终用途和销售管道划分-2026-2032年全球预测根际微生物市场按产品类型、作用方式、作物类型、配方、应用和最终用户划分-2026-2032年全球预测植物生长促进根际细菌市场(按微生物类型、作物类型、配方和应用方法划分)—全球预测(2026-2032 年)海藻生物肥料市场按作物类型、产品类型、应用方法、用途和通路划分-2026-2032年全球预测中东和非洲生物肥料市场份额分析、行业趋势、统计数据和成长预测(2026-2031 年)

根瘤菌接种剂市场按作物类型、形态、应用方法、最终用途和销售管道划分-2026-2032年全球预测根际微生物市场按产品类型、作用方式、作物类型、配方、应用和最终用户划分-2026-2032年全球预测植物生长促进根际细菌市场(按微生物类型、作物类型、配方和应用方法划分)—全球预测(2026-2032 年)海藻生物肥料市场按作物类型、产品类型、应用方法、用途和通路划分-2026-2032年全球预测中东和非洲生物肥料市场份额分析、行业趋势、统计数据和成长预测(2026-2031 年) 生物肥料市场-全球产业规模、份额、趋势、机会和预测,按类型、形态、作物类型、应用、微生物类型、地区和竞争格局划分,2020-2030年预测基于固氮菌的生物肥料市场—按产品类型、作物类型、应用方法、分销管道、最终用户和配方类型划分—2025-2032年全球预测生物肥料市场按类型、形态、应用方法、作物类型和分销管道划分-2025-2032年全球预测

生物肥料市场-全球产业规模、份额、趋势、机会和预测,按类型、形态、作物类型、应用、微生物类型、地区和竞争格局划分,2020-2030年预测基于固氮菌的生物肥料市场—按产品类型、作物类型、应用方法、分销管道、最终用户和配方类型划分—2025-2032年全球预测生物肥料市场按类型、形态、应用方法、作物类型和分销管道划分-2025-2032年全球预测