|

市场调查报告书

商品编码

1685783

北美塑胶瓶盖和封口:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)North America Plastic Caps And Closures - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

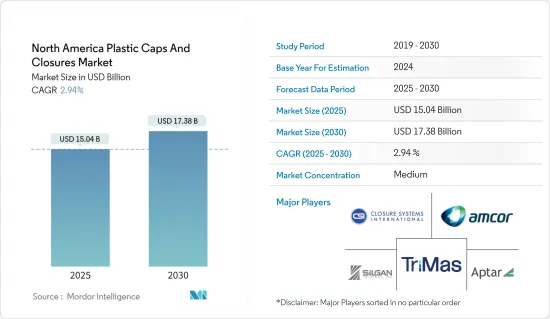

北美塑胶瓶盖和封口市场规模预计在 2025 年为 150.4 亿美元,预计到 2030 年将达到 173.8 亿美元,预测期内(2025-2030 年)的复合年增长率为 2.94%。

从产量来看,预计将从 2025 年的 3,982.5 亿件成长到 2030 年的 4,759.7 亿件,预测期内(2025-2030 年)的复合年增长率为 3.63%。

塑胶瓶盖和封盖可密封各种容器,确保其安全性和完整性。它们由坚韧耐用的聚合物製成,例如聚丙烯 (PP) 和聚乙烯 (PE)。塑胶瓶盖和封口通常用于包装食品和饮料 (F&B)、药品、化妆品、家用清洗产品等。

主要亮点

- 瓶盖和封盖主要由 PP 和 PE 製成。各行各业都严重依赖塑胶瓶盖和封口作为一种经济高效的密封解决方案。热感应瓶盖衬垫用于由多种塑胶材料製成的瓶子,包括 PP、HDPE 和 LDPE,以保护容器免于洩漏并提供防篡改证明。因此,预计预测期内市场将会成长。

- 随着对瓶装水和非酒精饮料的需求不断增加,饮料行业的塑胶瓶市场预计将扩大,从而推动对塑胶瓶盖和封盖的需求。瓶装水的需求是由消费者对高品质饮用水的趋势所驱动,特别是对饮用受污染的自来水后感染疾病的担忧,以及瓶装水的便利性和便携性。

- 瓶盖和封口是饮料包装的重要组成部分,可确保消费者收到优质的饮料。它确保产品的安全和质量,同时提供紧密的密封,方便最终用户打开和关闭。由于塑胶包装技术的进步,饮料瓶盖和封口产业的产品开发和创新正在激增。许多公司投入大量资源进行研发,以打造独特而经济的产品,从而推动该领域的创新快速成长。

- 对于包装来说,回收和环保至关重要。包装废弃物严重造成了海洋和垃圾掩埋场的塑胶污染。塑胶包装也是环境塑胶污染的重要来源之一。塑胶需要数百年才能分解,可能会影响海洋生物和生态系统。

- 一次性包装会被丢弃或回收,而不是重新使用。根据美国环保署 (EPA) 的数据,大约一半的城市固态废弃物由食物和食品包装材料组成。塑胶包装的问题在于它需要数年时间才能自然分解,导致塑胶污染我们的海洋、河流和湖泊,并散落在街道上。

- 塑胶製造业依赖原油和天然气等原料的成本和供应。这些价格波动会影响产业的盈利和永续性。石油是多种包装材料使用的原料。因此,如果需求激增、供应链出现问题或价格上涨,包装製造商将面临挑战。

北美塑胶瓶盖和封盖市场趋势

饮料将成为最大的终端用户产业

- 瓶装水因其方便性而成为最常消费的饮料之一。瓶装水包装也适合远距运输,这就是为什么瓶装水包装如此广泛的原因。

- 根据国际瓶装水协会(IBWA)和饮料行销公司(BMC)的统计,美国人饮用的瓶装水比其他饮料都多。健康意识、生活水准的提高以及瓶装水的需求和消费的增加是推动北美瓶装水需求的主要因素,从而推动全部区域对瓶装水包装的需求。预计这将推动瓶装水塑胶瓶盖和瓶塞的需求。

- 推动水瓶和容器需求的主要因素是消费者对健康和天然产品的兴趣。塑胶被广泛用作水包装材料,进一步推动了该地区瓶盖和封口市场的发展。

- 根据丹麦的一项研究,加拿大人平均每天消耗 335 公升水,相当于 670 个标准水瓶(500 毫升)。

- 该行业的製造商正致力于推出新产品作为业务扩展的一部分。例如,2024 年 5 月,AlpekPolyester USA LLC 在 NPE2024 上发布了一种用于瓶盖的新型 PET 树脂。该材料将以“CAPETall”品牌出售,并将满足您所有瓶盖生产需求。该材料预计将于2025年上市。该公司还表示,CaPETall 是100% PET 产品,可改善消费后宝特瓶回收和 PET 循环经济。

- 2024年3月,Beyond Plastic宣布首批生物分解性宝特瓶瓶盖之一进入市场。瓶盖由聚羟基烷酯(PHA) 製成,这是一种透过细菌发酵产生的生物聚合物。新型环保瓶盖看起来与传统的石油基塑胶瓶盖相同,但具有可回收、可堆肥和在敏感条件下生物分解等创新优势。这种瓶盖已在美国推出,可用于瓶装水和其他行业。

预计美国将出现显着成长

- 化妆品瓶盖由于其卫生、使用方便、分配性能好以及能够为香水和乳霜等产品带来整体外观的能力而在美国广受欢迎。此外,各包装公司均致力于生产符合永续包装标准的瓶盖和封口,例如新材料和轻量化特性。

- 根据美国人口普查局的数据,到2023年,美国食品和饮料年度零售额将达到约9,853亿美元,而2017年为7,288亿美元。随着饮料消费量的消费量,尤其是瓶装水、软性饮料、果汁和酒精饮料,该国对饮料包装解决方案的需求也相应增加。

- 消费者对改善外观和保持个人卫生的兴趣日益浓厚,加之提供价格更实惠的高檔化妆品的公司不断增多,推动了消费者在化妆品和个人保健产品上的支出增加。

- 据电子商务成长机构 CommonThreads 称,美国化妆品和个人护理行业规模到 2023 年将达到 900 亿美元。

- 由于美国化妆品和个人护理行业的扩张,该国对包括瓶盖和封口在内的初级包装的需求正在增长,从而促进了所研究市场在数量和金额方面的整体增长。

- 随着瓶装水作为更有益于健康的产品以及随时随地的补水需求的增加,美国瓶装水市场近年来达到了新的高度,预计未来几年还将继续增长。

- 因此,预计未来几年该国的产量将大幅增长,从而导致对瓶盖的以金额为准需求增加。

北美塑胶瓶盖和封盖产业概况

北美塑胶瓶盖和封口市场半固体,主要企业包括 Silgan Holdings Inc.、Amcor PLC、Closure Systems International Inc.、AptarGroup Inc. 和 TriMas Corporation。市场参与者正在采用联盟、收购等各种策略来增强其产品供应并获得永续的竞争优势。

- 2024 年 5 月,Aptar Closures 推出了适用于美容、个人和家庭护理应用的新型电子商务桌面封口机。 Aptar Closures 的 E-Disc Top 可确保运输过程中不会发生洩漏,并且无需使用衬垫,也无需承担额外的运输准备费用。

- 2023 年 12 月,TriMas 集团的包装部门 Affaba &Ferrari 宣布与欧洲食品和饮料市场的客户合作。该公司扩大了其产品组合,增加了与传统封盖设计相比更具永续的新型创新繫绳盖产品。该公司最新推出的产品是专为可口可乐设计的 38 毫米运动饮料盖,计划于 2024 年推出。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概况

- 产业价值链分析

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 地缘政治情势如何影响市场

第五章 市场动态

- 市场驱动因素

- 瓶装饮料需求推动塑胶瓶盖和封口的需求

- 各类最终用户对创新解决方案的需求不断增加

- 市场限制

- 对製造商在环境恶化方面的监管更加严格

- 立式袋包装的轻巧、经济高效的替代品

第六章 市场细分

- 按材质

- 聚乙烯 (PE)

- 聚对苯二甲酸乙二醇酯(PET)

- 聚丙烯(PP)

- 其他材料

- 按类型

- 螺桿式

- 自动贩卖机

- 无螺丝

- 儿童安全

- 按最终用户产业

- 饮料

- 瓶装水

- 软性饮料

- 烈酒

- 其他饮料

- 食物

- 製药和医疗保健

- 化妆品和盥洗用品

- 家用化学品(清洁剂、清洁剂、肥皂、抛光粉)

- 其他最终用户产业

- 饮料

- 按国家

- 美国

- 加拿大

第七章 竞争格局

- 公司简介

- Silgan Holdings Inc.

- Amcor PLC

- Closure Systems International Inc.

- AptarGroup Inc.

- TriMas Corporation

- Guala Closures SpA

- Berry Global Inc.

- Tetra Pak Group

- O.Berk Company LLC

- BERICAP Holding GmbH

- Pano Cap Canada Ltd

- Erie Molded Plastics Inc.

第八章投资分析

第九章:未来市场展望

The North America Plastic Caps And Closures Market size is estimated at USD 15.04 billion in 2025, and is expected to reach USD 17.38 billion by 2030, at a CAGR of 2.94% during the forecast period (2025-2030). In terms of production volume, the market is expected to grow from 398.25 billion units in 2025 to 475.97 billion units by 2030, at a CAGR of 3.63% during the forecast period (2025-2030).

Plastic caps and closures seal various containers to ensure their safety and integrity. They are made from strong, durable polymers, including polypropylene (PP) and polyethylene (PE). Plastic caps and closures are commonly used for packaging food and beverages (F&B), pharmaceuticals, cosmetics, and household cleaning products.

Key Highlights

- Caps and closures use PP and PE as the primary raw materials for manufacturing. Various industries rely heavily on plastic caps and closures for a cost-effective sealing solution. A heat induction cap liner could be used on bottles made of different plastic materials, such as PP, HDPE, and LDPE, to protect the container from leakage and provide tamper evidence characteristics to it. Due to this, the market is expected to witness growth during the forecast period.

- With the rising demand for bottled water and non-alcoholic beverages, the market for plastic bottles in the beverage industry is expected to expand, bolstering the demand for plastic caps and closures. The demand for bottled water is attributed to the predisposition of customers to want high-quality drinking water, specifically, their concern about contracting diseases after drinking tainted tap water and the convenience and portability of bottled water.

- Caps and closures comprise a significant part of beverage packaging, ensuring the delivery of top-notch beverages to consumers. They have seals that guarantee product safety and quality while allowing effortless opening and reclosing for end-users. The beverage caps and closure industry has seen a surge in product development and innovations due to technological advancements in plastic packaging. Numerous companies are dedicating substantial resources to research and development efforts to create distinctive and economical products, leading to a rapid increase in innovations within this sector.

- Recycling and environmental considerations are essential when it comes to packaging. Packaging trash significantly impacts plastic contamination in the oceans and landfills. Plastic packaging is also a significant cause of the environment's plastic pollution. Plastic can affect marine life and ecosystems since it takes hundreds of years to disintegrate.

- Single-use packaging is either thrown away or recycled instead of reused. According to the US Environmental Protection Agency (EPA), about half of all municipal solid waste comprises food and materials used in food packaging. The issue with plastic packaging is that its natural degradation can take many years, which leads to plastic polluting the oceans, rivers, and lakes and littering the streets.

- The plastic manufacturing industry depends on the cost and availability of raw materials like crude oil and natural gas. Any changes in these prices can have an impact on the industry's profitability and sustainability. Oil is the raw material used in a wide range of packaging materials. Hence, when there is an upsurge in demand, a problem with the supply chain or increased prices is where packaging manufacturers will face difficulties.

North America Plastic Caps And Closures Market Trends

Beverages to be the Largest End-user Industry

- Bottled water is one of the most consumed beverages due to its convenience. The packaging of bottled water makes it also suitable for long-distance transportation, and the packaging of bottled water is widespread.

- According to the International Bottled Water Association (IBWA) and the Beverage Marketing Corporation (BMC), Americans drink bottled water more than any other beverage. Health awareness, a higher standard of living, and rising demand and consumption of bottled water are major factors pushing the demand for bottled water in North America, consequently driving the demand for bottled water packaging across the region. This is expected to drive the demand for plastic caps and closures for bottled water.

- The major factor driving the demand for bottles and containers for water is consumers' interest in healthy and natural products. Plastic is a widely used packaging material for water, which further leverages the caps and closures market in the region.

- According to a study by Danamark, on average, a typical person in Canada consumes 335 liters of water daily, which is the equivalent of 670 standard water bottles (500 ml size).

- Manufacturers operating in the industry are focused on launching new products as part of their business expansion. For instance, in May 2024, AlpekPolyester USA LLC introduced a new PET resin for bottle caps at NPE2024. This material is marketed under the brand CAPETall, and it meets all the production needs of bottle caps. The material is expected to be available in 2025. The company also stated that CaPETall is a 100% PET product that improves post-consumer PET bottle recycling and the PET circular economy.

- In March 2024, Beyond Plastic introduced one of the first biodegradable plastic bottle caps to enter the market. The closure is made from polyhydroxyalkanoate (PHA), a biopolymer created using bacteria fermentation. The new, eco-friendly cap looks just like traditional petroleum-based plastic caps but brings transformative advantages such as being recyclable, compostable, and biodegradable, even in sensitive conditions. Such caps launched in the country can be used for bottled water and in other industries.

The United States is Expected to Witness Significant Growth

- Closures for cosmetics are also gaining traction in the United States due to their hygienic qualities, ease of use, dispensing characteristics, and ability to provide a cohesive look to products such as fragrances and face creams. Various packaging companies also emphasize manufacturing caps and closures that meet sustainable packaging criteria, including new materials and lightweight nature.

- According to the US Census Bureau, the annual sales of US retail food and beverage stores reached approximately USD 985.3 billion in 2023, compared to USD 728.8 billion in 2017. As beverage consumption increases, particularly bottled water, soft drinks, juices, and alcoholic beverages, the demand for beverage packaging solutions in the country rises correspondingly.

- The rising focus of consumers on enhancing physical appearance and maintaining personal hygiene, along with the rise of companies offering more affordable versions of high-end cosmetic products, has increased consumer spending on cosmetics and personal care products.

- According to Common Thread Co., an e-commerce growth agency, the US cosmetics and personal care industry reached USD 90 billion in 2023.

- In response to the expansion of the cosmetics and personal care industry in the United States, the demand for primary packaging, including caps and closures, is growing in the country, thus contributing to the overall growth of the market studied in terms of volume and value.

- Due to the growing demand for bottled water as a better-for-you product and for on-the-go hydration, the bottled water market in the United States has reached new heights in recent years, and it is expected to witness growth in the upcoming years.

- In response, production is expected to boom in the country in the upcoming years, which, in turn, is expected to bolster the demand for bottle caps in terms of value.

North America Plastic Caps And Closures Industry Overview

The North American plastic caps and closures market is semi-consolidated with the presence of key players like Silgan Holdings Inc., Amcor PLC, Closure Systems International Inc., AptarGroup Inc., and TriMas Corporation. Players in the market are adopting various strategies, such as partnerships and acquisitions, to enhance their product offerings and gain sustainable competitive advantage.

- In May 2024, Aptar Closures introduced a new e-commerce Disc Top Closure for beauty, personal, and home care applications. Aptar Closures' E-Disc Top securely protects against in-transit leakage while eliminating the need for liners and extra shipping preparation fees.

- In December 2023, TriMas Corporation's packaging division, Affaba & Ferrari, announced its collaboration with customers in the European food and beverage market. The company expanded its portfolio by adding new and innovative products for tethered caps that are sustainable compared to traditional closure designs. The company's latest addition to the lineup included a 38 mm sports drink cap designed for Coca-Cola, which is scheduled to be launched in 2024.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Impact of Geopolitical Scenarios on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Demand for Bottled Beverages Drive the Demand for Plastic Caps and Closures

- 5.1.2 Increased Demand for Innovative Solutions from Different End Users

- 5.2 Market Restraints

- 5.2.1 Stringent Regulations on Manufacturers Pertaining to Environmental Degradation

- 5.2.2 Lightweight and Cost-effective Stand-up Pouch Packaging Alternatives

6 MARKET SEGMENTATION

- 6.1 By Material

- 6.1.1 Polyethylene (PE)

- 6.1.2 Polyethylene Terephthalate (PET)

- 6.1.3 Polypropylene (PP)

- 6.1.4 Other Types of Materials

- 6.2 By Type

- 6.2.1 Threaded

- 6.2.2 Dispensing

- 6.2.3 Unthreaded

- 6.2.4 Child-resistant

- 6.3 By End-user Industry

- 6.3.1 Beverage

- 6.3.1.1 Bottled Water

- 6.3.1.2 Soft Drinks

- 6.3.1.3 Spirits

- 6.3.1.4 Other Beverages

- 6.3.2 Food

- 6.3.3 Pharmaceutical and Healthcare

- 6.3.4 Cosmetics and Toiletries

- 6.3.5 Household Chemicals (Detergents, Cleaners, Soaps, and Polishes)

- 6.3.6 Other End-user Industries

- 6.3.1 Beverage

- 6.4 By Country

- 6.4.1 United States

- 6.4.2 Canada

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Silgan Holdings Inc.

- 7.1.2 Amcor PLC

- 7.1.3 Closure Systems International Inc.

- 7.1.4 AptarGroup Inc.

- 7.1.5 TriMas Corporation

- 7.1.6 Guala Closures SpA

- 7.1.7 Berry Global Inc.

- 7.1.8 Tetra Pak Group

- 7.1.9 O.Berk Company LLC

- 7.1.10 BERICAP Holding GmbH

- 7.1.11 Pano Cap Canada Ltd

- 7.1.12 Erie Molded Plastics Inc.

8 INVESTMENT ANALYSIS

9 FUTURE OUTLOOK OF THE MARKET

塑胶瓶盖和封盖:全球市场份额和排名、总销售额和需求预测(2025-2031 年)

塑胶瓶盖和封盖:全球市场份额和排名、总销售额和需求预测(2025-2031 年) 塑胶瓶盖和封口市场(按产品类型、材料、最终用途和分销管道)—2025-2032 年全球预测

塑胶瓶盖和封口市场(按产品类型、材料、最终用途和分销管道)—2025-2032 年全球预测 2025年全球塑胶瓶盖和封口市场报告

2025年全球塑胶瓶盖和封口市场报告 2032年塑胶瓶盖和封口市场预测:依产品类型、原料、製造流程、应用和地区分析

2032年塑胶瓶盖和封口市场预测:依产品类型、原料、製造流程、应用和地区分析 塑胶瓶盖和封盖:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)美国塑胶瓶盖和封口:市场占有率分析、行业趋势和成长预测(2025-2030)

塑胶瓶盖和封盖:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)美国塑胶瓶盖和封口:市场占有率分析、行业趋势和成长预测(2025-2030) 2025 年至 2033 年塑胶瓶盖和封口市场报告(按产品类型、原料、容器类型、技术、最终用途和地区划分)

2025 年至 2033 年塑胶瓶盖和封口市场报告(按产品类型、原料、容器类型、技术、最终用途和地区划分) 塑胶瓶盖和封口市场规模、份额、按瓶盖类型、材料类型、容器类型、技术、最终用途产业和地区分類的成长分析 - 2025-2032 年产业预测中东和非洲塑胶盖子与封口装置-市场占有率分析、产业趋势、统计、成长趋势预测(2025-2030)中国塑胶瓶盖和封口:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)

塑胶瓶盖和封口市场规模、份额、按瓶盖类型、材料类型、容器类型、技术、最终用途产业和地区分類的成长分析 - 2025-2032 年产业预测中东和非洲塑胶盖子与封口装置-市场占有率分析、产业趋势、统计、成长趋势预测(2025-2030)中国塑胶瓶盖和封口:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)