|

市场调查报告书

商品编码

1939009

3D动作捕捉:市占率分析、产业趋势与统计、成长预测(2026-2031年)3D Motion Capture - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

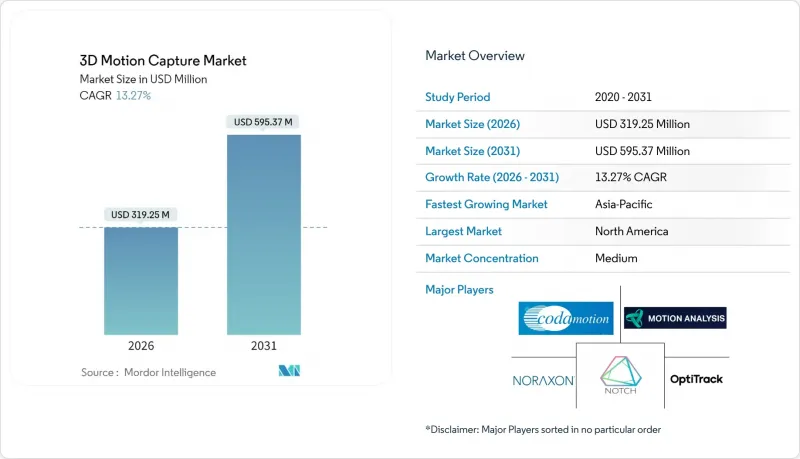

预计 3D 动作捕捉市场将从 2025 年的 2.8185 亿美元成长到 2026 年的 3.1925 亿美元,到 2031 年将达到 5.9537 亿美元,2026 年至 2031 年的复合年增长率为 13.27%。

这一成长表明,3D动作捕捉市场正持续从小众娱乐应用领域转型为医疗保健、体育分析和工业自动化等领域的广泛应用。边缘设备上更快的AI推理速度、不断下降的相机成本以及更精准的无标记演算法正在扩大基本客群。随着工作室和诊所对更高影格速率的需求,硬体更新换代週期依然活跃。同时,基于订阅的软体模式使小规模团队能够以较低的前期成本使用高级功能。随着现有企业专注于无标记产品,而新参与企业则透过整合云端边缘工作流程来脱颖而出,市场竞争日益激烈。

全球3D动作捕捉市场趋势与洞察

无标记运动捕捉技术在远距復健和远距物理治疗的快速应用

医疗机构越来越依赖基于摄影机的系统,这些系统能够以小于10°的平均绝对误差测量关节角度,并将数据安全地传输给临床医生。这种方法减少了患者的出行,缩短了治疗週期,并有助于追踪客观的治疗效果。随着远端动作捕捉评估被纳入健保报销范围,支付方的覆盖范围也不断扩大。供应商也积极回应,推出了简化的校准流程,使治疗师能够在狭小的空间内设置单一摄影机套件。随着临床有效性的不断检验,无标记动作捕捉技术正在为新兴的数位医疗服务提供支持,并加速3D动作捕捉市场的发展势头。

在媒体和娱乐製作流程中日益普及

工作室正将动作捕捉技术与LED幕墙和游戏引擎渲染相结合,在拍摄过程中可视化最终场景,从而减少40%的后製工作。 Vicon进军无标记技术领域,凸显了这一转变,因为传统的光学专家正努力保护其收入来源。其为虚幻引擎开发的即时插件,使动画团队能够即时迭代镜头设计,缩短回馈週期。成本的下降正在加速多角色体积技术的应用,而这项技术过去需要巨额预算才能实现,如今独立电影製作人和虚拟製作公司也纷纷采用。由此带来的生产力提升,持续推动3D动作捕捉市场维持强劲成长动能。

高精准度3D动作捕捉生态系的前期投入成本很高

专业光学系统通常售价超过10万美元,这限制了其普及,只有财力雄厚的摄影棚、研究实验室和顶级运动队伍才能负担得起。即使是穿戴式惯性套件,硬体起价约为4,590美元,永久授权软体起价约为3,790美元。订阅模式和低成本的单摄影机解决方案降低了准入门槛,但并不能完全消除小规模营运商的资金障碍。除非价格进一步下降或资金筹措管道更加畅通,否则高昂的进入成本可能会限制3D动作捕捉市场某些细分领域的普及。

细分市场分析

到2025年,硬体将占3D动作捕捉市场46.10%的份额,凸显了摄影机、深度感测器和惯性测量单元在所有安装应用中的重要性。影格速率、解析度和装置内AI处理的持续改进推动了更新换代。该领域也受惠于跨产业需求,涵盖娱乐、医疗保健等多个领域。服务领域虽然规模较小,但预计将以15.06%的复合年增长率成长,这主要得益于用户倾向于将校准、维护和分析外包。软体收入介于两者之间,这得益于定期更新、云端部署以及与内容製作流程的紧密整合。

随着硬体效能的提升,工作室为了保持竞争力,不得不升级设备,而新参与企业则将NVIDIA Jetson等人工智慧加速器直接嵌入感测器模组。服务成长与市场成熟同步,客户越来越重视能够节省时间的专业技术。云端原生软体即服务(SaaS)使小规模的团队能够在投入资金之前测试无标记工作流程,从而扩大了3D动作捕捉市场的用户群。

到2025年,光学平台将占据3D动作捕捉市场62.90%的份额。目前,电影公司仍依赖多机位拍摄来捕捉高预算电影的表演,精确度可达亚毫米级。研究机构和精英运动项目也倾向于使用光学钻机进行详细的动态研究。同时,以惯性穿戴装置为代表的非光学系统,由于其便携性和易于安装的特点,预计将以14.28%的复合年增长率增长,使其适用于现场训练和远端医疗。

混合架构融合了光学和惯性技术,兼具两者的优势:绝对的精度和不受遮蔽的影响。供应商提供跨多个感测器流的同步时间戳,误差小于150微秒,从而实现无缝资料融合。这种融合正在拓展3D运动捕捉市场的应用范围,使其能够应用于纯光学或惯性解决方案无法胜任的领域。

区域分析

预计到2025年,北美将占据39.95%的收入份额,这主要得益于好莱坞製片厂、大学体育项目以及远距远端医疗的蓬勃发展。创业投资资金以及完善的中间件供应商生态系统,为早期原型製作和大规模部署提供了支援。该地区受益于清晰的FDA核准途径,降低了医疗应用监管的不确定性。此外,各公司也正在投资身临其境型培训和虚拟製作,进一步巩固了主导地位。

预计亚太地区在2026年至2031年间将以15.62%的复合年增长率成长。 NAVER D2SF对韩国Start-UpsMOVIN的投资等资本注入,反映出市场对该地区日益增长的兴趣。诸如2024年欧洲杯等大型体育赛事展示了先进的分析流程,推动了国内联赛采用类似工具。製造业基础设施的完善降低了硬体成本,促进了娱乐、机器人和医疗保健等行业的快速部署。政府对工业数位化的支持进一步拓展了3D动作捕捉市场的机会。

欧洲正透过整合研究主导创新和公共卫生,稳步推进相关工作。诸如瑞典皇家理工学院(KTH)等机构的计划正在展示符合严格隐私法的先进摄影机復健工具。 GDPR正在塑造以边缘运算为中心的架构,使提供本地分析服务的供应商受益。中东、非洲和拉丁美洲的需求正在涌现,尤其是在运动表现和远端医疗领域。在远端医疗领域,动作捕捉技术正在帮助缓解医疗人员短缺的问题。随着设备价格的下降,预计这些地区将对3D动作捕捉市场产生新的需求。

其他福利:

- Excel格式的市场预测(ME)表

- 分析师支持(3个月)

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 不断创造更逼真的虚拟实境体验

- 电脑视觉在职业运动分析的应用日益广泛

- 在媒体和娱乐製作流程中日益普及

- 与人工智慧驱动的数位人体建模集成,以实现符合人体工学的兼容性

- 无标记运动捕捉技术在远距復健和远距物理治疗的快速应用

- 对用于训练自主机器人的高精度运动资料集的需求

- 市场限制

- 高精准度3D动作捕捉生态系的初始准入成本很高

- 大型动态影像库中内容拥有者的智慧财产权和隐私权问题

- 缺乏开放的交换标准限制了跨平台工作流程。

- 高速影像感测器和惯性测量单元供应链的变异性

- 产业价值链分析

- 监管环境

- 技术展望

- 宏观经济因素如何影响市场

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 按类型

- 硬体

- 相机

- 感应器

- 配件

- 软体

- 服务

- 硬体

- 按系统

- 光学3D运动捕捉系统

- 主动光学

- 被动光学

- 非光学3D运动捕捉系统

- 惯性

- 电磁学

- 马达驱动

- 光学3D运动捕捉系统

- 透过捕获技术

- 标记底座

- 无标记

- 透过使用

- 动态研究与医学

- 媒体与娱乐

- 工程与工业

- 教育

- 其他用途

- 透过部署模式

- 本地部署

- 基于云端的

- 按地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 欧洲

- 德国

- 法国

- 英国

- 义大利

- 西班牙

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 澳洲

- 亚太其他地区

- 中东和非洲

- 中东

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 埃及

- 奈及利亚

- 其他非洲地区

- 中东

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Vicon Motion Systems Ltd.

- Leyard Optoelectronic Co. Ltd.(NaturalPoint Inc./OptiTrack)

- Motion Analysis Corporation

- Qualisys AB

- Xsens Technologies BV

- Codamotion-Charnwood Dynamics Ltd.

- Noraxon USA Inc.

- PhaseSpace Inc.

- Phoenix Technologies Inc.

- AIQ Synertial Ltd.

- Notch Interfaces Inc.

- Perception Neuron-Noitom Ltd.

- Rokoko Electronics ApS

- STT Systems SL

- Simi Reality Motion Systems GmbH

- Animazoo-Synertial Limited

- QualiSense Motion Inc.

- Perception Digital Ltd.

- Organic Motion Inc.

- AI-Driven Solesense Corp.

第七章 市场机会与未来展望

The 3D motion capture market is expected to grow from USD 281.85 million in 2025 to USD 319.25 million in 2026 and is forecast to reach USD 595.37 million by 2031 at 13.27% CAGR over 2026-2031.

This growth underscores how the 3D motion capture market is continuing to shift from niche entertainment use to wider adoption in healthcare, sports analytics, and industrial automation. Faster artificial intelligence inference on edge devices, falling camera costs, and more accurate marker-less algorithms are broadening the customer base. Hardware refresh cycles remain brisk as studios and clinics seek higher frame rates, while subscription-based software models enable smaller teams to access premium features without incurring large upfront costs. Competitive intensity is increasing as incumbents pivot toward marker-less offerings and new entrants differentiate through integrated cloud-edge workflows.

Global 3D Motion Capture Market Trends and Insights

Rapid Uptake of Marker-Less MoCap in Tele-Rehabilitation and Remote Physiotherapy

Healthcare providers are increasingly relying on camera-based systems that report joint angles with a mean absolute error of below 10° and stream data securely to clinicians. The approach reduces travel burdens for patients, shortens therapy cycles, and supports objective outcome tracking. Reimbursement frameworks now recognize remote motion capture assessments, expanding payer coverage. Vendors respond with simplified calibration flows that let therapists install single-camera kits in smaller spaces. As clinical validation broadens, marker-less motion capture underpins new digital health services, fueling momentum in the 3D motion capture market.

Growing Adoption in Media and Entertainment Production Pipelines

Studios combine motion capture with LED walls and game-engine rendering to visualize final scenes during filming, cutting post-production labor by 40%. Vicon's entry into marker-less technology validates the shift as legacy optical specialists seek to protect revenue streams. Real-time plugins for Unreal Engine allow animation teams to iterate shot design live, shrinking feedback loops. Cost declines encourage indie filmmakers and virtual production agencies to adopt multi-actor volumes that once required blockbuster budgets. The resulting productivity gains keep the 3D motion capture market on a strong expansion track.

High Upfront Cost of Precision 3D MoCap Ecosystems

Professional optical installations often exceed USD 100,000, restricting adoption to well-funded studios, labs, and elite sports franchises. Even body-worn inertial kits start around USD 4,590 for hardware and USD 3,790 for perpetual software licenses. Subscription models and low-cost single-camera offerings lower barriers but do not fully remove capital hurdles for small agencies. Until price points fall further or financing options expand, elevated acquisition costs will temper the pace of adoption for certain customer segments inside the 3D motion capture market.

Other drivers and restraints analyzed in the detailed report include:

- Rise in Creation of More Realistic Virtual Reality Experiences

- Demand for High-Fidelity Motion Datasets to Train Autonomous Robots

- Supply-Chain Volatility for High-Speed Image Sensors and IMUs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hardware accounted for 46.10% of the 3D motion capture market in 2025, underscoring the importance of cameras, depth sensors, and inertial units in every installation. Continuous improvements in frame rate, resolution, and on-device AI processing stimulate replacement cycles. This segment also benefits from cross-industry demand that spans entertainment and healthcare. Services, while smaller, are forecast to post a 15.06% CAGR as users outsource calibration, maintenance, and analytics. Software revenue sits between the two, lifted by regular updates, cloud deployment, and tight integration with content pipelines.

Rising hardware performance prompts studios to refresh their rigs to stay competitive, and new entrants bundle AI accelerators, such as NVIDIA Jetson, directly into sensor modules. Services growth aligns with market maturation, where customers value time-saving expertise. Cloud-native software-as-a-service lets small teams test marker-less workflows before committing capital, broadening the 3D motion capture market user base.

Optical platforms held 62.90% share of the 3D motion capture market size in 2025. Studios still rely on multi-camera volumes to capture high-budget cinematic performances at sub-millimeter accuracy. Research labs and elite sports programs also favor optical rigs for detailed biomechanical studies. In parallel, non-optical systems led by inertial wearables are expected to grow 14.28% CAGR, thanks to portability and easy setup that suit field training and tele-health.

Hybrid architectures mix optical and inertial technologies to combine the best of both worlds: absolute accuracy and freedom from occlusion. Suppliers offer synchronized time-stamping across sensor streams under 150 microseconds, enabling seamless data fusion. This convergence expands the 3D motion capture market footprint into environments where pure optical or pure inertial solutions fall short.

The 3D Motion Capture Market Report is Segmented by Type (Hardware, Software, and Services), System (Optical 3D MoCap Systems, and Non-Optical 3D MoCap Systems), Capture Technology (Marker-Based, and Marker-Less), Application (Biomechanical Research and Medical, Media and Entertainment, and More), Deployment Mode (On-Premise, and Cloud-Based), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America held 39.95% revenue share in 2025, anchored by Hollywood studios, collegiate sports programs, and robust tele-health adoption. Venture funding, combined with a deep ecosystem of middleware suppliers, supports early prototyping and large-scale deployment. The region benefits from clear FDA pathways that reduce regulatory ambiguity for medical applications. Enterprises also invest in immersive training and virtual production, reinforcing North America's leadership in the 3D motion capture market.

Asia-Pacific is projected to grow at a 15.62% CAGR between 2026 and 2031. Capital infusions such as NAVER D2SF's backing of Korean start-up MOVIN reflect rising regional interest. Major sporting events, such as EURO 2024, showcased advanced analytics pipelines that inspire domestic leagues to adopt similar tools. The manufacturing base lowers hardware costs, encouraging fast rollouts across entertainment, robotics, and healthcare. Government support for industrial digitalization further amplifies opportunity across the 3D motion capture market.

Europe posts steady gains through research-driven innovation and the integration of public health. Projects at institutions like KTH demonstrate deep camera-based rehabilitation tools compliant with strict privacy laws.GDPR shapes edge-heavy architectures, benefiting local software vendors offering on-premise analytics. Middle East and Africa and Latin America present emerging demand, primarily in sports performance and tele-medicine where motion capture bridges clinician shortages. As equipment prices fall, these regions will add incremental volume to the 3D motion capture market.

- Vicon Motion Systems Ltd.

- Leyard Optoelectronic Co. Ltd. (NaturalPoint Inc./OptiTrack)

- Motion Analysis Corporation

- Qualisys AB

- Xsens Technologies B.V.

- Codamotion - Charnwood Dynamics Ltd.

- Noraxon USA Inc.

- PhaseSpace Inc.

- Phoenix Technologies Inc.

- AIQ Synertial Ltd.

- Notch Interfaces Inc.

- Perception Neuron - Noitom Ltd.

- Rokoko Electronics ApS

- STT Systems S.L.

- Simi Reality Motion Systems GmbH

- Animazoo - Synertial Limited

- QualiSense Motion Inc.

- Perception Digital Ltd.

- Organic Motion Inc.

- AI-Driven Solesense Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rise in creation of more realistic virtual reality experiences

- 4.2.2 Increased usage of computer vision in professional sports analytics

- 4.2.3 Growing adoption in media and entertainment production pipelines

- 4.2.4 Integration with AI-driven digital human modelling for ergonomic compliance

- 4.2.5 Rapid uptake of marker-less MoCap in tele-rehabilitation and remote physiotherapy

- 4.2.6 Demand for high-fidelity motion datasets to train autonomous robots

- 4.3 Market Restraints

- 4.3.1 High upfront cost of precision 3D MoCap ecosystems

- 4.3.2 Content-owner IP and privacy concerns for large-scale motion libraries

- 4.3.3 Absence of open interchange standards limiting cross-platform workflows

- 4.3.4 Supply-chain volatility for high-speed image sensors and IMUs

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitute Products

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type

- 5.1.1 Hardware

- 5.1.1.1 Cameras

- 5.1.1.2 Sensors

- 5.1.1.3 Accessories

- 5.1.2 Software

- 5.1.3 Services

- 5.1.1 Hardware

- 5.2 By System

- 5.2.1 Optical 3D MoCap Systems

- 5.2.1.1 Active Optical

- 5.2.1.2 Passive Optical

- 5.2.2 Non-optical 3D MoCap Systems

- 5.2.2.1 Inertial

- 5.2.2.2 Electromagnetic

- 5.2.2.3 Motorized

- 5.2.1 Optical 3D MoCap Systems

- 5.3 By Capture Technology

- 5.3.1 Marker-based

- 5.3.2 Marker-less

- 5.4 By Application

- 5.4.1 Biomechanical Research and Medical

- 5.4.2 Media and Entertainment

- 5.4.3 Engineering and Industrial

- 5.4.4 Education

- 5.4.5 Other Applications

- 5.5 By Deployment Mode

- 5.5.1 On-premise

- 5.5.2 Cloud-based

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 France

- 5.6.3.3 United Kingdom

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 United Arab Emirates

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Egypt

- 5.6.5.2.3 Nigeria

- 5.6.5.2.4 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Vicon Motion Systems Ltd.

- 6.4.2 Leyard Optoelectronic Co. Ltd. (NaturalPoint Inc./OptiTrack)

- 6.4.3 Motion Analysis Corporation

- 6.4.4 Qualisys AB

- 6.4.5 Xsens Technologies B.V.

- 6.4.6 Codamotion - Charnwood Dynamics Ltd.

- 6.4.7 Noraxon USA Inc.

- 6.4.8 PhaseSpace Inc.

- 6.4.9 Phoenix Technologies Inc.

- 6.4.10 AIQ Synertial Ltd.

- 6.4.11 Notch Interfaces Inc.

- 6.4.12 Perception Neuron - Noitom Ltd.

- 6.4.13 Rokoko Electronics ApS

- 6.4.14 STT Systems S.L.

- 6.4.15 Simi Reality Motion Systems GmbH

- 6.4.16 Animazoo - Synertial Limited

- 6.4.17 QualiSense Motion Inc.

- 6.4.18 Perception Digital Ltd.

- 6.4.19 Organic Motion Inc.

- 6.4.20 AI-Driven Solesense Corp.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and unmet-need assessment

3D动作捕捉市场分析及预测(至2035年):依类型、产品、服务、技术、应用、组件、部署、最终使用者及流程划分

3D动作捕捉市场分析及预测(至2035年):依类型、产品、服务、技术、应用、组件、部署、最终使用者及流程划分 全球无标记动作捕捉市场规模、份额、趋势和成长分析报告(2026-2034)

全球无标记动作捕捉市场规模、份额、趋势和成长分析报告(2026-2034) 全矩阵撷取检测器市场:按产品类型、应用、最终用户和销售管道- 全球预测 2026-2032 年动作感测器模组市场按技术、安装类型、分销管道、安装方式、应用和最终用户产业划分-2026-2032年全球预测机器人运动轨道市场按产品类型、组件、运动类型和应用划分 - 全球预测 2026-2032

全矩阵撷取检测器市场:按产品类型、应用、最终用户和销售管道- 全球预测 2026-2032 年动作感测器模组市场按技术、安装类型、分销管道、安装方式、应用和最终用户产业划分-2026-2032年全球预测机器人运动轨道市场按产品类型、组件、运动类型和应用划分 - 全球预测 2026-2032 全球动作捕捉手套市场占有率及排名、总收入及需求预测(2025-2031年)

全球动作捕捉手套市场占有率及排名、总收入及需求预测(2025-2031年) 2032 年生物力学动作捕捉市场预测:按组件、系统类型、应用、最终用户和地区进行的全球分析

2032 年生物力学动作捕捉市场预测:按组件、系统类型、应用、最终用户和地区进行的全球分析 全球无标记动态捕捉市场

全球无标记动态捕捉市场 2025 年至 2033 年 3D 动作捕捉市场(按类型、应用、系统和地区)报告

2025 年至 2033 年 3D 动作捕捉市场(按类型、应用、系统和地区)报告 无标记动作捕捉市场,按类型、应用和地区 - 2024-2032 年行业分析、市场规模、市场份额和预测

无标记动作捕捉市场,按类型、应用和地区 - 2024-2032 年行业分析、市场规模、市场份额和预测